Togo Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

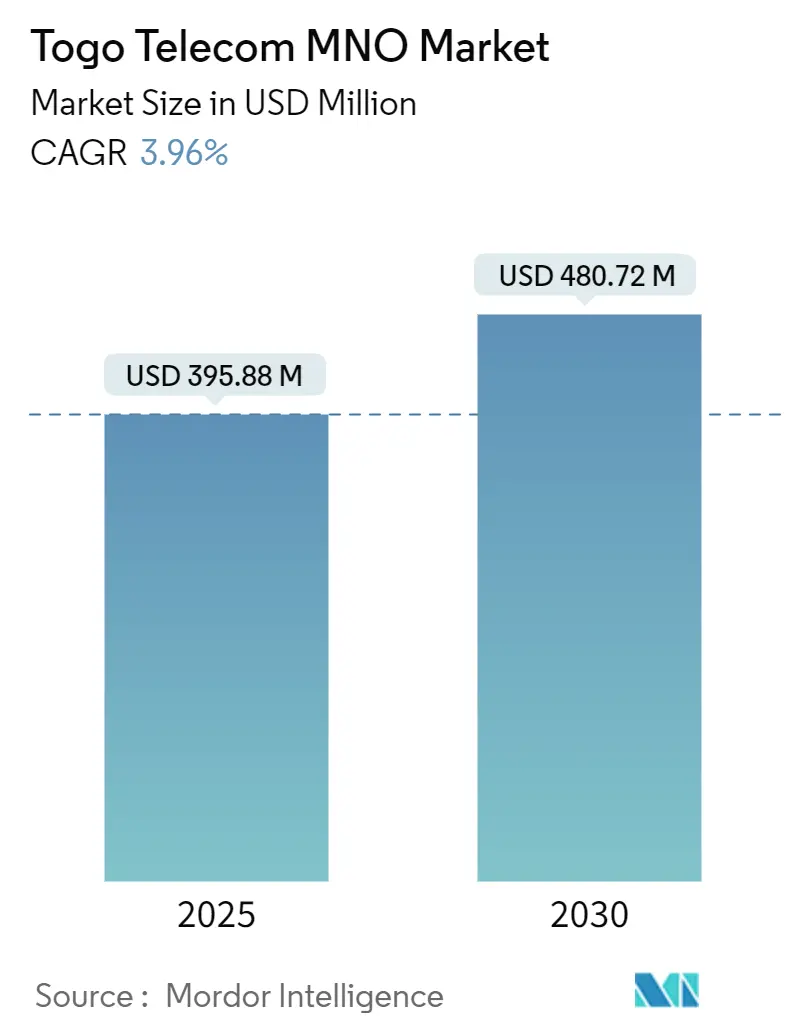

| Market Size (2025) | USD 395.88 Million |

| Market Size (2030) | USD 480.72 Million |

| Growth Rate (2025 - 2030) | 3.96% CAGR |

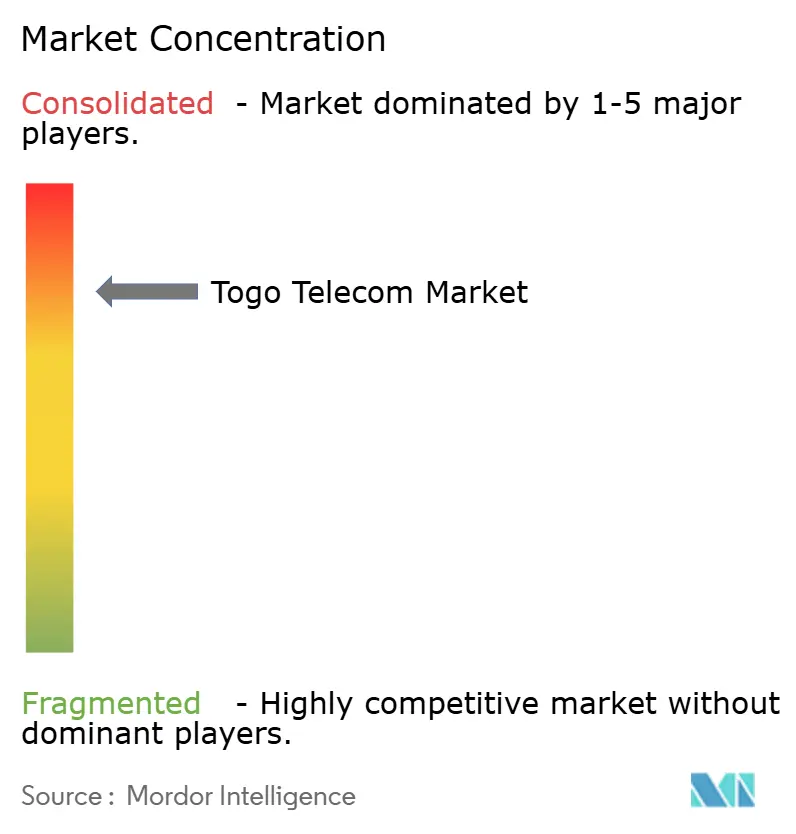

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Togo Telecom MNO Market Analysis by Mordor Intelligence

The Togo telecom MNO market size stands at USD 395.88 million in 2025 and is forecast to reach USD 480.72 million in 2030, expanding at a 3.92% CAGR. This measured rise stems from sustained capital inflows-most visibly the World Bank’s USD 100 million digital-transformation loan approved in December 2024 and the International Finance Corporation’s EUR 55 million facility for Togocom-to accelerate nationwide 4G and fiber rollout.[1]World Bank, “Togo Digital Acceleration Project,” worldbank.org ECOWAS free-roaming implementation in October 2024 reshapes international-calling economics, while mobile money’s CFA 917 billion transaction value underpins stickier average revenue per user (ARPU). Infrastructure resilience improves through Google’s Equiano cable landing, yet security concerns in northern prefectures and a heavy tax burden still temper growth prospects.[2]International Finance Corporation, “IFC Loans EUR 55 Million to Togocom,” ifc.org

Key Report Takeaways

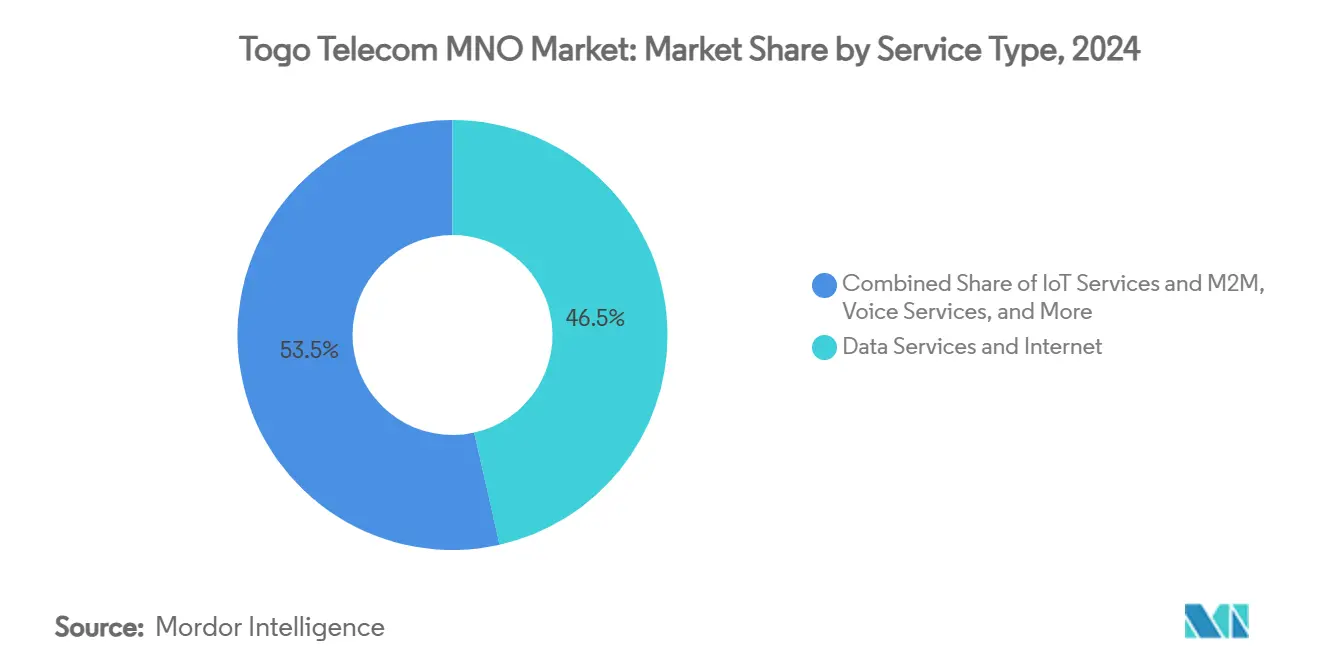

- By service type, data and internet services led with 46.66% revenue share in 2024; IoT and M2M services are projected to expand at a 4.49% CAGR to 2030.

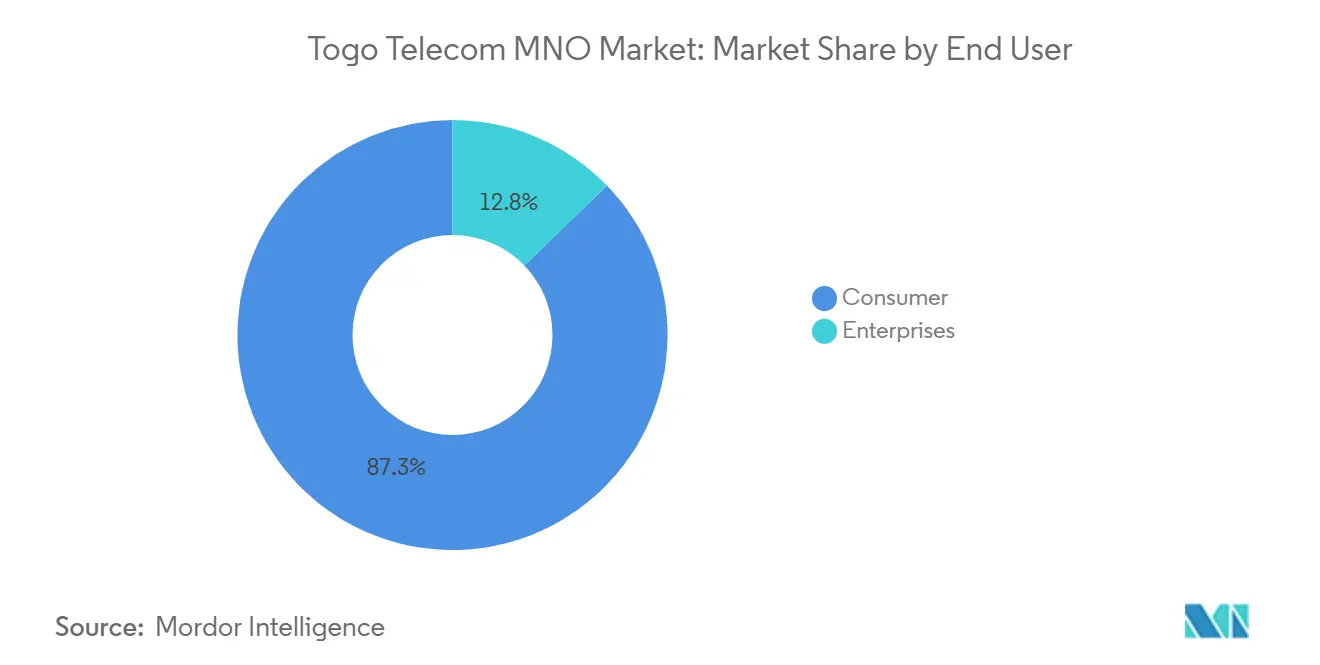

- By end user, the consumer segment represented 87.25% of market value in 2024, whereas enterprise demand is forecast to register a 4.28% CAGR through 2030.

Togo Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Traction of mobile data-first bundles and social-media packs | +0.8% | National, concentrated in Lomé and Kara urban centers | Short term (≤ 2 years) |

| Rapid 4G rollout supported by World Bank West Africa Digital Integration project | +0.6% | National, with priority on rural connectivity gaps | Medium term (2-4 years) |

| Expansion of regional free-roaming (ECOWAS) agreement | +0.4% | Cross-border corridors, Lomé-Ouagadougou trade route | Medium term (2-4 years) |

| Strong uptake of mobile money driving stickier ARPU | +0.5% | National, highest penetration in urban areas | Short term (≤ 2 years) |

| Government subsidy scheme for rural fibre backhauls (2025-28) | +0.3% | Rural prefectures, northern regions priority | Long term (≥ 4 years) |

| Upcoming Lomé data-centre hub attracting OTT traffic localisation | +0.2% | Lomé metropolitan area, regional spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Traction of Mobile Data-First Bundles and Social Media Packs

Operators now prioritize data-centric tariffs, bundling low-denomination social-media passes that fit the spending patterns of Togo’s median-age-19 population. Social-media users are rising, catalyzing surging demand for budget-friendly gigabyte packages. The mechanism raises ARPU without chasing incremental subscribers because the majority of the residents already own a SIM card. Integrated offers that allow airtime conversion into TMoney top-ups further entwine connectivity with financial services and reinforce customer loyalty.

Rapid 4G Rollout Supported by West Africa Digital Integration

World Bank co-financing lowers backbone-network costs by funding neutral colocation sites and rural fiber-spurs, enabling operators to stretch 4G into settlements heretofore limited to 2G coverage. IFC’s loan terms tie disbursement to achieving 95% connectivity for schools and clinics by 2025, aligning commercial incentives with universal-service objectives. Shared passive-infrastructure models keep capex down and speed deployment, helping narrow the urban-rural broadband gap.

Expansion of ECOWAS Free-Roaming Agreement

Since October 2024, calls and SMS within Ghana, Togo, and Benin are priced at domestic rates for 30 days, which removes the deterrent cost of cross-border communications along the high-traffic Lomé-Ouagadougou route. While operators surrender part of roaming revenue, they recover value through larger minute volumes, improved churn metrics, and data-package upselling to frequent travelers. Extension of the regime to other ECOWAS members could ultimately create a contiguous West African retail-tariff zone, exacerbating price-based rivalry yet enlarging addressable demand.

Strong Uptake of Mobile Money Driving Stickier ARPU

Mobile-money flows reached USD 1.54 billion in early 2024 after the government cut transaction levies to 10%. This deepens financial inclusion—mobile-money penetration stands at 42.4%—and binds subscribers to their host network because account balances and transaction histories are non-portable even under number-portability rules. Emerging entrants such as Gozem Money may disrupt the incumbent duopoly, but the overall payment ecosystem raises daily SIM interaction frequency and cushions revenue volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sector-specific tax burden on SIMs and airtime | -0.4% | National, disproportionate impact on low-income segments | Short term (≤ 2 years) |

| Limited international bandwidth redundancy beyond WACS cable | -0.3% | National, critical for data services growth | Medium term (2-4 years) |

| Chronic right-of-way disputes slowing fiber trenching | -0.2% | Urban expansion areas, peri-urban development zones | Long term (≥ 4 years) |

| Security-related shutdown risks in northern prefectures | -0.2% | Northern border regions, Savanes prefecture | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Sector-Specific Tax Burden on SIMs and Airtime

Composite taxes on handsets, SIM cards, and recharge vouchers weigh heavily on low-income users, suppressing incremental subscriber growth despite latent demand. Operators attempting to pass through costs risk eroding the affordability of data bundles just as 4G coverage expands, pushing marginal users back to zero-rated over-the-top (OTT) messaging. Government willingness to trim mobile-money levies suggests space for broader telecom-tax reforms that could unlock an additional 0.4-0.6 percentage-point CAGR lift.

Limited International Bandwidth Redundancy Beyond WACS Cable

Dependence on the single legacy WACS link exposes the country to outages and constrains wholesale-capacity price declines. Although Google’s Equiano landing diversified supply in 2022, a second independent route remains necessary to guarantee always-on enterprise-grade connectivity demanded by financial-services and cloud-outsourcing customers. Until new subsea routes or satellite gateways materialize, tight backhaul supply may bottleneck high-definition streaming and large-file cloud adoption for SMEs.[3]Togo First, “Equiano Cable Boosts International Capacity,” togofirst.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Underpin Digital Shift

Data and internet services captured 46.66% of 2024 revenue, illustrating how usage has moved from basic voice toward broadband. The Togo telecom MNO market size for data services is projected to widen in lockstep with smartphone adoption and social-media engagement. IoT and M2M services are still nascent, but their 4.29% CAGR through 2030 signals rising demand from agriculture sensors and logistics tracking. Voice revenue continues to decline as a proportion of total turnover, yet a sizeable prepaid base still relies on per-minute packs for informal communications. Operators therefore balance legacy revenue protection with upselling paths into data-heavy bundles linked to mobile-money discounts.

OTT video and music platforms finally achieve scale thanks to localized content delivery nodes in Lomé’s carrier hotel, lowering latency and buffering. Enterprise demand for managed data links rises as the government’s e-health and e-education programs hook up 8,000 public-sector sites. Taken together, these factors position data services as the anchor product around which adjacent revenue lines, such as cloud and cybersecurity, can develop.

By End User: Enterprises Accelerate Digital Adoption

Consumers still contribute 87.25% of operator revenue, yet enterprise connections grow faster at a 4.28% CAGR as ministries, banks, and logistics firms digitize workflows. The Togo telecom MNO market size for enterprise connectivity thus expands more rapidly, driven by SLAs that require a minimum 99.9% uptime and burstable throughput. Smart city pilots and agricultural IoT platforms tip fresh enterprise demand into the addressable base.

The Novissi digital-cash program showed how large-scale, government-led platforms can register over 1 million residents in a week, signaling systemic readiness for advanced e-government services. Consumer revenue growth, in contrast, derives mainly from upselling data-bundled offers rather than net-new SIM additions, highlighting the need for ARPU-friendly innovation rather than pure subscriber acquisition.

Geography Analysis

Urban corridors dominate the usage. Lomé alone concentrates over 72% of national GDP and 65% of the population, making it the undisputed hub for high-capacity backhaul, data-center investment, and corporate headquarters. The Togo telecom MNO market hence sees 75% of total spend originate in cities even though just 44.8% of residents live there, reflecting higher per-capita disposable income and digital-service affinity. Fiber rings radiate from the port city toward the Ghana border and northward along the Lomé-Ouagadougou trade axis, mirroring transport arteries that carry both physical and digital traffic.

The Maritime and Plateaux regions post the highest SIM penetration, benefiting from proximity to Equiano’s landing station and the first carrier-neutral colocation site opened in 2021. By contrast, the northern Savanes prefecture struggles with both economic deprivation and security risks that periodically cut power and backhaul to tower sites. Operators regularly report forced diesel diversions and staff-movement bans, mirroring Orange Burkina Faso’s inability to reach 15% of its northern towers.

Government intervention seeks to rebalance this geographic skew. Rural-fiber backhaul subsidies between 2025-28 earmark trenching support for underserved prefectures, while solar mini-grids improve base-station uptime where grid supply is episodic. Free Wi-Fi zones are already live at university campuses in Lomé and Kara, and the next phase extends shared access points to 500 rural schools. ECOWAS free-roaming also lifts traffic in border towns, especially in Kpalimé and Sanvee-Condji, where petty traders cross daily and now call home at domestic tariffs.

Competitive Landscape

Three nationwide mobile-network operators create a moderately concentrated arena. AXIAN-owned Yas (formerly Togocom) retains lead share strengthened by TMoney’s 61% grip on the mobile-money pool, while Moov Africa counters via its Flooz wallet and regional brand leverage. New MVNOs such as Telecel and ISP-turned-mobile player GVA-Togo Mobile nibble at urban data-hungry niches, relying on wholesale access to Yas and Moov radio networks.

Strategic differentiation pivots on digital-financial-services integration rather than pure connectivity. TMoney adds micro-savings and pay-as-you-go solar to lock in daily transactions; Moov Flooz partners with agro-dealers for fertilizer-voucher disbursement. Gozem Money’s expected late-2025 launch in tandem with NSIA Bank could spark price competition in peer-to-peer transfers, yet winning scale will hinge on agent-network density.

Technology focus stays on 4G densification ahead of any mass-market 5G case. Operators co-invest in passive infrastructure to speed coverage and defray capex, supported by the regulator’s infrastructure-sharing guidelines. ECOWAS roaming parity erases a traditional profit line but opens data-bundle cross-sales to business travelers. Overall, market conduct remains price-competitive yet rational, with spectrum auctions and quality-of-service audits providing external discipline.

Togo Telecom MNO Industry Leaders

Togocom

Moov Africa Togo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: World Bank approved USD 100 million to connect 8,000 public institutions and train one million citizens in digital skills

- November 2024: AXIAN Telecom rebranded Togocom to “Yas,” unifying its pan-African mobile identity.

- October 2024: Ghana, Togo, and Benin activated 30-day free-roaming for voice and SMS under ECOWAS guidelines.

- January 2024: IFC extended EUR 55 million to Togocom for network modernization.

Togo Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current size of the Togo telecom market?

The Togo telecom MNO market size stands at USD 395.88 million in 2025 and is forecast to grow to USD 480.72 million by 2030.

Which service category generates the most revenue?

Data and internet services lead the revenue mix with a 46.66% share in 2024, reflecting the shift from voice-centric plans to broadband consumption.

How fast is enterprise demand growing?

Enterprise connectivity revenue is projected to rise at a 4.28% CAGR through 2030 as ministries, banks, and logistics firms digitize operations.

What impact does the ECOWAS free-roaming agreement have on operators?

The policy removes international tariffs for 30 days, raising traffic volumes along trade corridors while compressing legacy roaming margins.

Why is mobile money critical to operator strategy?

With CFA 917 billion in annual transactions, mobile-money platforms deepen customer loyalty and stabilize ARPU, offsetting price competition in core connectivity.

Is 5G deployment imminent in Togo?

Operators remain focused on 4G densification; they intend to evaluate 5G only after handset penetration and enterprise use cases justify the investment.

Page last updated on: