Mozambique Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

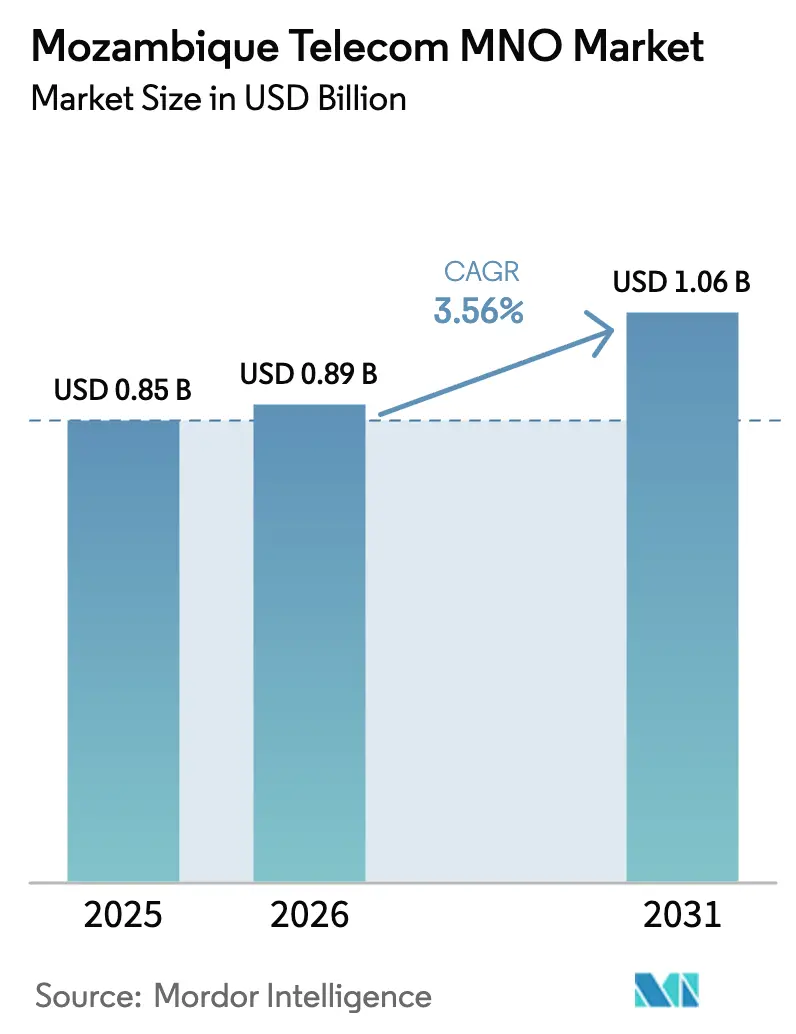

| Base Year Market Size (2025) | USD 0.85 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.06 Billion |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mozambique Telecom MNO Market Analysis by Mordor Intelligence

The Mozambique telecom MNO market size is projected to expand from USD 0.85 billion in 2025 and USD 0.89 billion in 2026 to USD 1.06 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031. Intensifying LNG-related enterprise demand, widening 4G rural coverage, and rapid mobile-money uptake continue to pull revenue toward data-centric and financial-service streams while voice and SMS shrink. Hardware cost deflation for low-Earth-orbit (LEO) satellite backhaul now enables 4G activation in districts where fiber remains uneconomic, narrowing the urban-rural digital divide. However, cyclone-driven infrastructure risk, spectrum-renewal uncertainty, and low per-capita income lengthen payback periods for fresh tower builds, compelling operators to balance rural expansion with enterprise contracts. The Mozambique telecom MNO market therefore enters the forecast period as a cautiously growing, capital-intensive arena in which service-quality leadership often diverges from subscriber scale.

Key Report Takeaways

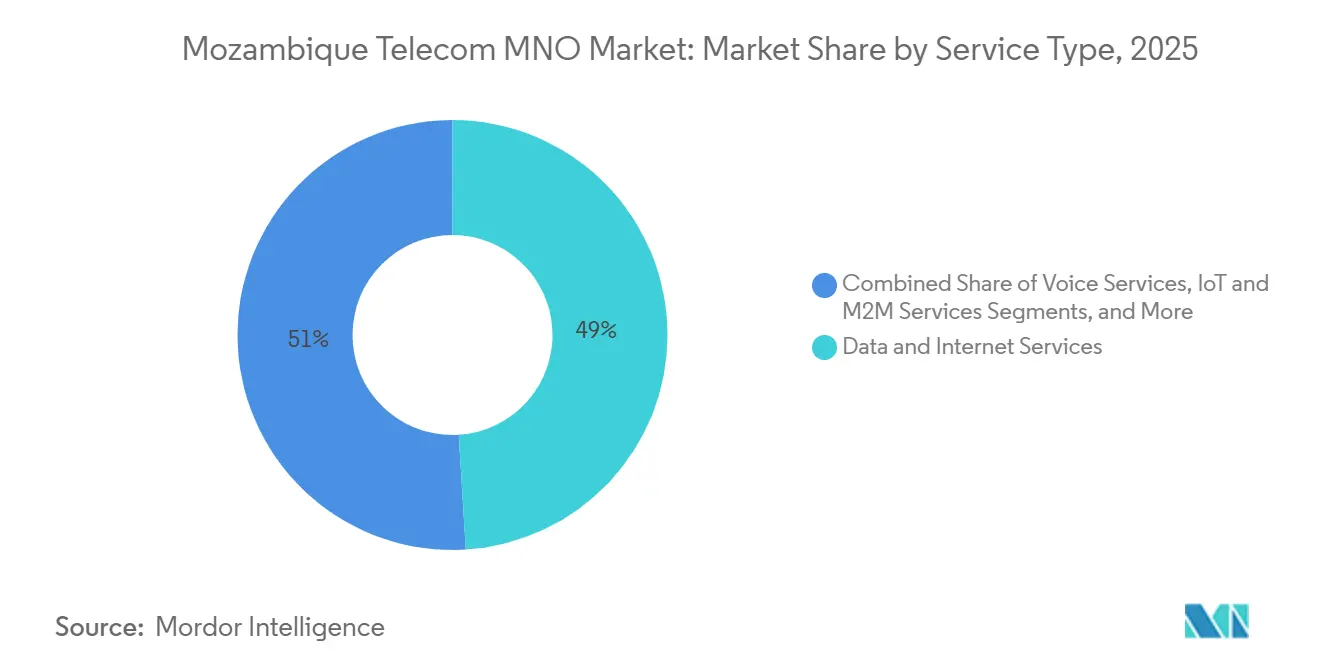

- By service type, Data and Internet Services led with 49.02% of the Mozambique telecom MNO market share in 2025, while IoT and M2M Services are forecast to post the fastest 4.03% CAGR through 2031.

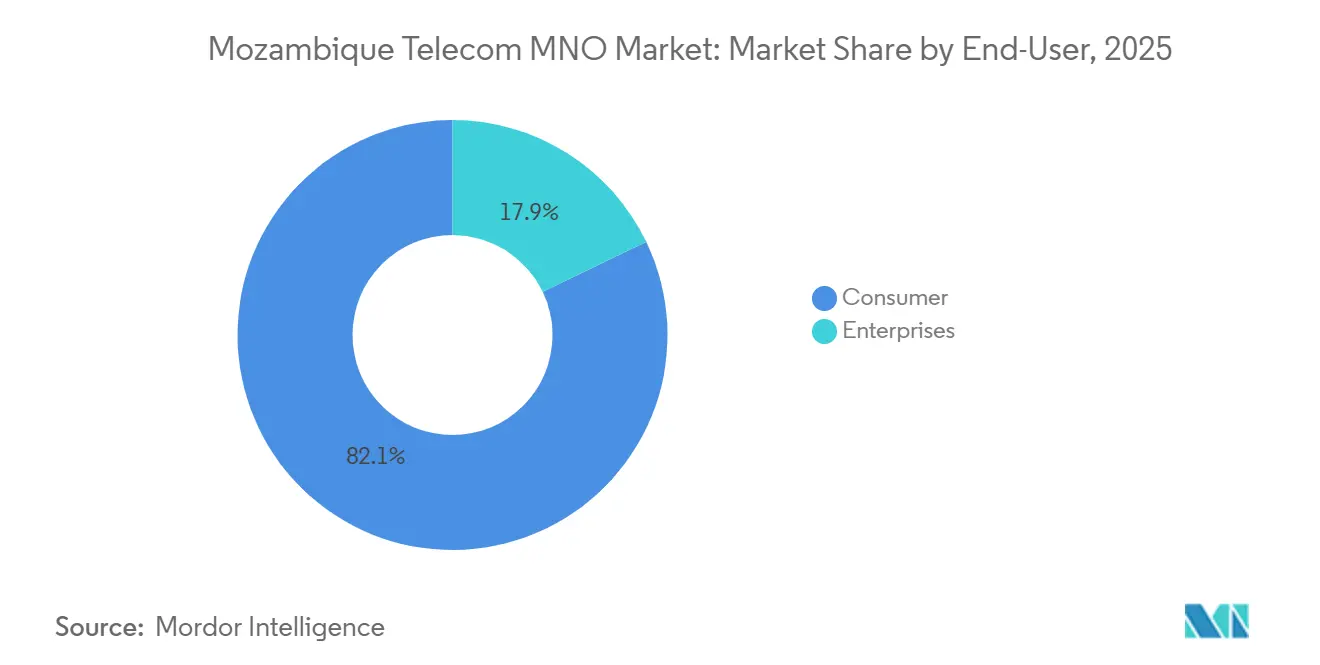

- By end-user, the Consumer segment commanded 82.13% of 2025 revenue, whereas Enterprise connectivity is projected to register the highest 4.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mozambique Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LNG Megaproject-Driven Enterprise Connectivity Demand | +1.2% | Cabo Delgado and Nampula corridor | Long term (≥ 4 years) |

| Expansion of 4G Footprint into Rural Districts | +0.9% | Nationwide, priority in Zambezia, Nampula, Tete | Medium term (2-4 years) |

| Rapid Growth in Mobile Money Ecosystem | +0.7% | Urban centers of Maputo, Beira, Nampula | Short term (≤ 2 years) |

| Entry of LEO Satellite Backhaul Lowering Data Costs | +0.5% | Remote zones of Niassa and Cabo Delgado | Medium term (2-4 years) |

| Planned 5G Licensing and Trials in Maputo | +0.3% | Maputo and provincial capitals | Short term (≤ 2 years) |

| Cross-Border Terrestrial Fiber Corridors to Malawi and Tanzania | +0.2% | Northern border provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

LNG Megaproject-Driven Enterprise Connectivity Demand

TotalEnergies secured USD 4.7 billion in U.S. Export-Import Bank financing in March 2025, restarting its USD 20 billion Mozambique LNG project and reviving demand for high-availability private LTE, VSAT, and managed WAN links along the Cabo Delgado coastline.[1]TotalEnergies, “Mozambique LNG Project Financing and Construction Timeline,” totalenergies.com Eni obtained environmental approval for the 3.5 million-tonne-per-annum Coral Norte FLNG in December 2024, targeting first gas by 2028 and reinforcing long-cycle connectivity contracts that carry ARPU multiples up to ten times consumer levels. ExxonMobil is expected to reach final investment decision on the 15.2 million-tonne Rovuma LNG train in 2026, further thickening the enterprise pipeline. These megaprojects require redundant satellite-hybrid backhaul for offshore rigs, real-time asset telemetry, and workforce e-learning platforms, producing multi-year revenue visibility for operators prioritizing service-level agreements. As a result, the Mozambique telecom MNO market gains a steady enterprise anchor that offsets volatile prepaid voice income.

Expansion of 4G Footprint into Rural Districts

Movitel operated about 1,800 sites by 2024, 55% of which stand in rural areas, lifting national 4G coverage to 70% and 3G to 59.7%.[2]Movitel, “Annual Report and Subscriber Growth Update,” movitel.co.mz Vodacom and Tmcel collectively pushed 4G to 65.45% in 2023, compared with negligible levels four years earlier. The government’s December 2024 "Internet for All" program channels USD 200 million from the World Bank Digital Acceleration Project plus USD 343 million from ProEnergia Plus to co-locate solar-powered towers, particularly in Zambezia and Nampula where mobile-broadband penetration sits below 15%. Coupling tower builds with mobile-money agent expansion, 252,144 points by mid-2024, improves transaction density, raising tower returns. The Mozambique telecom MNO market consequently enters a phase in which rural densification plays twin roles of network extension and digital-financial inclusion.

Rapid Growth in Mobile Money Ecosystem

Platforms processed 401 million transfers worth MZN 340 billion (USD 5.3 billion) in 2023, underscoring mobile money’s ascent from value-added service to revenue pillarZ. Movitel’s e-Mola user base surged 169% in H1 2024 to nearly 6 million accounts, driving a 23% jump in first-half revenue. Vodacom’s M-Pesa broadened into micro-credit and insurance even as a fiscal-year 2025 repricing trimmed service revenue 12.8%.[3]Vodacom Group, “Integrated Report 2025,” vodacom.com An 8% agent-commission tax introduced in August 2025 compressed merchant margins yet failed to slow transaction velocity, confirming durable consumer appetite. Operators monetizing wallet activity also gain churn insulation; e-Mola subscribers churn 30% less than voice-only users, cementing cross-sell synergies that underpin data adoption.

Entry of LEO Satellite Backhaul Lowering Data Costs

Starlink slashed hardware prices 45.7% to MZN 22,000 (about USD 47 monthly service) by April 2024, making satellite backhaul viable for small enterprises and rural schools.[4]Starlink, “Mozambique Service Launch and Pricing Updates,” starlink.com Vodacom concluded a pan-African resale deal with Starlink in November 2025, enabling satellite-terrestrial hybrid sites that halve per-megabit costs where fiber is absent. OneWeb, via Dimension Data and Q-KON, targets government verticals with latency-sensitive solutions such as tele-medicine. Competitive tension is forcing terrestrial carriers to cut wholesale rates, which accelerates tower rollouts in low-density districts. As satellite economics improve, the Mozambique telecom MNO market sees unprecedented optionality in rural backhaul, hastening universal broadband goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclone-Induced Coastal Infrastructure Damage Risk | -0.8% | Sofala, Zambezia, Inhambane, Nampula coastline | Short term (≤ 2 years) |

| Low Disposable Income and Digital Literacy Gaps in Hinterland | -0.6% | Niassa, Cabo Delgado, Tete rural districts | Long term (≥ 4 years) |

| Elevated Spectrum Renewal Fees and Sector-Specific Taxes | -0.4% | Nationwide | Medium term (2-4 years) |

| Persistent SIM Registration Bottlenecks and Gray-Market SIMs | -0.2% | Informal urban settlements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyclone-Induced Coastal Infrastructure Damage Risk

Cyclone Freddy inflicted USD 150 million in regional damage during early 2023, toppling 263 Vodacom sites across Sofala and Manica and triggering USD 19.5 million in Movitel restoration outlays between 2019 and 2023. Operators now embed annual storm-hardening budgets equal to 3-5% of network capex, raising effective site costs and stretching break-even in otherwise population-dense littoral cities. February 2026 floods proved less destructive after resilience upgrades, yet Mozambique’s 2,500 km coastline remains on an 18-24-month cyclone cycle, sustaining elevated risk premiums. The Mozambique telecom MNO market consequently carries a persistent weather-related cost burden that tempers investor enthusiasm for coastal densification.

Low Disposable Income and Digital Literacy Gaps in Hinterland

Average broadband service costs USD 3.90 per month, 8.5% of per-capita GDP below USD 500, compared with the 4.7% global median, underscoring affordability constraints. Electricity access stood at 48% in 2024, with rural districts averaging under 12 grid-powered hours daily. Digital-literacy shortfalls mean barely 30% of rural adults navigate smartphone menus beyond voice calls, capping prepaid ARPU below USD 3. As a result, the Mozambique telecom MNO market expands in volume but struggles to lift spending per user, forcing operators to rely on subsidies or universal-service funds for hinterland network economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Overtakes Voice, IoT Emerges

Data and Internet Services captured 49.02% of the Mozambique telecom MNO market in 2025, mirroring the rapid substitution of OTT messaging for traditional voice. Vodacom’s voice revenue declined 12.8% in fiscal 2025 as WhatsApp and Telegram use deepened. Meanwhile, IoT and M2M traffic is positioned to rise at a 4.03% CAGR, buoyed by LNG telemetry, agriculture-sector GPS tracking, and early smart-meter pilots in Maputo and Beira. Messaging and PayTV remain peripheral given low disposable income and modest fixed-broadband reach. Operators that integrate mobile-money wallets with data bundles demonstrate greater ARPU resilience.

Voice and SMS will continue to erode as smartphone penetration climbs toward 40% by 2031. Mobile-money ecosystems embed financial exchanges within data sessions, elevating lifetime customer value and offsetting price compression. The Mozambique telecom MNO market size for IoT connectivity is small today yet strategic, acting as a beachhead for managed services that generate enterprise stickiness. Carriers that scale IoT platforms alongside data loyalty packages are likely to enhance margin depth over the forecast horizon.

By End-User: Enterprise Growth Outpaces Consumer Base

Consumer accounts for 82.13% of 2025 revenue, but enterprise demand is forecast to advance at 4.47% CAGR, outstripping mass-market growth. Starlink-Vodacom hybrid offers give small businesses and rural schools high-availability links once reserved for corporates. Movitel logged a 26.7% enterprise-revenue surge in early 2024 on the back of private LTE for Tete mining and Nacala port logistics .

Consumer ARPU remains under USD 3 and churn exceeds 3% monthly in Maputo and Beira, hampering profitability. Yet government Digital Transformation projects targeting 13,000 schools promise steady connectivity contracts. Operators that prioritize enterprise service-level agreements, bundled with IoT and mobile money, are expected to enjoy Mozambique telecom MNO market share advantages, whereas carriers tied to prepaid consumer voice face structural margin erosion.

Geography Analysis

Growing Mobile Data Consumption Per Capita

Southern provinces, led by Maputo and Matola, generate the highest data consumption per user and house Vodacom’s USD 25 million Tier III data center completed in July 2024. Central hubs like Beira show accelerating 4G take-up following cyclone-resilience upgrades, while Sofala’s frequent storm exposure still depresses tower density relative to demand.

Northern Cabo Delgado and Nampula are seeing outsized enterprise momentum due to LNG megaprojects. Coral Norte, Mozambique LNG, and prospective Rovuma LNG collectively attract expatriate staff and supply-chain traffic that push premium data and private LTE orders. As a result, the Mozambique telecom MNO market size for enterprise connectivity in the north is set to outstrip the consumer-led south by the late 2020s.

The interior provinces of Niassa and Tete lag in both penetration and spending, constrained by low electrification and sparse population. LEO satellite backhaul combined with solar-microgrid programs are expected to narrow the gap, but return on investment remains thin without universal-service subsidies. The Mozambique telecom MNO market therefore exhibits a pronounced north-south corporate skew and an east-west rural deficit that shapes capital-allocation priorities.

Competitive Landscape

Government Spectrum Allocations for 5G Readiness

Three licensees, Movitel, Vodacom, and Tmcel, collectively control 100% of subscribers, leaving the Mozambique telecom MNO market moderately concentrated. Movitel surpassed Vodacom in May 2024 by reaching 11.7 million active SIMs, yet Vodacom retains network-quality leadership with 21-26 Mbps download speeds compared with Movitel’s 8-9 Mbps, reflecting divergent CapEx focus.

Vodacom’s Matola data center positions the firm for cloud hosting and content-delivery demand, while its Starlink partnership adds a satellite-hybrid arrow to the rural-coverage quiver. Movitel emphasizes rural tower density, leveraging its Viettel backing to undercut peers on build costs. Tmcel, burdened by EUR 59.7 million (USD 65.0 million) losses in 2024, still holds key government contracts but lacks funding for broad 4G upgrades.

No independent tower companies operate, meaning all 4,600 sites remain operator-owned, limiting infrastructure-sharing savings seen elsewhere. The regulator pivoted from auctions to administrative spectrum awards in November 2025, mandating 5G in every provincial capital but delaying fee clarity, a decision that clouds long-range capital planning. Operators with diversified enterprise portfolios and resilient backhaul strategies are therefore best placed to secure profitable Mozambique telecom MNO market share gains.

Mozambique Telecom MNO Industry Leaders

Vodacom Mozambique

Movitel (Viettel Global)

Tmcel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Instituto Nacional de Comunicações de Moçambique began issuing administrative 5G frequency allotments following the 2025 auction cancellation.

- November 2025: Vodacom Mozambique signed a resale partnership with Starlink, bundling satellite backhaul with rural 4G sites.

- November 2025: Government confirmed shift to administrative spectrum allocation with compulsory provincial-capital 5G coverage.

- October 2025: INCM opened a public consultation on streamlined spectrum-licensing procedures.

Mozambique Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means.

The Mozambique Telecom MNO Market Report is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, IoT and M2M Services, OTT and PayTV Services, and Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, Rest of Service Type)), End-User (Enterprises, and Consumer), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What Is the Projected Revenue of the Mozambique Telecom MNO Market by 2031?

It is expected to reach USD 1.06 billion by 2031.

Which Service Category Currently Leads Revenue?

Data and Internet Services led with 49.02% of 2025 revenue.

Which Segment Is Forecast to Grow Fastest Through 2031?

IoT and M2M connectivity is projected to expand at a 4.03% CAGR.

Why Are LNG Projects Important for Operators?

They generate long-term private LTE and backhaul contracts that stabilize enterprise revenue.

How Is Satellite Backhaul Affecting Rural Coverage?

Starlink and OneWeb partnerships are halving per-megabit costs, enabling 4G rollout in low-density areas.

What Remains the Biggest Operational Risk for Network Assets?

Recurring cyclone damage along the 2,500 km coastline raises capex for storm-hardening measures.

Page last updated on: