Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

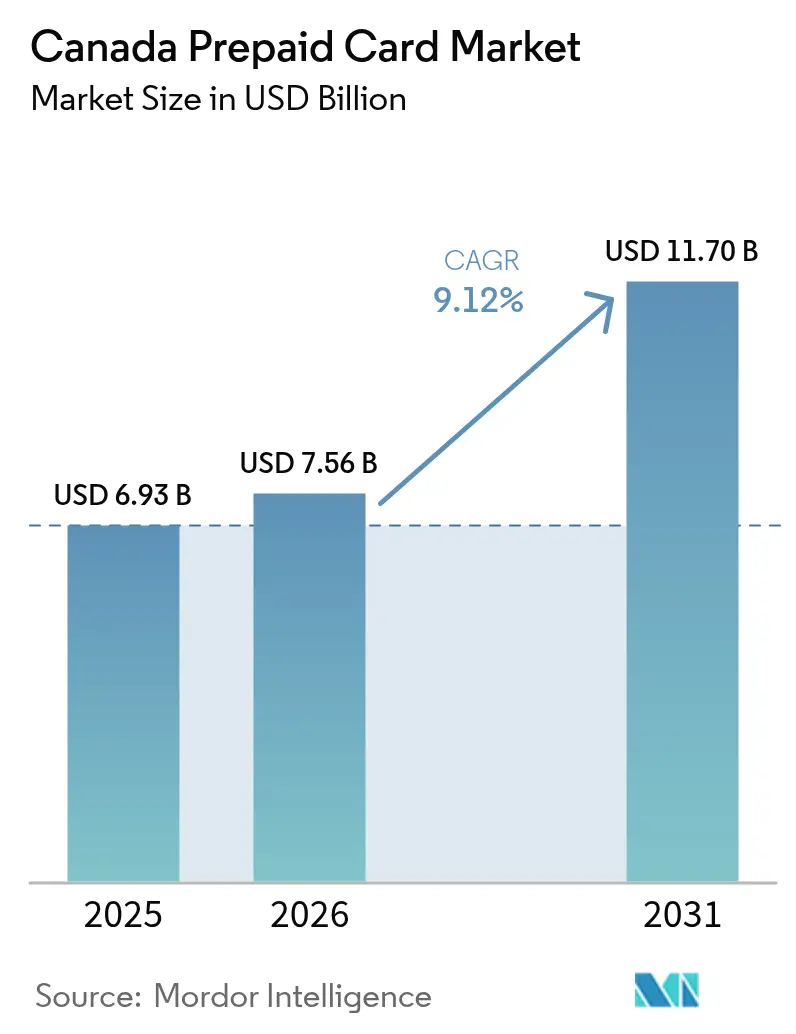

| Base Year Market Size (2025) | USD 6.93 Billion |

| Market Size (2026) | USD 7.56 Billion |

| Market Size (2031) | USD 11.7 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

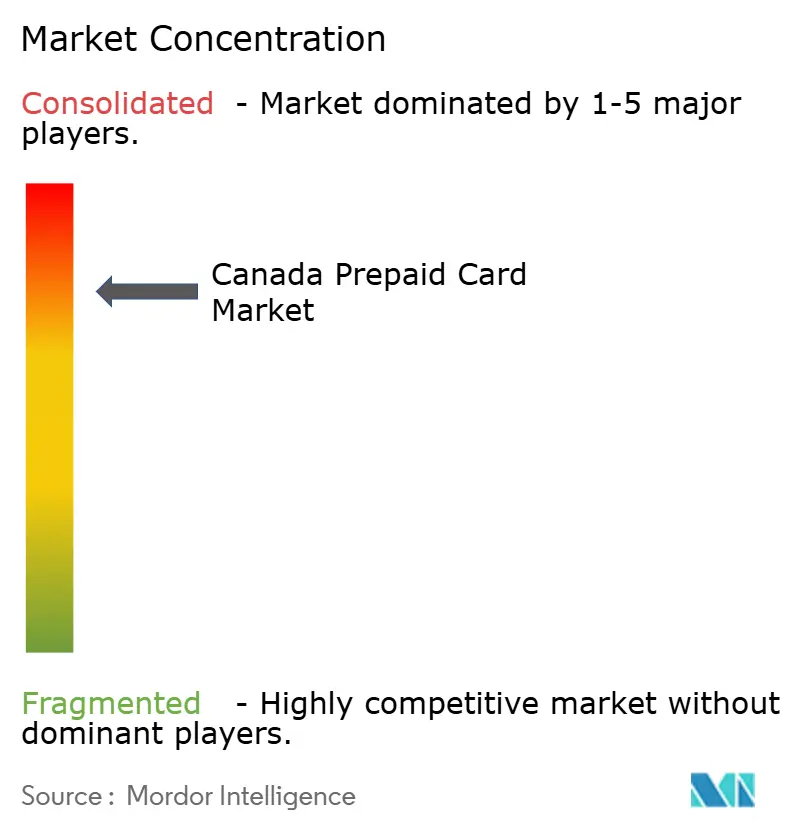

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Prepaid Card Market Analysis by Mordor Intelligence

Canada prepaid card market size in 2026 is estimated at USD 7.56 billion, growing from 2025 value of USD 6.93 billion with 2031 projections showing USD 11.7 billion, growing at 9.12% CAGR over 2026-2031. The measured expansion underscores a payments environment where prepaid products complement, rather than displace, mainstream banking channels. Rising smartphone penetration, sustained migration toward contactless behavior, and targeted government benefit digitization collectively underpin demand. Corporations seeking agile payout tools, gig-economy platforms offering instant wage access, and newcomers without established bank relationships also propel transactions. Concurrently, network tokenization and mobile-wallet provisioning broaden acceptance, positioning prepaid instruments as secure digital cash substitutes.

Key Report Takeaways

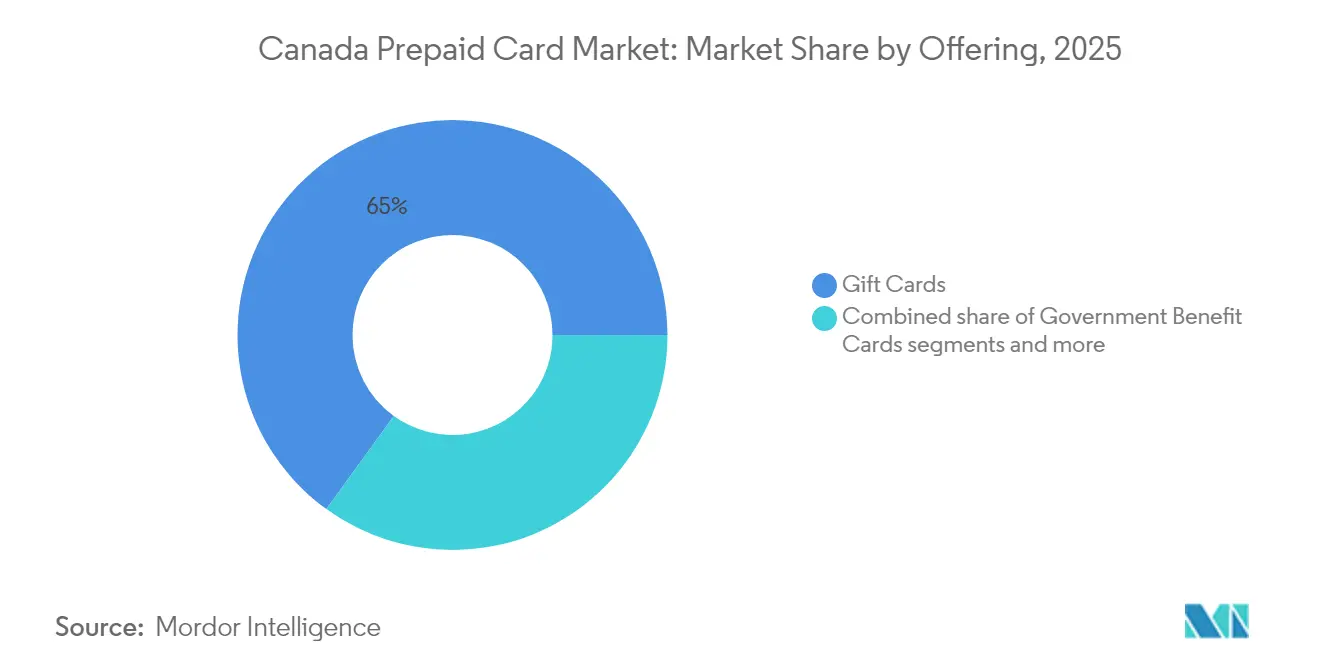

- By offering gift cards commanded 65.02% of the Canada's prepaid card market share in 2025; government benefit cards are projected to expand at a 12.43% CAGR through 2031.

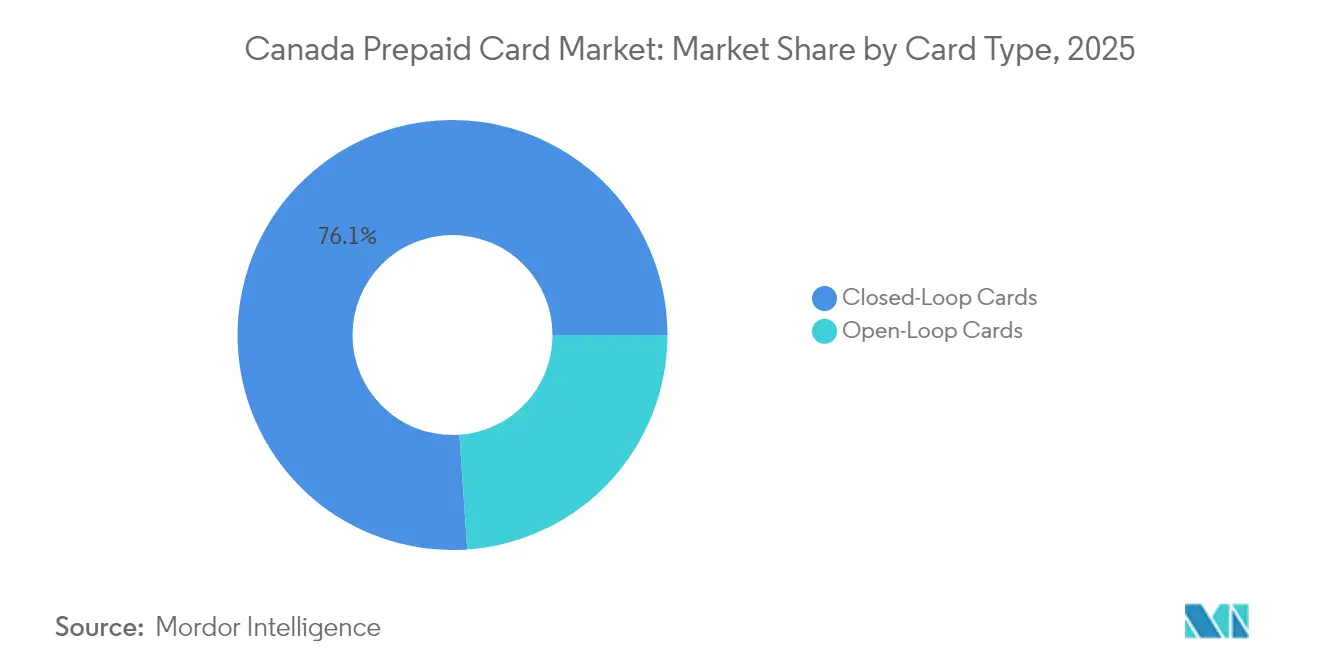

- By card type, closed-loop cards held 76.10% share of the Canada prepaid card market size in 2025, while open-loop cards record the highest forecast CAGR at 11.05% through 2031.

- By end user, retail applications accounted for 51.10% share of the Canada prepaid card market size in 2025 and corporate programs are advancing at a 10.05% CAGR to 2031.

- By geography, Ontario led with 44.52% share of the Canada prepaid card market size in 2025; Atlantic Canada is forecast to expand at a 9.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Prepaid Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first, cashless culture | +1.2% | National, strongest in urban centers | Medium term (2-4 years) |

| E-commerce & contactless post-COVID-19 | +0.9% | National, high in Quebec and Ontario | Short term (≤ 2 years) |

| Government benefit digitization | +0.8% | National, early gains in Alberta, Atlantic | Long term (≥ 4 years) |

| Fintech gig-payroll & neo-bank GPR cards | +0.7% | Urban centers, suburban expansion | Medium term (2-4 years) |

| Tokenization & mobile-wallet provisioning | +0.5% | National, fastest in metros | Short term (≤ 2 years) |

| Canada Post rural distribution | +0.3% | Rural & Indigenous, Northern Territories | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Digital-First, Cashless Payments Culture

Card usage now dominates daily spending, with smartphone adoption at 90% and more than 44% of consumers actively placing prepaid credentials inside Apple Pay or Google Pay wallets. This new baseline of cash avoidance keeps the Canada prepaid card market firmly embedded in omnichannel routines, from in-store NFC taps to QR-enabled peer transfers. [1]Payments Canada, “Corporate Reports 2025,” payments.ca.. Younger cohorts, often credit-averse yet digitally fluent, gravitate to prepaid accounts that deliver real-time notifications and hard spending limits, enabling disciplined budgeting without the friction of legacy checking products. Financial institutions integrate branded prepaid issuers inside their broader mobile platforms, viewing the cards as cost-effective on-ramps that deepen data-driven engagement cycles and cross-selling opportunities. Tokenization elevates security, enabling issuers to limit exposure even when credentials sit in multiple wallets simultaneously, thereby enlarging merchant acceptance and reinforcing trust.

Accelerated E-Commerce and Contactless Adoption Post-COVID-19

A permanent behavioral reset followed pandemic restrictions; tap-to-pay interactions routinely exceed 80% of card-present volume in major metros, and e-commerce remains at least 25% above 2019 baselines. The Canada prepaid card market gains because contactless functionality now ships as standard on prepaid plastics, closing a former parity gap with debit. At physical merchants, prepaid cards transact at the same interchange tiers as debit, eliminating point-of-sale hesitancy once associated with “gift card only” stigma. Online, users seamlessly load virtual prepaid accounts into merchant wallets, bypassing legacy 16-digit data entry. Retailers adopt open-loop gift solutions to attract international tourists who prefer prepaid for foreign travel budgeting. The convergence of in-store tap and online click eliminates friction, widening prepaid’s relevance across every shopping scenario.

Government Benefit Digitization & Modernized Disbursement

Federal and provincial ministries have prioritized cost-efficient, traceable electronic benefit delivery. When the Canada Revenue Agency upgraded MyAccount services, it embedded direct-to-card disbursement rails that instantly load refunds onto government-issued prepaid Visa cards. Alberta’s Employment Ministry replicates the model, distributing energy rebates on provincially branded prepaid products. Administration savings reach double-digit percentages due to reduced paper check printing and reconciliation, while beneficiaries receive funds days sooner, anchoring the Canada prepaid card market in social policy infrastructure. Long-term mandates under the Retail Payment Activities Act formalize registration rules, drawing fintech partners into multi-year benefit delivery tenders that guarantee transaction volumes well into the next decade.

Fintech-Driven Gig-Payroll & Neo-Bank GPR Card Programs

Platform economies rely on real-time liquidity. Uber and Lyft drivers can access daily earnings via Payfare-issued Mastercard debit credentials, fueling recurring load activity that advances the Canada prepaid card market. KOHO Financial amplified reach by linking postal branches to its MyMoney Account, giving cash-reliant Canadians a physical top-up route alongside in-app reload. Funding rounds topping USD 140 million validate investor appetite for prepaid-anchored neo-banks that bundle savings vaults, stock micro-purchases, and credit-building tools beneath a single mobile interface. The competitive response sees incumbent banks white-labeling prepaid payroll offerings to retain contractor relationships, while enterprise software vendors embed prepaid rails for expense control. An iterative feedback loop between gig apps and fintech processors continually spawns micro-features, instant tip payout, mileage reimbursement, and rewards that keep prepaid solutions sticky.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High interchange & program fees | -0.8% | National, acute for small issuers | Medium term (2-4 years) |

| Card-not-present fraud & AML costs | -0.6% | National, higher in e-commerce hubs | Short term (≤ 2 years) |

| Patchy NFC/mobile SMB acceptance | -0.4% | Rural & small-city merchants | Medium term (2-4 years) |

| Fee-cap & expiry-rule compliance | -0.3% | National regulatory scope | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Interchange & Program-Management Fees Eroding Margins

Prepaid programs operate on thinner spreads than credit. When interchange tiers compress or network assessment fees rise, smaller issuers lacking multi-product cross-subsidies quickly face negative unit economics. The 2025 expansion of the Code of Conduct now subjects facilitators and aggregators to disclosure mandates, triggering thousands of dollars in incremental audit expense per program. Consolidation accelerates as at-risk portfolios seek umbrella sponsorship under Peoples Trust or equivalent large BIN sponsors who amortize compliance at scale. Fee compression simultaneously nudges issuers to migrate to virtual-only constructs, eliminating plastic manufacturing costs and shipping, yet adoption decelerates in cash-dominant segments requiring physical reload.

Rising Card-Not-Present Fraud & AML Compliance Costs

As contactless acceptance widens, criminals shift to card-not-present vectors, exploiting e-commerce channels where credential entry remains frictionless. Prepaid issuers, already absorbing interchange cuts, must license advanced behavioral analytics to stay ahead. FINTRAC now expects real-time suspicious-activity monitoring capable of flagging structured reload patterns exceeding USD 10,000 monthly thresholds [2]: Financial Transactions and Reports Analysis Centre of Canada (FINTRAC), “Guidance on Prepaid Payment Products,” fintrac-canafe.gc.ca. . Penalties for inadequate controls rose to USD 1.48 million (CAD 2 million) per infraction in 2025, deterring new entrants and discouraging niche issuers from pursuing high-velocity online gaming cards. Larger players leverage tokenization and 3-D Secure 2.0 to dampen fraud, but capital investments weigh on P&L until volume thresholds are reached.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Gift Cards Sustain Volume Leadership While Benefit Cards Accelerate

Gift cards generated the largest transaction volume in 2025, capturing 65.02% of spending as corporate incentives, seasonal gifting peaks, and merchant-branded promotions kept issuance steady. Load value remained resilient even as broader retail inflation curtailed discretionary budgets, confirming their entrenched role in consumer culture. Government benefit cards, however, chart the most dynamic trajectory with a 12.43% CAGR through 2031. Each incremental province that shifts energy subsidies or tax refunds to prepaid channels funnels millions of reload dollars annually into the Canada prepaid card market. The Working Canadians Rebate, paying USD 185 lump sums directly onto prepaid Visa accounts, exemplifies policy-driven volume surges. Corporate incentive programs also diversify, with multinational employers swapping check-based holiday bonuses for instant digital gift codes to accommodate hybrid workers. Closed-loop merchant suites continue to issue bulk codes for loyalty redemption, though the momentum gradually tilts toward open-loop alternatives as consumers seek flexibility post-holiday.

Entering 2026, card manufacturers report backlog orders for dual-network gift products that can toggle between closed and open environments, signaling convergence. Nevertheless, merchant-controlled breakage economics keep pure closed-loop gift models profitable, encouraging retailers to extend omnichannel redemption experiences. Meanwhile, Indigenous-focused offerings such as OneFeather PAY tap cultural events to distribute honoraria via prepaid, illustrating niche pathways. Overall, the segment blend ensures both volume stability and high-growth adjacencies, making offering diversity a cornerstone strategy for issuers targeting the Canada prepaid card market.

By Card Type: Open-Loop Momentum Challenges Closed-Loop Dominance

Closed-loop instruments accounted for 76.10% of 2025 value loads, buoyed by entrenched retailer ecosystems and superior promotional economics. Their proprietary nature allows merchants to fund bonuses like “bonus 10% reload,” preserving breakage upside. Yet from 2025 onward, open-loop cards look set to erode that share, growing at 11.05% CAGR. Mobile-wallet readiness is a decisive catalyst: once a card tokenizes in Apple Pay, consumers perceive parity with debit, compelling broader usage. Cross-border capabilities further differentiate open-loop credentials for snowbird travelers and cross-border e-commerce aficionados. Merchants too capitalize; hospitality brands issue open-loop reimbursement cards for guest inconvenience payouts, simplifying multi-currency scenarios.

Network rails collaborate with processors to shorten time-to-market by offering turnkey BIN sponsorship and compliance toolkits, lowering barriers for vertical-specific schemes. Real-Time Rail integration in 2026 promises near-instant funding, especially valuable for gig payroll cards that demand second-by-second balance availability. Conversely, closed-loop programs innovate with in-app top-ups and real-time e-gift code issuance to stay relevant, particularly in loyalty ecosystems. Issuers hedging bets operate dual inventory, ensuring presence wherever consumer preference swings. The interplay sets up a competitive equilibrium where both card types co-exist, yet open-loop trajectories undeniably pull market gravity in their favor.

By End User: Corporate Wallets Emerge as High-Velocity Growth Engine

Retail still generates the largest share, at 51.10% of total 2025 load volumes, reflecting mainstream consumer engagement with store gift cards, transit passes, and reloadable spending purses. However, corporate adoption, advancing at 10.05% CAGR, injects fresh dynamism into the Canada prepaid card market. Employers now roll out virtual expense cards with parameterized spending rules that terminate automatically post-project, slashing reconciliation cycles. Gig-economy stalwarts dispense daily earnings via prepaid rails, simultaneously capturing interchange and reinforcing platform loyalty. Procurement departments issue single-use virtual cards for vendor payments, tightening control over maverick spending.

Government end-users scale gradually but steadily through digital benefit dispersion; each newly digitized program becomes a stable load funnel with predictable seasonality. Cross-government collaboration with fintech vendors fosters modular platforms easily cloned across agencies, reducing marginal deployment cost and accelerating adoption. Corporate HR teams experiment with prepaid as a non-taxable reward mechanism, driving wallet share beyond traditional cash bonuses. Conversion-rate analytics reveal employees spend rewards faster when funds hit a prepaid balance versus bank direct deposit, generating earlier economic impact and reinforcing adoption. Collectively, the enterprise segment’s appetite for configurability and real-time funding positions it as the next multibillion-dollar pillar within the market.

Geography Analysis

Ontario’s massive population and deep financial-services roots anchor its 44.52% share of Canada prepaid card market load activity in 2025. Toronto’s fintech corridor attracts venture investment and global partnerships, evidenced by KOHO Financial scaling national distribution through 6,000-plus Canada Post outlets. Concentrated headquarters of multinationals spur corporate payroll and incentive card issuance, while newcomer inflows sustain consumer GPR adoption. Provincial regulators maintain bilingual disclosure guidelines yet support innovation, creating an accommodating sandbox for product pilots. Growing suburban transit prepaid programs add steady micropayment volume, tying transportation agencies into nationwide EFT corridors .

Atlantic Canada, posting a 9.18% CAGR through 2031, leverages government-funded financial-inclusion strategies aimed at coastal and rural constituencies. Postal and credit-union collaborations establish reload kiosks in towns previously reliant on cash remittances. Provincial energy-rebate cards distribute seasonally high-value loads that recipients frequently retain for everyday purchases post-benefit, heightening velocity. Indigenous communities adopt culturally branded cards for local stipend disbursement, fostering trust and economic circulation within reserves. The region’s tourism revival also triggers merchant open-loop acceptance upgrades, feeding back into higher card utilization.

Quebec navigates a unique regulatory environment after Bill 72 tightened prepaid disclosure, yet the province remains an innovation hub for closed-loop retail cards aligned with distinct linguistic branding. Small federal agencies test dual-language prepaid portals here before launching nationwide, grounding market experimentation. Prairie provinces and British Columbia deliver balanced growth, underpinned by resource-sector contractor payroll cards and Pacific trade fuelling cross-border open-loop demand. Northern territories rely heavily on Canada Post distribution and satellite-connected point-of-sale terminals, making prepaid cards critical for communities with limited broadband. Collectively, geography diversification indicates no single region monopolizes upside, guaranteeing consistent national throughput for the Canada prepaid card market.

Competitive Landscape

The Canada Prepaid Card Market remains moderately concentrated, with the top five entities commanding a substantial share of the 2024 load value. Visa leads the market, bolstered by its dominant position in open-loop GPR issuance and robust tokenization support that reduces fraud for issuers. Mastercard follows closely, leveraging Mastercard Send to power gig-economy instant payouts. People's Trust anchors the BIN sponsorship ecosystem, supplying compliance infrastructure to numerous fintech brands. KOHO Financial reflects consumer appetite for fee-light neo-banks that wrap savings and budgeting atop prepaid cores. Network duopoly dynamics create high switching costs for program managers, but partnership models soften barriers, allowing new vertical specialists to piggyback on established rails.

Strategic alliances multiply: H&R Block issues instant tax refund cards on Peoples Trust rails, while Payfare embeds Pay-to-Card APIs that deliver gig wages in under 30 seconds. Processor Marqeta’s expansion into Canada furnishes white-label issuing capability for on-demand delivery firms, adding competitive heat for legacy processors. Consolidation trends continue; smaller closed-loop gift platforms are selling into large payment aggregators to access compliance tools, while large banks quietly acquire payroll card fintechs to broaden SME product suites.

Innovation focus shifts toward value-added overlays such as real-time location-based spend controls and card-linked offers. Visa and Mastercard publish developer toolkits that allow third-party apps to orchestrate dynamic spending rules without jeopardizing PCI scope. Peoples Trust pilots artificial-intelligence fraud engines integrating FICO anomaly scoring, reporting early reductions in false positives [4]FICO, “Canada Bankcard Industry Benchmarking Trends Q2 2025,” fico.com. . Market participants expect Real-Time Rail connectivity in 2026 to intensify rivalry by allowing direct-to-card funding from bank accounts, compressing settlement windows and elevating customer expectations. Overall, the strategic chessboard remains fluid, but incumbents’ scale advantages dictate a competitive equilibrium.

Canada Prepaid Card Industry Leaders

Visa Inc.

Mastercard Inc.

Peoples Trust Company

KOHO Financial

Blackhawk Network

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: KOHO Financial launched the MyMoney Account in partnership with Canada Post, expanding access to underbanked populations through postal distribution networks.

- February 2025: H&R Block Canada partnered with Peoples Trust to launch enhanced tax refund prepaid cards, enabling faster access to refunds during tax season. The partnership combines H&R Block's customer base with Peoples Trust's prepaid infrastructure to offer immediate fund availability upon tax filing completion.

- January 2025: Criminal interest rate reforms took effect, lowering the threshold from 60% to 35% APR and creating new compliance obligations for prepaid card issuers offering credit-like features.

- November 2024: Quebec adopted Bill 72, implementing stricter consumer lending rules affecting prepaid products with credit features. The legislation requires enhanced disclosure of credit limits, restricts unsolicited credit documentation, and strengthens consumer protections for fraudulent fund transfers.

Canada Prepaid Card Market Report Scope

A prepaid card is a kind of payment card one can use to purchase or pay bills, such as credit cards or debit cards. Banks, financial institutions, and others issue these cards with loaded funds. Users can make a transaction without having to pay interest in the future.

Canada’s prepaid cards market is segmented by offering (general purpose cards, gift cards, government benefit cards, incentive/payroll cards, and other offerings), card type (closed-loop cards and open-loop cards), and end user (retail, corporate, and government). The report also covers the market sizes and forecasts for Canada’s prepaid card market in value (USD) for all the above segments.

By Offering

| General Purpose Cards |

| Gift Cards |

| Government Benefit Cards |

| Incentive/Payroll Cards |

| Other Offerings |

By Card Type

| Closed-Loop Cards |

| Open-Loop Cards |

By End User

| Retail |

| Corporate |

| Government |

By Geography

| Atlantic Canada |

| Quebec |

| Ontario |

| Prairie Provinces |

| British Columbia |

| Northern Territories |

| By Offering | General Purpose Cards |

| Gift Cards | |

| Government Benefit Cards | |

| Incentive/Payroll Cards | |

| Other Offerings | |

| By Card Type | Closed-Loop Cards |

| Open-Loop Cards | |

| By End User | Retail |

| Corporate | |

| Government | |

| By Geography | Atlantic Canada |

| Quebec | |

| Ontario | |

| Prairie Provinces | |

| British Columbia | |

| Northern Territories |

Key Questions Answered in the Report

How large is the Canada prepaid card market in 2026?

The Canada prepaid card market size reached USD 7.56 billion in 2026 and is projected to reach USD 11.7 billion by 2031, advancing at a 9.12% CAGR over 2026-2031.

Which card type is growing fastest?

Open-loop prepaid cards post the fastest momentum, supported by 11.05% CAGR projections due to tokenization and mobile-wallet compatibility.

What drives corporate adoption of prepaid solutions?

Corporations use prepaid cards for gig-worker payroll, expense management, and employee incentives, seeking real-time control and reduced reconciliation.

Which region shows the highest growth rate?

Atlantic Canada leads with a 9.18% CAGR forecast, bolstered by benefit digitization and expanded postal distribution in rural areas.

What regulatory change most affects issuers?

The 2025 expansion of the Code of Conduct extends transparency and compliance obligations to payment facilitators and aggregators processing prepaid transactions.

Page last updated on: