Canada Credit Cards Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

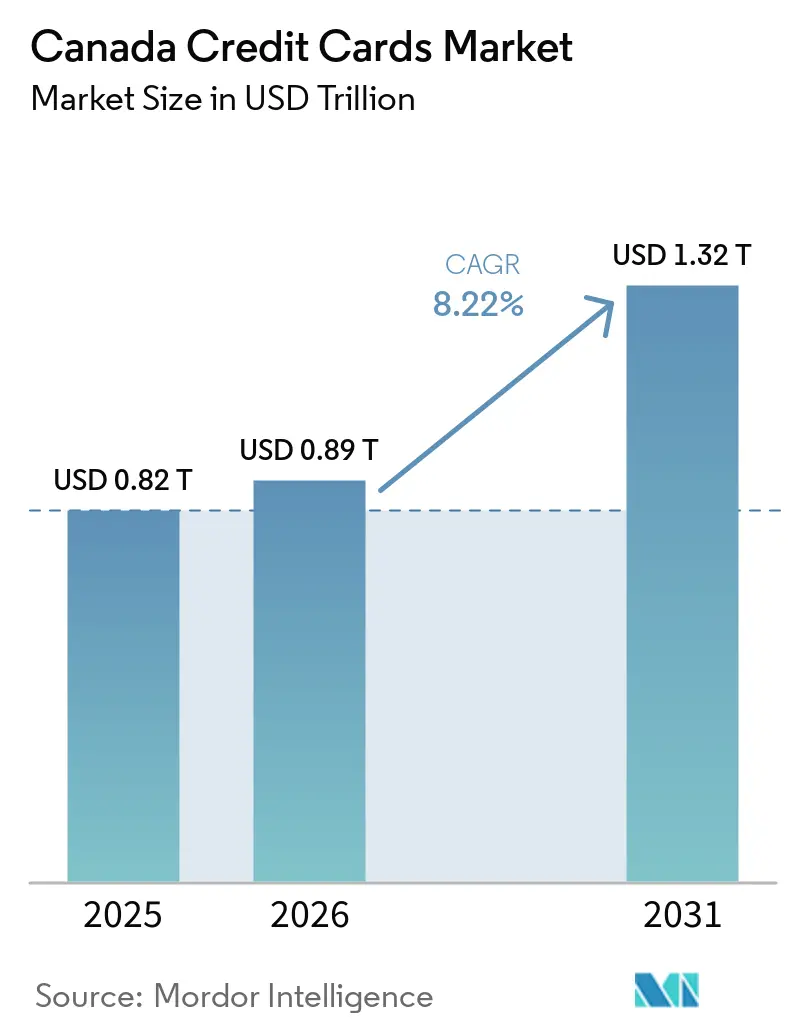

| Base Year Market Size (2025) | USD 0.82 Trillion |

| Market Size (2026) | USD 0.89 Trillion |

| Market Size (2031) | USD 1.32 Trillion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Credit Cards Market Analysis by Mordor Intelligence

The Canada Credit Cards Market size is expected to grow from USD 0.82 trillion in 2025 to USD 0.89 trillion in 2026 and is forecast to reach USD 1.32 trillion by 2031 at 8.22% CAGR over 2026-2031.

Card usage remains central to household spending as rewards ecosystems from large issuers strengthen loyalty, with consumers prioritizing convenience and points accumulation in everyday categories. E-commerce expansion and the continued rise of contactless payments are lifting card frequency both online and in-store, helped by strong digital rails and near-universal acceptance among merchants. Apple’s Tap to Pay on iPhone is broadening acceptance for micro-merchants by removing the need for dedicated terminals, which supports incremental volumes in underserved small business segments. At the same time, the October 2024 reduction in small-business interchange rates is easing acceptance friction for merchants, while modest but visible increases in card delinquencies are keeping risk management at the forefront for issuers as they balance growth with prudent underwriting.

Key Report Takeaways

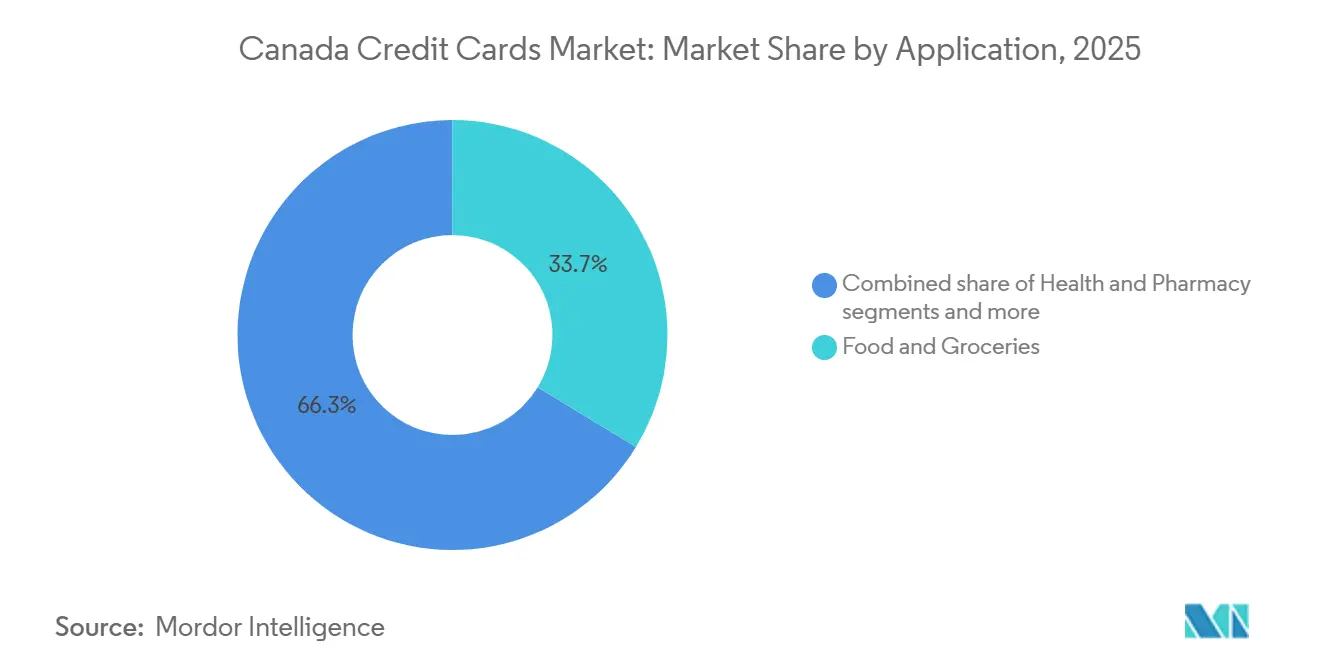

- By application, Food & Groceries led with 33.73% of the Canada credit cards market share in 2025, while Travel & Tourism is projected to expand at a 9.16% CAGR through 2031.

- By card type, General Purpose credit cards held 91.38% of the Canada credit cards market share in 2025, while Specialty and co-branded credit cards are forecast to grow at a 7.26% CAGR to 2031.

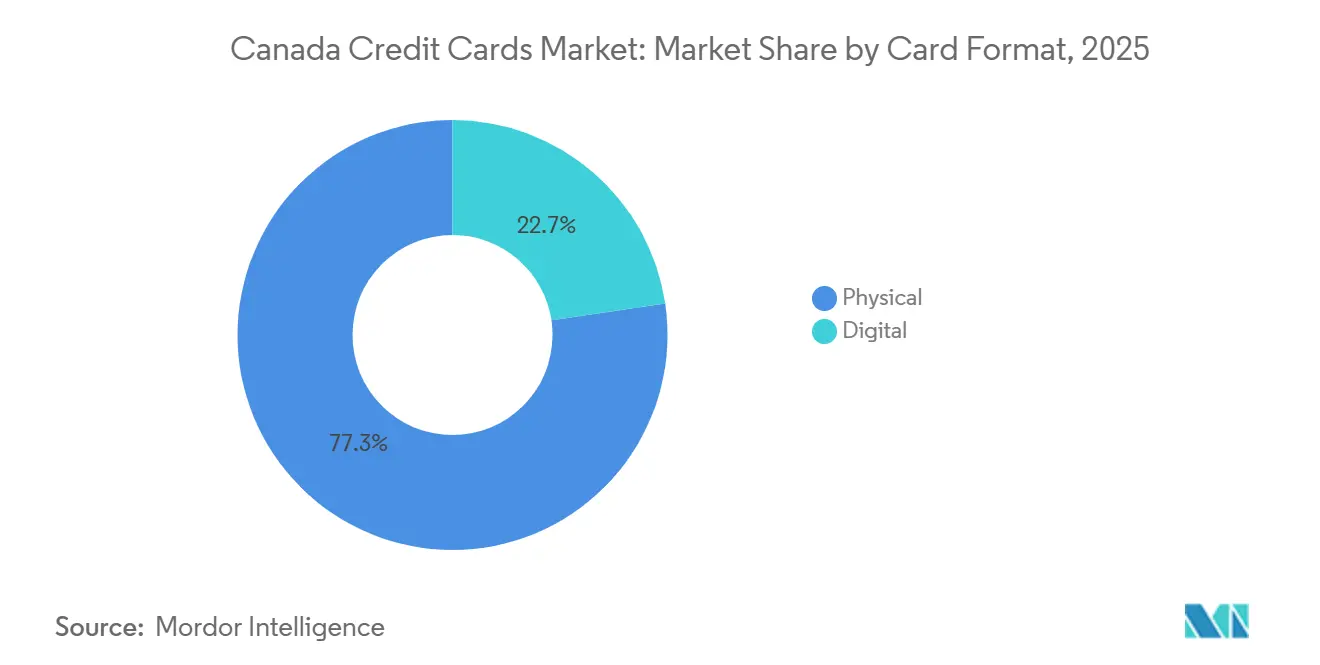

- By card format, Physical cards accounted for 77.37% of the Canada credit cards market share in 2025, while Digital tokenized credentials are expected to grow at a 13.73% CAGR to 2031.

- By provider, Visa led with 57.24% of the Canada credit cards market issuer network share in 2025, while Mastercard is projected to expand at a 6.77% CAGR through 2031.

- By geography, Ontario commanded 39.87% of the Canada credit cards market share in 2025 transaction value, while Alberta is projected to grow at a 7.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Canada. The credit cards market share in our global report expresses these relative weights.

Canada Credit Cards Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rewards ecosystems and co-brands intensify spend capture | + 1.8% | Global, strongest in Ontario and BC metro clusters | Medium term (2-4 years) |

| E-commerce tailwinds keep cards central to remote checkout | + 1.5% | Global, spill-over to the Asia-Pacific cross-border | Long term (≥ 4 years) |

| Contactless ubiquity and rising mobile wallet usage lift card frequency | + 1.3% | National, younger cohorts drive usage | Short term (≤ 2 years) |

| Big Five banks' distribution scale deepens card cross-sell penetration | + 1.2% | National, large urban centers | Medium term (2-4 years) |

| Tap to Pay on iPhone unlocks micro-merchant credit acceptance at scale | + 0.9% | National, urban retail corridors | Medium term (2-4 years) |

| Reduced SMB interchange lowers acceptance friction | + 0.5% | National, broad small-business base | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rewards Ecosystems and Co-brands Intensify Spend Capture

Rewards-driven competition has tightened loyalty, with points-rich grocery, gas, and travel categories encouraging repeat card use and steady wallet share gains in 2026 [1]Association des banquiers canadiens, “Cartes de Crédit, Usage et Avantages,” Canadian Bankers Association, cba.ca. Large co-brand programs are key to this pattern as merchants and issuers align incentives that keep spending within their ecosystems, which anchors high-frequency baskets like groceries and pharmacy. Seasonality amplifies this effect since targeted promotions around major shopping periods shift discretionary dollars toward programs with bonus earning rates and simplified redemption rules. Issuers have also improved digital experiences so cardholders can redeem, request replacements, or adjust limits within mobile channels, which strengthens stickiness and increases the odds that the primary card remains top of wallet. As more co-brands scale, the Canada credit cards market benefits from increasing embedded loyalty that spurs incremental frequency across fuel, grocery, and travel corridors.

E-commerce Tailwinds Keep Cards Central to Remote Checkout

E-commerce adoption keeps card-not-present transactions central to online retail, with digital payments accounting for the bulk of transaction value in Canada’s evolving checkout flows. Consumers who actively use mobile payments are more likely to transact online with credit credentials and do so more frequently, which sustains card prominence in subscription and on-demand commerce. The payment industry’s modernization focuses on transparency and secure authentication, supporting this growth through standardized messaging and clear fee disclosure, which helps merchants maintain stable acceptance. Cardholder concerns about fraud are real, yet zero-liability policies and better risk detection have preserved confidence in card rails during checkout [2]Equifax Canada, “Credit Card Balances Expected to Peak in December With the Holiday Season,” Equifax Canada, equifax.ca. As online volumes rise, the Canada credit cards market continues to capture remote baskets through tokenized credentials, issuer-hosted security layers, and streamlined click-to-pay experiences.

Big Five Banks’ Distribution Scale Deepens Card Cross-sell Penetration

Large banks are using their extensive customer bases and digital adoption to cross-sell cards at onboarding and during key life events, reinforcing incumbent share. Visible mobile adoption across millions of clients supports instant limit increases, self-serve card controls, and push offers, which increase activation rates and keep primary-card status within bank ecosystems. Portfolio disclosures also indicate that banks manage loss provisions carefully, balancing growth with prudent risk controls while credit quality stabilizes in late 2025 and early 2026. Scale continues to expand through M&A, with National Bank’s acquisition of Canadian Western Bank deepening its reach in Western Canada and opening new cross-sell corridors for small-business cards and commercial clients. As cross-selling matures, the Canada credit cards market captures incremental spend from existing bank relationships faster than challengers can displace entrenched issuers.

Tap To Pay On iPhone Unlocks Micro-merchant Credit Acceptance at Scale

Apple’s Tap to Pay on iPhone lets merchants accept contactless payments with just an iPhone and a supported app, which removes hardware costs and accelerates the path to card acceptance for very small sellers. Early deployments with large processors and retailers illustrate how in-aisle or mobile checkout can reduce queues and improve conversion in discretionary categories. This low-friction acceptance model is significant because card readiness among micro-merchants has historically lagged due to terminal lease costs and service fees. As more small businesses adopt software point-of-sale in 2026, the Canada credit cards market gains from a larger acceptance footprint across restaurants, home services, salons, and local transport. The interplay of Tap to Pay and lower small-business interchange rates helps normalize acceptance economics for low-ticket merchants and expands the universe of card-accepting locations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising delinquencies and higher revolving balances elevate credit losses | - 1.1% | Alberta and Ontario stress pockets | Short term (≤ 2 years) |

| SMB interchange cuts compress issuer margins in affected spend mixes | - 0.7% | National small-merchant segments | Medium term (2-4 years) |

| Open banking (CDBA) compliance and data sharing raise costs, intensifying switching | - 0.4% | National, federal oversight | Long term (≥ 4 years) |

| Higher e-commerce fraud and chargebacks necessitate costlier risk controls | - 0.3% | National, card-not-present focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Delinquencies and Higher Revolving Balances Elevate Credit Losses

Serious card delinquency rates edged up to 0.95% by Q4 2025, which indicates a slower pace of deterioration than prior years but still warrants careful provisioning by issuers. [3]TransUnion Canada, “Canadian Household Debt Reaches $2.6 Trillion as Balanced Growth Emerges at Both Ends of the Risk Spectrum,” TransUnion, transunion.ca. Pressures are uneven across age and risk bands, with below-prime balances growing faster than prime tiers and some regions displaying more persistent stress, which requires localized risk tuning. Consumers’ payment-to-balance ratios have softened since mid-2023, and that signals households are stretching repayment timelines to manage cash flow. Education and disclosure remain central, since minimum payment behavior can obscure amortization costs and extend debt duration for many users. This backdrop makes prudent underwriting, tighter line management, and targeted early-intervention strategies critical for the Canada credit cards market in 2026.

Open Banking (CDBA) Compliance and Data Sharing Raise Costs, Intensify Switching

Canada is advancing open banking and payments modernization under a federal framework that prioritizes security, standardization, and consumer-directed data portability [4]Bank of Canada, “Making Change, Accelerating Payments Innovation,” Bank of Canada, bankofcanada.ca. The resulting API-based model supports safer data transmission than screen scraping and will encourage new product design that leverages transaction histories for underwriting. For incumbents, there are upfront integration and governance costs tied to consent management, standardized messaging, and operational resilience requirements. The competitive result can be higher switching as agile players use consumer-permissioned data to present targeted pre-approvals and more relevant rewards. Over time, these shifts will challenge long-standing distribution moats in the Canada credit cards market while supporting broader access for credit-thin consumers under safer data-sharing rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Groceries and Travel Drive Polarized Growth

Food and groceries led the applications mix with 33.73% in 2025, reflecting loyalty-driven spend consolidation at large banners and everyday frequency that anchors the Canada credit cards market share at the category level. Co-branded programs that integrate card spend with grocery and pharmacy rewards deepen engagement, and the reach of national loyalty ecosystems keeps baskets on card rails throughout the month. Cardholder spending data from major banks showed grocery and essential retail holding steady into late 2025, even as discretionary categories softened in some regions. The contactless habit loop in-store and the convenience of saved credentials online both contribute to high transaction counts in this category. As more merchants embrace Tap to Pay and small-business interchange relief, acceptance among small grocers and independent retailers should continue to expand in 2026.

Travel and tourism is the fastest-growing application with a projected 9.16% CAGR through 2031, supported by refreshed airline and travel co-brands, higher discretionary mobility, and competitive earn-and-redeem structures that tie card spend to leisure goals. Bank trackers observed that travel spending cooled at times in late 2025 but remained resilient in 2026 as itineraries shifted and price-sensitive consumers optimized rewards during bookings. The convenience of online booking and digital wallets enhances card acceptance across airlines, hotels, and OTA platforms, and tokenized credentials help improve approval rates and lower friction at checkout. With real-time disbursement capabilities growing in parallel for travel providers and merchants, payment experiences continue to become more immediate, which encourages digital-first consumers to keep cards top of wallet for trips. These dynamics collectively reinforce the Canada credit cards market as the preferred tender in both everyday essentials and higher-value travel spending.

By Card Type: General Purpose Commands Share, Specialty Niches Grow Faster

General-purpose credit cards held a 91.38% share in 2025 as diversified issuers leveraged onboarding, cross-sell, and digital servicing to maintain primacy in the Canada credit cards market. Incumbents disclosed sizable card portfolios supported by wide mobile adoption, which enables rapid activation, credit-line adjustments, and rewards engagement in-app. Portfolio data also show measured risk provisioning and the use of analytics to calibrate limits for prime and super-prime cohorts that drive higher spending without commensurate loss rates. Canadians continue to value convenience and rewards when selecting primary cards, which sustains general-purpose adoption as the baseline product across the mass market. These fundamentals give the Canada credit cards market a stable core anchored by mainstream issuers and widely accepted products.

Specialty and co-branded credit cards are projected to grow at a 7.26% CAGR through 2031 from a smaller base, driven by targeted ecosystems that reward category-specific engagement and align directly with merchant strategies. The announced acquisition of PC Financial by EQB aligns a large co-brand portfolio with a nation-scale loyalty platform, which can amplify grocery and pharmacy spending on the card. As issuers tailor propositions to frequent travelers, fuel shoppers, or grocery power users, specialty cards complement general-purpose anchors and deliver incremental share in priority categories. The Canada credit cards industry is also adopting inclusive designs and accessibility features that broaden product relevance to more customers, which supports sustained product-level growth over time. Together, these trends sustain a two-speed card-type mix, where general-purpose cards provide scale and specialty cards expand in depth in strategic niches.

By Card Format: Physical Dominates, Digital Tokens Surge

Physical cards accounted for 77.37% of the 2025 format share as near-universal issuance and contactless enablement supported tap-and-go usage for everyday purchases in stores across Canada. Cardholders still value tactile form factors for trust and familiarity, and in-person contactless usage continues to rise as terminals are now broadly set up for NFC acceptance. Branch and mobile channels work together to sustain activation, with in-person advice supporting complex decisions while apps enable ongoing card management and rewards redemptions. With card-present fraud rates comparatively lower than online channels, merchants and consumers remain confident in the security of chip and contactless methods. This consistent usage baseline ensures the Canada credit cards market keeps its anchor in physical formats even as tokens scale.

Digital and tokenized formats are projected to grow at 13.73% CAGR through 2031 as mobile wallets and virtual cards gain traction for both in-store and online use. Tokenization shields primary account numbers by using unique transaction codes, and biometrics streamlines authentication for mid-ticket purchases that exceed simple tap limits. Apple’s Tap to Pay further ties smartphones to acceptance, which helps normalize device-based transacting across micro-merchants and pop-up retail. As consumer behavior becomes omnichannel, the ability to pay seamlessly with the same credentials online and in-store reinforces momentum for digital-first experiences. This multi-rail readiness positions the Canada credit cards market to accommodate stronger adoption of tokens across contactless POS, e-commerce, and in-app checkouts.

By Provider: Visa Leads, Mastercard Gains

Visa led with a 57.24% share in 2025, as deep issuer partnerships and widespread acceptance sustained scale in the Canada credit cards market share at the network level. Broad merchant readiness for contactless and robust card-on-file usage in e-commerce supports network throughput in both card-present and card-not-present channels. Visa’s presence within major bank portfolios contributes to distribution depth, which stabilizes network share at the top of the market. With Canada’s payments modernization underway, global networks with scale advantages remain well-positioned to defend their role in high-volume categories. These anchors shape issuer strategy and consumer choice across spending categories and geographies.

Mastercard is projected to grow at a 6.77% CAGR to 2031 by leaning into co-brands, inclusive designs, and SMB-centric services, including near-instant payouts for businesses. Product innovation, such as tactile notches for accessibility, showcases a broadening reach across customer groups. Partnerships that support merchants with faster disbursements and updated digital experiences complement card-spend growth. Together, these moves position Mastercard to compete effectively on rewards, user experience, and small-business enablement within the Canada credit cards market.

Geography Analysis

Ontario held 39.87% of transaction value in 2025, underscoring the province’s central role in the Canada credit cards market and reflecting concentration in Toronto, where a significant share of national volumes is processed. Economic conditions tightened in 2025, with unemployment rising and cost-of-living pressures elevating credit reliance for some households, which contributed to higher delinquency rates. Bank trackers showed that Ontario’s spending outpaced the national average at points during 2025, with apparel and travel contributing to relative strength before weather and caution affected activity in early 2026. The large incumbent footprint also concentrates card marketing in the province, including premium propositions that target frequent travelers and higher-spend segments. Over time, open banking standardization and real-time payment testing will interact with Ontario’s dense merchant base, reinforcing digital adoption patterns that already favor card rails.

Quebec posted the lowest total delinquency rate among provinces in late 2025, which reflects more conservative borrowing behavior and lower average non-mortgage debt compared with higher-cost regions. Electronic payments and contactless usage are entrenched across the province, which sustains a supportive environment for card frequency as cash use declines. Established regional issuers and nationwide banks continue to invest in bilingual servicing and disclosure, which supports trust and consistent usage among Quebec consumers. Spending trends remained resilient into late 2025 relative to some other regions, aided by everyday categories and targeted promotions that encouraged card use. As payments modernization unfolds, the province’s mature digital base is well placed to adopt standardized, API-enabled experiences that reinforce card usage across channels.

British Columbia and Alberta show different risk and growth profiles that shape issuer strategies through 2031, with Alberta projected near the top of provincial growth at a 7.67% CAGR. British Columbia’s strong technology employment base and widespread acceptance of infrastructure support robust contactless adoption, which lifts card frequency in everyday retail. Alberta’s elevated delinquency pockets reflect cyclical wage volatility in sectors linked to energy, which encourages issuers to fine-tune underwriting and early-intervention outreach. Spending momentum varied into late 2025 with parts of Western Canada pulling back, which underscores the value of localizing offers and rewards to maintain activation through cycles. National standards for real-time rails and consumer-directed banking will apply evenly, yet adoption may differ by region as urban centers with high smartphone usage lead in digital-first behaviors that reinforce card rails.

Mordor Intelligence examines the credit cards market across diverse other regional markets as well, including Europe, while also offering granular country-level perspectives for Japan, Hong Kong, and Israel and more.

Competitive Landscape

Market concentration remains high due to distribution strength and large installed customer bases at major banks, with one leading issuer disclosing a 27.3% share within the six-bank universe and strong digital engagement supporting cross-sell. Network acceptance is near universal, and rewards ecosystems are well developed, which keeps the Canada credit cards market structurally anchored to incumbent capabilities. The combination of bank distribution and global network readiness at contactless-enabled terminals reinforces scale advantages in both card-present and card-not-present flows. With consumers ranking convenience and rewards highly in primary-card selection, large issuers continue to offer competitive earn-and-redeem options to attract and retain affluent transactors. Issuers also deploy analytics to adjust limits and acquisition strategies as credit quality stabilizes, which maintains portfolio resilience while pursuing measured growth.

Strategic moves from incumbents and challengers are reshaping loyalty and distribution. The agreement for EQB to acquire PC Financial aligns a large card portfolio with a 17 million-member loyalty platform, which should intensify grocery and pharmacy spend capture on the card once closed. National Bank’s acquisition of Canadian Western Bank extends its reach in Western Canada and should broaden small-business cross-sell opportunities for card products in commercial corridors. Mastercard has emphasized inclusive product design and faster merchant disbursements, which complement network-scale card growth with services that attract SMBs and improve cash flow. At the same time, Apple’s Tap to Pay implementation shows how software-based acceptance can expand the addressable merchant base without incremental hardware. These initiatives push the Canada credit cards market toward broader acceptance and deeper loyalty programs aligned with everyday and travel categories.

Regulatory shifts are also shaping strategy. Lower small-business interchange reduces merchant friction and can lift acceptance and throughput at the long tail of retail and services. The revised Code of Conduct has accelerated complaint handling and elevated transparency, which improves the merchant experience and clarifies pricing structures. Meanwhile, open banking will standardize secure data sharing and could increase switching as fintechs leverage permissioned data to pre-approve applicants with targeted offers and card-linked benefit bundles. Issuers that balance personalization, risk discipline, and rewards economics are best placed to defend share while growing profitably in the Canada credit cards market through 2031.

Canada Credit Cards Industry Leaders

Royal Bank of Canada (RBC)

Toronto-Dominion Bank (TD)

Scotiabank

Canadian Imperial Bank of Commerce (CIBC)

Bank of Montreal (BMO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Casa, a Canadian payments and rewards platform, has partnered with Scotiabank to enhance housing payment solutions for Canadians. This collaboration enables ScotiaGold Passport Visa cardholders to pay rent or condo fees via the Casa platform without incurring transaction fees, aligning with their shared focus on rewarding significant expenditures.

- January 2026: Royal Bank of Canada (RBC) and Canadian Tire Corporation, Limited have announced a strategic loyalty partnership aimed at expanding Triangle Rewards' reach and strengthening RBC's Avion Rewards program while enhancing its merchant partner network.

- December 2025: EQB announced an agreement to acquire PC Financial and affiliates from Loblaw, including a large PC Mastercard portfolio and an exclusive long-term partnership with PC Optimum, targeting closure in 2026, subject to approvals.

- November 2025: Royal Bank of Canada (RBC) and DoorDash expanded their partnership, offering eligible RBC credit cardholders and Avion Rewards members complimentary DashPass access. DashPass offered free delivery, reduced service fees on qualifying DoorDash orders, and exclusive savings.

Canada Credit Cards Market Report Scope

A credit card is a rectangular plastic or metal instrument issued by banks or financial services firms, enabling cardholders to borrow funds for transactions at merchants that accept card-based payments.

The Canada credit cards market report is segmented by application (food & groceries, health & pharmacy, restaurants & bars, consumer electronics, media & entertainment, travel & tourism, other applications), card type (general purpose credit cards, specialty & other credit cards), card format (physical, digital), provider (visa, mastercard, other providers), and geography (Ontario, Quebec, British Columbia, Alberta, Rest of Canada). The market forecasts are provided in terms of Value (USD).

| Food & Groceries |

| Health & Pharmacy |

| Restaurants & Bars |

| Consumer Electronics |

| Media & Entertainment |

| Travel & Tourism |

| Other Applications |

| General Purpose Credit Cards |

| Specialty & Other Credit Cards |

| Physical |

| Digital |

| Visa |

| Mastercard |

| Other Providers |

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Application | Food & Groceries |

| Health & Pharmacy | |

| Restaurants & Bars | |

| Consumer Electronics | |

| Media & Entertainment | |

| Travel & Tourism | |

| Other Applications | |

| By Card Type | General Purpose Credit Cards |

| Specialty & Other Credit Cards | |

| By Card Format | Physical |

| Digital | |

| By Provider | Visa |

| Mastercard | |

| Other Providers | |

| By Geography | Ontario |

| Quebec | |

| British Columbia | |

| Alberta | |

| Rest of Canada |

Key Questions Answered in the Report

What is the Canada credit cards market outlook to 2031?

The Canada credit cards market size is projected to be USD 0.82 trillion in 2025, USD 0.89 trillion in 2026, and reach USD 1.32 trillion by 2031, at an 8.22% CAGR from 2026 to 2031.

Which applications are most influential for spending in Canada?

Food and groceries led with 33.73% of spend in 2025, while travel and tourism is the fastest-growing use case with a projected 9.16% CAGR through 2031.

How are regulation and policy shaping card acceptance?

The Government of Canada's October 2024 interchange cuts lowered in-store rates to a 0.95% annual weighted average for eligible small businesses and updated the Code of Conduct to shorten complaint handling and improve transparency.

What role do contactless and mobile wallets play in Canada?

Contactless is entrenched across point-of-sale and is complemented by mobile wallets that use tokenization and biometrics, which together increase frequency and reduce checkout friction.

Which networks and issuers have the strongest positions?

Visa leads the provider mix, Mastercard is growing through partnerships and product innovations, and top banks maintain dominance through scale and cross-sell, including one issuer disclosing a 27.3% share of the six-bank universe.

How are delinquencies trending, and what does that mean for risk?

Serious card delinquency rates rose modestly into Q4 2025, and issuers are balancing growth with disciplined underwriting, line management, and early-intervention strategies.

Page last updated on: