Europe Credit Cards Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.96 Trillion |

| Market Size (2026) | USD 1 Trillion |

| Market Size (2031) | USD 1.23 Trillion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

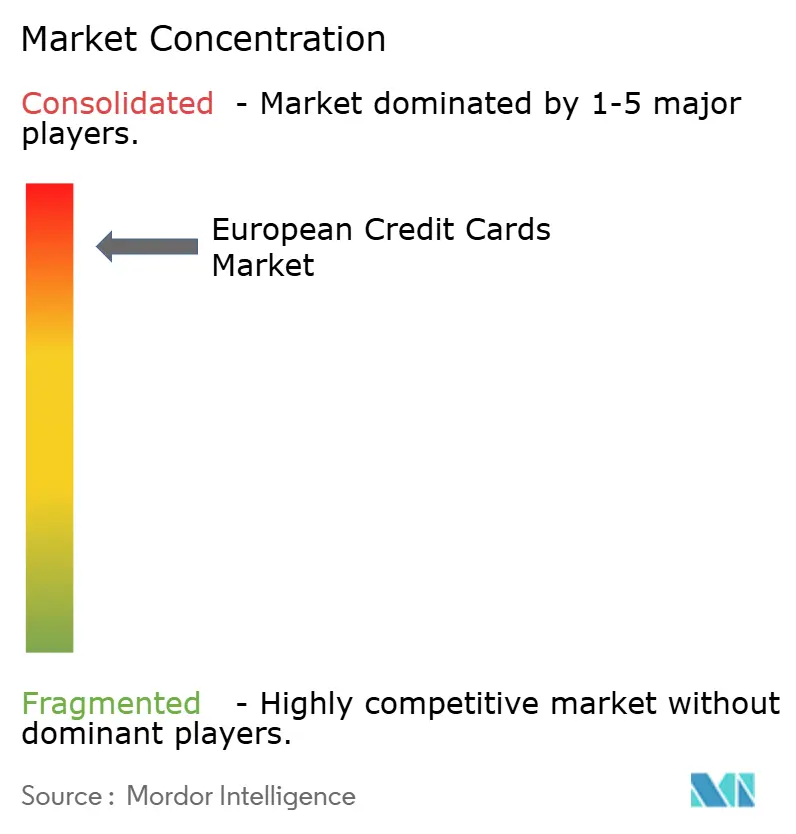

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Credit Cards Market Analysis by Mordor Intelligence

The Europe Credit Cards Market size is projected to be USD 0.96 trillion in 2025, USD 1 trillion in 2026, and reach USD 1.23 trillion by 2031, growing at a CAGR of 4.24% from 2026 to 2031.

The expansion of digital commerce reinforces growth, as European B2C e-commerce turnover increased 7% to USD 990.45 billion (EUR 842.00 billion) in 2024, which kept card-on-file use and recurring payments active across categories. Rebound in cross-border leisure travel and a stronger corporate travel outlook into 2026 are lifting premium card spending and average ticket sizes, which support higher-value transactions for issuers and networks. The regulatory setting shapes economics and choice, with EU caps on consumer credit interchange and an instant payments mandate that compels euro transfers to settle in 10 seconds, which together push providers to reinforce authentication and risk controls to defend card use cases. Networks and issuers are scaling tokenization, Click to Pay, and passkeys to reduce fraud and friction, which helps protect approvals and keeps card credentials embedded inside leading wallets. These forces collectively guide product design, commercialization, and partnerships across the European credit card market as providers balance regulated margins with technology-led value.

Key Report Takeaways

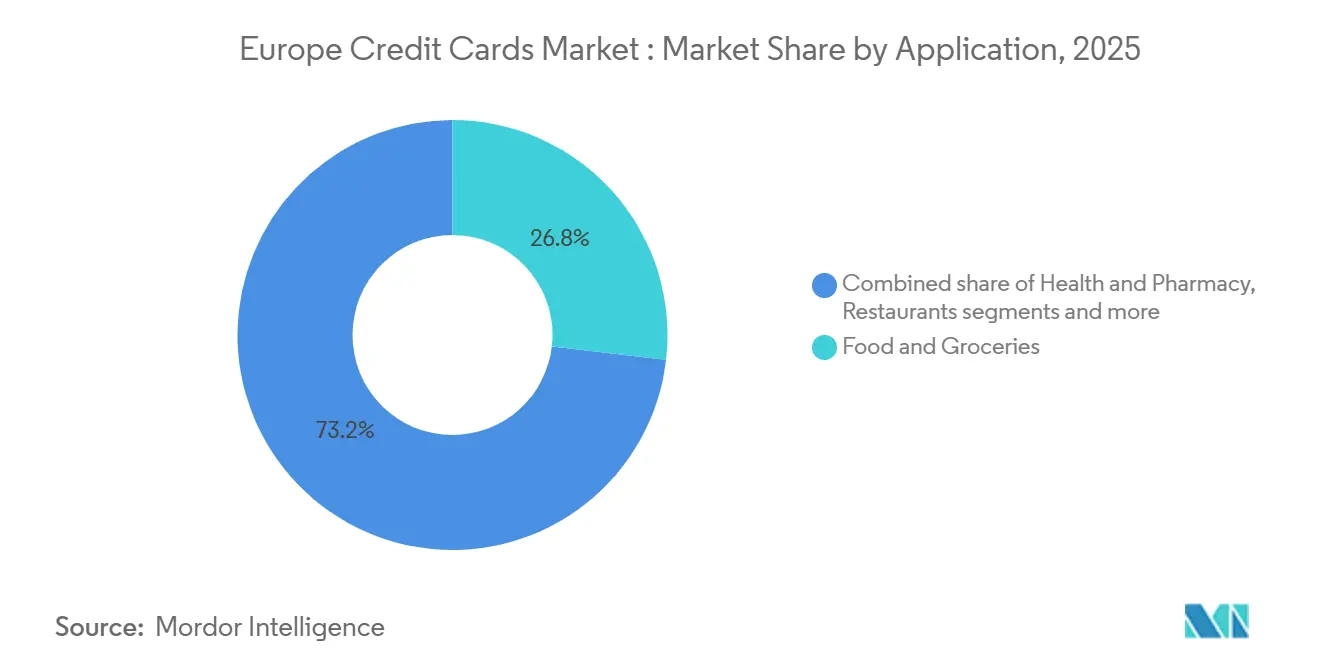

- By application, food & groceries led with 26.83% of the European credit card market share in 2025, while travel & tourism is forecast to post a 4.83% CAGR to 2031.

- By card type, general-purpose credit cards held 91.14% of the European credit card market share in 2025, while specialty & other credit cards are projected to grow at a 5.12% CAGR through 2031.

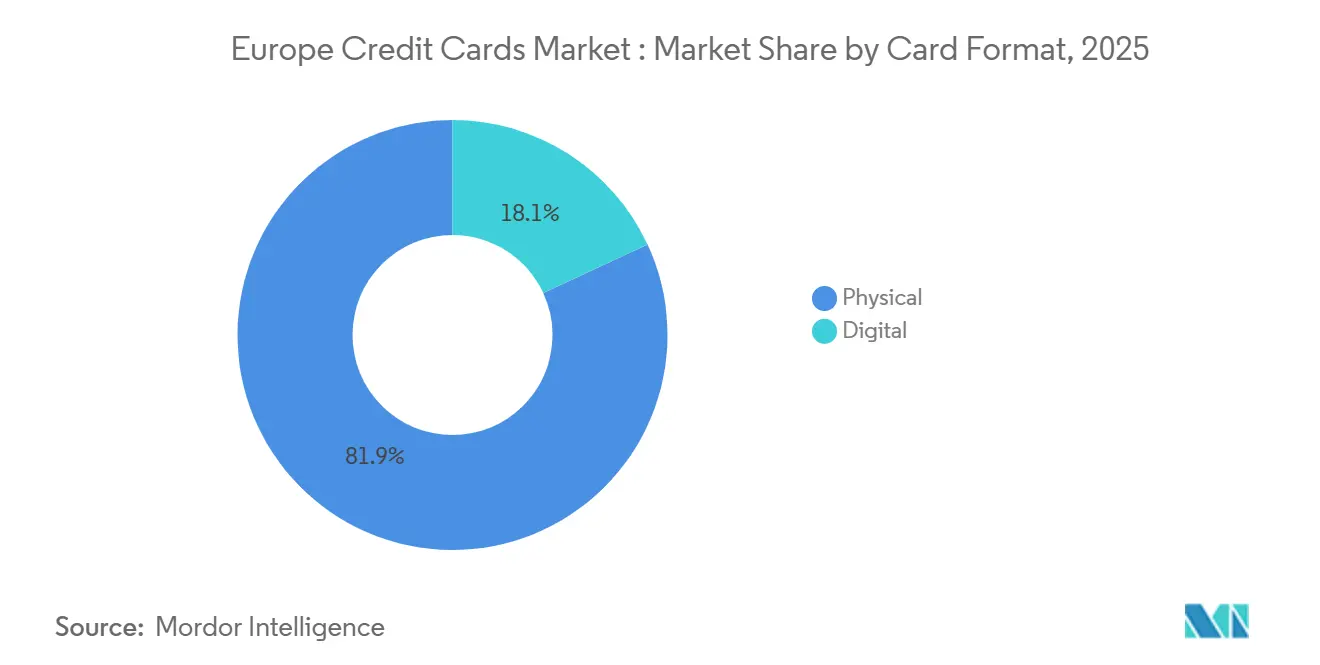

- By card format, physical cards retained 81.92% of the European credit card market share in 2025, while digital cards are expected to expand at a 5.63% CAGR to 2031.

- By provider, Visa led with 51.34% of the European credit card market share in 2025, while Mastercard is projected to grow fastest at a 5.94% CAGR through 2031.

- By geography, the United Kingdom accounted for 24.45% of the European credit card market share in 2025, while Spain is projected as the fastest-growing geography at a 5.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in Europe includes both locally based firms and those operating across multiple regions. The market landscape in the global credit cards industry research shows how these players are arranged internationally.

Europe Credit Cards Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cash-to-Cashless Shift & Contactless Adoption Surge | +0.8% | Global, strongest in Nordics, Western Europe, weakest in Eastern Europe | Medium term (2-4 years) |

| Explosive E-commerce Growth Across the EU | +1.2% | Western Europe's core, Southern Europe accelerating | Short term (≤ 2 years) |

| Post-COVID Rebound in Cross-Border Travel Spend | +0.9% | Southern Europe, Northern Europe, United Kingdom corporate hubs | Medium term (2-4 years) |

| PSD2-Enabled Fintech Credit Expansion | +0.7% | Spain, Germany, France, EU-wide open banking | Long term (≥ 4 years) |

| Embedded-Finance & Co-Branded Card Proliferation | +0.5% | National and Pan-European | Medium term (2-4 years) |

| BNPL-Credit Card Hybrids Driving New Issuance | +0.4% | Germany, France, the Nordics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cash-to-Cashless Shift & Contactless Adoption Surge

Cash use keeps shrinking in daily transactions as digital payments normalize across Europe, with adoption gaps by subregion creating uneven but durable growth vectors for the European credit card market. Northern and Western Europe show the highest digital shopping participation among adults, while Eastern and Southern Europe lag and provide scope for catch-up as acceptance and consumer familiarity improve. Contactless use and card preference remain strong, with consumers citing convenience and speed, and merchants signaling alignment with card acceptance as a default for retail environments, which supports continued card volume growth in mixed-payment settings. Tokenization and streamlined checkout continue to scale, with Mastercard reporting nearly half of European e-commerce transactions tokenized and Click to Pay enrollment more than doubling across 26 markets, which helps secure card credentials in wallets and protects approval rates [1]Mastercard Newsroom, “Mastercard’s Checkout Transformation Gains Ground Across Europe,” Mastercard, mastercard.com. Consumer recognition of card security and merchant preference for cards add reinforcement, with both groups trusting card rails for domestic and cross-border transactions over the alternatives. Together, these factors underpin a steady migration from cash and help core issuers capture consistent growth in the European credit card market.

Post-COVID Rebound in Cross-Border Travel Spend

Recovered tourism and corporate travel lift high-yield card spend, which supports premium issuance and category-specific co-brand programs that reinforce the European credit card market. European travel demand remained firm as spending outpaced arrivals in 2025, which boosts transaction values in travel, hospitality, and transportation categories tied to cardholder rewards and insurance features[2]European Travel Commission, “Europe’s Travel Demand Remains Steady as Spending Outpaces Arrivals,” ETC Corporate, etc-corporate.org. Business travel is projected to reach USD 458.64 (EUR 389.90 billion) in 2026, which signals healthy corporate activity and supports the issuance of cards with enhanced controls, reporting, and insurance bundles used by enterprise and SME segments [3]Global Business Travel Association, “European Business Travel Spending to Reach 389.9 Billion Euros in 2026,” GBTA, gbta.org. Co-branded travel products are evolving around cross-border needs, highlighted by the European Travel Commission-Mastercard-ICBC card that targets Chinese visitors and links acceptance, destination support, and cultural elements into one credential. This rebound adds momentum to the European credit card market as issuers match travel-linked benefits with revived cross-border volumes and diversify revenue beyond interchange by monetizing insurance and FX. The travel-led mix shift favors premium portfolios that can maintain loyalty and keep spend engaged across borders, which steadies growth through the cycle for the European credit card market.

PSD2-Enabled Fintech Credit Expansion

Open banking has expanded the addressable base for non-bank lenders, which broadens issuance routes and encourages innovative underwriting approaches within the European credit card market. Spanish microdata show that Paytech firms achieved revenue and return gains post-PSD2, indicating lowered entry barriers and more efficient customer acquisition for regulated providers that plug into bank data with customer permission. Strong Customer Authentication improves fraud control and supports tokenized and biometric flows that lower friction at checkout and in-app, which benefits card approval rates and helps keep issuers competitive in digital commerce. Nordic consumer expectations for instant provisioning, real-time controls, and seamless wallet integration show how embedded issuance is becoming a baseline, and fintech-bank collaborations scale faster in markets with mature API standards. EU-level audits note that adoption of open banking remains uneven and that standardization is critical to scale, which pushes ecosystems toward common technical specifications that reduce integration costs for issuers. As these rails mature, the European credit card market benefits from broader distribution through platforms and channels that offer credit at the point of need while staying within regulatory guardrails.

Embedded-Finance & Co-Branded Card Proliferation

Issuers and platform partners are positioning cards as multi-revenue assets by tying them to subscriptions, travel insurance, and service bundles, which raises per-customer economics for the European credit card market. Program-level math in Germany shows meaningful income generation from interchange alone at modest spend levels, and layering FX and embedded services can enhance portfolio yield when interchange is constrained. Personalization of the physical card and packaging experience helps acquisition and spend lift, with reported gains from premium materials and targeted features like biometric card authentication and dynamic CVV. Co-brand momentum is visible in travel, where a new European Travel Commission-Mastercard-ICBC product seeks to guide a large visitor cohort toward curated acceptance and benefits across multiple European destinations. Ecosystem partners in benefits and mobility are also leveraging card credentials and commercial capabilities to broaden issuance without recreating card acceptance infrastructure from scratch. This partner-led motion continues to diversify the European credit card market, tying issuance to vertical software and affinity programs with differentiated economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange-Fee Caps & Stricter EU Regulations | -0.6% | EU-27 consumer credit caps; UK cross-border CNP oversight | Long term (≥ 4 years) |

| Inflation-Driven Consumer Caution on Revolving Debt | -0.4% | Eurozone-wide, the Spanish jurisprudence discipline on revolving | Medium term (2-4 years) |

| Instant-Payment & Wallet Substitution Risk | -0.5% | SEPA core instant mandate and wallet gains | Short term (≤ 2 years) |

| ESG-Led Tightening of Consumer-Credit Rules | -0.3% | EU-27 consumer protection focuses, Spain disclosure rulings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interchange-Fee Caps & Stricter EU Regulations

Capped interchange for consumer credit at 0.30% across the EU compresses issuer economics and shifts growth focus toward value-added services, commercial card issuance, and product differentiation that reduces churn in the European credit card market. EU-level audits describe progress in digital payments and the influence of regulation on pricing, innovation, and market structure, which guides how issuers invest in fraud controls and authentication to protect approval rates. Industry associations emphasize the role of interchange in funding network security and innovation, a view that underscores how caps reroute business models toward services and subscriptions. In the United Kingdom, regulators scrutinize post-Brexit cross-border card-not-present pricing, and industry participants track proposals to align fees with pre-Brexit benchmarks for online transactions between the United Kingdom and the EEA. Issuers balance these constraints by investing in tokenization, passkeys, and risk systems that help defend approval performance and transaction margins in the European credit card market.

Instant-Payment & Wallet Substitution Risk

The EU’s instant payment mandate requires euro credit transfers to settle within 10 seconds, which presents substitution risk for low-value domestic card transactions and pushes issuers to improve tokenization and digital ID layers to defend use cases in the European credit card market. Instant infrastructure had limited usage relative to total transfers until regulatory attention accelerated bank implementations, and issuer responses now target risk scoring and authentication to preserve seamless checkout where cards remain embedded. EU audit projections indicate wallets will expand their share of e-commerce and in-store transactions by 2026, which further shifts consumer interfaces even when cards remain the underlying rail through tokenization. Cards continue to earn preference and trust from both consumers and merchants, which forms a strong base for issuers to extend credentials into wallets and to invest in authentication that protects approval rates. Banks and schemes are responding with enrollment growth in Click to Pay and deployment of passkeys, which reduce friction and secure card-not-present flows across the European credit card market. Continued wallet growth is expected, but cards retain foundational roles as rails for both domestic and cross-border transactions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: E-Commerce and Travel Anchor Growth, Yet Food Dominates the Share

Food & Groceries held 26.83% of the 2025 value, which reflects the category’s essential nature and broad in-store acceptance, while e-commerce groceries expand click-and-collect and delivery payments that reinforce card usage patterns. Travel & Tourism is set to be the fastest-growing, supported by revived international arrivals and spending, as well as a healthy business travel outlook that sustains premium features and category-specific rewards. The European credit card market benefits from the return of cross-border flows and the mix shift toward transportation, dining, and entertainment spend that spreads card activity across multiple travel-linked merchant categories. Online media, consumer electronics, and restaurants keep stable shares as households embed repeat digital purchases and on-premises spending supported by cards and tokenized credentials that improve approval rates and fraud control. With cards anchoring 40% of e-commerce and 63% of in-store transactions by value in 2022, issuers are positioned to grow with the breadth of everyday payments that define the European credit card market.

The European credit card market size for Travel & Tourism is projected to expand at a 4.83% CAGR by 2031, and this is reinforced by premium card benefits that match evolving traveler needs in insurance, lounge access, and flexible redemptions. Business travel recovery into 2026 supports corporate card demand, expense tools, and stronger underwriting supported by real-time controls and data-rich reporting, which deepens issuer ties with enterprises and SMEs. Co-brand partnerships continue to surface in travel corridors that combine destination networks, acceptance reach, and multilingual service layers for visitors, as seen in the European Travel Commission-Mastercard-ICBC card. E-commerce-linked applications stay resilient as tokenization and passkeys reduce checkout friction and sustain card-on-file relationships within subscription and content ecosystems. Overall, application diversity and strong acceptance underpin persistent activity in the European credit card market across everyday and discretionary categories.

By Card Type: General-Purpose Dominance Masks Specialty Acceleration

General-purpose Credit Cards accounted for 91.14% of the 2025 value, which reflects the breadth of bank issuance and the reach of global acceptance that secures cross-border transactions and standard rewards frameworks. Specialty & Other Credit Cards are projected to grow faster at a 5.12% CAGR through 2031, as issuers extend co-brands and embedded finance credentials into vertical software platforms and affinity communities that prize tailored benefits and controls. Mastercard’s expansion of tokenization, Click to Pay, and passkeys across Europe enables both general-purpose and specialty portfolios to improve security and conversion in digital journeys for the European credit card market. Enterprise and SME spending needs are attracting more attention in specialty programs built with commercial features, usage restrictions, and automated reporting, which match stricter budgeting and compliance standards. Personalization trends across card form factors, materials, and packaging continue to lift acquisition and spend per user, which supports growth in both mainstream and niche portfolios of the European credit card market.

The European credit card market benefits from specialty programs that target travel, mobility, and benefits use cases, because these products monetize beyond interchange through insurance, FX, and subscription fees. European travel-focused co-brands that link destination support with multilingual service suggest new paths for targeting international visitor segments, which adds volume and retention for issuers running dual portfolios. Visa’s partnerships with major European banks also reinforce general-purpose issuance and control more end-customer journeys as debit, credit, and co-brands align under a common acceptance umbrella. As issuers expand capabilities through network and processor relationships, specialty cards can justify premium pricing, while general-purpose cards remain the gateway for broad consumer coverage across the European credit card market. This twin-track approach defends share while enabling targeted growth in high-yield verticals that prize tailored features and flexible integrations. Over the forecast period, general-purpose incumbency is likely to hold, while specialty expansion outpaces in growth terms based on use-case depth and monetization options.

By Card Format: Physical Incumbency Challenged by Digital Velocity

Physical cards maintained 81.92% of the 2025 value, reflecting long-standing acceptance and the comfort many consumers have with tangible credentials for in-store and travel purchases. Digital cards are projected to grow at a 5.63% CAGR to 2031 as instant issuance, wallet provisioning, and granular spend controls are expected features in several European markets, especially in the Nordics. Tokenization and Click to Pay are scaling across markets and support in-app and web purchases with better approval performance, lower fraud, and less friction, which cement card rails inside digital wallets for the European credit card market. Consumer and merchant preferences still favor cards, which protects the relevance of both physical and digital credentials even as wallets gain share. With passkeys and similar security improvements becoming more common, issuers now complement physical programs with robust digital twins that drive high-frequency usage within the European credit card market.

The European credit card market size for Digital cards is forecast to grow in tandem with wallet adoption and merchant support for invisible checkout, while physical cards hold their share through trust, ubiquity, and offline utility. Issuers are also differentiating physical experiences through card materials, eco-options, tactile accessibility, and biometric form factors that reinforce product value and retention. EU-level guidance on digital payments and authentication helps standardize experiences across markets, which supports cross-border travel and e-commerce for cardholders who expect consistent identity and security journeys. Over time, physical and digital coexist as complements, with virtual credentials powering online subscriptions and one-time e-commerce, while physical cards carry in-store and travel tasks that benefit from a tangible form factor. Together, they keep the European credit card market resilient across varied channels and customer preferences.

By Provider: Visa Leads, Yet Mastercard Grows Faster Amid Sovereign Push

Visa led providers with 51.34% in 2025, anchored by deep bank relationships and broad acceptance across cross-border corridors that keep mainstream portfolios active. Mastercard is projected to grow fastest at a 5.94% CAGR through 2031, supported by strong momentum in tokenization, Click to Pay, and passkeys that lift approval performance and reduce friction across European markets in the European credit card market. Bank partnerships reinforce both networks’ positions, as seen in Commerzbank’s expanded agreement that makes Visa the preferred card partner and aligns Girocard with Visa debit functionality for international and online transactions. Card-enabled benefits and mobility solutions expand with issuers and payments partners, which intensifies ecosystem roles for networks as they provide commercial capabilities and risk services that complement acceptance. Scheme-neutral initiatives also advance, with European institutions and banks exploring options to reinforce sovereignty and provide shared rails for digital payments that can integrate with e-commerce over time.

The European credit card market share held by Visa reflects its embedded position in large issuers’ portfolios and enduring cross-border acceptance, while Mastercard’s growth vector aligns with its value-added services and authentication rollout across numerous European markets. European banking groups also highlight collaborative efforts to improve domestic and regional digital-payment options in areas like e-commerce, which complements rather than displaces global card rails in the near term. As issuers and networks execute on convergence between security, data, and acceptance, providers aim to secure both share and growth despite interchange ceilings. Over the forecast period, provider dynamics will likely balance incumbency with innovation, and both major networks appear positioned to defend and expand key use cases in the European credit card market.

Geography Analysis

The United Kingdom accounted for 24.45% of the European credit card market share in 2025, supported by high online shopping participation and mature digital adoption that helps sustain card volumes in both e-commerce and in-store payments. United Kingdom consumers report strong usage of online services within the 16 to 74 age group, which aligns with a deeper base of card-on-file credentials and active recurring payments. Cross-border travel and business spend recovery reinforce premium issuance for corporate and high-value leisure segments, which keeps rewards and insurance features central to portfolio strategies into 2026. Regulatory attention on cross-border online card fees and broader instant-payment policy watchlists adds complexity for issuers, who respond with tokenization and authentication improvements to protect approval outcomes in the United Kingdom context. The European credit card market in the United Kingdom remains resilient as networks and issuers focus on frictionless checkout and identity solutions that translate across channels.

Germany and France sustain large contributions to the European credit card market due to population scale, economic strength, and continued digitization of retail and services. Germany’s banking partnerships emphasize broad acceptance and international reach, highlighted by Commerzbank’s strategic alignment with Visa that extends debit functionality for online and cross-border transactions and supports new credit products from 2026. France shows a mature pattern where cards hold meaningful shares of online and in-person transactions, and domestic schemes continue to play an important role alongside global networks in anchoring acceptance. EU-level oversight points to wallet growth by 2026 in both online and in-store use, which makes tokenized credentials even more important as a bridge between wallets and card rails across these large markets. Together, these countries leverage stable merchant acceptance and expanding digital uptake, which sustains issuer engagement and product innovation for the European credit card market.

Spain is forecast as the fastest-growing geography at a 5.81% CAGR to 2031, with tourism-driven recovery and rising digital adoption improving the base for card activity in travel and retail. Broader European travel spending trends favor markets with strong destination appeal, and that supports category-specific card usage tied to hospitality, mobility, and entertainment throughout 2026. BENELUX builds regional digital-payment initiatives and bank-led collaborations that aim to enhance e-commerce flows while keeping strong links to card rails for acceptance and risk controls. The Nordics maintain leadership in e-shopping participation and digital wallets, which is consistent with high expectations for instant issuance, granular controls, and frictionless wallet experiences that keep card credentials central to repeated usage in the European credit card market. Across the Rest of Europe, rising e-commerce engagement and cross-border travel trends contribute to a larger base of card-on-file relationships and in-store adoption, which set conditions for steady growth through the forecast period. The geography mix, therefore, provides both scale and speed components that reinforce the European credit card market.

Mordor Intelligence tracks the credit cards market with additional country-level coverage spanning Japan, Hong Kong, Israel, and Canada, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Network incumbency, bank partnerships, and ecosystem alliances define competitive dynamics in the European credit card market as issuers pursue growth within regulated economies. Visa retained a leading provider position in 2025, supported by established bank ties, while Mastercard’s projected faster growth reflects traction in tokenization, passkeys, and Click to Pay expansion that lifts digital approvals across Europe. Commerzbank’s extended partnership with Visa underlines bank-network collaboration to strengthen international and online acceptance for customers and prepare new debit and credit launches from 2026. Edenred’s agreement with Visa shows ecosystem participants tapping network capabilities for benefits, mobility, and B2B solutions that rely on card rails and commercial features. These ties extend reach and service depth as providers seek to differentiate through security, analytics, and embedded finance in the European credit card market.

Issuers and processors are investing in platform modernization and AI-enhanced operations to improve resilience, risk control, and onboarding efficiency. Worldline’s 2030 transformation plan targets platform consolidation, AI-driven operations, and stronger free cash flow, which aligns its merchant services and issuing capabilities with a long-term runway that complements card acceptance. Mastercard and bank partners are pushing checkout transformation that advances tokenization and authentication across web and app flows to reduce fraud and protect approval rates across the European credit card market. Bank issuers continue to target digital-first opportunities, with challengers and regionals launching card programs that emphasize self-serve controls and integration into billing and accounting, as seen with product rollouts into Germany by Nordic players. Across this landscape, the balance of innovation and compliance remains central to defending share and improving unit economics in the European credit card market.

European institutions and banks are also exploring regional payment initiatives to enhance sovereignty while coexisting with global networks. The ECB has underscored the importance of European control over key payment infrastructures and the need for innovation to keep pace with global platforms while integrating with existing rails used by consumers and merchants. Large banking groups highlight partnerships designed to strengthen e-commerce support and regional interoperability, which can feed future wallet and instant-payment developments that still rely on card credentials for reach and risk services. In the near term, tokenization gains, bank-network deals, and portfolio modernization are likely to drive market outcomes more than new schemes, which stabilizes competition around user experience, data, and security. Consequently, incumbents and their partners will continue to defend and extend the European credit card market through trusted rails embedded in evolving digital fronts.

Europe Credit Cards Industry Leaders

Visa Inc.

Mastercard Inc.

American Express Co.

Cartes Bancaires CB

Bancontact Payconiq Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The European Travel Commission, Mastercard, and ICBC launched a European Travel co-branded credit card targeting Chinese visitors, combining destination support with Mastercard’s global acceptance and ICBC’s cross-border financial capabilities to simplify travel spend across Europe.

- October 2025: Edenred and Visa announced a strategic partnership to accelerate innovation in Benefits & Engagement, Mobility, and B2B Payment Solutions, certifying Edenred’s in-house issuing and processing infrastructure with Visa Europe and enabling new virtual payment products across multiple activities from early 2026.

- March 2025: Instabank launched a fully digital credit card in Germany in collaboration with Visa and several fintech partners, enabling self-managed portfolios, flexible card issuance, and usage restrictions aligned with business needs and digital-first consumer expectations.

- February 2025: Commerzbank and Visa expanded their long-term partnership to equip Girocards with Visa debit functionality for international and online purchases and to introduce new Visa debit and credit cards for retail customers from 2026, alongside tailored solutions for business and corporate clients.

Europe Credit Cards Market Report Scope

A credit card is a financial product issued by banks, enabling customers to borrow funds within a pre-approved limit. It facilitates transactions for goods and services. The issuer determines the credit limit based on factors such as the customer’s income and credit score.

The Europe credit card market report is segmented by application (food & groceries, health & pharmacy, restaurants & bars, consumer electronics, media & entertainment, travel & tourism, other applications), card type (general purpose credit cards, specialty & other credit cards), card format (physical, digital), provider (visa, mastercard, other providers), and geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). The market forecasts are provided in terms of value (USD).

| Food & Groceries |

| Health & Pharmacy |

| Restaurants & Bars |

| Consumer Electronics |

| Media & Entertainment |

| Travel & Tourism |

| Other Applications |

| General Purpose Credit Cards |

| Specialty & Other Credit Cards |

| Physical |

| Digital |

| Visa |

| Mastercard |

| Other Providers |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX |

| NORDICS |

| Rest of Europe |

| By Application | Food & Groceries |

| Health & Pharmacy | |

| Restaurants & Bars | |

| Consumer Electronics | |

| Media & Entertainment | |

| Travel & Tourism | |

| Other Applications | |

| By Card Type | General Purpose Credit Cards |

| Specialty & Other Credit Cards | |

| By Card Format | Physical |

| Digital | |

| By Provider | Visa |

| Mastercard | |

| Other Providers | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected size and growth rate for the European credit card market by 2031?

The European credit card market size is projected to reach USD 1.23 trillion by 2031, growing at a 4.24% CAGR from 2026 to 2031.

Which application category is set to grow the fastest through 2031 in Europe?

Travel & Tourism is projected to be the fastest-growing application at a 4.83% CAGR, supported by recovering cross-border travel and business spend.

Which provider currently leads in Europe, and who is growing faster?

Visa led providers with 51.34% in 2025, while Mastercard is projected to post the fastest growth at a 5.94% CAGR through 2031.

How is wallet adoption affecting card usage across Europe?

Wallets are gaining share online and in-store, yet tokenized card credentials still anchor many wallet transactions, keeping cards central to digital checkout.

What regulatory factor most affects issuer economics in Europe?

The Interchange Fee Regulation that caps consumer credit interchange at 0.30% compresses margins and pushes issuers toward value-added services and authentication-led improvements.

Which country held the largest share of Europe's credit card activity in 2025?

The United Kingdom accounted for 24.45% in 2025, supported by high online shopping participation and mature digital adoption.

Page last updated on: