Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

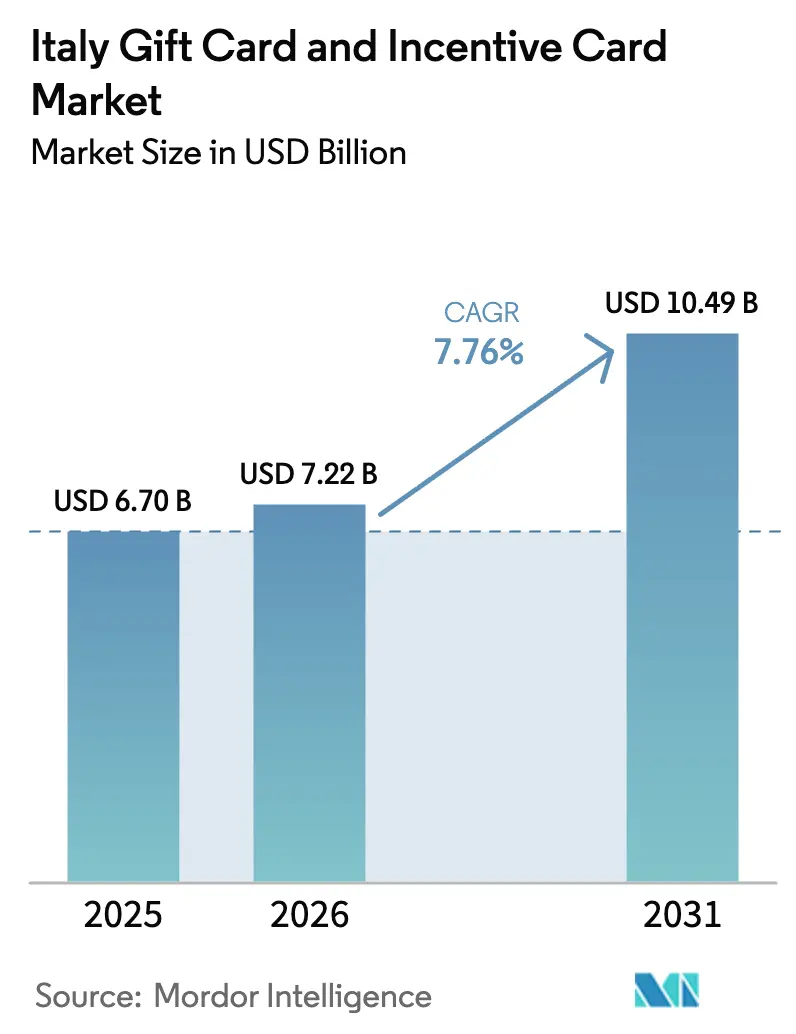

| Base Year Market Size (2025) | USD 6.70 Billion |

| Market Size (2026) | USD 7.22 Billion |

| Market Size (2031) | USD 10.49 Billion |

| Growth Rate (2026 - 2031) | 7.76% CAGR |

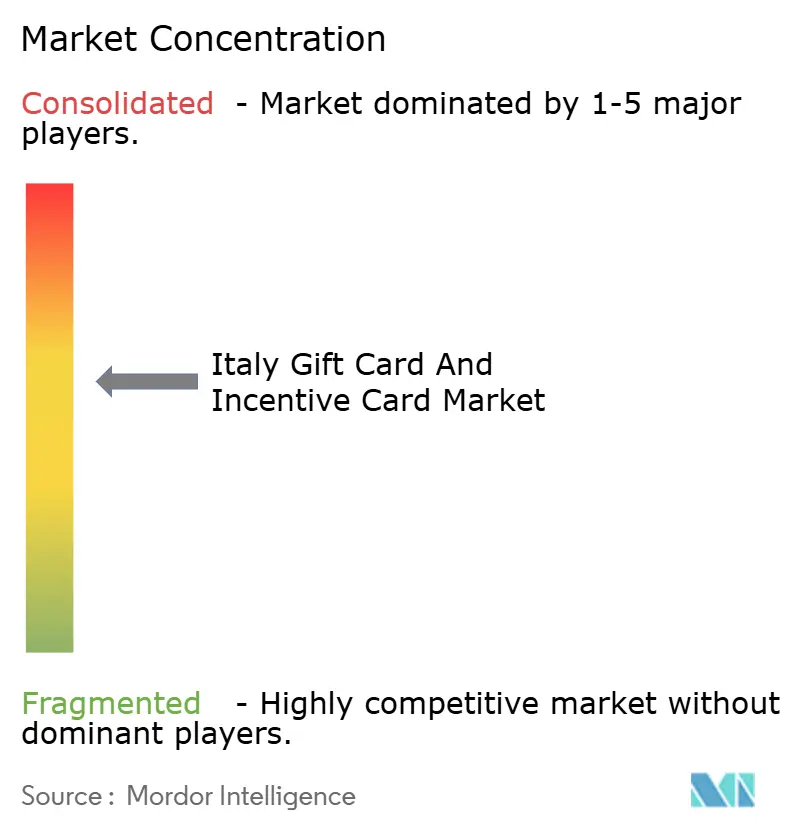

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Gift Card And Incentive Card Market Analysis by Mordor Intelligence

The Italy gift card and incentive card market size in 2026 is estimated at USD 7.22 billion, growing from 2025 value of USD 6.70 billion with 2031 projections showing USD 10.49 billion, growing at 7.76% CAGR over 2026-2031. Widespread contactless adoption—58% of point-of-sale card transactions—signals a decisive consumer shift toward digital payments. Regulatory support, including a 30% tax credit on electronic payment fees for smaller firms, lowers acceptance costs and encourages merchants to issue gift cards. Open-loop products grow fastest as Nexi’s EUR 220 million European Investment Bank loan accelerates multi-merchant acceptance. Meanwhile, Edenred’s EUR 464 million Italy revenue underscores robust B2B demand for employee incentives. Physical cards still dominate amid historically low banking trust, yet digital formats are expanding at double-digit rates as Satispay, PostePay, and other fintech platforms embed virtual cards in everyday apps.

Key Report Takeaways

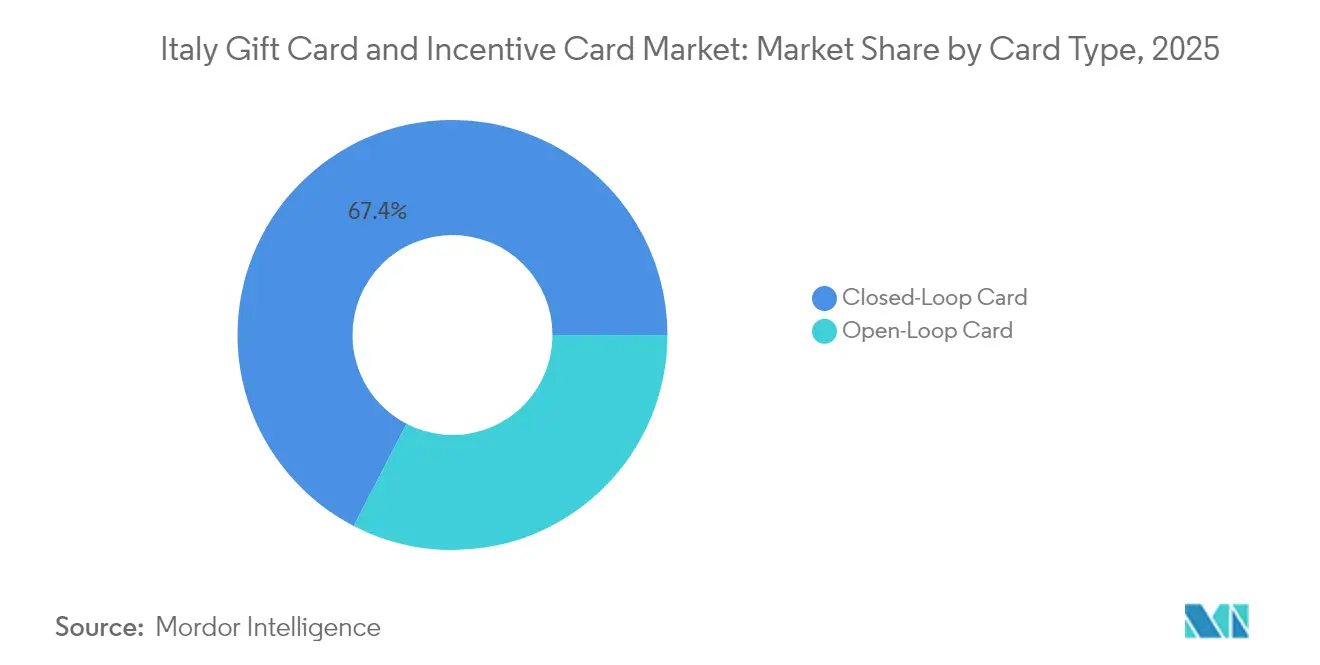

- By card type, closed-loop captured 67.40% of the Italy gift card and incentive card market share in 2025, while open-loop is projected to expand at a 8.94% CAGR through 2031.

- By format, physical cards held 59.40% of the Italy gift card and incentive card market size in 2025; digital cards are pacing a 12.43% CAGR to 2031.

- By consumer type, individuals retained 68.90% of the 2025 share of the Italy gift card and incentive card market, whereas corporate programs are forecasted to rise at a 9.45% CAGR.

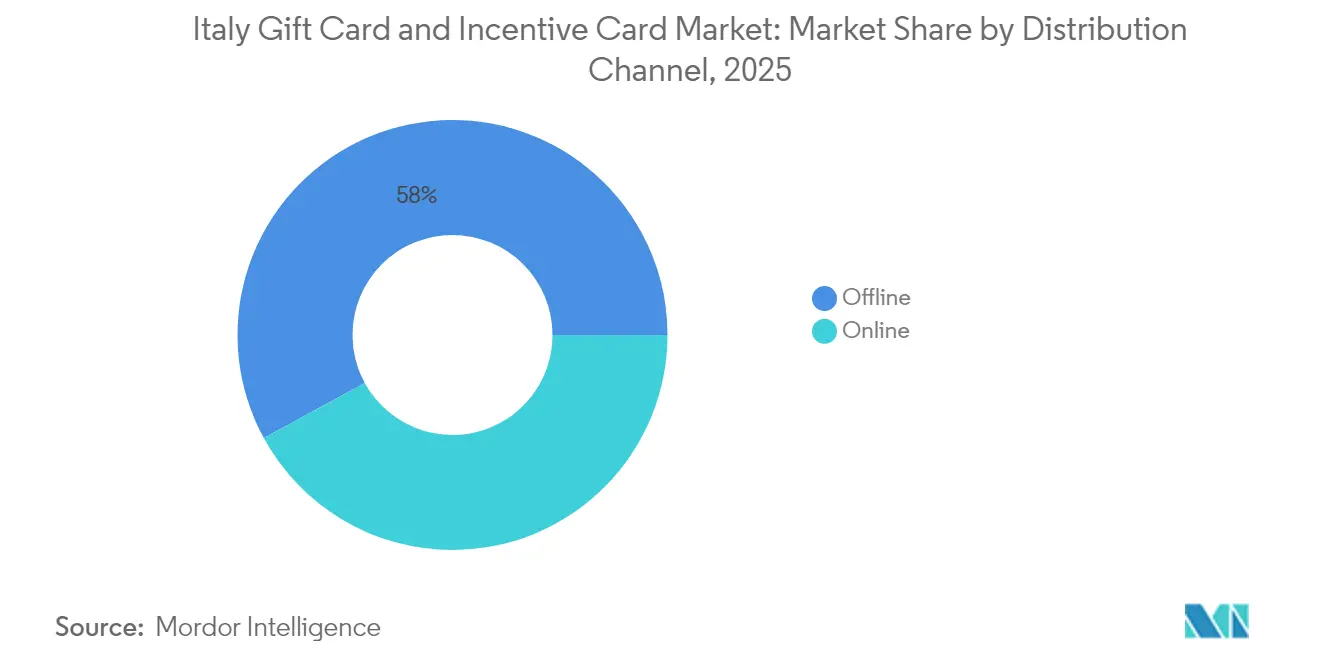

- By distribution channel, offline outlets accounted for 57.95% of the Italy gift card and incentive card market share in 2025; online channels are projected to grow at 11.55% CAGR.

- By industry of application, “Other Industries” led with 33.10% share of the Italy gift card and incentive card market, yet Health, Wellness & Beauty is advancing fastest at 9.92% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Gift Card And Incentive Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce & mobile payments adoption | +2.1% | National; strongest in northern cities | Medium term (2–4 years) |

| Corporate demand for employee incentives & loyalty tools | +1.8% | Milan, Rome, Turin hubs | Long term (≥ 4 years) |

| Regulatory push for cashless transactions & tax incentives | +1.4% | SME-heavy southern regions | Short term (≤ 2 years) |

| Growing popularity of digital/contactless gift cards | +1.2% | Youth segment nationwide | Medium term (2–4 years) |

| ESG-linked gift cards for sustainability-minded consumers | +0.8% | Northern metros | Long term (≥ 4 years) |

| Integration with BNPL & super-apps enabling micro-gifting | +0.5% | E-commerce platforms | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surge in e-commerce & mobile payments adoption

Mobile commerce already represents a significant share of total online sales, yet only a relatively small portion of in-store payments are mobile, exposing an untapped bridge for omnichannel gift cards. Digital wallets carry around 35% of online transaction value today and should reach 46% by 2027, making wallet-ready gift cards a natural fit. EU rules mandating instant payments by 2025 promise real-time corporate bulk issuance, while PostePay’s 7.2 million Evolution cards illustrate platform-led cross-selling. Cross-border shopping by around 50% of Italian consumers expands demand for multi-currency cards. Overall, omnichannel commerce acts as a flywheel for the Italy gift card and incentive card market.

Corporate demand for employee incentives & loyalty tools

Edenred’s EUR 464 million Italy revenue and its acquisition of IP Gruppo API’s energy card unit reveal the scale of B2B expansion. Pluxee’s 18.6% organic growth after spinning off from Sodexo highlights SME appetite for digital incentives. Epipoli’s partnerships with grocer Esselunga demonstrate the convergence of gift cards with loyalty data platforms. Italian tax treatment favors electronic benefits, and rising retention costs push firms to offer flexible rewards. As a result, corporate uptake lifts long-term growth for the Italy gift card and incentive card market.

Regulatory push for cashless transactions & tax incentives

A 30% tax credit on electronic fees effectively subsidizes small merchants that accept gift cards, easing entry barriers. Mandatory e-invoicing dovetails with digital card issuance for simpler back-office reconciliation. Contactless penetration reached 58% of card transactions following PSD2 and GDPR security frameworks, bolstering consumer trust. Antitrust oversight of the Nexi-SIA merger maintains pricing competition in processing services[1]OECD, “Competition Enforcement in Payment Services: Italy Case Study,” oecd.org. Lower interchange caps than the EU average reduce issuer costs, widening product margins and accelerating adoption.

Growing popularity of digital/contactless gift cards

Visa’s push-to-wallet tokenization lets virtual cards drop straight into Apple Pay or Google Pay, eliminating activation friction[2]Visa Inc., “Virtual Cards: Push-to-Wallet Expansion,” visa.com. Satispay’s launch of in-app gift cards leverages its eight-million-user base during a 22% pandemic-era rise in digital payments. The European Payments Council urges stronger customer authentication, encouraging issuers to adopt biometric login and real-time monitoring. Local payment rails BANCOMAT Pay and PagoBANCOMAT now integrate with Amazon Italia, proving global merchants can adopt Italian-specific digital cards. Collectively, these trends draw younger demographics deeper into the Italy gift card and incentive card market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising fraud & cybersecurity concerns | −1.1% | Digital-first segments nationwide | Short term (≤ 2 years) |

| Stringent AML/KYC compliance costs | −0.9% | B2B, high-value issuers | Medium term (2–4 years) |

| Breakage liabilities as the closed-loop stock saturates | −0.7% | Mature retail programs | Long term (≥ 4 years) |

| Ageing populations are slower to adopt digital gifting | −0.6% | Rural south & islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising fraud & cybersecurity concerns

The European Payments Council cites escalating social-engineering attacks that force issuers to invest in AI-driven monitoring, inflating operating costs[3]European Payments Council, “Payment Threats & Fraud Trends Report 2024,” europeanpaymentscouncil.eu. Authorized push-payment scams exploit the irreversibility of gift cards, eroding consumer confidence. Upcoming EU Payment Services Regulation debates liability allocation, creating strategic uncertainty. Smaller fintechs must buy outsourced security tools, squeezing margins, while larger processors like Nexi pour hundreds of millions into cyber defense. Persistent media coverage of data breaches slows the onboarding of new users in the Italy gift card and incentive card industry.

Stringent AML/KYC compliance costs for issuers

Overlapping GDPR and Digital Services Act rules mandate heavier data-protection procedures. Edenred expects a EUR 60 million EBITDA hit from Italy’s merchant-fee cap and related compliance upgrades. Antitrust scrutiny of mergers such as Nexi-SIA lengthens deal timelines and requires detailed reporting. Smaller issuers struggle with fixed-cost burdens, curbing product launches. Cross-border offerings must reconcile varied EU AML regimes, slowing the international scalability of the Italy gift card and incentive card market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Card Type: Open-loop innovation challenges closed-loop tradition

Closed-loop cards commanded 67.40% of the Italy gift card and incentive card market share in 2025 as retailers used them to lock customers into proprietary ecosystems. Their dominance secures data capture, boosts private-label margins, and funds tailored promotions. Carrefour’s aim to raise private-label penetration to 40% of food sales by 2026 shows how gift cards steer traffic to in-house brands. Epipoli and Esselunga’s loyalty partnership layers personalized offers on closed-loop wallets, broadening engagement.

Open-loop alternatives are projected to scale at a 8.94% CAGR through 2031, aided by BANCOMAT Pay’s integration on Amazon Italia and Visa’s token-push APIs. Nexi’s EUR 220 million EIB loan underwrites multi-merchant acceptance upgrades, lowering per-transaction friction. Lower interchange caps let issuers price competitively, while 50% cross-border shopper penetration makes universal cards attractive. As open-loop utility broadens, they are on track to trim the closed-loop share in the Italy gift card and incentive card market size over time.

By Format Type: Digital innovation transforms traditional gifting

Physical cards retained 59.40% of the Italy gift card and incentive card market share in 2025, bolstered by cultural affinity for tangible presents and Italy’s dense brick-and-mortar network. Eurocommercial Properties’ 24 Italian shopping centers exemplify locations where impulse gift-card racks thrive.

Yet digital versions are leaping ahead at 12.43% CAGR, powered by Satispay in-app issuance, Visa push-to-wallet flows, and ESG sentiment that favors plastic-free gifting. Epipoli’s MyGiftCardPlusGreen replaces PVC with virtual codes while aligning spend with eco-merchants. Retailers trim production and logistics costs, freeing capital for targeted promotions. Data-rich digital cards feed loyalty analytics, making them key to the future growth of the Italy gift card and incentive card market.

By Consumer Type: Corporate segment drives strategic growth

Individuals still represent 68.90% of transaction value, reflecting entrenched holiday and family gifting norms. However, corporate demand is climbing at a 9.45% CAGR as firms adopt cards for tax-advantaged benefits and reward schemes. Edenred’s takeover of IP Gruppo API’s energy card base brings 50,000 B2B clients, highlighting momentum.

Tax credits on electronic fees lower employers’ costs, and wellness-linked cards satisfy growing ESG and wellbeing mandates. Pluxee’s SME push illustrates white-space potential, especially for Italy’s 4 million small businesses. As corporate uptake accelerates, the Italy gift card and incentive card industry stands to rebalance toward B2B revenue streams.

By Distribution Channel: Omnichannel strategies bridge the physical-digital divide

Offline outlets accounted for 57.95% of the Italy gift card and incentive card market share in 2025, thanks to widespread supermarket chains, newsstands, and malls that support instant gratification. Omnichannel leaders such as Carrefour embed QR-code vouchers redeemable both in-store and online, ensuring channel fluidity.

Online sales are expanding at 11.55% CAGR on the back of 50% cross-border e-commerce participation and rising mobile wallet penetration. Viva.com’s support for BANCOMAT Pay across merchant sites enables unified settlement flows. Reduced inventory needs, instant fulfillment, and data-driven upsells make digital malls cost-effective for issuers, positioning online as the growth engine for the Italy gift card and incentive card market.

By Industry of Application: Health & Wellness leads sector transformation

The other industry segment controlled 33.10% of the Italy gift card and incentive card market share in 2025, given the broad mix of automotive, home improvement, and services. Yet Health, Wellness & Beauty is racing ahead at 9.92% CAGR as consumers prioritize self-care post-pandemic. Klépierre’s clothing-for-card recycling taps into wellness and sustainability by incentivizing wardrobe decluttering.

Food & Beverage cards leverage Italy’s culinary culture, while electronics benefit from digital-device demand fueled by National Recovery Plan grants. ESG alignment remains a universal theme: Epipoli’s green vouchers and IKEA’s circularity workshops ensure that environmental consciousness permeates every vertical, solidifying diversified momentum within the Italy gift card and incentive card market size.

Geography Analysis

Northern regions dominate transaction value thanks to higher incomes, dense retail infrastructure, and advanced broadband. Lombardy, Veneto, and Emilia-Romagna host fintech clusters where Nexi’s innovation programs and EIB-backed projects flourish. Corporate headquarters in Milan, Rome, and Turin generate outsized B2B demand, evidenced by Edenred’s robust regional sales.

Southern Italy lags in digital adoption yet stands to benefit most from the 30% tax credit that offsets acceptance fees for small merchants. Here, physical cards bridge cash-centric cultures, while education campaigns aim to migrate users online. Tourist hotspots in Tuscany, Liguria, and Veneto provide seasonal spikes as travelers redeem airport and duty-free gift cards tied to Avolta’s retail footprint.

Cross-border dynamics matter: half of Italian shoppers buy from foreign sites, requiring multi-currency, open-loop solutions. EU instant-payment mandates will harmonize settlement nationwide, eroding regional gaps. As infrastructure equalizes, the Italy gift card and incentive card market should exhibit more balanced geographic dispersion while still anchored by the economic weight of the north.

Competitive Landscape

Market concentration is moderate and tightening. Investcorp’s 2025 purchase of Epipoli marks renewed consolidation as private equity aggregates niche processors. Nexi and SIA’s earlier merger, under antitrust conditions, created a national champion that invests EUR 395 million annually in technology upgrades. Visa, Mastercard, and American Express continue to supply rails, but local fintechs such as Satispay and Viva.com win share through low-cost acquisition models.

Strategic differentiation pivots on ecosystems rather than card issuance alone. Edenred is bundling analytics and wellness content to offset the EUR 60 million EBITDA drag from interchange caps. Pluxee positions itself as an SME partner, layering fuel, meals, and wellness benefits into a single platform. Avolta leverages airport concessions to cross-sell travel gift cards with duty-free coupons, while Poste Italiane capitalizes on its 35 million-customer reach to launch bundled telecom-banking-gifting services.

Technology drives arms-race dynamics. Visa’s API suite allows instant wallet tokenization, while Nexi’s cloud migration reduces fraud-detection latency. ESG remains a branding battlefield: Epipoli’s green gift cards and Klépierre’s circular retail initiatives resonate with younger consumers. Competitive intensity will increase as interchange revenue compresses and players pivot to value-added services to protect margins inside the Italy gift card and incentive card market.

Italy Gift Card And Incentive Card Industry Leaders

Epipoli Group

Nexi Payments

PostePay

Edenred

Amazon.com

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Investcorp completed the acquisition of Epipoli, accelerating payments sector consolidation.

- January 2025: Recharge secured a £38 million facility from ABN AMRO to finance European gift card acquisitions.

- December 2024: Satispay launched in-app gift cards, expanding beyond peer-to-peer payments.

- October 2024: Visa broadened push-to-wallet virtual-card functionality for Apple Pay and Google Pay adoption.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Italian gift card and incentive card market as the total face value of prepaid instruments, physical or digital, open-loop or closed-loop, that consumers or corporates load and redeem within Italy for goods, services, or employee rewards during the calendar year.

Scope Exclusion: Cards that can be reloaded for general-purpose spending or cross-border travel wallets fall outside this definition.

Segmentation Overview

- By Card Type

- Open-Loop Card

- Closed-Loop Card

- By Format Type

- Digital Card

- Physical Card

- By Consumer Type

- Individual (B2C)

- Corporate (B2B)

- By Distribution Channel

- Online

- Offline

- By Industry of Application

- Food and Beverages

- Health, Wellness, and Beauty

- Apparel, Footwear, and Accessories

- Consumer Electronics

- Other Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed issuers, large retailers, HR outsourcing firms, and fintech enablers across Lombardy, Lazio, Emilia-Romagna, and Campania. Discussions clarified discounting rules, average selling prices, and expected corporate demand after the 2024 fringe-benefit cap revision, allowing us to reconcile secondary patterns and pressure-test growth triggers.

Desk Research

We began with publicly available datasets from Banca d'Italia payment statistics, Eurostat retail trade indices, and the Italian Tax Agency's e-invoice portal, which together outline transaction velocity, sectoral sales, and VAT-linked redemption patterns. Trade bodies such as Federdistribuzione and Assolavoro provide merchant density and corporate incentive penetration figures, while patent filings on prepaid tokenization, sourced via Questel, signal technology adoption curves. Annual reports and 10-Ks of major retailers, plus press releases captured through Dow Jones Factiva, give illustrative load values and breakage ratios. The sources listed are illustrative, not exhaustive; many additional materials informed our evidence base.

Market-Sizing & Forecasting

A top-down spend potential model translates household consumption, corporate benefit budgets, and tourism inflows into a gift-card addressable pool, which is then sense-checked through sampled ASP × volume build-ups from major issuers. Variables such as contactless card share, e-commerce penetration, inflation-adjusted discretionary spend, VAT-free fringe-benefit ceilings, seasonality around Christmas, and digital channel mix feed the model. A multivariate regression with ARIMA overlay projects these drivers to 2030, while gaps in bottom-up issuer data are bridged using retail footfall proxies and online search intensity.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance checks against independent payment indicators, and peer debriefs before sign-off. The study refreshes annually; interim updates trigger when material events, such as policy changes or issuer mergers, shift market baselines.

Why Our Italy Gift Card and Incentive Card Baseline Commands Reliability

Published estimates frequently diverge because firms select different card types, conversion rates, and refresh cadences.

Key gap drivers include: some publishers mix general-purpose reloadables with gift cards, others apply aggressive unit growth assumptions without adjusting ASP decline, and a few freeze 2023 exchange rates. Mordor's disciplined scope, driver-level forecasting, and yearly refresh reduce these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.70 B (2025) | Mordor Intelligence | - |

| USD 8.47 B (2025) | Regional Consultancy A | Includes government welfare vouchers; limited issuer interviews |

| USD 11.50 B (2024) | Trade Journal B | Uses face value of unused cards and reloadables; 2021 FX locked |

| USD 6.20 B (2024) | Global Consultancy C | Applies static ASP, under-represents corporate incentives |

In sum, the tighter scope, transparent variables, and annual update cadence give decision-makers a balanced, reproducible baseline that, in our view, sets a dependable reference point amid wider market noise.

Key Questions Answered in the Report

What is the current size of the Italy gift card and incentive card market?

The market stands at USD 7.22 billion in 2026 and is set to reach USD 10.49 billion by 2031 at a 7.76% CAGR.

Which card type is growing fastest?

Open-loop products show the strongest momentum with a projected 8.94% CAGR through 2031 as consumers seek multi-merchant flexibility.

Why are corporate gift cards gaining traction?

Italian firms leverage a 30% electronic-fee tax credit and appreciate gift cards as tax-efficient, flexible employee rewards, spurring a 9.45% CAGR in the corporate segment.

How important are digital gift cards in Italy?

Digital formats grow at 12.43% CAGR, driven by wallet integration, instant delivery, and sustainability preferences, though physical cards still dominate overall spend.

What are the main risks facing issuers?

Rising fraud, stricter AML/KYC obligations, and breakage liabilities on saturated closed-loop inventories weigh on margins and operational complexity.

Which regions present the biggest expansion opportunities?

Northern Italy leads in spending, but Southern regions offer significant upside as tax incentives and education efforts convert cash-oriented merchants to digital gift card acceptance.

Page last updated on: