Malted Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.27 Billion |

| Market Size (2031) | USD 13.33 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malted Milk Market Analysis by Mordor Intelligence

The Malted Milk Market size was valued at USD 9.75 billion in 2025 and estimated to grow from USD 10.27 billion in 2026 to reach USD 13.33 billion by 2031, at a CAGR of 5.35% during the forecast period (2026-2031). Increased household expenditure on functional nutrition, expanded applications of malt extracts in dairy and bakery products, and consistent capacity expansions by key manufacturers are driving market growth. Regulatory clarity regarding minimum milk-fat content and moisture thresholds in Canada, along with enhanced government support for dairy infrastructure in India, is strengthening the category's resilience. Furthermore, the premiumisation of adult meal-replacement beverages is contributing to this momentum. Although barley-based variants currently represent a smaller segment, they are gaining traction due to their clean-label attributes and the diversification of global barley supply chains. At the same time, escalating cost pressures from fluctuating barley and wheat yields are prompting companies to strengthen supplier partnerships and invest in agronomic initiatives, accelerating the transition toward sustainability-focused supply chains. Furthermore, specialty malted milk is gaining traction in clinical nutrition, especially for patients needing calorie-dense and easily digestible options. E-commerce's expansion, particularly in India and the Gulf Cooperation Council, is breaking down entry barriers for smaller players, broadening product variety, and introducing the category to a fresh consumer base. With these converging factors, malted milk is poised to outpace several other dairy-based beverages, even amidst potential macroeconomic headwinds.

Key Report Takeaways

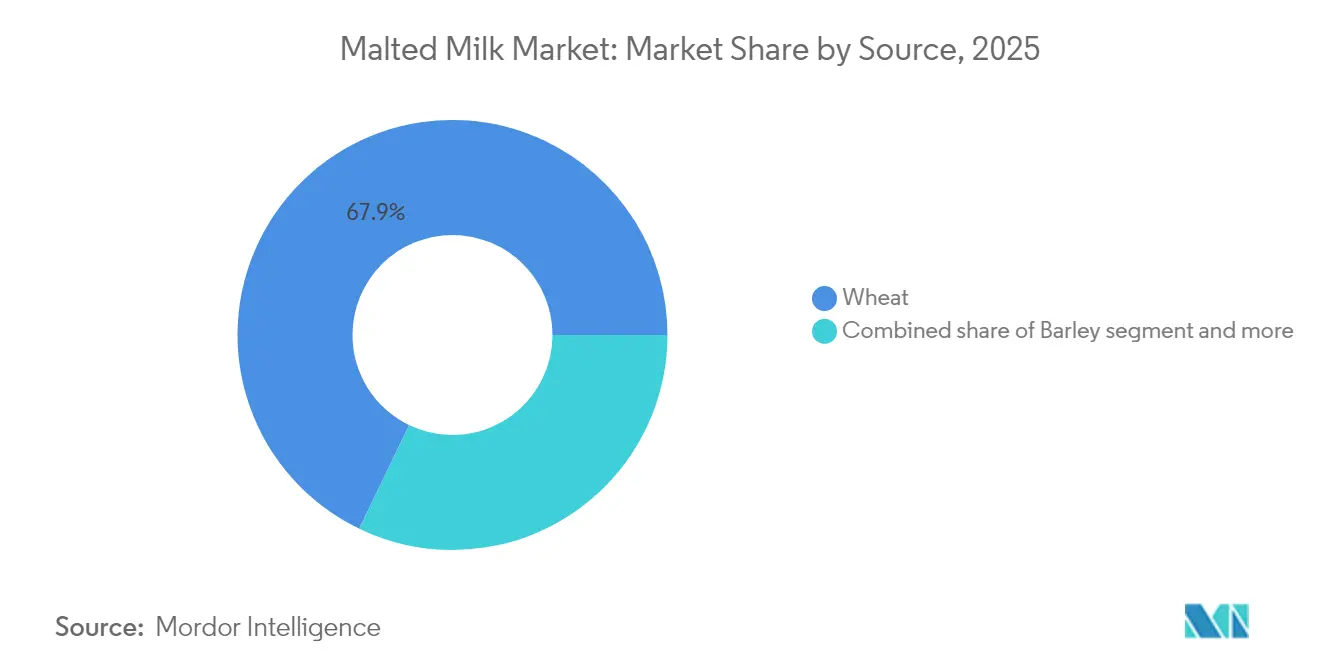

- By grain source, wheat-based products led with 67.86% of malted milk market share in 2025, whereas barley-based counterparts are projected to advance at an 8.29% CAGR through 2031.

- By form, powder accounted for 80.75% share of the malted milk market size in 2025; liquid offerings are forecast to expand at a 7.34% CAGR between 2026 and 2031.

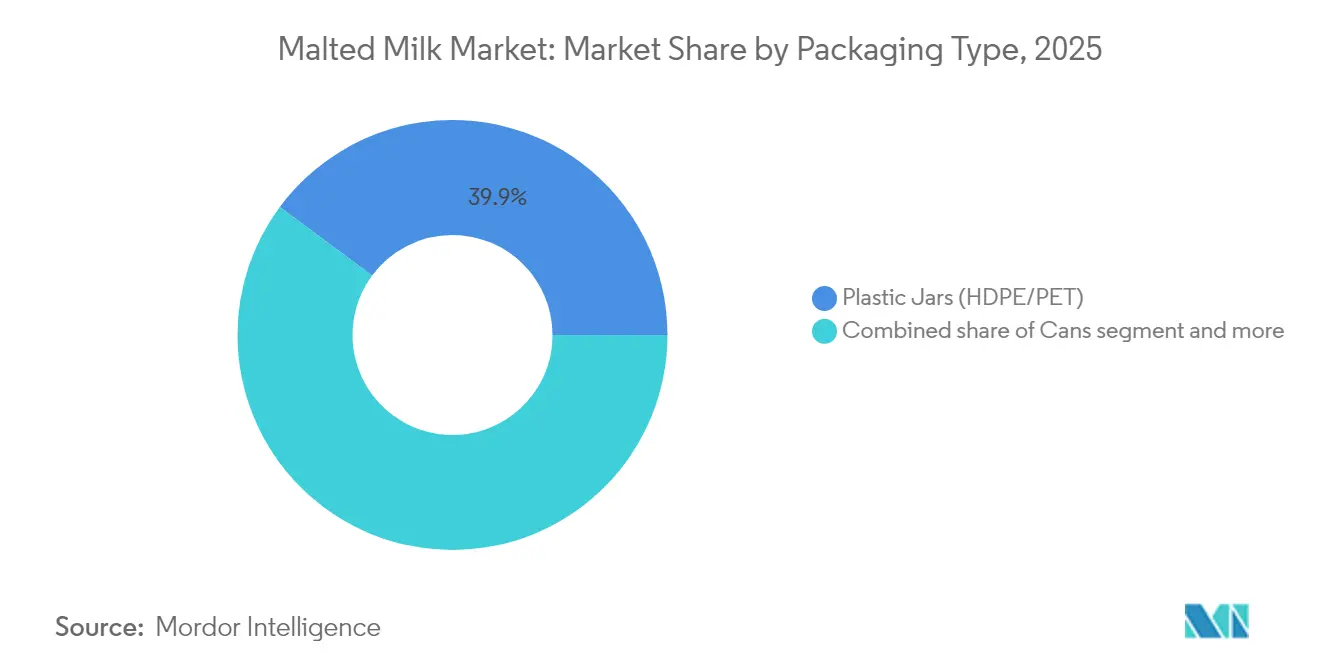

- By packaging type, plastic jars (HDPE/PET) held a 39.85% revenue share in 2025, but pouches are expected to post the highest CAGR of 8.38% from 2026 to 2031.

- By distribution channel, retail remained dominant with a 43.95% share in 2025, while foodservice is projected to rise at a 12.18% CAGR through 2031.

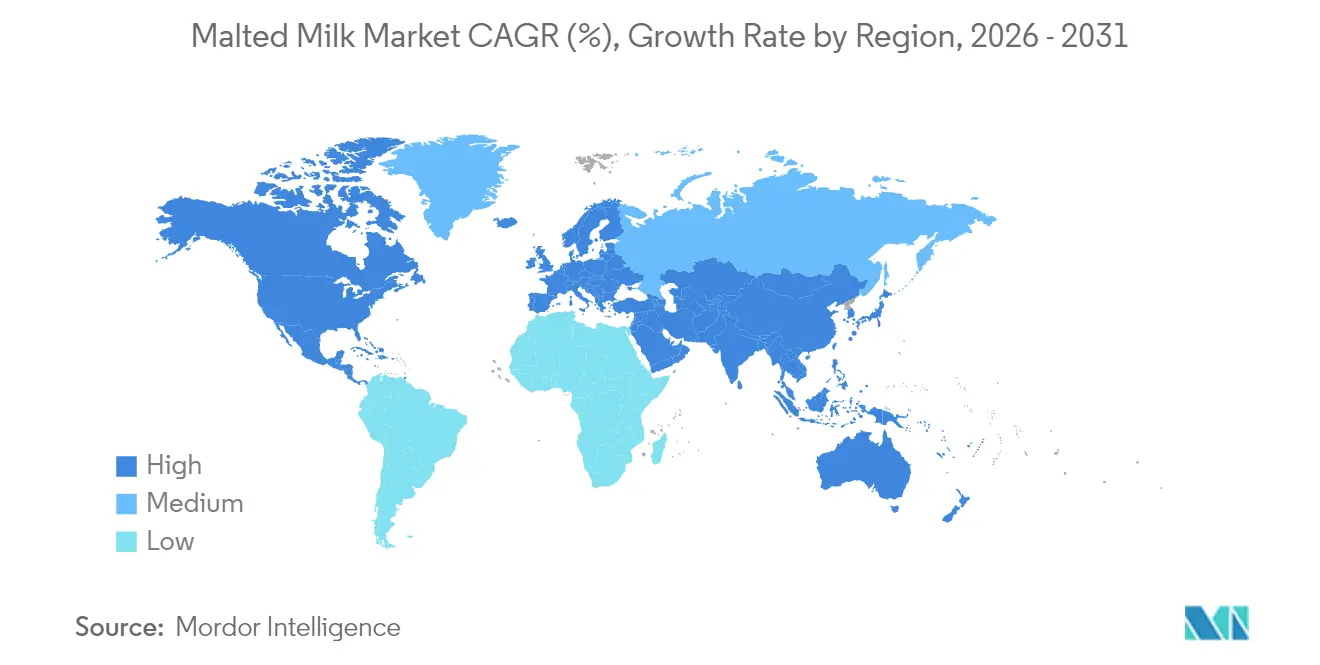

- By region, the Asia-Pacific captured 36.72% of 2025 revenue, whereas the Middle East and Africa region is set to deliver the fastest regional growth at a 8.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Malted Milk Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing penetration of malt-based dairy beverages | +0.9% | Asia-Pacific | Medium term (2-4 years) |

| Surging demand from artisanal and functional bakery producers | +0.6% | North America, Europe | Medium term (2-4 years) |

| Clean-label positioning driving barley-based malted milk adoption | +0.5% | Europe, Oceania | Long term (≥ 4 years) |

| Nutritional appeal among health-conscious consumers boosts growth | +0.7% | Global | Short term (≤ 2 years) |

| Government-led school nutrition programs incorporating malted milk | +0.4% | Asia-Pacific, Middle East | Short term (≤ 2 years) |

| Premiumisation trend in adult nutrition shakes leveraging malt extracts | +0.3% | Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing penetration of malt-based dairy beverages

With increasing health awareness, consumers are shifting towards beverages that provide both protein and essential micronutrients. Malt-based dairy drinks effectively meet this demand while maintaining a familiar taste profile. Brand managers have strategically repositioned several traditional malted products as "complete nutrition" solutions, expanding the market beyond children to include time-pressed adults seeking meal replacement options. The integration of malted ingredients into dairy beverages is gaining momentum as manufacturers respond to consumer demand for nutritionally enhanced products. Milk production in India in 2024 was 239.30 million tonnes, according to the Department of Animal Husbandry and Dairying [1]Source: Department of animal husbandry and dairying, "Animal Husbandry Statistics 2024", dahd.gov.in. Milk production in India in 2024 was Milk production in India in 2024 was Milk production in India in 2024 was Milk production in India in 2024 was driven by increased herd size, government support, and favorable weather conditions. The Indian government's 'White Revolution 2.0' initiative is investing in dairy infrastructure and support programs to enhance production and consumption, creating favorable conditions for malted milk product development. The growing allocation of fridge space for malt-fortified milk in modern trade outlets reflects stronger merchandising efforts and improved supplier-retailer partnerships. While flavor innovation remains limited, volume growth is primarily driven by increased product availability and targeted marketing, rather than significant reformulations, underscoring the sustained consumer preference for core taste profiles. New dairy suppliers entering private-label agreements can capitalize on this stable flavor demand by prioritizing supply-chain efficiency over costly product development initiatives.

Surging demand from artisanal and functional bakery producers

Artisanal bakery operators are increasingly incorporating malted milk powder to enhance caramelization and browning, delivering improved flavor profiles without relying on artificial additives. This strategic shift is driving growth in the malted milk market share within the bakery ingredient segment while introducing malted powders to consumers who may not traditionally consume them in liquid form. The emphasis on sustainable sourcing, now a key feature on bakery menus, aligns with malt suppliers' carbon footprint reduction initiatives, creating opportunities for co-branding partnerships. In November 2023, Soufflet Malt completed the acquisition of United Malt Group, strategically positioning itself to leverage this trend by prioritizing sustainable malt solutions for brewing and food industries. The unique flavor profile and nutritional advantages of malted milk powder enhance the taste and functionality of baked goods, catering to consumers seeking premium-quality products. Investments in advanced bakery equipment, such as high-capacity planetary mixers, facilitate precise hydration of malted milk powders, ensuring consistent crumb quality in premium baked goods. This differentiation allows bakers to justify higher price points, effectively offsetting the incremental costs of premium ingredients. Additionally, bakery outlets are becoming experiential marketing platforms for malt producers, showcasing core beverage brands to new consumer segments through dessert-based cross-promotions.

Clean-label positioning driving barley-based malted milk adoption

Barley-based malted products are experiencing growing demand among label-conscious consumers, driven by barley's strong association with traditional brewing heritage. Manufacturers are strategically focusing on offering concise ingredient lists that exclude artificial flavors and colorants, thereby reinforcing transparency and enabling the ability to charge slight price premiums. Additionally, product reformulation teams are leveraging barley's higher β-glucan content to position these products as heart-health-friendly, creating a distinct competitive advantage over wheat-based alternatives. The increasing consumer preference for transparent and clean-label ingredient lists is significantly influencing the adoption of barley-based malted milk products. In 2023, 40% of U.S. consumers regularly purchased food or beverages influenced by natural labels, as reported by the International Food Information Council [2]Source: International Food Information Council, "2023 Food and Health Survey", ific.org. The European Union, Russia, and Australia, as the leading global producers of barley, provide a reliable and stable supply base to support clean-label product formulations. Emerging trends indicate a growing focus on high-fiber barley varieties due to their recognized health benefits. This development is directly impacting the malted milk market, as manufacturers aim to enhance the nutritional value of their offerings while maintaining their commitment to clean-label standards.

Nutritional appeal among health-conscious consumers boosts growth

Companies are strategically expanding their product portfolios to emphasize benefits such as gut health, bone strength, and sleep support, aligning with functional segmentation trends in the sports nutrition market. Malted milk, fortified with B-vitamins, calcium, and vitamin D, nutrients often under-consumed in typical diets, features scientifically validated packaging claims. The high nutritional value of malted milk products is driving adoption among health-conscious consumers seeking functional beverage solutions. As per Canadian Food and Drug Regulations, malted milk must contain at least 7.5% milk fat and is produced by blending milk with liquid derived from a mash of ground barley malt and meal [3]Source: Government of Canada, "Justice Laws", laws.gc.ca. Partnerships with dieticians and pediatricians enhance product credibility and facilitate access to institutional channels like hospitals and eldercare facilities, expanding beyond traditional retail distribution. Social media insights indicate a growing trend of consumers associating malted drinks with evening routines, highlighting the untapped market potential for sleep-support blends. By incorporating calming herbal extracts into malted products, brands can establish a premium sub-category with higher profit margins. Additionally, this functional focus drives the adoption of precise portion-control packaging, which can lower per-cup sugar consumption and better align with public health initiatives.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising consumer shift to plant-based “milk” alternatives | -0.6% | North America, Europe | Medium term (2-4 years) |

| Volatile barley and wheat prices due to climate-linked yield variations | -0.5% | Global | Short term (≤ 2 years) |

| High sugar content and rising health concerns | -0.4% | North America, Europe | Short term (≤ 2 years) |

| High prevalence of lactose intolerance in limiting penetration | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer shift to plant-based “milk” alternatives

In North America and Western Europe, the rising prominence of dairy-free beverages is creating a competitive challenge for the traditional malted milk market. Younger consumers, motivated by environmental sustainability and lactose intolerance, are increasingly adopting plant-based alternatives. Taste tests conducted in Southeast Asia reveal that malt flavor effectively masks the off-notes present in legume-based beverages, presenting an opportunity for hybrid malt-and-oat formulations to gain traction in the region. Leading malt brands have already secured trademarks for plant-based product extensions, signaling a convergence of competitive boundaries in the coming years. Traditional malted milk manufacturers are leveraging co-manufacturing agreements with established alternative dairy processors to accelerate market entry and minimize capital expenditure risks. Companies that strategically manage dual portfolios of dairy and dairy-free products are well-positioned to mitigate category cannibalization while capitalizing on emerging growth opportunities.

Volatile barley and wheat prices due to climate-linked yield variations

Extreme weather events have disrupted global barley and wheat supplies, driving volatility in malt prices and compressing producer margins. Futures prices now experience significant intra-seasonal fluctuations, complicating budgeting processes for procurement teams in the malted milk industry. To mitigate these price swings, leading manufacturers are diversifying sourcing origins across continents, accepting increased logistical complexities to achieve cost stability. Additionally, some producers are adopting enzymatic treatments that enable partial substitution of lower-grade grains without compromising diastatic power, thereby reducing raw material risks. Forward-looking companies are securing long-term contracts with growers cultivating drought-resistant varieties, ensuring supply at predetermined premiums. These strategies strengthen the alignment between sustainability initiatives and financial performance, positioning ESG metrics as integral to grain sourcing strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Source: Barley Gaining Ground Despite Wheat Dominance

In 2025, wheat-based products captured 67.86% of the revenue, reflecting their established consumer preference and cost-effective sweetness profile. The global availability of wheat and consistent enzyme performance during malting ensure predictable flavor outcomes. However, evolving regulatory focus on dietary fiber and clean-label trends is driving product innovation teams to emphasize barley’s higher soluble fiber content. Two-row barley grains, recognized for their superior diastatic power, enable efficient sugar conversion and deliver sweeter taste profiles without additional sucrose.

Barley is projected to achieve a robust 8.29% CAGR from 2026 to 2031, unlocking significant growth opportunities. Increasing consumer awareness of beta-glucan’s cardiovascular benefits is expected to narrow the market share gap between barley and wheat in the malted milk segment. The geographically diverse barley production across Europe, Russia, Oceania, and North America provides resilience against regional climatic disruptions. To meet the demand for premium offerings, product developers are incorporating roasted or specialty crystal malts, which naturally deliver caramel-like flavors while eliminating the need for artificial additives. This differentiation strategy appeals to health-conscious adult consumers seeking indulgent yet wellness-aligned options.

Form: Liquid Variants Challenging Powder’s Dominance

In 2025, powder formulations dominated the malted milk market, contributing 80.75% of total sales. This strong performance is attributed to their extended shelf life, ease of storage in households, and compatibility with single-serve sachet packaging, which aligns with consumer preferences for convenience and practicality. Legacy brands have maintained significant household penetration in major markets such as India, China, and Brazil, further driving the growth of the powder format segment. Despite this dominance, the ready-to-drink (RTD) category is emerging as a high-growth segment, with liquid malted beverages projected to achieve a CAGR of 7.34% (2026-2031). This growth is fueled by increasing consumer demand for convenience and strategic partnerships with foodservice providers, including cafés, schools, and convenience stores, which are expanding the availability of RTD products.

Liquid malted beverages are leveraging advanced aseptic processing technologies to preserve flavor integrity and reduce reliance on cold-chain logistics. These innovations are enabling manufacturers to penetrate rural markets with limited refrigeration infrastructure, thereby expanding their distribution networks. Although the formulation of liquid malted beverages involves higher complexity due to the need for emulsion stability, successful product launches in popular flavors such as chocolate, vanilla, and cereal are resonating with younger consumer segments. This trend is not only driving increased adoption among younger demographics but also contributing to the premiumization of the malted beverage consumption experience, positioning the RTD category as a key growth driver in the market.

Packaging Type: Pouches Disrupting Traditional Formats

Plastic jars accounted for 39.85% of the 2025 volume, reflecting their established role in family-size pantry storage. HDPE and PET formats safeguard product integrity and enable wide-mouth openings for convenient scooping. However, eco-concerns and e-commerce growth accelerate a shift to flexible pouches, which are light, require less resin, and lower inbound freight costs. Pouches now post an 8.38% CAGR, making them the fastest-growing packaging segment through 2031.

Leading fillers are strategically investing in recyclable mono-material laminates and post-consumer-recycled (PCR) content to align with circular-economy objectives and enhance their sustainability credentials. In Malaysia, processors are actively experimenting with bio-based resins and high-barrier inks to achieve an optimal balance between environmental sustainability and shelf-life stability, while also adhering to halal compliance standards and addressing the implications of stricter deposit regulations. For brand owners, the adoption of lightweight pouches not only facilitates improved gross-margin retention in the face of inflationary pressures but also creates opportunities to reallocate budgets toward promotional activities, thereby strengthening their competitive positioning in the market.

Distribution Channel: Foodservice Expansion Reshaping Market Dynamics

Retail outlets maintain a stronghold on 43.95% of global turnover, capitalizing on their established shelf presence and offering larger pack sizes with competitive price-per-serving advantages. Meanwhile, the foodservice sector is projected to achieve a 12.18% CAGR (2026-2031), driven by the expansion of café culture, the growth of fast-casual breakfast formats, and meal contracts with educational institutions. In the Middle East, the increasing demand for bulk liquid malted bases, utilized in specialty shakes, is supported by a robust quick-service restaurant pipeline and widespread adoption of delivery apps.

Participation in the foodservice sector enhances brand visibility among adult consumers, encouraging subsequent purchases of companion SKUs for home consumption and fostering an integrated omni-channel strategy. Additionally, the versatility of malt-based recipes enables chefs to incorporate malt flavors into desserts, smoothies, and bakery fillings, driving higher ingredient utilization. In office cafeterias, the adoption of brand-owned fountain dispensers and self-serve machines is contributing to incremental daily servings during weekday operations.

Geography Analysis

Asia-Pacific retains the largest malted milk market share at roughly 36.72% in 2025, buoyed by population growth, increasing middle-class income, and a cultural preference for milk-based nutritional beverages. Regulatory changes mandating clearer sugar labeling have prompted leading brands to reformulate their offerings, resulting in products with reduced sucrose content and enhanced micronutrient profiles. Establishing new greenfield factories in eastern India strategically reduces lead times for delivering finished goods to underserved regions, enabling manufacturers to capture additional rural demand. Tier-2 cities are experiencing the fastest growth in unit sales, reflecting a shift in adoption from urban to suburban areas. By introducing smaller stock-keeping units, manufacturers successfully engage price-sensitive rural consumers, who later transition to larger pack sizes as brand loyalty strengthens.

The Middle East and Africa region is emerging as the fastest-growing region, with a 8.93% CAGR anticipated through 2031, as consumers increasingly opt for premium, functional beverages. Rising awareness of obesity-related health concerns is driving demand for nutrient-dense yet flavorful drinks, positioning malted milk as a preferred choice due to its satiating properties and absence of caffeine. Government-imposed sugar taxes are further incentivizing manufacturers to develop lower-sugar variants. Boutique cafés in Dubai and Riyadh are introducing malted milk lattes, demonstrating the compatibility of Western coffee culture with traditional malted milk offerings. Regional dairy processors are entering licensing agreements with global malt brands, facilitating localization, reducing tariff exposure, and accelerating time-to-market. This growth in the Middle East provides global companies with a strategic opportunity to offset revenue stagnation in mature Western markets.

Europe and North America, while mature markets, are witnessing a resurgence in demand for malted milk under the "new-stalgia" trend, which modernizes traditional flavors with updated nutritional benefits. The report emphasizes a consumer inclination toward reimagined familiar flavors with a contemporary appeal. Regulatory scrutiny on sugar content has driven innovation, with brands adopting natural sweeteners like stevia to maintain flavor while meeting stringent nutritional standards. Digital marketing campaigns are leveraging heritage storytelling to justify premium pricing, connecting long-standing brand loyalty with contemporary wellness trends. Additionally, several European manufacturers are integrating traceable barley supply chains, utilizing blockchain technology to verify provenance and appeal to ethically conscious consumers.

Competitive Landscape

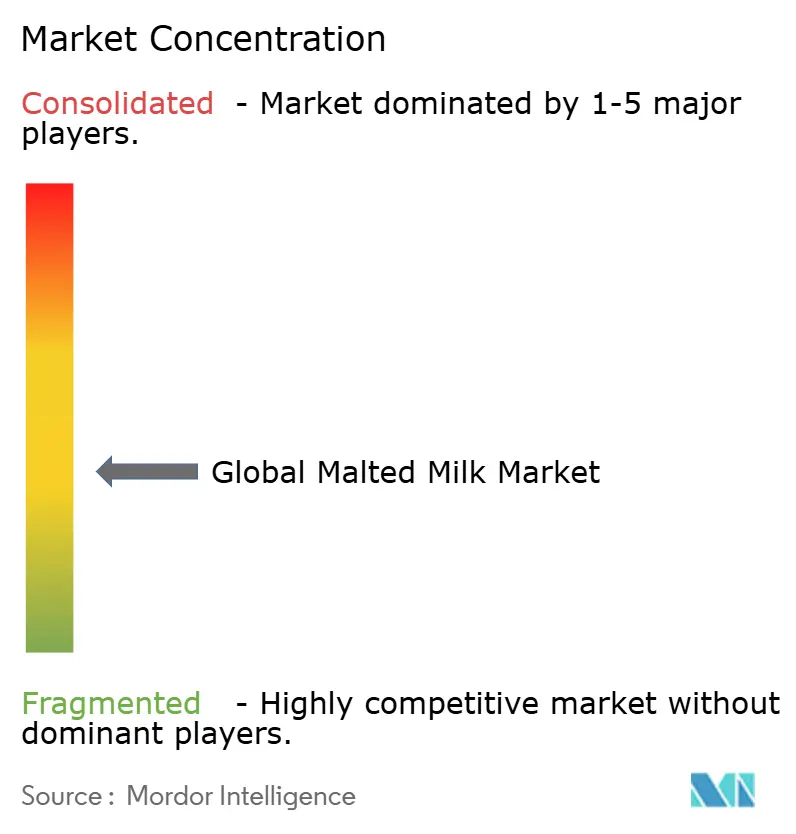

The malted milk market is moderately fragmented, with key players such as Nestle S.A., Associated British Foods Plc, Unilever Plc, Amul (Gujarat Cooperative Milk Marketing Federation), among others commanding significant market shares. These companies are implementing distinct strategies, prioritizing product innovation and health-oriented reformulations to strengthen their competitive positions.

Under increasing regulatory scrutiny, particularly regarding nutritional claims and sugar content, established market players are proactively revising their product positioning and formulations. This evolving regulatory framework offers significant growth potential for agile competitors with strong clean-label credentials. These players are well-equipped to adapt to shifting consumer preferences and meet stringent regulatory requirements, thereby enhancing their competitive advantage in the market.

Growth opportunities are emerging in specialized segments, including functional malted milk products addressing specific health needs and plant-based alternatives catering to the increasing demand for dairy-free options. The industry is increasingly leveraging technological advancements to improve production efficiency and product quality. For instance, Nestlé's CHF 2.5 billion 'Fuel for Growth' initiative focuses on driving operational efficiency and category growth, underscoring the critical role of technology in maintaining a competitive edge.

Malted Milk Industry Leaders

-

Nestle S.A.

-

Associated British Foods Plc

-

Unilever Plc

-

Amul (Gujarat Cooperative Milk Marketing Federation)

-

Briess Malt and Ingredients Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Nestlé has introduced a new low-sugar malted milk drink, aligning with its strategic initiative to address the increasing consumer demand for healthier and sugar-conscious product options across the European market.

- March 2024: Nestlé Australia has invested USD 32 million to upgrade its Smithtown factory, which produces Milo. This strategic investment enhances the Milo manufacturing line by incorporating advanced technology and expanding production capacity.

- January 2024: Ovaltine has introduced a high-protein malted milk powder specifically designed to cater to the growing demand among athletes and fitness enthusiasts. This product aims to address the nutritional needs of this target audience by offering a convenient and effective solution for protein intake.

- September 2023: Nestlé has reformulated its malted milk powder products to include more natural ingredients, aligning with its sustainability goals and addressing growing consumer preferences for cleaner labels and healthier product options.

Global Malted Milk Market Report Scope

Malted milk is a beverage created by combining dried milk with a malt-based formulation.

The malted milk market is segmented by source, form, packaging type, distribution channels, and geography. Based on the source, the market is segmented into wheat, barley, and others. Based on form, the market is segmented into powder and liquid. Based on packaging type, the market is segmented into cans, plastic jars (HDPE/PET), pouches, and others. Based on distribution channels, the market is segmented into retail, food processing, and food service. The retail segment is further segmented into hypermarkets/ supermarkets, convenience stores, online retailers, and other off-trade channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Wheat |

| Barley |

| Others |

| Powder |

| Liquid |

| Cans |

| Plastic Jars (HDPE/PET) |

| Pouches |

| Others |

| Retail |

| Hypermarkets/Supermarkets |

| Convenience Stores |

| Online Retailers |

| Other Off-Trade Channels |

| Food Processing (Industrial) |

| Foodservice |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Wheat | |

| Barley | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Packaging Type | Cans | |

| Plastic Jars (HDPE/PET) | ||

| Pouches | ||

| Others | ||

| By Distribution Channel | Retail | |

| Hypermarkets/Supermarkets | ||

| Convenience Stores | ||

| Online Retailers | ||

| Other Off-Trade Channels | ||

| Food Processing (Industrial) | ||

| Foodservice | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the malted milk market?

The malted milk market is valued at USD 10.27 billion in 2026 and is projected to reach USD 13.33 billion by 2031.

Which region holds the largest share in the malted milk market?

Asia Pacific leads with a 36.72% revenue contribution in 2025.

Which grain source is expanding the fastest within malted milk formulations?

Barley-based products are forecast to grow at an 8.29% CAGR between 2026 and 2031, outpacing wheat variants.

How quickly is the foodservice distribution channel growing for malted milk?

Foodservice sales are projected to advance at a 12.18% CAGR through 2031.

Page last updated on: