Scented Candles Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

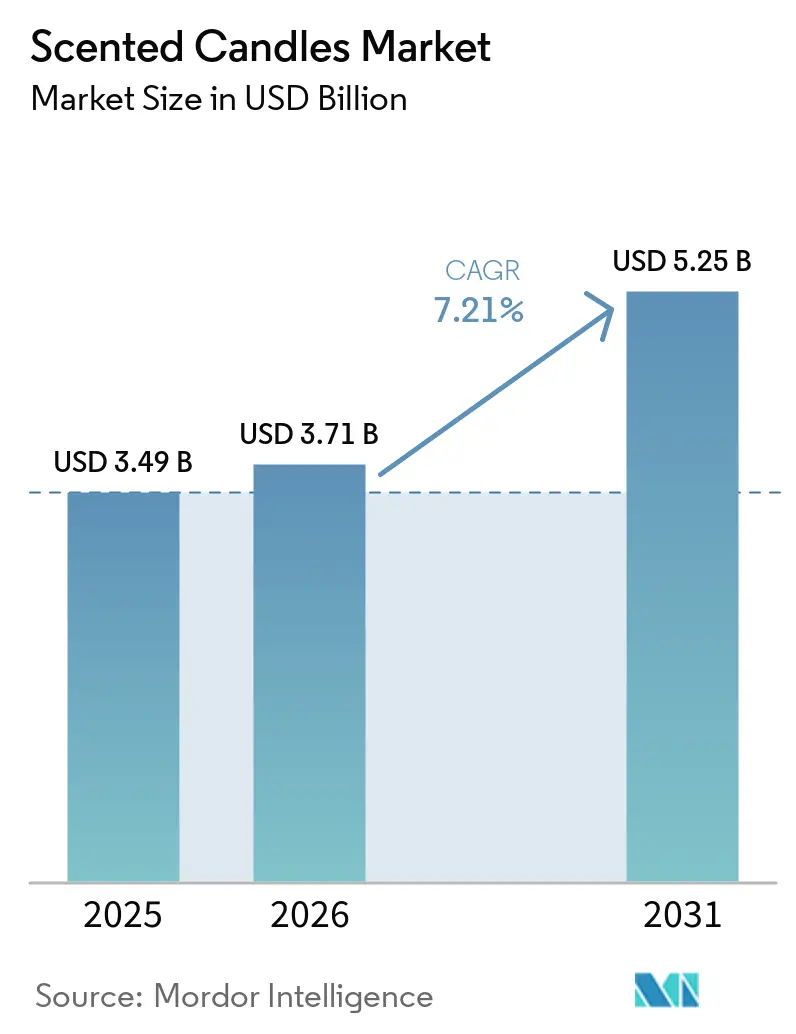

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 5.25 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

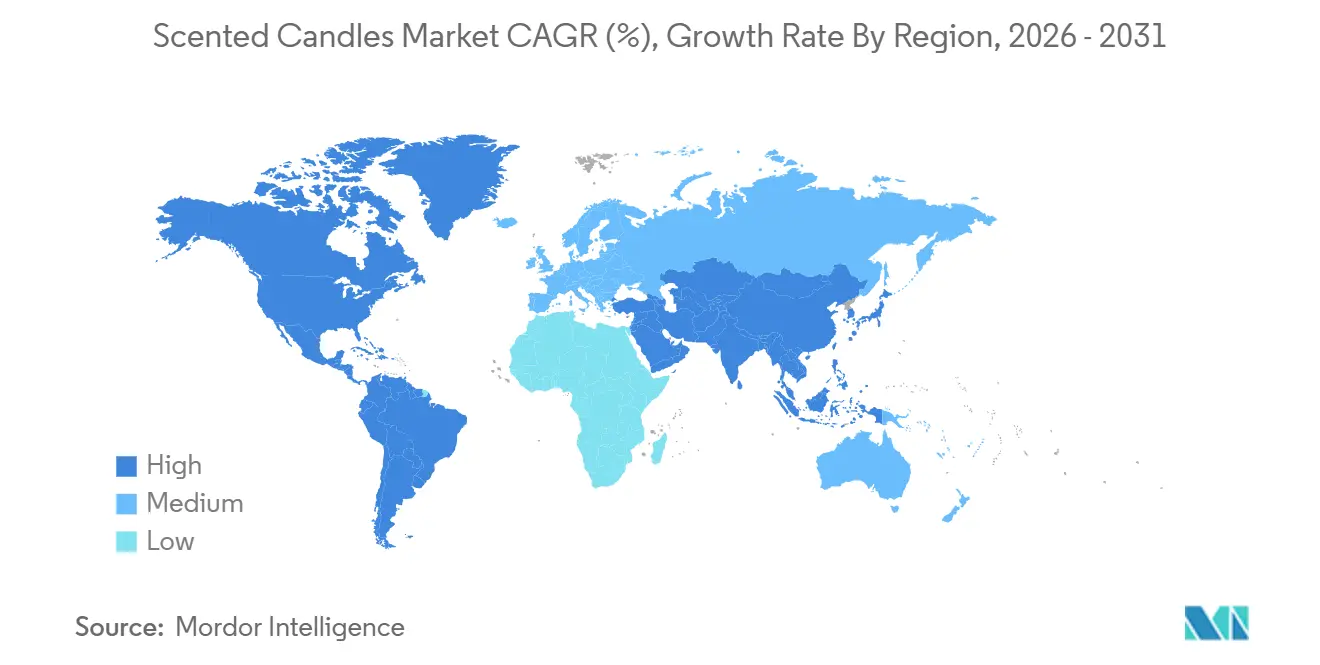

| Fastest Growing Market | South America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Scented Candles Market Analysis by Mordor Intelligence

The scented candles market size was valued at USD 3.49 billion in 2025 and is estimated to grow from USD 3.71 billion in 2026 to reach USD 5.25 billion by 2031, at a CAGR of 7.21% during the forecast period 2026-2031. The scented candles market is benefiting from a durable shift in household spending, where fragrance is now tied more closely to daily living, mood setting, and personal identity than to occasional gifting alone. Growth is also being supported by a wider mix of retail touchpoints, with large store networks sustaining volume while digital channels improve discovery and repeat purchase for newer brands. The scented candles market is becoming harder for smaller suppliers to enter at scale because product safety, ingredient disclosure, and fragrance compliance standards are lifting testing and labeling requirements across major regions. Competition is staying active because established players are reinvesting in product renewal, channel expansion, and seasonal launches, while premium labels are using cleaner formulations and stronger brand stories to defend higher price points. The scented candles market also shows selective resilience because any macroeconomic slowdown is likely to pressure premium and discretionary purchases first, while everyday home fragrance demand in mass formats remains more stable.

Key Report Takeaways

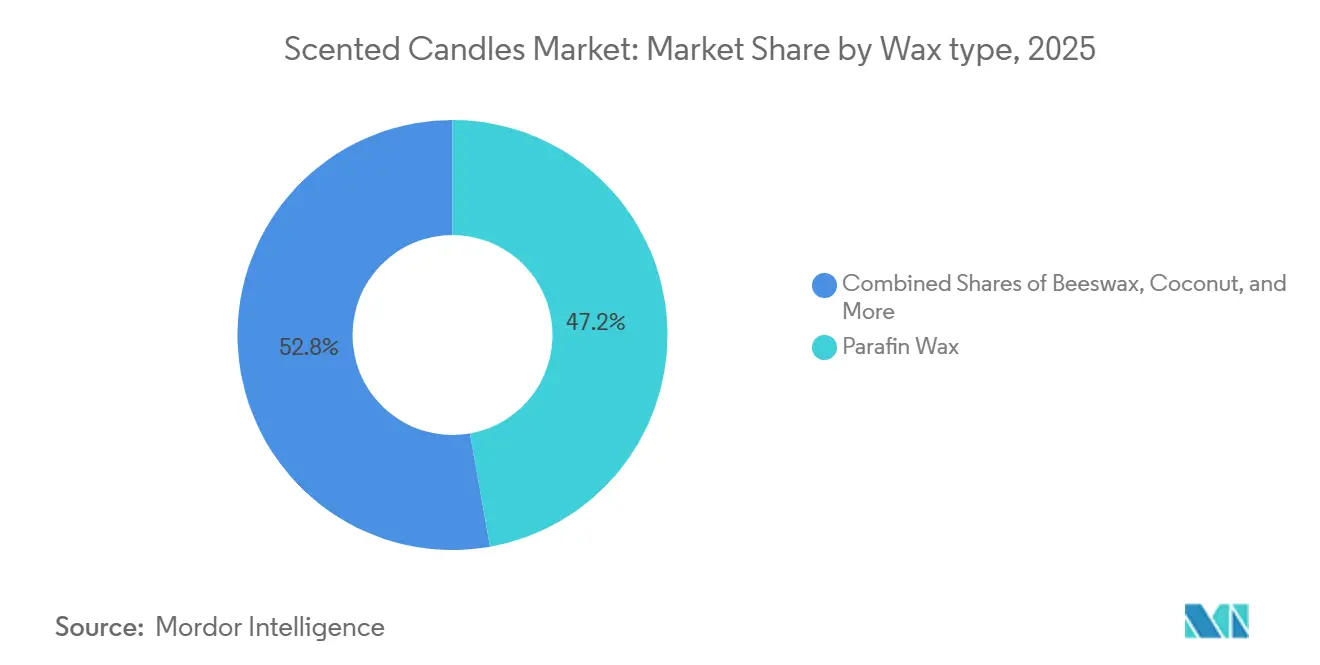

- By wax type, paraffin wax held 47.21% of the scented candles market share in 2025, while beeswax is projected to expand at a 7.24% CAGR through 2031.

- By category, mass accounted for 83.45% of the scented candles market size in 2025, while premium is forecast to grow at a 7.37% CAGR through 2031.

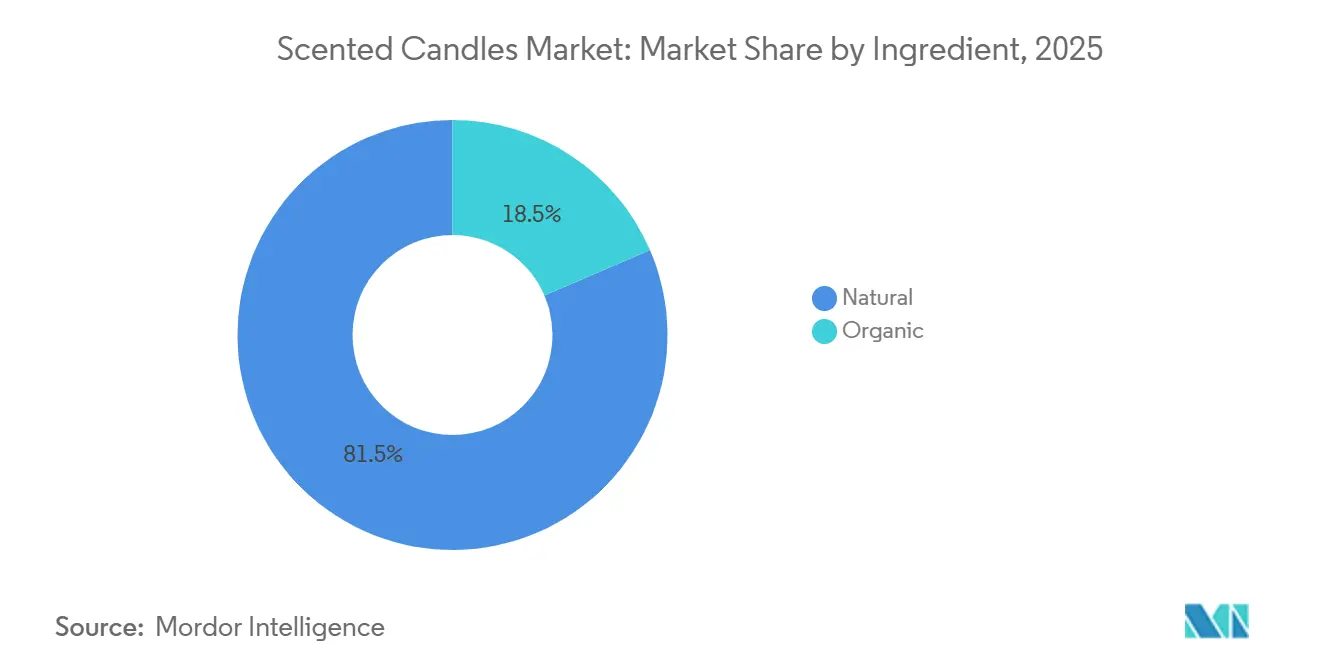

- By ingredient, natural formulations led with 81.46% share of the scented candles market size in 2025, while organic recorded the highest projected CAGR at 7.45% through 2031.

- By distribution channel, supermarkets and hypermarkets captured 43.25% of the scented candles market share in 2025, while online retail stores are advancing at a 7.77% CAGR through 2031.

- By geography, North America held 34.86% of the scented candles market size in 2025, while South America is set to record the fastest regional CAGR of 7.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Scented Candles Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Home Fragrance Trend | +1.8% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Rising Wellness and Self-Care Culture | +1.5% | North America & Europe; spill-over to APAC | Long term (≥ 4 years) |

| Seasonal and Festive Demand for Scented Candles | +0.9% | Global; peak impact in North America & Europe Q4 | Short term (≤ 2 years) |

| Demand for Premium Home Décor Products | +1.0% | North America, Europe; emerging in APAC | Medium term (2-4 years) |

| Rising Preference for Natural and Organic Products | +0.8% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Influence of Social Media and Lifestyle Marketing | +0.7% | Global; concentrated in North America, APAC, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Home Fragrance Trend

The scented candles market has moved beyond a narrow décor niche and is now tied to everyday household fragrance use in many mature consumer markets, owing to the rising disposable income. According to the Office for National Statistics data from 2024, the average annual disposable income around the age of 55-65 was GBP 49,173[1]Source: Office for National Statistics, " Average annual disposable income in the United Kingdom, By Age Group", ons.gov.uk. This shift matters because it supports more regular repurchase behavior rather than limiting demand to holiday gifting or one-time discretionary spending. Large branded players continue to treat home fragrance as a core category, which shows that candles remain important inside broader fragrance and body-care portfolios. The scented candles market also benefits from its ability to fit both low-ticket impulse purchases and planned lifestyle purchases, which gives brands multiple entry points across store and online settings. As adoption deepens in newer urban markets, the category is likely to gain further support from localized scent profiles, repeat purchases, and stronger household familiarity.

Rising Wellness and Self-Care Culture

Scented candles have migrated into functional wellness routines, occupying a role previously reserved for spa settings and professional therapies. The association between ambient fragrance and stress modulation has driven brands to extend scent portfolios across adjacent categories: Voluspa, whose revenue grew nearly 60% over five years, launched a seven-scent eau de parfum collection in June 2025, explicitly positioning fine fragrance as an extension of its home wellness brand identity. The second-order shift carries category-level consequences: as candles transition from gift items into daily self-care rituals, repurchase cycles shorten, and basket sizes expand as consumers layer complementary formats, diffusers, room sprays, and wax melts into the same sensory routine. German consumer trend coverage from autumn 2025 documented a consumer pivot away from overpowering seasonal scents toward nuanced, therapeutic fragrance profiles, lightly smoky cedarwood, amber, and gourmand accords, reflecting a preference for candles that actively support stress relief rather than simply mark a season[2]Source: Stern.de. "Duftkerzen-Trends 2025: Diese Varianten liegen im Herbst im Trend." stern.de. Brands that anchor their scented candle lines within evidence-based wellness positioning, citing aromatherapy properties or partnering with wellness platforms, are more likely to command premium pricing and retain customers than those relying on aesthetic appeal alone.

Rising Preference for Natural and Organic Products

Consumer migration away from paraffin-based products toward vegetable wax formulations is no longer an emerging preference; it is a mainstream demand signal reshaping raw material procurement strategies across the industry. Sebrae-SP data from early 2026 shows that micro-entrepreneurs in Brazil's scented candle segment in São Paulo state grew 195.6% in five years, from 570 entities in 2021 to 1,685 in 2025, with consumer demand for coconut wax and natural aromatherapy candles cited as the primary catalyst. A less-discussed consequence is occurring in Europe: Germany's Deutsche Umwelthilfe formally demanded in November 2025 that mandatory ingredient labeling be extended to all candles, creating pressure for brands to proactively disclose wax composition and fragrance sourcing ahead of any formal legislative action. Suppliers that secure USDA Organic, IFRA-compliance, or vegan certifications can differentiate meaningfully in both retail and e-commerce channels, and consumer willingness to pay a 20-40% premium for certified natural formulations is documented across both French and Brazilian consumer surveys.

Influence of Social Media and Lifestyle Marketing

Social commerce has become a direct acquisition channel for home fragrance candle brands, compressing the path from discovery to purchase for a visually driven product category. Voluspa's e-commerce business grew 180% over five years, supported by a deliberate social media and creator content strategy. The brand used TikTok Shop as a launch partner for its fine fragrance extension in June 2025. The underappreciated dimension of social media's role is qualitative: platforms do not merely expose consumers to new brands, they manufacture the need for specific scent experiences by embedding candles into curated lifestyle moments, from reading rituals to yoga practices to dinner table settings. Voluspa's collaboration with Universal Pictures on Wicked: For Good in October 2025, producing two film-inspired limited-edition candle and diffuser sets, demonstrates a broader trend toward culturally resonant IP partnerships that generate earned media beyond traditional promotional budgets. For marketing strategists, the insight with the highest forward relevance is that user-generated content and creator endorsements consistently outperform static advertising in home fragrance, particularly among consumers aged 25-40, who drive the premium and organic sub-segments.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Substitute Products | -0.8% | Global | Long term (≥ 4 years) |

| Environmental Concerns Regarding Use of Paraffin Wax | -0.7% | Europe (strictest enforcement); North America | Medium term (2-4 years) |

| Regulatory Compliance Challenges | -0.5% | EU, UK, US | Medium term (2-4 years) |

| Sensitivity to Economic Downturns | -0.6% | Global; pronounced in MEA and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns Regarding Use of Paraffin Wax

Research published in Environmental Science and Technology Letters in February 2025 confirmed that even flame-free alternatives such as scented wax melts generate indoor atmospheric nanoparticle concentrations comparable to combustion-based candles, indicating that the broader category carries indoor air quality risk, not paraffin alone. A less-discussed consequence is the regulatory acceleration this research is catalyzing: Germany's environmental advocacy organizations formally called for mandatory ingredient labeling on all candles and the extension of EU deforestation regulations to palm oil-based wax blends in late 2025, which would significantly expand compliance costs for brands mixing paraffin with palm derivatives. Manufacturers reliant on paraffin face a dual squeeze: rising consumer rejection in premium and mid-premium tiers, and a tightening EU regulatory perimeter under CLP Regulation 1272/2008 and REACH (EC 1907/2006) that is progressively raising labeling and traceability requirements. Brands that have proactively transitioned to certified natural wax formulations are positioned to capture the consumer base being pushed out of paraffin products, provided they can demonstrate certification credibility beyond marketing claims.

Availability of Substitute Products

The scented candles market competes with a widening range of ambient fragrance alternatives, including reed diffusers, electric ultrasonic diffusers, wax melts, room sprays, and emerging smart scent devices. Established brands are preemptively managing this substitution risk by offering identical fragrance collections across multiple product formats: LAFCO New York's product range spans 3-wick candles, signature candles, classic candles, and reed diffusers within the same fragrance identity, allowing consumers to self-select format without shifting brand loyalty. The strategic risk concentrates most acutely in the mid-market: premium consumers tend to combine candles with diffusers as a multi-format ritual, retaining candles for their aesthetic and ritualistic value, while mass-market consumers are more price-sensitive and likelier to substitute on functional grounds. An insight from recent peer-reviewed research adds nuance here: a study published in Environmental Science and Technology Letters in February 2025 found that scented wax melts produce indoor nanoparticle concentrations equivalent to combustion candles, challenging the premise that flame-free formats represent a materially safer alternative and potentially moderating consumer migration to wax melts if this evidence reaches mainstream awareness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wax Type: Natural Alternatives Pressure Paraffin Incumbency

Paraffin wax accounted for 47.21% of the scented candles market by wax type in 2025, while beeswax is projected to record the fastest growth at a 7.24% CAGR through 2031. Paraffin kept its lead because it still benefits from familiar manufacturing economics, broad supply availability, and price points that fit mass retail and promotional formats. That advantage remains strongest in supermarket and everyday-use channels where affordability shapes purchase behavior more than ingredient purity. Beeswax is growing faster because it is associated with cleaner burn performance, longer use time, and a more premium natural image. Coconut and other blends are also gaining traction because they give brands flexibility to balance fragrance throw, texture, and clean-label positioning without relying fully on one wax input.

Wax type has become a visible quality signal in the scented candles industry rather than just a technical formulation choice. Consumers increasingly connect wax origin with burn experience, soot levels, sustainability, and even the credibility of a brand’s broader wellness claims. That shift favors suppliers that can explain why a wax system was chosen and how it supports both performance and transparency. It also gives premium and direct-to-consumer brands more room to justify higher pricing, especially when the wax narrative is tied to vessel reuse, refillability, or responsible sourcing. The scented candles market is therefore likely to keep paraffin strong in volume terms while steadily shifting premium growth toward beeswax and blended natural alternatives.

By Category: Premium Momentum Tests Mass Market Volume Lead

Mass held 83.45% of revenue in 2025, which shows how strongly the scented candles market still depends on high-volume everyday purchasing. This segment remains anchored in supermarkets, hypermarkets, big-box stores, and established specialty chains that can move large seasonal and promotional volumes. Its scale reflects the routine role of home fragrance in household spending, where shoppers often buy candles alongside broader basket needs rather than as a standalone luxury purchase. Bath & Body Works continued to invest in marketplace expansion and broader brand renewal in 2026, which supports the view that large-format accessible price points remain central to volume defense in the category. The mass base also benefits from stronger visibility during fourth-quarter shopping periods, when gifting and seasonal décor can quickly lift unit movement.

Premium is the faster-growing segment with a 7.37% CAGR through 2031, which shows that trading up remains active even as mass keeps the largest revenue base. Consumers are not treating these categories as direct substitutes in every case because many households buy accessible candles for routine use and reserve premium formats for gifting, occasions, or personal indulgence. That makes the segmentation less about replacement and more about layered consumption within one annual spend pattern. In the scented candles market, premium labels gain when they combine distinctive scent curation, elevated packaging, and cleaner formulation language in a way that feels consistent across product and brand identity. The result is a category structure where mass protects scale while premium shapes margins, brand aspiration, and innovation speed.

By Ingredient: Natural Formulations Mainstream, Organic Growth Accelerates

Natural ingredients commanded 81.46% of the ingredient segment in 2025, confirming that the scented candles market has moved clean-label positioning well beyond a small niche. Natural now functions as a basic expectation in many premium and mid-premium offers, especially where consumers can easily compare product pages and ingredient descriptions online. This change is greatest in urban markets where transparency, sustainability, and indoor air quality are closely tied to purchase choices. It also supports new brand entry because ingredient language gives smaller suppliers a clear path to differentiation when they cannot match larger rivals on store count or advertising scale. In the scented candles market, natural positioning is increasingly tied to broader brand trust rather than to a single wax or fragrance claim in isolation.

Organic ingredients are forecast to grow at a 7.45% CAGR through 2031, which shows that the next stage of demand is moving from general natural language toward verifiable certification and sourcing proof. Buyers who already prefer plant-based or cleaner products are now more likely to look for evidence that those claims stand up under closer review. This makes certification, supplier traceability, and compliance language more valuable in digital channels where consumers rely on written product detail instead of in-store scent testing. LAFCO’s recent product communication around soy wax blends, essential oil-based fragrance, and materials such as cotton wicks shows how premium brands are using detailed ingredient presentation to support trust and product differentiation. The scented candles industry is therefore likely to reward brands that can move from vague natural claims to clearer and more auditable ingredient stories.

By Distribution Channel: Supermarkets Anchor Volume, Online Channels Accelerate

Supermarkets and hypermarkets held 43.25% of channel share in 2025, which kept them at the center of the scented candles market from a volume perspective. These outlets benefit from heavy foot traffic, impulse purchase patterns, and seasonal displays that make candles highly visible during gift-driven and décor-led shopping periods. They also support accessible pricing, multi-buy offers, and quick replenishment, which is why mass brands continue to rely on them for scale. Specialty stores remain important as well because they help premium and artisan suppliers present candles in a more curated environment where vessel design, scent identity, and gifting value are easier to communicate. Other distribution channels, including hospitality and bespoke gifting, add useful revenue streams even if they do not match mainstream retail on unit volume.

Online retail stores are the fastest-growing channel and are projected to expand at a 7.77% CAGR through 2031, reflecting the way the scented candles market is shifting toward search-led discovery and repeat digital purchasing. This channel lowers entry barriers for challenger brands because national reach no longer depends entirely on physical shelf access. It also gives established players another path to defend relevance with younger consumers who move between brand sites, marketplaces, and social commerce during one purchase journey. Bath & Body Works highlighted its earlier-than-planned Amazon launch in February 2026 as part of its multi-year transformation strategy, which shows that even major specialty retailers now see third-party digital presence as important to future growth. The scented candles industry is likely to see the strongest competitive pressure where online reach, creator-led discovery, and strong repeat purchase economics intersect.

Geography Analysis

North America retained the largest share of the scented candles market at 34.86% in 2025, and the region also represented the largest scented candles market share because of mature retail infrastructure, deep household penetration, and strong consumer familiarity with home fragrance routines. The United States remains the clear regional anchor because it combines large store networks, strong brand recognition, and consistent seasonal demand. Newell Brands reported that Yankee Candle U.S. core sales grew 6% in the fourth quarter of 2025 after a full brand relaunch, and the company plans to take that relaunch into Europe in 2026, which reinforces North America’s role as a testing ground for branded innovation[3]Source: Newell Brands, “Newell Brands Announces Fourth Quarter and Full Year 2025 Results,” newwellbrands.com. Canada and Mexico remain smaller but meaningful adjacency markets, where brand extension and rising online availability continue to widen category reach. Europe followed as the second-largest geographic block, supported by a developed premium and artisan base, stricter ingredient expectations, and steady demand for both local and imported candle offerings.

Asia-Pacific remains one of the more structurally underserved opportunities in the scented candles market over the medium term. China leads regional growth because urban middle-class households are spending more on décor-led lifestyle products and premium fragrance formats. South Korea stands out for its fragrance-aware consumer base, where premium scent adoption across several formats creates a receptive environment for high-end candle propositions. India, Vietnam, Thailand, Indonesia, and Singapore are also expanding their role as urban incomes and e-commerce access improve product availability across the region. Japan and Australia remain more mature sub-markets where premium positioning and specialty retail have already built a stable demand base.

South America is the fastest-growing region in the scented candles market, with a forecast CAGR of 7.95% during 2026-2031. Brazil is the main regional driver because urbanization, self-care spending, and interest in natural wax formats are lifting both consumer demand and small-scale brand activity. Colombia, Chile, and Peru add to this momentum as middle-income households increase spending on home-oriented discretionary products. The Middle East and Africa region is still at an earlier stage of adoption, but the United Arab Emirates and Saudi Arabia offer clear premium potential, while South Africa, Nigeria, Morocco, Egypt, and Turkey form the main urban demand nodes for future expansion.

Competitive Landscape

The scented candles market is moderately fragmented, with many regional producers and a broad mix of branded global participants. No single company holds a dominant position, which keeps pricing, seasonal launches, and channel access central to competition. Large players are leaning on store networks, digital expansion, and brand reinvestment to protect volume and defend customer retention. Premium and niche operators are focusing more on design, ingredient language, and lifestyle positioning so they can protect higher price points without matching the physical reach of mass players. This split keeps the scented candles market active across both value-led and aspiration-led demand pools.

Bath & Body Works reported fiscal 2025 net sales of USD 7.3 billion and stated that its multi-year Consumer First Formula includes marketplace expansion, product innovation, and brand elevation, with USD 175 million in fiscal 2026 cost savings expected to be reinvested into growth initiatives. That approach shows how major scale operators are using cost discipline to fund faster product renewal rather than relying only on legacy brand awareness. Newell Brands also reported that Yankee Candle U.S. core sales grew 6% in the fourth quarter of 2025 after a full relaunch, and it plans to extend that effort to Europe in 2026 while also relaunching WoodWick and Chesapeake Bay. These moves indicate that the scented candles market now rewards continuous portfolio refresh more than passive shelf presence.

Smaller premium brands are responding with faster seasonal curation, stronger material storytelling, and tighter visual identity. LAFCO’s recent introductions, including Saffron Sandalwood, Pumpkin Seed & Sandalwood, and the Tomato Season Collection, show how premium suppliers use frequent launches, glass design, and detailed ingredient presentation to keep attention high without competing directly on mass pricing. The next competitive white space is likely to stay concentrated in refillable formats, cleaner wax systems, and digital customer acquisition models that improve repeat buying economics. Brands that cannot support fast launch cycles, credible ingredient communication, and flexible channel strategy will find it harder to sustain visibility in the scented candles market after 2026.

Scented Candles Industry Leaders

-

Newell Brands

-

Dyptique

-

Estée Lauder Companies

-

Bath & Body Works

-

Bolsius

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SEVA Home launched ELEMENTAL, a luxury candle collection inspired by Earth, Water, Fire, Air, and Space, designed to combine fragrance with emotional storytelling and artisanal craftsmanship.

- November 2025: Maison Monravel launched its first scented candle collection with a wellness-led positioning, framing the fragrances as “olfactory remedies” inspired by the restorative properties of plants. The debut line includes six scents such as Citrus Maxima and Sancta Myrrha, and the brand plans to sell them online and through a limited pop-up at Le Bon Marché in Paris.

- November 2025: Liberty Beauty has introduced a scented candle collection that turns its signature patterns into home fragrance, with each scent matched to a decorated reusable glass vessel. The launch emphasizes design-led, premium home fragrance.

Global Scented Candles Market Report Scope

| Paraffin Wax |

| Beeswax |

| Coconut & Other Blends |

| Mass |

| Premium |

| Natural |

| Organic |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Thailand | |

| Singapore | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Wax Type | Paraffin Wax | |

| Beeswax | ||

| Coconut & Other Blends | ||

| By Category | Mass | |

| Premium | ||

| By Ingredient | Natural | |

| Organic | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the scented candles space in 2026 and where is it headed by 2031?

It stands at USD 3.71 billion in 2026 and is projected to reach USD 5.25 billion by 2031, growing at a 7.21% CAGR over 2026-2031.

Which wax type leads sales and which one is growing the fastest?

Paraffin wax led with 47.21% share in 2025, while beeswax is the fastest-growing wax type with a 7.24% CAGR through 2031.

Which sales channel matters most today and which one is expanding the quickest?

Supermarkets and hypermarkets remain the largest channel with 43.25% share in 2025, while online retail stores are expanding the fastest at a 7.77% CAGR.

Which region currently leads global demand for scented candles?

North America led in 2025 with 34.86% share, supported by mature retail networks, strong brand presence, and high household penetration of home fragrance products.

Page last updated on: