Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

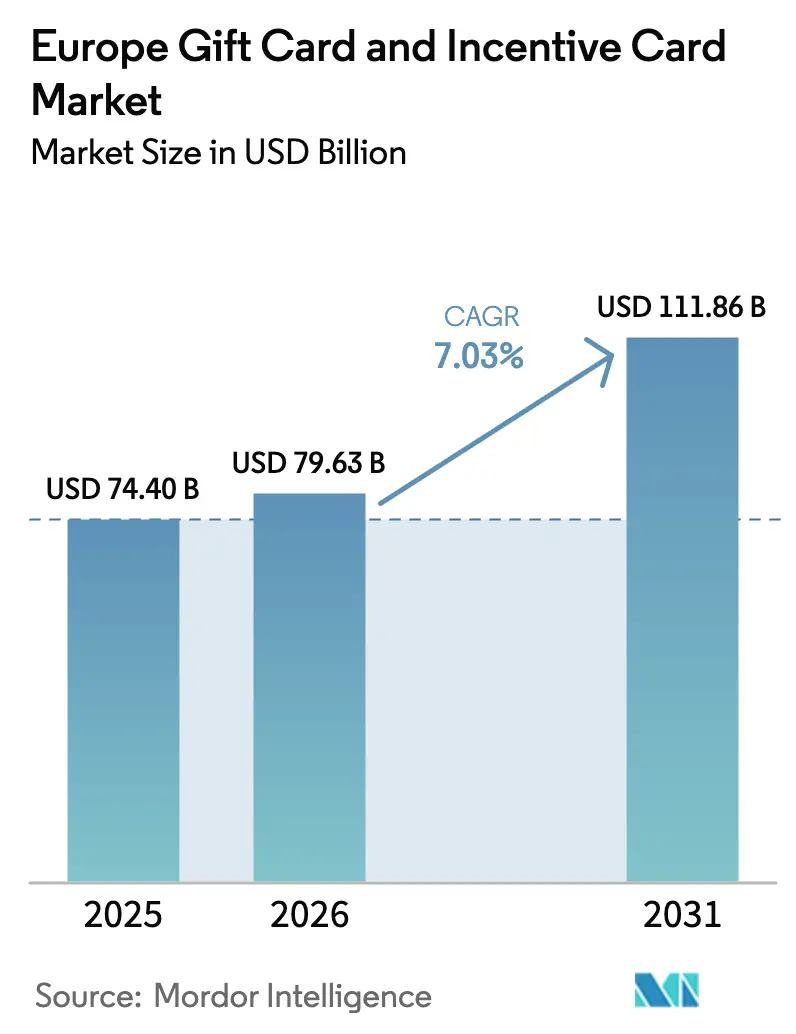

| Base Year Market Size (2025) | USD 74.40 Billion |

| Market Size (2026) | USD 79.63 Billion |

| Market Size (2031) | USD 111.86 Billion |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Gift Card And Incentive Card Market Analysis by Mordor Intelligence

The European gift card and incentive card market size was valued at USD 74.40 billion in 2025 and estimated to grow from USD 79.63 billion in 2026 to reach USD 111.86 billion by 2031, at a CAGR of 7.03% during the forecast period (2026-2031). An expanding digital-payment ecosystem, widespread mobile-wallet acceptance, and instant-payment rails anchor this growth path. Corporate incentive budgets remain the largest revenue engine, yet Gen-Z self-use and budgeting habits add a steady, non-seasonal layer of demand. PSD3 and the EU Digital Identity Wallet streamline KYC and enable instant top-ups, partially offsetting new EUR 150 value caps for anonymous prepaid loads. Municipal multi-merchant schemes and pan-European payment initiatives further expand addressable volumes by reducing cross-border frictions inside the European gift card and incentive card market. Competitive intensity is moderate: scale incumbents exploit pan-regional settlement infrastructure, while API-first fintechs target niche use cases and geography gaps to win share.

Key Report Takeaways

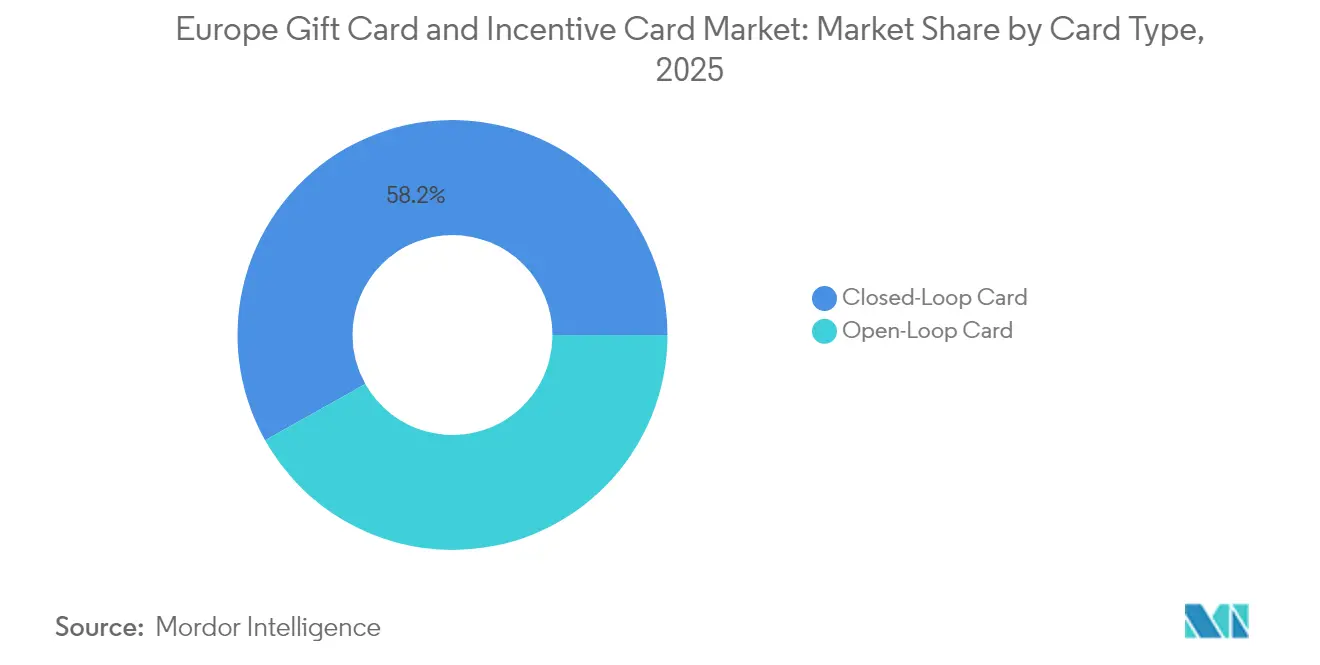

- By card type, closed-loop products held 58.15% of the Europe gift card and incentive card market share in 2025, while open-loop formats in the Europe gift card and incentive card market are projected to expand at a 8.78% CAGR to 2031.

- By format, digital cards captured 57.80% of the Europe gift card and incentive card market size in 2025, and digital issuance across the Europe gift card and incentive card market is expected to advance at a 10.12% CAGR over the forecast period.

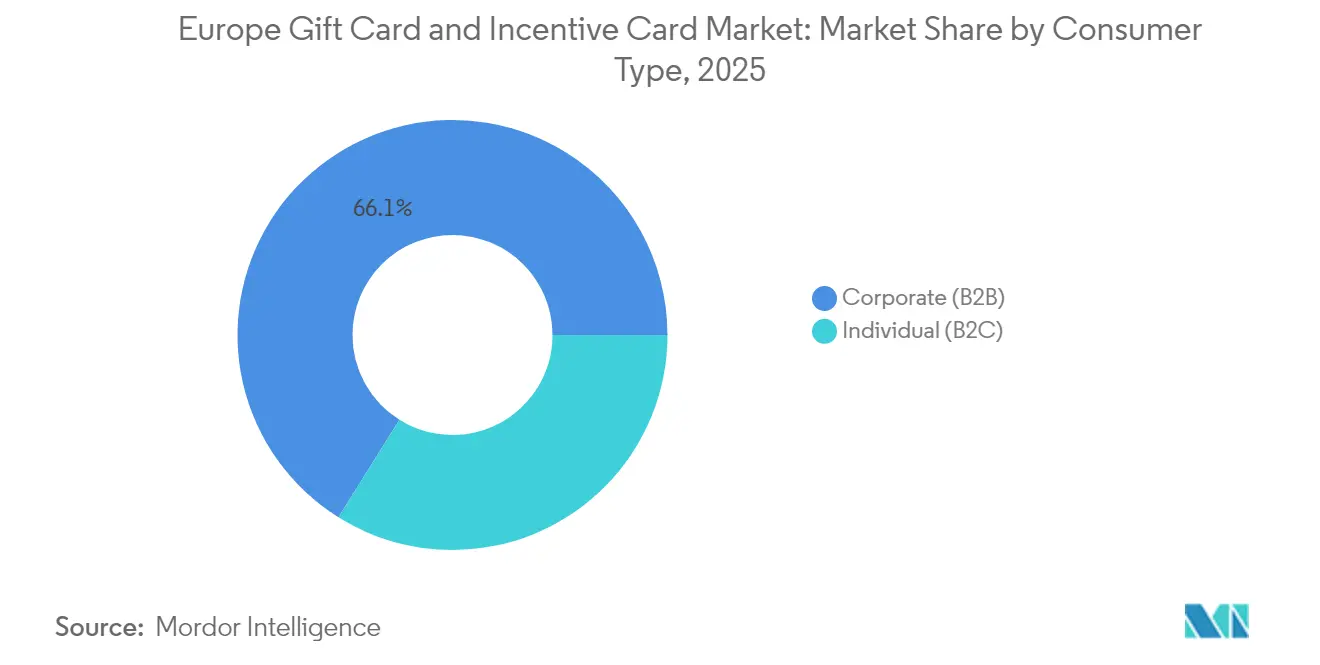

- By consumer type, the corporate B2B segment commanded 66.10% of the Europe gift card and incentive card market in 2025, whereas individual B2C demand within the Europe gift card and incentive card market is growing fastest at an 8.42% CAGR through 2031.

- By distribution channel, online sales accounted for 61.90% of the Europe gift card and incentive card market size in 2025, and online penetration in the Europe gift card and incentive card market is rising at a 11.75% CAGR.

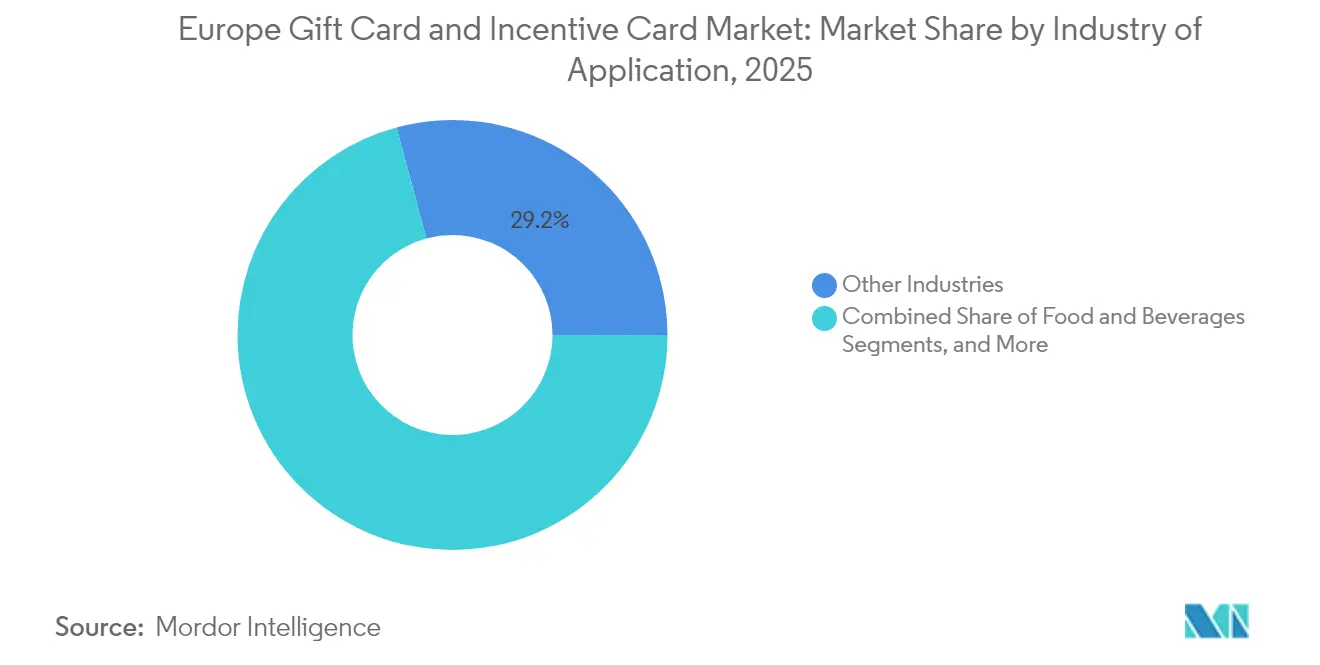

- By industry application, the other industries segment held a 29.20% of the Europe gift card and incentive card market size in 2025, whereas consumer electronics leads growth in the Europe gift card and incentive card market, registering a 10.05% CAGR to 2031 and outpacing traditional categories such as food & beverages.

- By country, the United Kingdom dominated with 23.30% revenue share of the Europe gift card and incentive card market in 2025, while Spain is the fastest-growing national segment of the Europe gift card and incentive card market at a 9.10% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Gift Card And Incentive Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce & mobile-wallet proliferation | +1.8% | Global, Nordic leadership | Medium term (2–4 years) |

| Corporate incentive program scaling | +2.1% | DACH, Benelux, Nordics | Long term (≥ 4 years) |

| Gen-Z self-use & budgeting adoption | +1.2% | Urban EU markets | Medium term (2–4 years) |

| Municipal “local town” multi-merchant cards | +0.7% | Belgium, Netherlands first-movers | Long term (≥ 4 years) |

| PSD3 & EU Digital ID instant top-ups | +1.4% | EU-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce & Mobile-Wallet Proliferation

Mobile commerce now drives a growing share of online checkouts, and contactless payments dominate point-of-sale volumes across the Nordics[1]Ecommerce Europe, “European E-commerce Report 2024,” Ecommerce Europe, ecommerce-europe.eu. As wallets gain ubiquity, consumers increasingly perceive stored-value gift cards as a frictionless extension of everyday payment habits. Tokenized redemption removes checkout barriers and encourages spontaneous gifting, especially on cross-border sites where traditional cards incur higher FX fees. Retailers benefit from lower chargeback rates and richer data streams, bolstering loyalty integrations and reinforcing sustained momentum within the Europe gift card and incentive card market.

Corporate Incentive Program Scaling

European employers facing tight labor markets allocate larger non-cash reward budgets. Digital gift cards deliver measurable engagement, tax efficiency, and instant distribution at scale. Integration with HRIS and ERP platforms allows automated loading, real-time spend tracking, and multi-country compliance. Edenred’s pan-regional acquisitions exemplify a land-and-expand strategy designed to deepen wallet share across client portfolios[2]Edenred, “Full-Year 2024 Results,” Edenred, edenred.com. Strong average order values and recurring cycles stabilize revenue flows and extend the corporate segment’s dominance in the Europe gift card and incentive card market.

Municipal “Local Town” Multi-Merchant Cards

Belgian and Dutch municipalities issue prepaid cards restricted to local post codes, funneling consumer euros into neighborhood SMEs and tracking economic impact through anonymized redemption data. Merchants welcome guaranteed footfall, and city councils leverage ESG narratives to secure EU cohesion fund grants. Fintech operators gain subsidized marketing and an early seat at future stimulus rounds, positioning the Europe gift card and incentive card market for deeper public-sector integration over the long term.

PSD3 & EU Digital ID Wallet-Enabled Instant Top-Ups

PSD3 elevates instant credit transfers, harmonizes data-access rules, and lowers authentication frictions, while the EU Digital Identity Wallet pilots bundle biometric IDs with payment credentials. Gift card issuers can embed “top-up now” buttons that pull verified IBANs directly, eliminating card-scheme costs and reducing fraud exposure. Visa’s participation in the 80-member pilot signals mainstream backing for the initiative. The convergence of regulatory and technology upgrades widens cross-border acceptance and further scales the Europe gift card and incentive card market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital gift-card fraud & chargebacks | -0.8% | High-volume markets | Short term (≤ 2 years) |

| KYC/AML value-cap constraints | -0.6% | EU-wide | Medium term (2–4 years) |

| Impending Digital Euro & Wero scheme substitution risk | -1.1% | Eurozone core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Gift-Card Fraud & Chargebacks

Fraud rings exploit rapid code delivery and anonymous loads, causing direct issuer losses and regulatory scrutiny. Mastercard’s ScamClassifier categorizes emerging attack vectors and highlights the speed at which criminals pivot toward new channels. While advanced analytics mitigate risks, smaller providers face resource constraints, and heightened fraud chatter can temper consumer appetite in the Europe gift card and incentive card market.

Impending Digital Euro & Wero Scheme Substitution Risk

The ECB’s planned Digital Euro, capped at EUR 1,500–2,500 per wallet, aims to facilitate small-ticket retail payments[3]European Central Bank, “Digital Euro – Preparation Phase Progress Update,” European Central Bank, ecb.europa.eu. In parallel, the Wero consortium’s instant SCT-Inst network challenges international scheme dominance. Both could displace basic stored-value use cases, yet branded promotions and analytics-rich loyalty functions offer defensible niches for gift card providers inside the Europe gift card and incentive card market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Card Type: Closed-Loop Dominance Faces Open-Loop Innovation

Closed-loop cards generated 58.15% of the Europe gift card and incentive card market size in 2025, capitalizing on retailer loyalty integrations and predictable redemption flows. However, open-loop formats are expected to post a 8.78% CAGR over the forecast period as cross-border shoppers and remote workers value universal acceptance. Mastercard tokenization upgrades narrow perceived fraud gaps and boost merchant acceptance, reinforcing open-loop momentum across the Europe gift card and incentive card market.

Retailers counter with enhanced closed-loop perks—tiered cashback, bonus credit events, and app-native gamification—that elevate lifetime value. Fintech aggregators now embed both card types in unified catalogs, letting corporate clients toggle based on workforce dispersion, tax treatment, and redemption analytics. As EU Digital ID wallets go live, cross-border acceptance gaps shrink, further redefining share dynamics.

By Format Type: Digital Cards Achieve Critical Mass

Digital issuance surpassed physical cards in 2025, capturing 57.80% of the Europe gift card and incentive card market size and is projected to expand at 10.12% CAGR. Environmental targets, instant delivery expectations, and mobile-wallet storage drive this inflection. QR codes, NFC passes, and printable e-wrappers combine convenience with sharable aesthetics. Physical variants still resonate where tactile gifting matters, yet rising parcel fees and plastic-waste regulations keep the pendulum firmly in digital’s favor.

Gamified balance-boost campaigns and AI-derived purchase prompts further lift redemption velocity. Providers redeploy savings from reduced printing into richer customer-service chatbots and localized language support, sharpening their competitive edge within the Europe gift card and incentive card market.

By Consumer Type: Corporate Segment Drives Value Creation

Corporate buyers accounted for 66.10% of the Europe gift card and incentive card market size; bulk procurement cycles linked to onboarding kits and seasonal spot bonuses underpin resilient demand. Real-time API issuance reduces HR workload across multi-country entities and provides audit-ready spend reports. Individual B2C usage, fueled by Gen-Z self-budgeting, grows at 8.42% CAGR, lengthening average redemption cycles and flattening the once-pronounced holiday spike inside the Europe gift card and incentive card market.

By Distribution Channel: Online Channels Capture Digital Transformation

Online portals held 61.90% of the Europe gift card and incentive card market size in 2025 and are climbing at 11.75% CAGR. Direct API distribution to BNPL apps, neobanks, and e-commerce checkouts extends reach with negligible marginal cost. Offline supermarket racks and petrol stations still attract impulse purchasers, but footfall momentum migrates toward click-and-collect models that pair e-purchases with in-store pick-up, sustaining a hybrid path for future growth.

By Industry Application: Consumer Electronics Emerge as Growth Leader

The other industries segment held 29.20% of the Europe gift card and incentive card market size in 2025. Consumer electronics outpace all verticals with a 10.05% CAGR, reflecting high average selling prices and tech-savvy employee rewards. Retailers preload gift cards ahead of flagship product releases, locking in demand and smoothing supply planning cycles. Travel, entertainment, and professional-services segments maintain solid single-digit trajectories through loyalty tie-ins and promotional bundles, reinforcing the Europe gift card and incentive card market’s sector diversity.

By Country: UK Leadership Meets Spanish Acceleration

The United Kingdom retained 23.30% of the Europe gift card and incentive card market size in 2025, benefiting from established corporate-benefit cultures and mature open-banking rails. Spain leads growth at 9.10% CAGR as smartphone penetration converts cash-heavy shoppers into wallet users. Germany, France, and Italy deliver scale with steady regulation-aligned growth, while Benelux and Nordic regions pioneer instant-payment integrations that influence broader market standards across the Europe gift card and incentive card market.

Geography Analysis

The United Kingdom’s digital infrastructure, high contactless usage, and HR perk adoption anchor its leadership. Post-Brexit rules oblige issuers to maintain dual compliance tracks, yet FCA consumer-duty requirements bolster customer confidence and maintain spend volumes. Spain’s e-commerce boom coincides with favorable tax treatment on meal and mobility vouchers, bolstering digital card penetration. French corporates expand voucher-to-cash-out options, while German surveys highlight consumer readiness for CBDC-adjacent products, hinting at potential cannibalization but also smoother adoption of innovative stored-value features.

Benelux markets leverage instant-payment orchestration: Belgium’s SCT Inst usage demonstrates settlement speed that helps issuers offer real-time top-ups. Nordic nations, though smaller in absolute value, lead Europe in per-capita card loads, creating a living lab for biometric wallet redemption and subscription-linked auto-reloads. Collectively, regional variances require layered go-to-market strategies, reinforcing the complexity and opportunity within the European gift card and incentive card market.

Competitive Landscape

The Europe gift card and incentive card market displays moderate concentration: Edenred, Sodexo, Blackhawk Network, WeGift, and InComm together control a considerable share of the market. Edenred’s acquisitions in Denmark and Brazil expand catalog depth and cross-sell potential. Sodexo pilots multispend “choice cards” that let workers toggle meal, mobility, and wellness allowances, tightening user engagement loops. Blackhawk Network embeds instant-issue codes into online grocery checkouts to raise basket sizes. API-first insurgents such as Tango Card and WeGift build white-label issuance rails for neobanks, leveraging rapid integration to undercut legacy pricing. The 16-bank Wero consortium’s planned fee-light instant-payment framework aims to disintermediate international card schemes, promising cost relief for high-volume gift card issuers.

Crypto-forward providers like Bitrefill convert digital assets into merchant balances, attracting speculative-asset holders and gaming communities. Hospitality-focused MyBeezBox packages experiences for hotels seeking ancillary revenue streams. Incumbents respond with machine-learning fraud controls that smaller rivals struggle to fund, preserving a scale-based moat even as API commoditization intensifies competition across the Europe gift card and incentive card market.

Europe Gift Card And Incentive Card Industry Leaders

Edenred

Sodexo

Blackhawk Network

InComm Payments

WeGift

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Mastercard introduced ScamClassifier, a framework targeting digital-payment fraud.

- April 2025: Hogan Lovells detailed PSD3 and DORA timelines relevant to payment providers.

- January 2025: The EU Digital Identity Wallet Consortium released an RFC to refine payment integration across 26 Member States, with Visa among 80+ participants in live pilots.

- September 2024: Sixteen European banks formed Wero, acquiring iDeal and Payconiq to build an SCT Inst-driven payment alternative.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European gift card and incentive card market as the value of all open and closed loop payment cards issued in physical or digital form that are purchased for consumer gifting, employee rewards, or promotional incentives across retail and service categories in 32 European economies. These cards hold a stored monetary value that can be redeemed at a single merchant or a network of merchants and can be re-loaded, topped up, or delivered instantly via mobile wallets.

Scope exclusion: prepaid payroll, remittance, and multi-currency travel cards fall outside this assessment.

Segmentation Overview

- By Card Type

- Open-Loop Card

- Closed-Loop Card

- By Format Type

- Digital Card

- Physical Card

- By Consumer Type

- Individual (B2C)

- Corporate (B2B)

- By Distribution Channel

- Online

- Offline

- By Industry of Application

- Food and Beverages

- Health, Wellness, and Beauty

- Apparel, Footwear, and Accessories

- Consumer Electronics

- Other Industries

- By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Interviews with gift card program managers, HR reward specialists, payment processors, and digital wallet providers across the United Kingdom, Germany, France, Spain, Nordics, and Benelux clarified corporate budget outlooks, average incentive denominations, and expected PSD3 impacts. Follow-up surveys with small retailers and neobanks filled data gaps on instant issuance costs and cross-border uptake, letting us fine-tune digital versus physical mix assumptions.

Desk Research

Mordor analysts first reviewed macro datasets from Eurostat, the European Central Bank's Retail Payments Statistics, and national payments supervisors such as BaFin and the FCA to anchor transaction volumes and card reload behavior. Trade bodies, including the Gift Card & Voucher Association and Incentive Research Foundation, offered adoption ratios and average load values by channel. We drew financial disclosures and investor decks from leading retailers, fintech issuers, and prepaid program managers for redemption rates and breakage trends. Paid databases like D&B Hoovers (issuer financials) and Dow Jones Factiva (deal flow) helped size revenue pools and check market developments. The sources cited above are illustrative only, and many additional publications informed desk validation.

Market-Sizing & Forecasting

A top-down construct converts national consumer spending, e-commerce turnover, and corporate incentive budgets into a gift card addressable pool, which is then split by penetration rates validated through expert calls. Selective bottom-up roll-ups of issuer reported card loads and sampled average selling price by channel test and calibrate totals. Key variables include (1) average reload value per active card, (2) share of corporate incentive budgets allocated to cards, (3) digital card penetration in total issuance, (4) number of active mobile wallet users, and (5) cross-border e-commerce value. Multivariate regression ties these drivers to historic market growth and projects values to 2030, while scenario analysis reflects regulatory or macro shocks. Where bottom-up evidence is thin, variance bands are applied before the final figure is locked.

Data Validation & Update Cycle

Outputs are benchmarked against independent payment volume indicators and issuer earnings. An anomaly checklist flags outliers, triggering secondary analyst review and re-contact of sources when needed. Reports refresh yearly, with interim updates issued if material regulations, major mergers, or macro swings arise. A final pre-release sweep ensures clients receive the most current view.

Why Our Europe Gift Card and Incentive Card Baseline Commands Reliability

Published estimates often vary because providers choose different card types, face value limits, and refresh cadences. Our disciplined scope selection, transparent driver set, and annual update policy keep Mordor's baseline dependable for planners.

Key gap drivers versus other publishers include narrower open loop coverage, divergent base year currency conversions, and optimism baked into digital uptake curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 74.4 B | Mordor Intelligence | - |

| USD 75.4 B | Regional Consultancy A | open loop only partly modeled, limited corporate budget validation |

| USD 78.9 B | Trade Journal B | higher ASP progression, biennial refresh cadence |

These contrasts show that our balanced, variable based model offers a traceable midpoint that decision makers can rely on for budgeting and strategic moves.

Key Questions Answered in the Report

How large is the Europe gift card and incentive card market in 2026?

The Europe gift card and incentive card market generated USD 79.63 billion in 2026, reflecting sustained digital-payment momentum.

What is the growth outlook for the Europe gift card and incentive card market through 2031?

Forecasts indicate a 7.03% CAGR, lifting market value to USD 111.86 billion by 2031.

Which product format is growing fastest in the Europe gift card and incentive card market?

Digital cards are expanding at a 10.12% CAGR due to mobile-wallet integration, instant delivery, and ESG considerations.

Why does the corporate B2B segment dominate the Europe gift card and incentive card market?

Employers integrate gift cards into scalable benefit programs, giving the B2B lane 66.10% of the 2025 market size and providing recurring, high-ticket purchases.

What regulatory change will most impact the Europe gift card and incentive card market over the next two years?

PSD3 plus the EU Digital Identity Wallet will enable instant top-ups, harmonize authentication, and unlock seamless cross-border usage.

What role will the Digital Euro play in the Europe gift card and incentive card market?

A 2027 launch could substitute basic low-value transactions, but branded promotions, loyalty analytics, and corporate-reward functions keep gift cards competitively differentiated.

Page last updated on: