Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

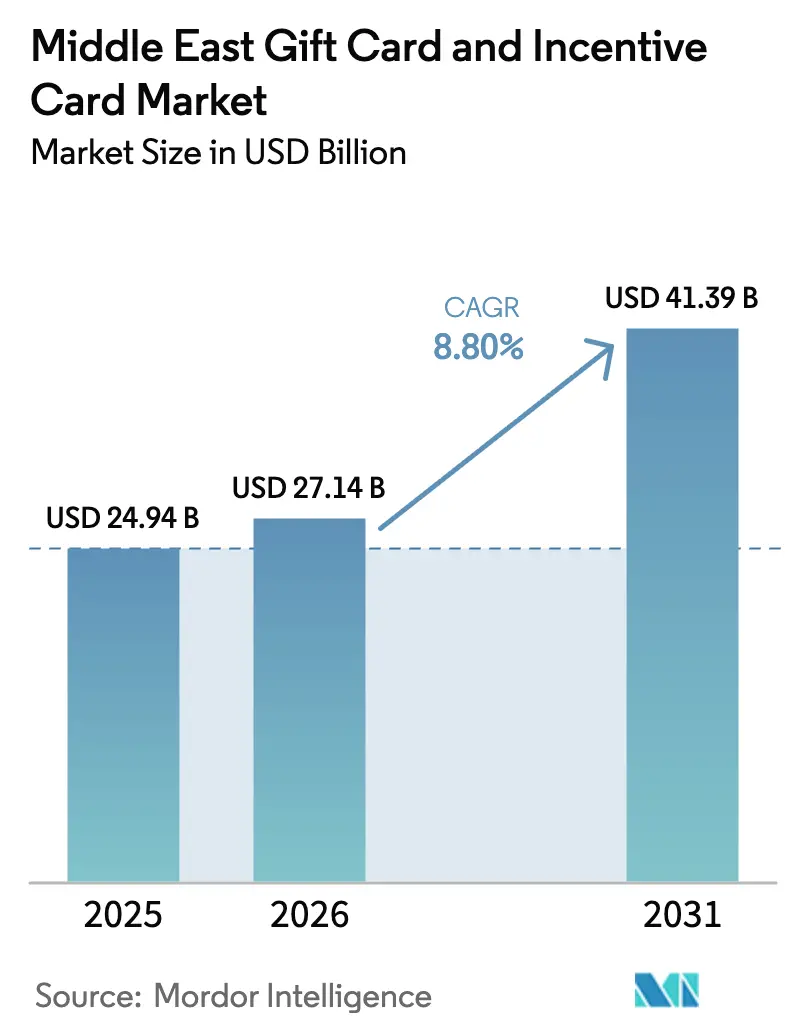

| Base Year Market Size (2025) | USD 24.94 Billion |

| Market Size (2026) | USD 27.14 Billion |

| Market Size (2031) | USD 41.39 Billion |

| Growth Rate (2026 - 2031) | 8.80% CAGR |

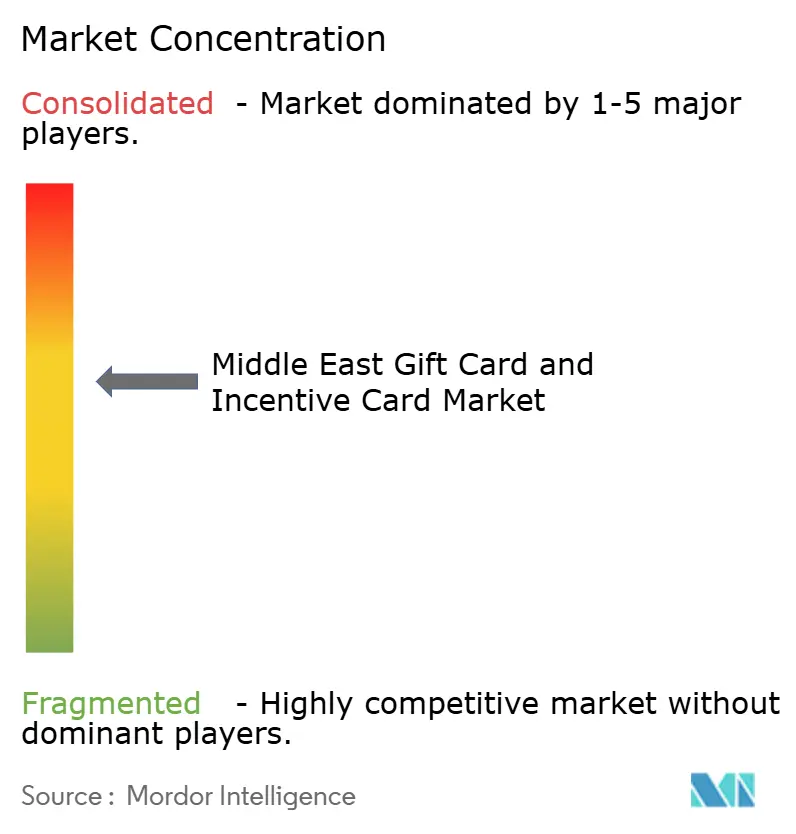

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Gift Card And Incentive Card Market Analysis by Mordor Intelligence

The Middle East Gift Card And Incentive Card Market size is projected to be USD 24.94 billion in 2025, USD 27.14 billion in 2026, and reach USD 41.39 billion by 2031, growing at a CAGR of 8.80% from 2026 to 2031.

Momentum in the Middle East gift card and incentive card market reflects the region’s ongoing pivot from cash to digital value, with government cashless mandates and real-time payment rails reinforcing consumer preference for instant redemption. Expansion of e-commerce and digital wallet acceptance provides embedded distribution points at checkout, which raises conversion for digital gifting at the moment of purchase. Banks and processors are standardizing API access and payouts, which shortens enterprise onboarding and supports rapid issuance for corporate rewards. Instant payment platforms, including account-to-account schemes, are maturing across the Gulf and are improving the utility of real-time issued gifts and incentive value.

Key Report Takeaways

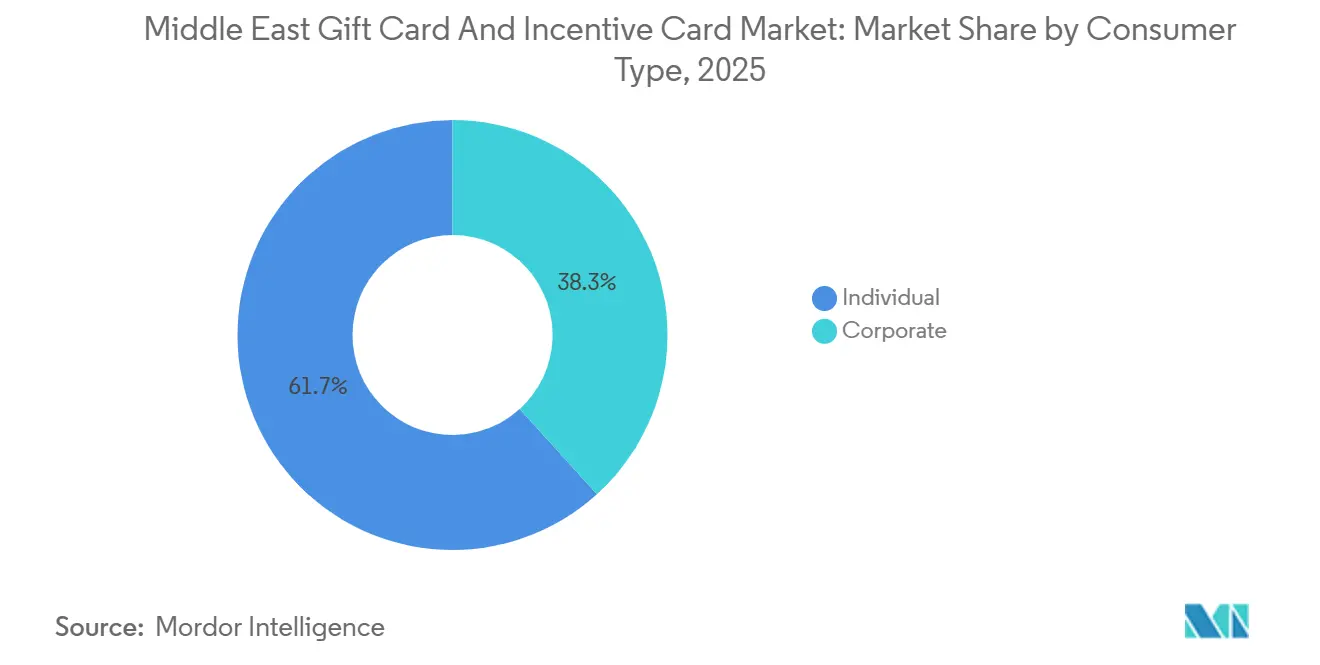

- By consumer type, individual purchasers led with 61.67% of the Middle East gift card and incentive card market share in 2025, while the corporate-SME segment is projected to expand at a 14.9% CAGR to 2031.

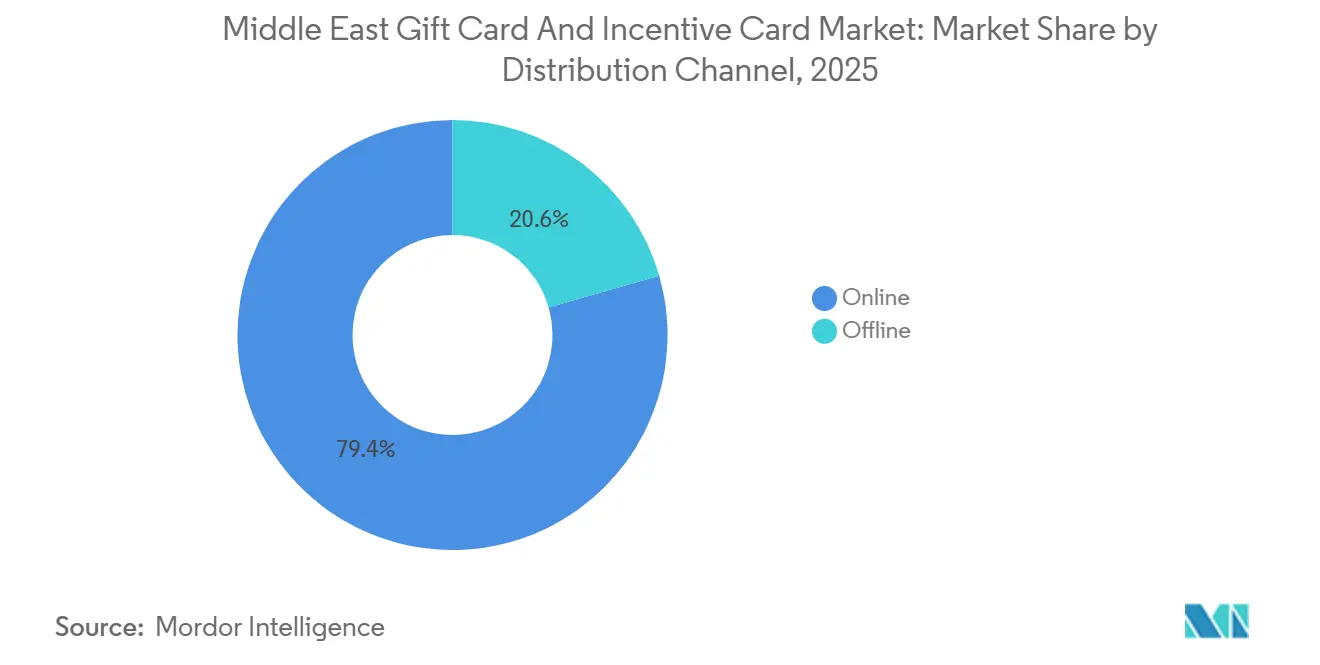

- By distribution channel, online accounted for 79.44% of the Middle East gift card and incentive card market share in 2025, and online is forecast to grow at a 19.4% CAGR through 2031.

- By product, e-gift cards represented 67.33% of the Middle East gift card and incentive card market share in 2025, with e-gift cards projected to advance at a 19.9% CAGR to 2031.

- By geography, Saudi Arabia held 43.87% of the Middle East gift card and incentive card market share in 2025 and is set to post the fastest CAGR at 15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Gift Card And Incentive Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive e-commerce & digital-payment penetration | +2.1% | Global, strongest in the UAE, KSA, Qatar | Short term (≤ 2 years) |

| Government cash-lite agendas (e.g., Saudi Vision 2030) | +1.8% | KSA, UAE, Qatar, Bahrain | Medium term (2-4 years) |

| Corporate digitization of employee rewards & perks | +1.4% | UAE, KSA, Qatar | Medium term (2-4 years) |

| Growing expat & millennial population with gifting culture | +1.2% | GCC-wide | Long term (≥ 4 years) |

| Rise of Sharia-compliant prepaid gifting products | +0.9% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| API-driven fintech platforms enabling embedded gift cards | +0.7% | UAE, KSA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive E-commerce & Digital-Payment Penetration

E-commerce in the Gulf continues to scale on top of strong digital wallet acceptance, which turns checkout flows into natural touchpoints for digital gift and incentive products. [1]Stripe, “Payments in the Middle East,” Stripe, stripe.com. Merchants in the region benefit from increasingly seamless integrations with local payment options, which support checkouts that include offer-driven or occasion-driven gift cards without redirecting users. Real-time, account-to-account platforms and instant-payment schemes have expanded across the Middle East, which reduces settlement latency for issuers and raises redemption confidence for consumers. Banks are productizing APIs for payouts and collections, which simplifies corporate workflows for bulk issuance and reconciled settlement of digital rewards. Consumers increasingly expect immediate value delivery and mobile wallet provisioning, and that preference aligns with the instant nature of e-gift formats in the Middle East gift card and incentive card market.

Corporate Digitization of Employee Rewards & Perks

Enterprises and SMEs are replacing paper vouchers with API-issued digital rewards because automated issuance improves traceability, spend controls, and reconciliation. Platforms that provide self-service dashboards, bulk purchasing, and brand personalization are gaining adoption, and vendors are investing in engineering capacity to accelerate new features. As more HR and payroll systems integrate with bank-grade APIs, corporate buyers can execute high-volume, rule-based issuance within normal approval workflows, which narrows the operational gap with cash-equivalent payouts. Retailers and large loyalty ecosystems are linking rewards to payment credentials, which expands redemption opportunities in-store and online for employees and program members. This shift reinforces a multi-merchant, multi-currency posture that suits cross-border employers and distributes across the Middle East gift card and incentive card market.

Rise of Sharia-Compliant Prepaid Gifting Products

Banks and retailers in the UAE are launching Sharia-compliant covered cards and rewards-linked payment credentials, which signal strong demand for halal-aligned stored value [2]Abu Dhabi Islamic Bank, “ADIB and Majid Al Futtaim Launch First Shariah-Compliant SHARE Covered Cards,” ADIB, adib.ae. Islamic banks in the region offer multiple prepaid variants and co-branded formats, which widen the set of everyday use cases within compliant structures. Growth in Islamic fintech across leading hubs, including Saudi Arabia and the UAE, creates a favorable context for compliant gift and incentive products that avoid interest-bearing features. Sharia review and transparent fee structures are becoming table stakes where regulators emphasize alignment with national Islamic finance strategies, which support market access for compliant issuers. As these products integrate with established loyalty ecosystems, compliant gifting vehicles can scale faster through retailer-led distribution in the Middle East gift card and incentive card market.

API-Driven Fintech Platforms Enabling Embedded Gift Cards

Issuer-processors and banking partners are investing in modular APIs that allow rapid card and stored-value launches across multiple countries[3]NymCard, “QED Investors Leads $33M Investment in NymCard,” NymCard, nymcard.com. Enterprise clients can integrate payouts-as-a-service to reduce operational friction and to distribute incentives through their own applications and channels. Open Finance programs and standardized API hubs are improving data access and consented flows, which expands the design space for embedded gift and reward journeys. The region’s progress with instant payments helps issuers shift from batch to real-time, which supports on-demand issuance and near-instant redemption. As non-banks and super-apps plug into issuer-processor stacks, competition focuses more on distribution, customer experience, and partnerships in the Middle East gift card and incentive card market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High fraud & charge-back risk in cross-border digital cards | -1.6% | UAE, KSA, global | Short term (≤ 2 years) |

| Fragmented consumer-protection / e-money regulation | -1.2% | UAE, KSA, Kuwait | Medium term (2-4 years) |

| Cultural reliance on cash in non-GCC markets | -0.8% | Wider MENA, selected GCC | Long term (≥ 4 years) |

| Dormancy-balance escheat rules are squeezing breakage revenue | -0.5% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Consumer-Protection / E-money Regulation

Regulatory frameworks in the Gulf set distinct licensing, capital, and reporting criteria, which lead to jurisdiction-specific operating models. In the UAE, stored value providers must meet paid-up capital and reserve obligations and follow in-country data storage, which favors incumbents with established compliance teams. Variation across markets requires modular compliance architectures and careful sequencing of launches, which slows scaling for startups in the Middle East gift card and incentive card market. As regulators refine consumer disclosure and risk controls, platform differentiation increasingly includes demonstrable compliance readiness. The result is a gradual consolidation of shares into well-capitalized issuers that can localize operations while maintaining cross-border consistency.

Dormancy-Balance Escheat Rules Squeezing Breakage Revenue

UAE regulations define dormant accounts and mandate transfers of unclaimed funds after a set period, which reduces traditional breakage revenue for programs. Consumer-protection rules require clear disclosure of fees and validity, which narrows the scope for ambiguous terms and emphasizes timely customer engagement. Issuers now design re-engagement campaigns and loyalty bridges to avoid dormancy thresholds, which raises operational complexity. Shorter tenor, high-velocity instruments can mitigate margin pressure where dormancy policies are strict. These changes advantage scaled platforms that can automate outreach and link balances to broader loyalty ecosystems in the Middle East gift card and incentive card market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consumer Type: Corporate-SME Drives Acceleration Despite Individual Dominance

Individual buyers held 61.67% of value in 2025, while corporates and SMEs are projected to grow at a 14.9% CAGR through 2031, signaling a shift toward programmatic issuance alongside strong personal gifting. The Middle East gift card and incentive card industry is seeing corporate adoption accelerate because HR and payroll systems can now trigger compliant, auditable digital rewards within existing approval flows. Dashboard-enabled platforms that allow bulk purchase, personalization, and spend tracking have lowered procurement friction for SMEs and mid-sized enterprises. Corporate buyers value spend controls and automated reconciliation, which digital formats deliver with fewer manual steps than paper vouchers or cash equivalents in the Middle East gift card and incentive card market. As loyalty ecosystems link rewards with payment credentials, employees gain more redemption flexibility across in-store and digital channels.

The Middle East gift card and incentive card market continues to serve strong personal-gifting traditions while adding corporate demand that is measurable and API-driven. The Middle East gift card and incentive card market size for corporate buyers is set to expand the fastest through 2031 as issuance shifts to digital rails that support instant delivery and lower operating costs. Platform investments in engineering and security are accelerating feature releases that directly address enterprise control and compliance requirements. Over the forecast window, personal-gifting demand remains resilient across cultural calendars, while corporate programs scale through partnerships with banks, processors, and super-apps in the Middle East gift card and incentive card market.

By Distribution Channel: Online Surges as Offline Stagnates

Online channels held 79.44% of value in 2025 and are projected to grow at a 19.4% CAGR through 2031, reflecting strong alignment between e-gift formats and mobile-first shopping in the region. The Middle East gift card and incentive card industry benefits from e-commerce growth and expanding wallet acceptance, which positions checkout pages and super-apps as efficient distribution endpoints. Real-time payment capabilities and API-based payouts improve funding and redemption flows, and this favors digital delivery over physical stores. As Open Finance matures, third-party integrations will make it easier for non-bank consumer apps to embed gift-card journeys that feel native. Online growth, therefore, compounds as issuers solve for speed, choice, and seamless provisioning in the Middle East gift card and incentive card market.

The Middle East gift card and incentive card market share for online channels reached 79.44% in 2025 as merchants bundled gifts with promotions, loyalty, and BNPL-aligned checkouts. Offline remains relevant in select use cases where physical presentation is preferred or where cash-oriented users value in-person purchase, although growth continues to trail digital alternatives. Retailers are investing in next-generation gift-card infrastructure to unify in-store and app experiences, which sustains omnichannel continuity. Over the forecast period, digital-first issuers and retailer-led ecosystems are expected to capture most incremental volume in the Middle East gift card and incentive card market.

By Product Type: E-gift Cards Dominate and Accelerate

E-gift cards accounted for 67.33% of market value in 2025 and are forecast to grow at a 19.9% CAGR to 2031, supported by instant delivery, lower issuance costs, and wallet provisioning. Retail ecosystems are integrating loyalty programs with payment credentials that can be issued digitally, which expands redemption choice and reduces dependence on plastic. Tokenization and mobile-wallet support enable secure contactless redemption of e-gifts, which raises utility in omnichannel environments. Product innovation continues across multi-merchant and co-branded formats, which further strengthens the appeal of digital issuance in the Middle East gift card and incentive card market. In contrast, physical cards maintain a smaller role for ceremonial gifting and specific user segments that value tangible presentation.

The Middle East gift card and incentive card market size will tilt further toward e-gift formats as issuer-processor APIs make cross-market launches faster and cheaper for merchants and platforms. Banks and large retailers will keep investing in compliant, loyalty-linked digital credentials to preserve ecosystem lock-in while improving customer experience. As a result, growth is expected to concentrate in digital, while physical formats adapt to premium and event-driven niches within the Middle East gift card and incentive card market. Over time, embedded finance patterns and instant-redemption experiences will make e-gifts the default option for both consumers and corporates.

Geography Analysis

Saudi Arabia held 43.87% of 2025 regional revenues and is projected to post the fastest growth at 15% through 2031, which sets the country as the anchor geography for the forecast period. Vision 2030’s target for an 80% non-cash share by 2030 keeps the modernization agenda central and supports merchant acceptance and consumer usage. Banks and fintechs are building scalable issuance on domestic and international rails, which enables cross-border and multi-merchant redemption within Saudi ecosystems. The Middle East gift card and incentive card market share for Saudi Arabia reflects both policy momentum and retailer adoption, with loyalty and rewards integrations now core to growth programs. Over the forecast window, platform investments and compliance readiness are expected to support scale effects in the Kingdom.

The UAE serves as a testbed for instant payments and Open Finance, which benefits real-time issuance and embedded redemption flows. The Central Bank’s stored-value and dormant-account rules formalize obligations for issuers, which strengthens consumer confidence and aligns with rising e-commerce usage. Loyalty ecosystems and retailers continue to expand digital credentials that unify shopping and rewards, which improves redemption convenience for residents and visitors. With robust app usage and payments modernization, the UAE remains a key driver of e-gift innovation in the Middle East gift card and incentive card market.

Across the rest of the Gulf, regulatory and infrastructure maturity varies, but digitization continues to advance. Qatar’s support for Islamic fintech development provides a favorable backdrop for compliant prepaid and rewards products linked to local ecosystems. In Bahrain, wallet and QR solutions are gaining traction through partnerships that accelerate merchant acceptance for everyday use cases. Kuwait is a candidate for omnichannel strategies that blend in-store and app-based purchases, as consumers exhibit strong card usage in retail and digital commerce. As instant-payment and Open Finance programs expand, these markets are expected to benefit from faster issuance and broader partner integrations in the Middle East gift card and incentive card market.

Competitive Landscape

Competitive intensity in the Middle East gift card and incentive card market is moderate, with leading issuers holding a significant share, while room remains for platform-based challengers. Issuer-processors are scaling regional infrastructure and commercial partnerships to enable rapid, compliant launches across multiple jurisdictions. Banks and large retail ecosystems are fusing loyalty with payment credentials to increase stickiness and redemption frequency. Retailers are also investing in next-generation issuance and management tools to unify in-store and in-app experiences, which differentiates redemption journeys. The mix of compliance strength, API maturity, and distribution reach is emerging as the primary source of advantage in the Middle East gift card and incentive card market.

Several strategic moves showcase the direction of competition. A leading issuer-processor secured new capital in 2025 to expand API-based issuing and cross-border capabilities across MENA, which supports bank and fintech partners with faster time to market. In late 2025, a prominent bank and a major retailer launched compliant covered cards that reward spending across thousands of outlets, which ties loyalty operations directly to payment credentials. At the same time, retailers are deepening their investment in digital gift-card programs to support enterprise and SME demand for branded incentives and omnichannel redemption. These shifts illustrate how both incumbents and challengers are aligning product roadmaps with embedded finance and instant-payment adoption in the Middle East gift card and incentive card market.

Operating models continue to evolve toward standardized APIs, data-protection compliance, and orchestrated fraud defenses. Stored-value and dormant-account rules push issuers to improve disclosure, data handling, and customer engagement, which raises barriers for unlicensed aggregators. Payment-network initiatives around tokenization and risk tools are improving consumer trust, which supports digital-first gifting and rewards adoption. As competitive advantages hinge more on compliance readiness and distribution efficiency, partnerships across banks, processors, and large retailers are likely to define share outcomes in the Middle East gift card and incentive card market.

Middle East Gift Card And Incentive Card Industry Leaders

Edenred

YouGotaGift

Resal

Merit Incentives

STC Pay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Al Dar Exchange and NymCard signed a strategic agreement in Doha to advance modern payment capabilities, support the evolution of payment services, enhance customer experiences, and expand digital channels. The collaboration combines Al Dar’s local presence with NymCard’s issuer-processor infrastructure to accelerate product delivery for consumers and businesses.

- February 2026: stc pay Bahrain partnered with Al Haddad Motors to elevate premium customer experiences and expanded its app’s language support to seven native options. The enhancements focus on usability and reach, supporting broader access to digital financial services across customer segments. The move demonstrates how wallet ecosystems are layering partnerships to grow everyday relevance.

- December 2025: Abu Dhabi Islamic Bank and Majid Al Futtaim launched the UAE’s first Sharia-compliant SHARE covered cards, offering 6% back in SHARE points at more than 5,000 stores. The launch integrates loyalty and payments to create a seamless path from earning to redemption within a large retail network. The product supports compliant digital issuance at scale in the Middle East gift card and incentive card market.

- March 2025: NymCard secured USD 33 million in Series B financing led by QED Investors, with participation from regional and existing investors, to scale API-based issuing and cross-border capabilities. The raise supports product compliance and partner expansion across more than ten MENA markets. The company’s capacity building reflects strong demand for embedded issuance among banks, fintechs, and enterprises.

Middle East Gift Card And Incentive Card Market Report Scope

The Middle Eastern gift card and incentive card market involves issuing and managing prepaid cards used for gifts or incentives. It includes physical and digital cards issued by retailers, banks, and specialized firms, catering to diverse consumer and corporate needs across the region.

The Middle East gift card and incentive card market report is segmented by consumer (individual, corporate), distribution channel (online, offline), product (e-gift card, physical card), and geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Oman). The market forecasts are provided in terms of value (USD).

By Consumer

| Individual | |

| Corporate | Small-scale Enterprises |

| Mid-tier Enterprises | |

| Large Enterprises |

By Distribution Channel

| Online |

| Offline |

By Product

| E-gift Card |

| Physical Card |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| By Consumer | Individual | |

| Corporate | Small-scale Enterprises | |

| Mid-tier Enterprises | ||

| Large Enterprises | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Product | E-gift Card | |

| Physical Card | ||

| By Geography | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Bahrain | ||

| Oman | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Middle East gift card and incentive card market?

The market size is expected to grow from USD 24.94 billion in 2025 to USD 27.14 billion in 2026 and is forecast to reach USD 41.39 billion by 2031 at 8.8% CAGR over 2026-2031, supported by cashless policies, embedded payments, and e-commerce expansion.

Which customer segment is growing fastest in the Middle East gift card and incentive card market?

Corporate and SME buyers are the fastest, with a projected 14.9% CAGR through 2031 as API-enabled issuance improves control, traceability, and reconciliation for rewards programs.

How is the channel mix evolving for the Middle East gift card and incentive card market?

Online channels represented 79.44% of value in 2025 and are set to grow at a 19.4% CAGR, driven by wallet acceptance, instant payments, and embedded checkout journeys across apps.

Which product format leads in the Middle East gift card and incentive card market?

E-gift cards lead with a 67.33% share in 2025 and are forecast to advance at a 19.9% CAGR, due to instant delivery, tokenization support, and wallet provisioning across devices.

Which country contributes the most to the Middle East gift card and incentive card market?

Saudi Arabia accounted for 43.87% of regional revenues in 2025 and is set to post the fastest growth at 15% through 2031, anchored by Vision 2030s cashless agenda.

What factors most influence competition in the Middle East gift card and incentive card market?

Compliance readiness, API maturity, and distribution reach are decisive, with banks, issuer-processors, and large retailers partnering to scale real-time issuance and loyalty-linked credentials.

Page last updated on: