Perfume Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 62.66 Billion |

| Market Size (2031) | USD 91.85 Billion |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Perfume Market Analysis by Mordor Intelligence

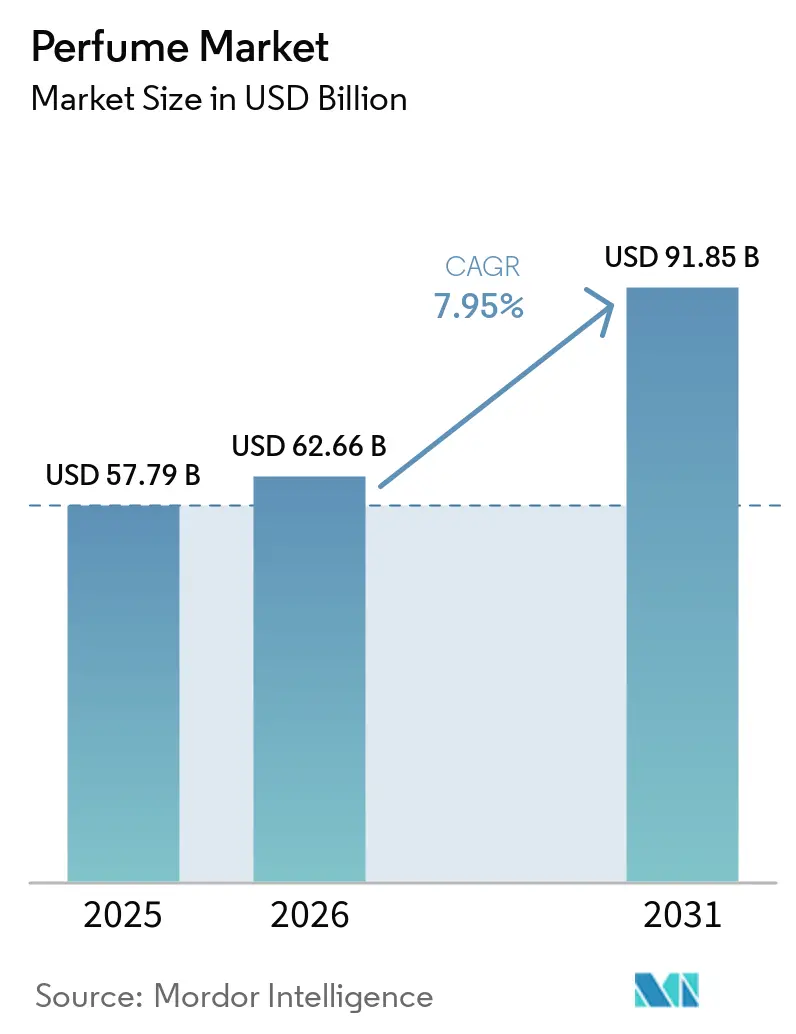

The perfume market size is expected to grow from USD 57.79 billion in 2025 to USD 62.66 billion in 2026 and is forecast to reach USD 91.85 billion by 2031 at a 7.95% CAGR over 2026-2031. The global perfume market is driven by increasing consumer interest in personal grooming, self-expression, and premium lifestyle products, particularly among younger demographics influenced by social media and celebrity endorsements. The rising demand for niche, long-lasting, and gender-inclusive fragrances, coupled with advancements in natural ingredients, sustainable packaging, and personalized scent experiences, is further contributing to market growth. Additionally, the rapid growth of e-commerce and travel retail channels has enhanced product accessibility and increased global brand visibility.

Key Report Takeaways

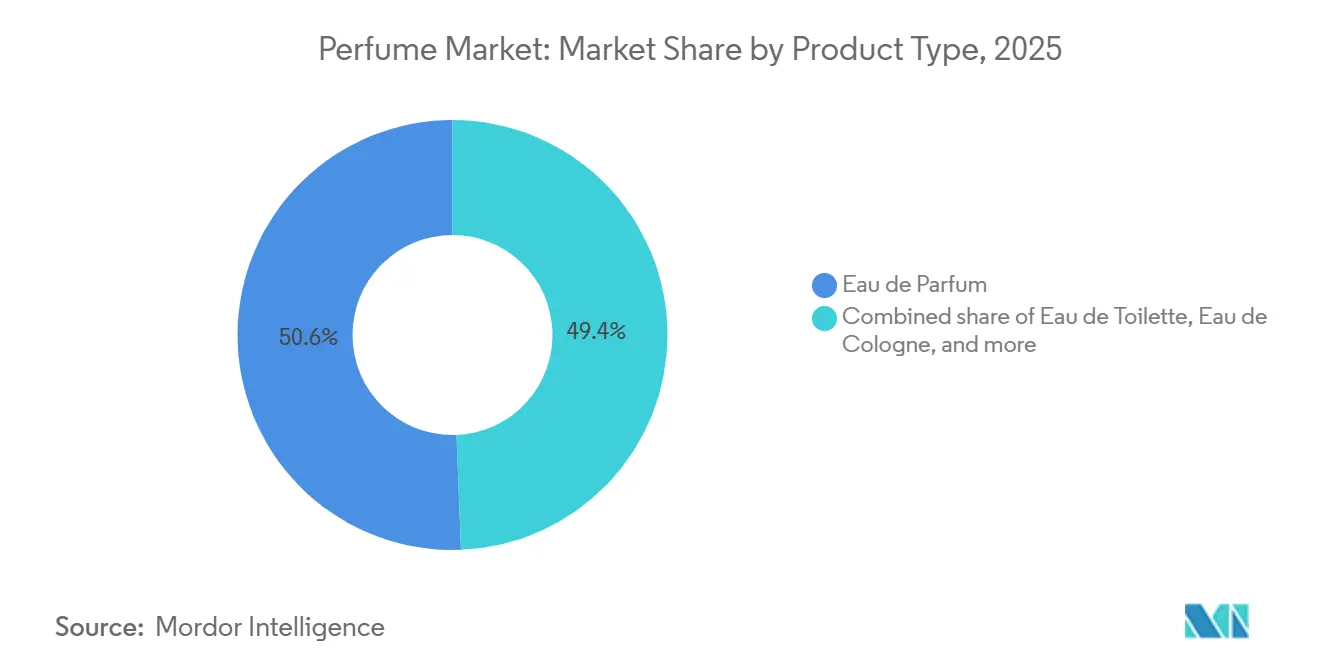

- By product type, Eau de Parfum led with 50.63% share in 2025, while Parfum/Extrait de Parfum is forecast to expand at 8.53% CAGR through 2031.

- By price tier, premium accounted for 64.05% of the perfume market size in 2025 and is projected to grow at 8.61% CAGR through 2031.

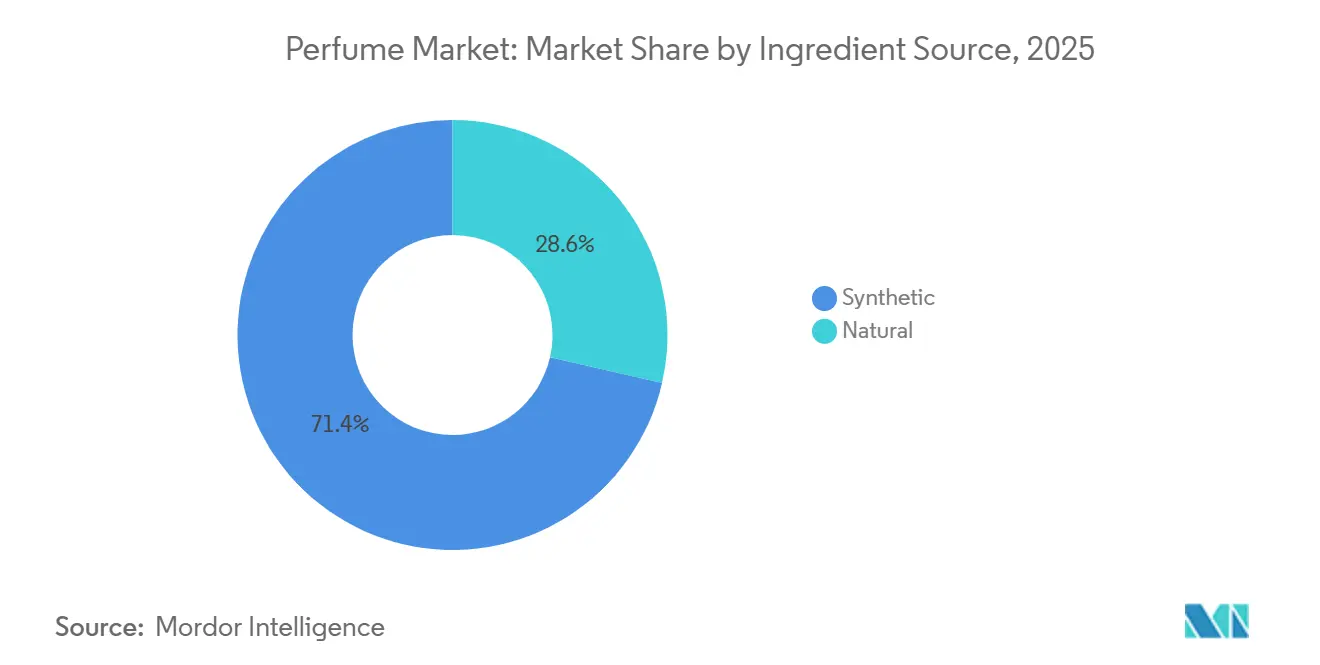

- By ingredient source, synthetic ingredients held 71.41% share in 2025, while natural ingredients are forecast to expand at 8.86% CAGR through 2031.

- By end user, women represented 53.83% share in 2025, while the unisex segment is projected to grow at 8.47% CAGR through 2031.

- By distribution channel, specialty stores held 40.68% share in 2025, while online retail stores are forecast to advance at 9.53% CAGR through 2031.

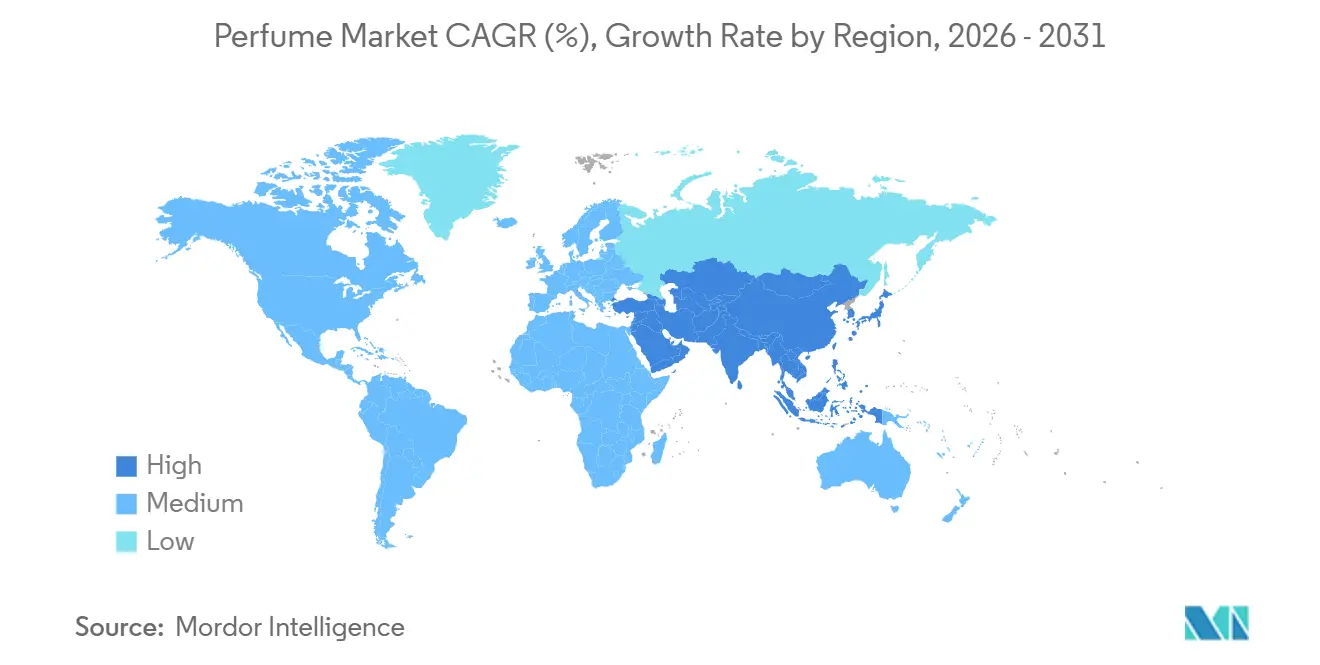

- By geography, North America held 44.83% of the perfume market share in 2025, while Asia-Pacific is forecast to grow at 8.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Perfume Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for personal grooming and self-expression | +2.0% | Global, with strongest intensity in North America and Europe | Medium term (2-4 years) |

| Growing influence of social media and beauty influencers | +1.5% | Global, particularly pronounced in North America, Asia-Pacific, and Latin America | Short term (≤ 2 years) |

| Expansion of gender-neutral and inclusive fragrance lines | +0.8% | Europe, North America, with spillover to Asia-Pacific and Latin America | Medium term (2-4 years) |

| Increasing demand for premium, niche, and artisanal fragrances | +1.8% | North America, Europe, Middle East, with growing relevance in Asia-Pacific | Long term (≥ 4 years) |

| Advancements in fragrance formulation technologies | +0.7% | Global, led by European fragrance R&D hubs | Medium term (2-4 years) |

| Rising preference for natural, clean-label, and sustainable ingredients | +0.6% | Europe, North America, with rising relevance in South Korea, Japan, and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for personal grooming and self-expression

Increasing consumer focus on personal grooming and self-expression is a key factor driving the growth of the global perfume market. Perfumes are increasingly perceived as an integral part of daily routines and personal identity. Consumers, particularly millennials and Gen Z, are using perfumes to express their personality, mood, and social image, resulting in rising demand for a variety of fragrance options, including luxury, niche, gender-neutral, and customized products. Additionally, the growing impact of social media, celebrity culture, and beauty influencers has heightened awareness of personal appearance and grooming practices, promoting frequent perfume purchases and experimentation with new fragrance collections.

Growing influence of social media and beauty influencers

The growing impact of social media and beauty influencers is significantly shaping the global perfume market by influencing consumer preferences, enhancing product awareness, and facilitating fragrance discovery among younger demographics. Platforms such as Instagram, TikTok, and YouTube serve as key channels for perfume brands to promote new product launches, luxury collections, and personalized fragrance experiences through influencer collaborations, celebrity endorsements, and trending beauty content. Consumers are increasingly guided by online reviews, tutorials, and lifestyle content, which drive interest in premium, niche, and gender-neutral fragrances. This trend is further supported by the expanding digital audience, as Eurostat reported that 89.3% of individuals aged 16–29 in the European Union used online social networks in 2025, underscoring the significant role of digital platforms in shaping fragrance purchasing decisions and fostering brand engagement[1]Source: Eurostat, "89% of 16-29-year-olds used socials in 2025," ec.europa.eu.

Expansion of gender-neutral and inclusive fragrance lines

The growth of gender-neutral and inclusive fragrance lines is becoming a significant driver in the global perfume market, as consumers increasingly prioritize individuality over traditional gender norms. Modern fragrance consumers, particularly younger demographics, are seeking versatile scents suitable for all genders. This trend is prompting perfume brands to create unisex collections featuring balanced notes such as floral, woody, citrus, and musky. For example, in March 2026, Daily Compounds introduced a new range of functional, gender-neutral fragrances in India. The collection included four fragrances: Forest 36, Desert 31, Tropics 12, and Seaside 09. These were developed in collaboration with the internationally recognized fragrance house IFF, utilizing their neuroscience-based BrainEmotions™ methodology to promote holistic wellness. This shift toward inclusivity enables companies to expand their customer base, enhance brand appeal, and align with changing social perspectives on identity and self-expression. Additionally, luxury and niche fragrance brands are increasingly adopting inclusive marketing strategies and minimalist packaging designs to cater to consumers seeking personalized and authentic fragrance experiences, further driving market growth.

The growing demand for premium, niche, and artisanal fragrances is a key driver of the global perfume market. Consumers are increasingly seeking exclusive, high-quality scents that emphasize uniqueness, sophistication, and long-lasting performance. There is a noticeable shift away from mass-produced fragrances, with buyers showing greater interest in personalized scent profiles, rare ingredients, handcrafted formulations, and luxury brand experiences. This trend is particularly evident among affluent consumers and younger demographics, who view premium fragrances as symbols of status, individuality, and self-expression. In response, luxury fashion houses and fragrance brands are expanding their high-end perfume offerings to meet this demand. For example, in September 2025, Balenciaga launched a 10-scent fine fragrance collection priced at USD 320 per bottle, marking its return to the luxury fragrance market and reflecting the increasing global interest in exclusive premium perfumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on fragrance ingredients and chemical usage | -1.2% | European Union, North America, Great Britain, with spillover to global supply chains | Short term (≤ 2 years) |

| Counterfeit and imitation products | -0.8% | Global, with highest incidence in South America, Southeast Asia, Middle East, and Eastern Europe | Medium term (2-4 years) |

| Rising consumer concerns regarding allergies and skin sensitivities | -0.6% | Europe, North America, Australia | Medium term (2-4 years) |

| Volatility in natural raw material availability | -0.5% | Global, concentrated in Asia-Pacific ingredient-origin countries and African growing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent regulations on fragrance ingredients and chemical usage

Stringent regulations on fragrance ingredients and chemical usage are significantly restraining the global perfume market. Manufacturers are under increasing pressure to ensure product safety, transparency, and compliance with regulatory requirements across various regions. Regulatory authorities are enforcing stricter rules on the use of synthetic chemicals, allergens, and potentially harmful substances in fragrance formulations. These measures lead to higher product development costs and more complex manufacturing processes. Additionally, companies must reformulate existing products, update packaging labels, and conduct extensive safety testing to meet evolving standards, posing operational and financial challenges, particularly for smaller fragrance brands. For example, EU Regulation 2023/1545 expanded Annex III of Regulation (EC) No 1223/2009, requiring the individual disclosure of 56 additional fragrance allergens on product labels when present above specified thresholds. The compliance deadline for products sold in the European Union is set for July 31, 2026[2]Source: EUR-Lex, "COMMISSION REGULATION (EU) 2023/1545 of 26 July 2023 amending Regulation (EC) No 1223/2009 of the European Parliament and of the Council as regards labelling of fragrance allergens in cosmetic products," eur-lex.europa.eu. This increasing regulatory scrutiny may restrict ingredient flexibility and delay the launch of new products in the perfume industry.

Counterfeit and imitation products

Counterfeit and imitation products pose a significant challenge to the global perfume market by adversely impacting brand reputation, consumer trust, and revenue for original fragrance manufacturers. The widespread availability of fake perfumes through unauthorized online platforms, street markets, and informal retail channels has led to an increased circulation of low-quality products that often replicate the packaging and scent profiles of premium brands. These counterfeit products not only diminish the sales of authentic perfumes but also raise safety concerns due to the potential inclusion of harmful or unregulated ingredients. Luxury and premium fragrance brands are particularly at risk, as counterfeiters frequently target high-demand products with strong market recognition. According to the European Union Intellectual Property Office, perfumes and cosmetics accounted for 3.04% of counterfeit products seized across the European Union in 2024, underscoring the ongoing issue of product imitation within the fragrance industry and its impact on market growth[3]Source: European Union Intellectual Property Office, "European Union seizes 112 million counterfeit items worth €3.8 billion in 2024," euipo.europa.e.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Concentration Formats Drive Premium Premiumization

Eau de Parfum accounted for 50.63% of the product-type market share in 2025, driven by increasing consumer preference for long-lasting yet moderately priced fragrances suitable for everyday use. With a balanced concentration of fragrance oils, Eau de Parfum provides stronger scent performance and better longevity compared to lighter variants like Eau de Toilette, making it appealing to consumers seeking value and durability. The growing influence of personal grooming trends, heightened interest in signature scents, and the expanding availability of premium and designer fragrance collections further support the popularity of Eau de Parfum products. Additionally, younger consumers are increasingly attracted to versatile fragrances that transition seamlessly between casual and formal settings, prompting brands to diversify their Eau de Parfum offerings across floral, woody, oriental, and fresh scent categories.

Parfum/Extrait de Parfum represents the fastest-growing product type, with a projected CAGR of 8.53% from 2026 to 2031. This growth is driven by rising demand for ultra-premium, luxury, and highly concentrated fragrance products that offer superior longevity and exclusivity. High-concentration perfumes are increasingly perceived as status symbols, associated with sophistication, craftsmanship, and individuality. The segment is gaining popularity among affluent consumers and fragrance enthusiasts who value richer scent profiles, extended wear time, and the use of rare or high-quality ingredients. Additionally, growing interest in artisanal perfumery, niche luxury brands, and personalized fragrance experiences is encouraging manufacturers to launch exclusive extrait collections featuring distinctive scent compositions and elegant packaging. The expansion of luxury retail channels and online premium fragrance platforms has further enhanced global accessibility to high-end parfum products.

By Price Tier: Premium Consolidates Its Lead While Masstige Accelerates

The premium price tier accounted for 64.05% of the 2025 market and is projected to achieve a CAGR of 8.61% during 2026–2031. This growth is driven by increasing consumer demand for luxury, exclusivity, and high-quality fragrance experiences. Premium perfumes are increasingly associated with personal identity, social status, and sophisticated lifestyles, prompting higher spending on designer, niche, and artisanal fragrance brands. The use of rare ingredients, superior scent longevity, elegant packaging, and personalized fragrance compositions has further enhanced the appeal of premium products among affluent consumers and younger luxury buyers. Additionally, celebrity endorsements, influencer marketing, and the expansion of luxury retail and e-commerce channels are improving brand visibility and accessibility, supporting the global growth of the premium perfume category.

The mass perfume segment in the global market is primarily driven by the rising demand for affordable and easily accessible fragrance products suitable for daily use. Consumers in urban and semi-urban regions are increasingly incorporating perfumes into their regular grooming routines, resulting in higher demand for budget-friendly options available through supermarkets, pharmacies, convenience stores, and online platforms. Mass-market perfumes are gaining traction due to their wide variety of scent profiles, attractive packaging, frequent promotional offers, and smaller pack sizes that cater to price-sensitive consumers. Furthermore, growing awareness of personal hygiene and grooming, along with the influence of social media trends and celebrity-inspired fragrances, is encouraging broader adoption of mass perfumes across various age groups and income levels.

By Ingredient Source: Synthetic Dominance Meets Natural-Facing Demand

Synthetic ingredients are projected to account for 71.41% of the ingredient source market in 2025, driven by the demand for cost-effective, durable, and highly stable fragrance formulations. These ingredients enable manufacturers to produce consistent scent profiles on a large scale while reducing reliance on seasonal or limited natural raw materials. Additionally, synthetic ingredients facilitate the creation of unique and complex fragrance notes that are challenging to obtain from natural sources, allowing brands to diversify their product offerings and meet evolving consumer preferences. Synthetic compounds also offer advantages such as enhanced longevity, stronger diffusion, and greater formulation flexibility, making them a preferred choice in both mass-market and premium fragrance segments. The emphasis on affordability, scalability, and innovation in fragrance chemistry continues to support the global growth of synthetic ingredient-based perfumes.

Natural ingredients are expected to grow at a CAGR of 8.86% from 2026 to 2031, fueled by increasing consumer preference for clean-label, sustainable, and plant-based personal care products. Consumers are showing a growing interest in perfumes formulated with essential oils, botanical extracts, and naturally derived ingredients due to concerns about synthetic chemicals, skin sensitivities, and environmental impact. The rising demand for organic and eco-conscious beauty products has prompted fragrance brands to focus on transparent ingredient sourcing, cruelty-free claims, and environmentally friendly packaging. Furthermore, the popularity of wellness-focused lifestyles and aromatherapy-inspired fragrances has heightened interest in natural perfumes, which are perceived as safer, more authentic, and luxurious. Premium and niche fragrance brands are leveraging natural ingredients to appeal to consumers seeking artisanal and sustainable scent experiences.

By End User: Women's Segment Anchors Revenue as Unisex Redefines Growth

Women accounted for 53.83% of the end-user market in 2025, driven by a growing focus on personal grooming, beauty enhancement, and self-expression through fragrance products. Perfumes have become an integral part of daily lifestyle and fashion routines for female consumers, leading to increased demand for diverse scent categories such as floral, fruity, oriental, and fresh fragrances. The influence of celebrity endorsements, beauty influencers, luxury branding, and social media trends has further boosted interest in premium and personalized perfumes among women. Additionally, ongoing product innovations, including long-lasting formulations, elegant packaging, and limited-edition collections, are fostering repeat purchases and brand loyalty. The expanding availability of perfumes through online platforms, specialty beauty stores, and luxury retail outlets is also driving the global growth of the women’s fragrance segment.

The unisex segment is projected to grow at a CAGR of 8.47% from 2026 to 2031, fueled by evolving consumer attitudes toward gender identity, inclusivity, and individuality in personal care products. Millennials and Gen Z consumers are increasingly favoring fragrances that transcend traditional gender classifications, prompting brands to develop versatile scent profiles suitable for all users. Unisex perfumes typically feature balanced notes such as citrus, woody, musky, aquatic, and herbal accords, appealing to those seeking minimalist and modern fragrance experiences. The rising popularity of niche and artisanal perfume brands, coupled with the influence of social media and contemporary fashion trends, has further driven demand for gender-neutral fragrances. Inclusive marketing campaigns and growing acceptance of self-expression through non-traditional beauty products are also contributing to the rapid expansion of the unisex perfume category globally.

By Distribution Channel: Specialty Retail Leads, Online Accelerates

Specialty stores accounted for 40.68% of the distribution channel market in 2025, driven by increasing consumer preference for personalized shopping experiences, expert product guidance, and access to premium fragrance collections. These stores enable customers to physically test and compare scents before purchasing, a critical factor in the fragrance industry where scent perception significantly influences buying decisions. Specialty stores often feature curated selections of luxury, niche, and designer perfumes, supported by trained beauty consultants who assist consumers in selecting fragrances based on personal preferences and lifestyle needs. Additionally, features such as attractive in-store displays, exclusive product launches, gift packaging services, and premium brand experiences enhance customer engagement and encourage higher-value purchases. The growing popularity of experiential retail and the demand for authentic branded products further bolster perfume sales through specialty retail channels globally.

Online retail stores are the fastest-growing distribution channel, with a CAGR of 9.53% projected for 2026–2031. This growth is driven by the rapid expansion of e-commerce platforms, increased smartphone usage, and shifting consumer preferences toward convenience and digital accessibility. Online channels provide consumers with the ability to explore a wide range of fragrance brands, compare prices, read customer reviews, and access exclusive online discounts and product launches from their homes. The influence of social media marketing, beauty influencers, and targeted digital advertising has further strengthened online perfume purchasing behavior, particularly among younger consumers. Moreover, advancements in virtual fragrance discovery tools, sample subscription services, and personalized product recommendations are helping to address consumer hesitation about buying perfumes online. The growth of direct-to-consumer brand websites and the availability of fast delivery services are also contributing to the continued expansion of perfume sales through online retail channels worldwide.

Geography Analysis

North America accounted for 44.83% of the 2025 perfume market, driven by strong consumer awareness of personal grooming, high demand for premium and luxury fragrances, and the growing influence of celebrity and influencer-driven beauty trends. Consumers in this region increasingly prefer long-lasting, niche, and personalized fragrances that align with their lifestyle and individuality, prompting continuous product innovation among global and regional perfume brands. The expansion of e-commerce platforms, subscription-based fragrance services, and direct-to-consumer marketing strategies has enhanced accessibility and product discovery in the United States and Canada. Additionally, the rising interest in clean-label, sustainable, and gender-neutral fragrances is fueling the growth of premium and artisanal perfume segments in the North American market.

The Asia-Pacific perfume market is projected to grow at a CAGR of 8.58% during 2026–2031, supported by rapid urbanization, evolving beauty and grooming trends, and increasing consumer exposure to international lifestyle influences through social media and digital platforms. Younger consumers in countries such as China, India, Japan, and South Korea are incorporating perfumes into their daily personal care routines, driving demand for both affordable and premium fragrance products. The strong presence of online retail channels, the growing popularity of K-beauty and luxury beauty products, and the expansion of international fragrance brands in emerging economies are further boosting market growth. Moreover, rising interest in natural ingredients, innovative fragrance formats, and the gifting culture during festivals and celebrations is contributing to increased perfume sales across the region.

The perfume markets in Europe, South America, and the Middle East and Africa are influenced by diverse cultural preferences, strong fragrance traditions, and growing consumer interest in personal grooming and luxury beauty products. Europe remains a key hub for premium and artisanal perfumery, supported by its long-established fragrance heritage, high demand for designer scents, and ongoing innovation in sustainable and niche perfumes. In South America, rising beauty consciousness, expanding retail accessibility, and strong consumer preference for affordable daily-use fragrances are driving market growth. Meanwhile, the Middle East and Africa region is experiencing increased demand for rich, long-lasting oriental and oud-based perfumes, shaped by cultural fragrance traditions and growing luxury consumption. The expansion of international perfume brands, duty-free retail, and digital commerce platforms in these regions is further contributing to the global growth of perfume sales.

Competitive Landscape

The global perfume market exhibits a moderately consolidated competitive environment, with a few multinational beauty and luxury conglomerates dominating a significant portion of the prestige fragrance segment. These companies leverage extensive brand licensing agreements, large-scale distribution networks, and premium product portfolios to maintain their market position. Simultaneously, independent and niche fragrance brands are gaining momentum by emphasizing exclusivity, artisanal craftsmanship, unique scent compositions, and culturally inspired narratives. Competition in the industry is increasingly influenced by innovation in fragrance concentration formats, premiumization strategies, and expansion into high-growth luxury categories.

Competitive strategies vary significantly between large-scale market participants and emerging niche players. Major fragrance groups focus on acquisitions, long-term licensing agreements, and portfolio expansion to strengthen their foothold in the luxury and ultra-premium perfume segments. In contrast, smaller brands prioritize selective retail placement, higher fragrance oil concentrations, and unique consumer experiences to differentiate themselves. The market is also experiencing ongoing consolidation as companies pursue mergers, strategic alliances, and extended licensing partnerships to ensure long-term revenue stability and enhance global market positioning.

Technology and personalization are emerging as critical competitive differentiators in the perfume market. Companies are incorporating artificial intelligence and digital recommendation tools into both online and offline retail environments to enhance fragrance discovery, improve customer engagement, and provide personalized scent recommendations. AI-powered beauty advisors, smart fragrance matching platforms, and data-driven marketing strategies are transforming consumer interactions with perfume brands across various retail channels. Additionally, emerging companies specializing in biotechnology, precision fermentation, and bio-based aroma ingredients are introducing sustainable alternatives to traditional perfume components. These innovations are driving environmentally conscious fragrance development and creating new competitive pressures within the fragrance supply chain.

Perfume Industry Leaders

-

The Estée Lauder Companies Inc.

-

L'Oréal Groupe

-

Coty Inc.

-

Chanel Limited

-

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: L'Oréal introduced the Maison Margiela Scentsorium Collection, a luxury line comprising six scents priced at USD 350 per 75 ml. This launch represents the group's third haute couture fragrance platform, alongside Valentino's Anatomy of Dreams and Armani/Privé.

- March 2026: Daily Compounds introduced a new range of functional, gender-neutral fragrances in India. The collection included four fragrances: Forest 36, Desert 31, Tropics 12, and Seaside 09. These were developed in collaboration with the internationally recognized fragrance house IFF, utilizing their neuroscience-based BrainEmotions™ methodology to promote holistic wellness.

- November 2025: Mäurer & Wirtz finalized the acquisition of Classic Parfums and The Nose Behind, which distribute brands such as Xerjoff, Casamorati, and Pana Dora & Co.

Global Perfume Market Report Scope

| Parfum / Extrait de Parfum |

| Eau de Parfum |

| Eau de Toilette |

| Eau de Cologne |

| Others |

| Mass |

| Premium |

| Natural |

| Synthetic |

| Women |

| Men |

| Unisex |

| Supermarkets and Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Parfum / Extrait de Parfum | |

| Eau de Parfum | ||

| Eau de Toilette | ||

| Eau de Cologne | ||

| Others | ||

| By Price Tier | Mass | |

| Premium | ||

| By Ingredient Source | Natural | |

| Synthetic | ||

| By End User | Women | |

| Men | ||

| Unisex | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the perfume market by 2031?

The perfume market is forecast to reach USD 91.85 billion by 2031, rising from USD 62.66 billion in 2026 at an 7.95% CAGR over 2026 to 2031.

Which product type leads global fragrance demand?

Eau de Parfum led with 50.63% share in 2025 because it balances premium positioning, wear time, and relative affordability better than most other concentration formats.

Which price tier is expanding the fastest in perfumes?

Premium is both the largest and the fastest-growing price tier, with 64.05% share in 2025 and an expected 8.61% CAGR through 2031.

Why is Asia-Pacific important for future fragrance growth?

Asia-Pacific is expected to grow at 8.58% CAGR through 2031 because several markets still have low fragrance penetration and rising middle-class spending is widening demand.

Page last updated on: