Japan Credit Card Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

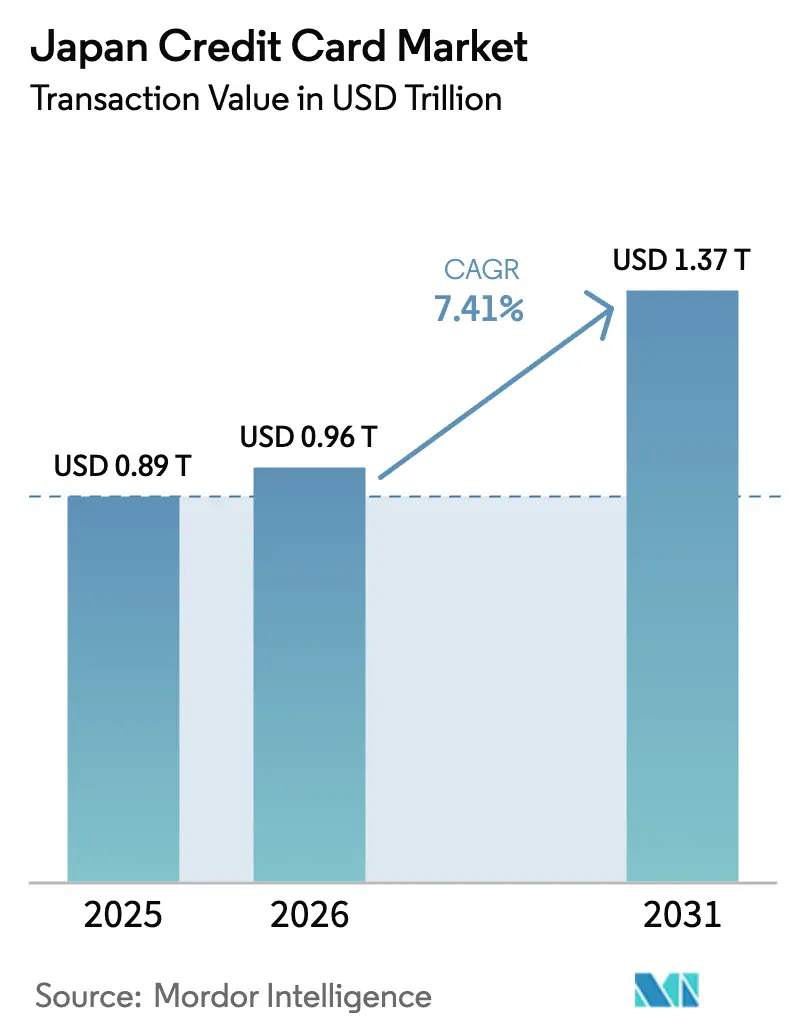

| Base Year Market Size (2025) | USD 0.89 Trillion |

| Market Size (2026) | USD 0.96 Trillion |

| Market Size (2031) | USD 1.37 Trillion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Credit Card Market Analysis by Mordor Intelligence

The Japan credit card market size was valued at USD 0.89 trillion in 2025 and estimated to grow from USD 0.96 trillion in 2026 to reach USD 1.37 trillion by 2031, at a CAGR of 7.41% during the forecast period (2026-2031). In 2024, the increasing reliance on credit cards as a primary mode of cashless transactions highlights the country’s ongoing transition toward a cashless economy. Despite this trend, the overall cashless payment ratio remains relatively low, indicating significant potential for growth in the adoption of digital payment methods. State-led digitalization programs, demographic shifts that favour contactless payments, and the integration of cards into super-app ecosystems continue to reinforce adoption momentum. Infrastructure modernization tied to the mandatory 3D Secure rule effective April 2025 is curbing fraud and raising merchant confidence, while inbound tourism recovery and embedded finance innovations are widening usage scenarios for both consumers and small businesses. Competitive dynamics remain intense, yet strategic alliances between banks, card networks, and fintech platforms are opening non-traditional distribution channels that extend the reach of the Japan credit card market.

Key Report Takeaways

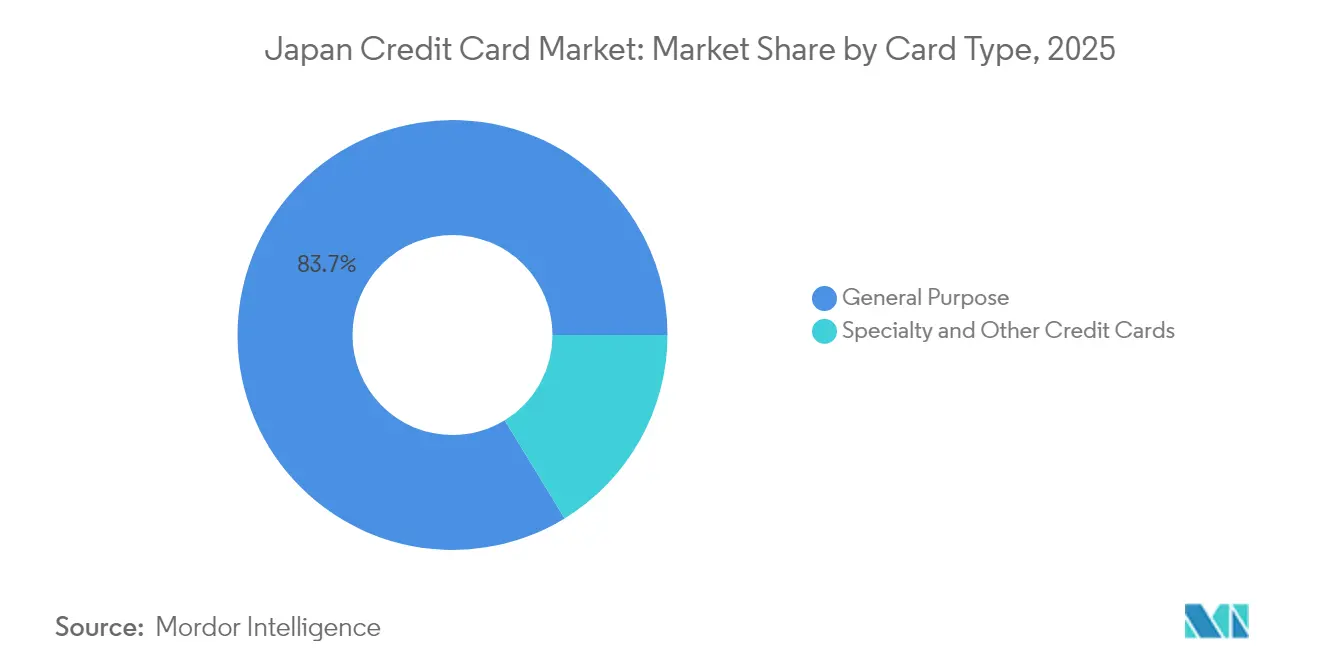

- By card type, general purpose cards held 83.74% of Japan credit card market share in 2025, while specialty & other cards are projected to expand at a 12.59% CAGR through 2031.

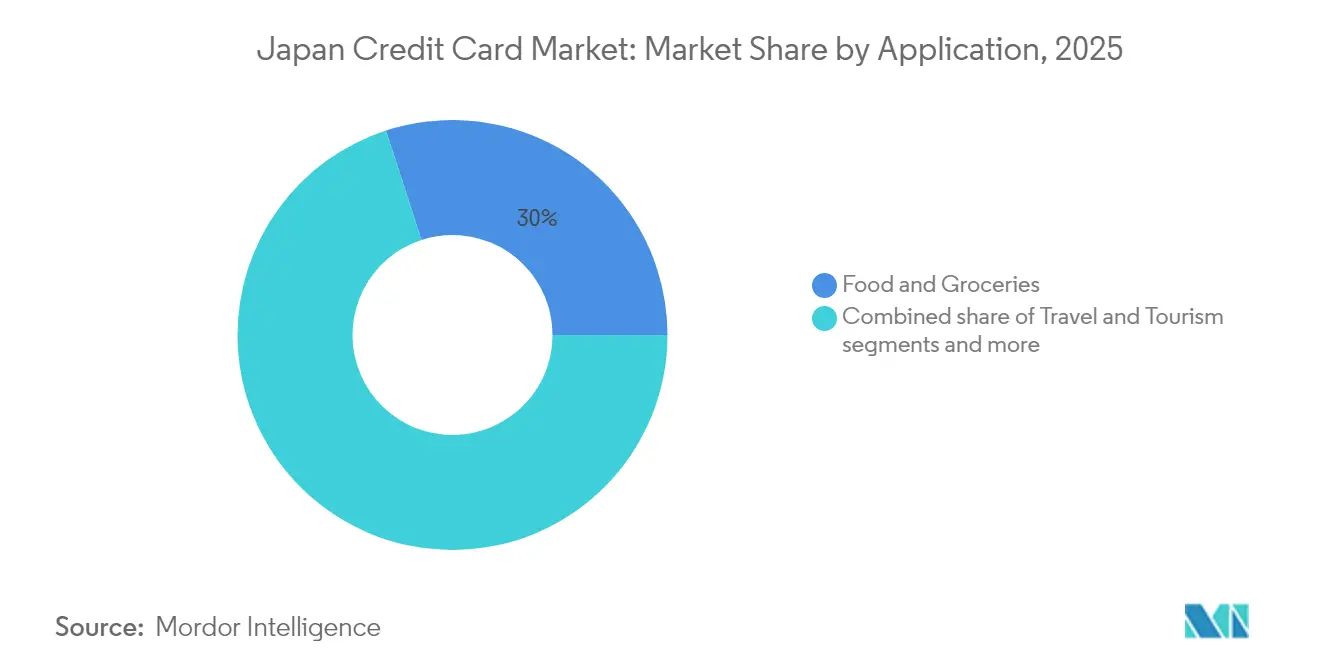

- By application, food & groceries captured 30.01% of Japan's credit card market size in 2025, whereas media & entertainment posts the strongest 10.18% CAGR through 2031.

- By provider, visa controlled 48.92% of Japan's credit card market share in 2025, yet discover-branded partners are on track for an 8.87% CAGR to 2031.

- By geography, the Kanto region accounted for 34.28% of Japan's credit card market size in 2025, and Kyushu & Okinawa show the highest 6.66% CAGR for the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Japan representing one among them. The global report on credit cards market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Japan Credit Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce penetration | +1.2% | Kanto and Kansai metro areas | Medium term (2-4 years) |

| Government-backed cashless push | +0.9% | Nationwide, strongest in Tokyo-Osaka-Nagoya | Short term (≤ 2 years) |

| Loyalty-program gamification | +0.7% | Urban centres | Medium term (2-4 years) |

| Pandemic-induced payment habit stickiness | +0.8% | Suburban and rural areas | Long term (≥ 4 years) |

| Integration into super-apps | +1.1% | Nationwide, spill-over to APAC | Medium term (2-4 years) |

| Growing BNPL-card hybrids | +0.6% | Urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce Penetration Drives Transaction Volume Growth

Surging online retail activity funnels incremental spending onto cards, lifting transaction counts and average ticket sizes across the Japan credit card market. PayPay’s 7.46 billion transactions in 2024, equivalent to one-fifth of all cashless activity, illustrate how super-apps amplify card-linked volumes both online and at point-of-sale. The Bank of Japan closely tracks JCB Consumption NOW data to gauge private consumption, underscoring the macroeconomic importance of card flows[1]Bank of Japan, “Outlook for Economic Activity and Prices (January 2025),” boj.or.jp . Specialty products benefit disproportionally, as subscription-based gaming and streaming services underpin Media & Entertainment’s double-digit expansion. Transport operators in Kansai have already enabled tap-to-ride credit card payments, blurred category lines, and driven habitual card usage for low-value mobility transactions that once favoured cash.

Government-Backed Cashless Push Accelerates Infrastructure Modernization

The Financial Services Agency and the Digital Agency are coordinating policy, subsidy, and regulatory levers that speed merchant acceptance and strengthen cybersecurity. Required 3D Secure authentication from April 2025 is absorbing fraud losses that climbed to JPY 541 billion (USD 3.60 billion) in 2023, addressing a key bottleneck for digital uptake. My Number digital IDs will be wallet-ready by late spring 2025, enabling biometric verification and further streamlining checkout flows. The Expo 2025 Osaka pilot of facial-recognition payments will showcase next-generation use cases across 1,000 terminals, illustrating how public events can seed nationwide rollouts. Together, these measures establish a secure, standards-based environment that sustains Japan's credit card market growth amid rising transaction complexity.

Loyalty-Program Gamification Enhances Customer Lifetime Value

Issuers are layering game mechanics onto point ecosystems to deepen engagement. Rakuten Card’s neighbourly cross-service rewards underpin ownership among nearly 8 in 10 Japanese cardholders, proving that rich earn-and-burn loops drive front-of-wallet status. JCB’s POICHI service lets shoppers accrue multiple currencies in one scan, lifting frequency while offering retailers targeted promotions. Card-based investment capabilities—such as JCB’s mutual-fund sweep with SBI Securities—are broadening spend categories into wealth accumulation, reinforcing monthly activity even for older demographics. Ageing segments exhibit conservative borrowing but remain highly engaged where points convert to everyday savings, allowing issuers to harvest interchange rather than revolve balances.

Integration of Credit Cards into Super-Apps Expands Ecosystem Reach

PayPay, Rakuten, and new fintech super-apps rely on credit cards as both funding rails and loyalty conduits. Rakuten’s alliance with Mizuho and Orient Corporation connects 900,000 merchant nodes to bank infrastructure, enabling one-tap credit issuance at checkout[2]Rakuten Group, “Rakuten Group, Rakuten Card, Mizuho Financial Group Form Business Alliance,” global.rakuten.com. SMBC’s capital link with Infcurion lets non-financial enterprises embed credit functions via APIs, already spawning more than 1.5 million corporate cards that ride the Visa network. Such network effects bind consumers into closed-loop environments, increasing data visibility for risk engines and cementing transaction share for platform-aligned issuers within the Japan credit card market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| An ageing population’s lower credit appetite | -1.8% | Nationwide, the steepest in rural prefectures | Long term (≥ 4 years) |

| Intensifying debit & QR-code competition | -1.3% | Smartphone-dense urban hubs | Short term (≤ 2 years) |

| Stricter FSA affordability controls | -0.9% | Nationwide, focused on metro areas | Medium term (2-4 years) |

| Cyber-fraud surge at regional ATMs | -0.7% | Suburban ATM networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing Population’s Lower Credit Appetite Constrains Expansion

Japan’s median age continues to climb, and older consumers generally avoid revolving balances, capping revenue potential for issuers. The senior demographic demonstrates a clear preference for card payments over cash transactions. Their card usage aligns more closely with debit card behaviour, underscoring a focus on transactional convenience rather than leveraging credit facilities. Rural depopulation compounds the issue, shrinking addressable volumes in regions where bank branch closures are already pronounced. Regulatory affordability guidelines further tighten underwriting, demanding more granular income validation for retirees. Issuers therefore pivot toward transaction-based economics, packaging generous points and cross-service bundles that resonate with frugal but digitally savvy seniors.

Intensifying Debit & QR-Code Competition Pressures Market Share

The market is witnessing a surge in rewards-focused debit cards and QR-code wallets introduced by banks and fintech providers, which are gradually diminishing the perceived benefits of credit cards. JCB has strategically partnered with regional banks to launch touch-enabled debit products, a move aimed at sustaining healthy network transaction volumes. However, these debit products generate lower interchange fees compared to credit cards, impacting revenue streams. In densely populated urban areas with high smartphone penetration, PayPay has established dominance in QR-based payment systems, particularly in convenience stores and quick-service restaurants. This trend is driving younger consumers to adopt mobile-native payment solutions. While these payments still rely on underlying card funding, they are compressing revenue margins for card issuers, signaling a shift in consumer payment preferences and its implications for the payment ecosystem.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Card Type: Specialized Products Outpace a Dominant Core

General-purpose cards represented 83.74% of Japan's credit card market size in 2025, reflecting their broad acceptance footprint and omnichannel utility. Specialty & Other cards are gaining ground at a forecast 12.59% CAGR as issuers court high-value niches with metal constructions, lifestyle privileges, and embedded finance options. JAL Luxury Card, launched August 2025, exemplifies ultra-premium positioning with annual fees up to JPY 599,500 (USD 3,990), targeting affluent travellers who demand exclusive lounge access. SME-focused products such as the forthcoming Orico-Aeon business card unlock working-capital lines for underserved corporate segments, illustrating how targeted propositions can widen participation without cannibalizing mainstream portfolios.

Fintech entrants’ experiment with creator-economy tie-ups, adding social identity layers that resonate with Gen Z. These novel formats exploit lean digital distribution to bypass costly physical channels, undercut fees, and gin up community engagement metrics. The diversification trend spreads issuer risk and incubates differentiated revenue streams, although scale remains centred on the stalwart General Purpose category that continues to anchor the Japan credit card market.

By Application: Consumption Patterns Shape Growth Focus

Food & Groceries commanded 30.01 of % Japan credit card market share in 2025, sustained by the supermarket sector’s broad contactless coverage and the rise of same-day delivery services. Media & Entertainment yields the highest expansion at a 10.18% CAGR, buoyed by subscription video, music streaming, and mobile gaming that generate stable monthly billings. Recent JCB-SBI Securities integration stretches card utility into investment contributions, hinting at a future where financial-services payments climb the application rankings.

Health & Pharmacy transactions benefit from digital prescription platforms and an aging population that values frictionless checkout in clinical settings. Travel & Tourism spending recovered briskly alongside the rebound in foreign arrivals, though regional disparities persist. Collectively, these patterns guide issuers to tailor category-specific bonuses and merchant co-marketing that reinforce loyalty and intensify spend concentration within the Japan credit card market.

By Provider: Visa’s Lead Faces Niche Network Encroachment

Visa processed 48.92% of all 2025 transaction value, leveraging an expansive terminal base and early contactless enablement in mass transit. Discover-branded partnerships are forecast at an 8.87% CAGR as Capital One’s acquisition resources accelerate acceptance, investments, and marketing. JCB safeguards domestic relevance with 56 million global acceptance points and new debit collaborations that lock regional banks into its rails. Mastercard emphasizes tokenization, pledging to retire static PANs by 2030 in favour of dynamic tokens and biometric passkeys, steps that may tighten merchant security requirements and influence issuer roadmaps.

Competition among providers is intensifying within digital channels, where issuers and super-apps must strategically decide between leveraging open-loop networks or adopting proprietary QR code frameworks. Robust backend capabilities, including advanced real-time fraud detection mechanisms, efficient token lifecycle management processes, and the availability of developer-friendly APIs, increasingly determine market success. These factors are becoming critical differentiators, surpassing the traditional reliance on the widespread distribution of physical card products.

Geography Analysis

Kanto accounted for 34.28% of Japan's credit card market size in 2025, anchored by Tokyo’s affluent consumer base and headquarters of global firms. Kyushu & Okinawa deliver the fastest 6.66% CAGR, lifted by tourism outlays and airport modernization. Kansai’s 40% contactless penetration outpaces most areas, proving that infrastructure density translates into usage frequency gains that amplify issuer returns. Hokkaido, Tohoku, and Chugoku-Shikoku regions derive spending boosts from nature-oriented travel, yet remain under-penetrated, signalling upside as hospitality providers upgrade terminals and loyalty tie-ins.

Japan’s diverse economic map produces distinct adoption curves for cards, necessitating nuanced go-to-market plays. Kanto leads in absolute volume, but its saturation requires issuers to chase wallet-share gains through premium tiers and bundled wealth products. Kyushu & Okinawa, buoyed by post-pandemic travel, view cards as gateways to tourist spend, thereby accelerating merchant acceptance upgrades across hotels and duty-free sites. Kansai’s embrace of transit tap-and-go indicates how public infrastructure can shift consumer psychology, presenting a template for other regions.

Chubu’s industrial backbone fuels B2B card uptake, especially as supply-chain digitalization mandates traceable expense controls. Issuers prioritizing aerospace and automotive supplier clusters can harvest volumes otherwise locked in bank transfers and paper invoicing. Geography-tailored outreach, such as local language concierge services and partnerships with prefecture-level banks, allows national brands to deepen relevance and defend share against regionally entrenched challengers.

Mordor Intelligence provides coverage of the credit cards market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Hong Kong, Israel, and Canada incorporating local coverage and market participation, as required.

Competitive Landscape

The top issuers command a significant share of purchase value, endowing the market with moderate concentration but leaving headroom for agile disruptors. Rakuten Card’s symbiosis with the e-commerce giant yields formidable acquisition economics, while Mizuho’s alliance supercharges cross-sell into bank accounts and mortgages. Sumitomo Mitsui Card invests in biometric plastics through its LIFE CARD subsidiary to counter fraud fatigue and differentiate on security. SMBC Group’s tie-up with Infcurion unlocks white-label issuance for retailers and SaaS firms, signalling a shift toward platform-as-a-service models that abstract away traditional bank rails.

Mid-tier players exploit niche focus, as Season Card targets lifestyle segments and AEON Credit Service leverages its retail footprint for co-branded penetration. Fintech entrants like Nudge push user-centric design, while PayPay Card Corp unifies QR wallet funding and revolving credit within a single app, enabling data flywheels that refine underwriting. International networks partner selectively—Discover via domestic alliances and Diners through high-end hospitality like Hotel New Otani’s premium program, to stake claims within profitable sub-pools. Collectively, these manoeuvres intensify innovation velocity yet leave incumbents with scale economics that sustain their leadership within the Japan credit card market.

Japan Credit Card Industry Leaders

JCB Co. Ltd.

Mitsubishi UFJ NICOS

Sumitomo Mitsui Card (SMCC)

Rakuten Card

AEON Credit Service

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Orient Corporation and AEON Financial Service set September launch for a co-branded business card targeting SMEs across the AEON Group network.

- May 2025: JCB, Orient Corporation, and Money Forward X partnered to embed AI underwriting into JCB’s SME portal Cashmap, automating credit decisions.

- April 2025: JAL Card introduced the JAL JCB Card Platinum Pro with a metal surface design and elevated mile bonuses.

Japan Credit Card Market Report Scope

A credit card, known as "kurejitto kādo" (クレジットカード) in Japanese, refers to a payment card issued by financial institutions or credit card companies. It enables cardholders to make purchases and access credit, allowing them to borrow funds up to a certain credit limit from the issuing institution. A complete background analysis of the Japanese credit card market, which includes an assessment of the economy, a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, are covered in the report.

The Japanese credit card market is segmented by card type, application, and provider. By card type, the market is sub-segmented into general-purpose credit cards and specialty & other credit cards. By application, the market is sub-segmented into food & groceries, health & pharmacy, restaurants & bars, consumer electronics, media & entertainment, travel & tourism, and other applications. By provider, the market is sub-segmented into visa, mastercard, and other providers. The report offers market size and forecasts for the Japanese credit cards market in value (USD) for all the above segments.

| General Purpose Credit Cards |

| Specialty & Other Credit Cards |

| Food & Groceries |

| Health & Pharmacy |

| Restaurants & Bars |

| Consumer Electronics |

| Media & Entertainment |

| Travel & Tourism |

| Other Applications |

| Visa |

| MasterCard |

| Other Providers |

| Hokkaido |

| Tohoku |

| Kanto |

| Kyushu & Okinawa |

| Rest of Japan |

| By Card Type | General Purpose Credit Cards |

| Specialty & Other Credit Cards | |

| By Application | Food & Groceries |

| Health & Pharmacy | |

| Restaurants & Bars | |

| Consumer Electronics | |

| Media & Entertainment | |

| Travel & Tourism | |

| Other Applications | |

| By Provider | Visa |

| MasterCard | |

| Other Providers | |

| By Geography | Hokkaido |

| Tohoku | |

| Kanto | |

| Kyushu & Okinawa | |

| Rest of Japan |

Key Questions Answered in the Report

What is the current value and projected growth of Japan’s credit-card spending?

Aggregate purchase value is USD 0.96 trillion in 2026 and is forecast to reach USD 1.37 trillion by 2031, implying a 7.41% CAGR.

Which card type captures the most consumer spend?

General-purpose cards account for 83.74% of overall transaction value, reflecting their broad merchant acceptance and multi-category utility.

Which application segment generates the largest share of transactions?

Food & Groceries leads with a 30.01% share thanks to ubiquitous supermarket acceptance and high shopping frequency.

Which provider is expanding fastest, and why?

Discover-branded partners are on track for an 8.87% CAGR through 2031, buoyed by Capital One’s planned investment to widen merchant acceptance and bolster network technology.

How are biometric technologies changing everyday card usage?

Issuers are enhancing security and expediting checkouts by testing fingerprint-enabled plastics and deploying facial-recognition terminals, like NEC's initiative for Expo 2025 Osaka.

What impending rule will tighten card-payment security in 2025?

From April 2025 all issuers and merchants must adopt 3D Secure authentication, a mandate designed to curb online fraud that hit JPY 541 billion in 2023.

Page last updated on: