Bulgaria Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 2.27 Billion |

| Market Size (2030) | USD 2.72 Billion |

| Growth Rate (2025 - 2030) | 3.72% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bulgaria Telecom MNO Market Analysis by Mordor Intelligence

The Bulgaria Telecom MNO Market size is estimated at USD 2.27 billion in 2025, and is expected to reach USD 2.72 billion by 2030, at a CAGR of 3.72% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 10.64 million Subscribers in 2025 to 12.68 million Subscribers by 2030, at a CAGR of 3.57% during the forecast period (2025-2030). This measured rise reflects a pivot from voice to data-centric revenue streams underpinned by 5G roll-outs, fiber-to-the-home (FTTH) projects, and steady EU funding that targets rural coverage gaps. Accelerated spectrum licensing, robust demand for mobile video, and the near-shoring boom in IT services keep data traffic moving upward, while network slicing and private 5G proposals open fresh enterprise opportunities. Operators mitigate pricing pressure by bundling converged fixed-mobile plans and leveraging government grants to limit capital risk. Regulatory FDI screening rules temper merger activity, yet infrastructure-light challengers continue to enter wholesale niches, sustaining healthy rivalry in the Bulgaria telecom MNO market.

Key Report Takeaways

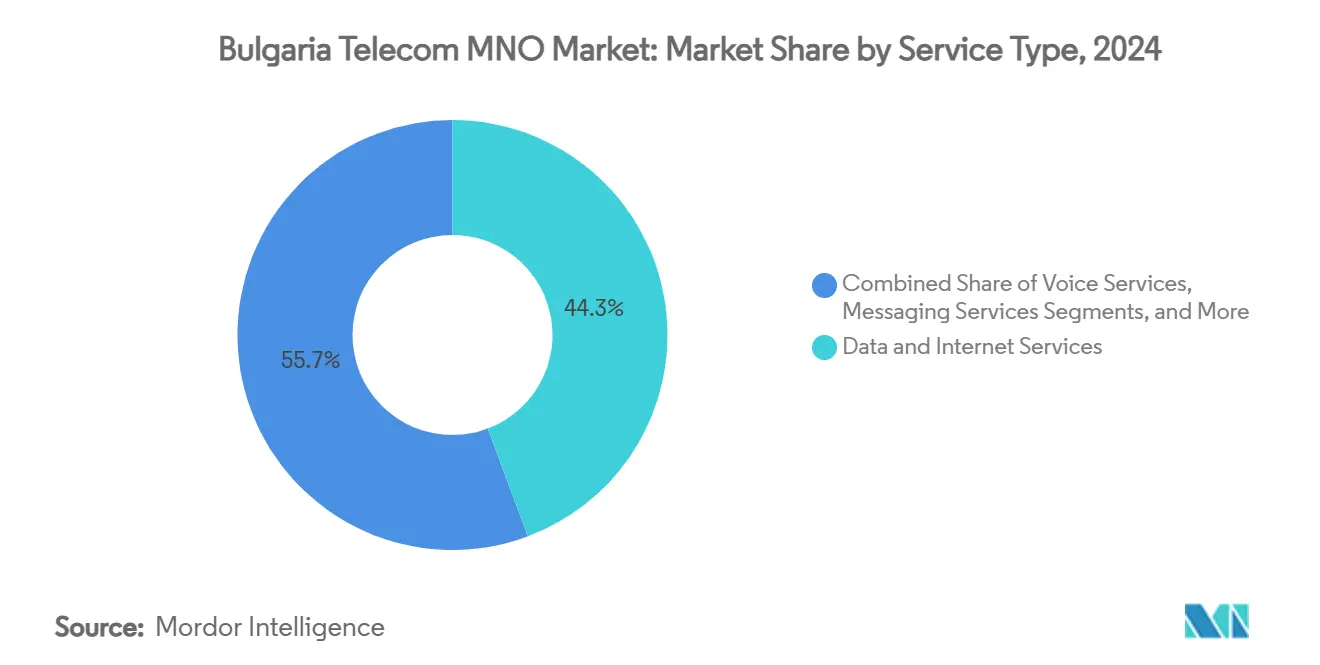

- By service type, data and internet services led with 44.28% revenue share in 2024, while IoT and M2M services are projected to post the fastest 4.75% CAGR through 2030.

- By end user, consumer subscriptions accounted for 68.26% revenue share in 2024, whereas enterprise connectivity is forecast to advance at a 3.82% CAGR to 2030.

Bulgaria Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Spectrum Auctions and Accelerated Roll-out by A1, Vivacom, Yettel | +0.8% | Sofia, Plovdiv, Varna | Medium term (2-4 years) |

| Surge in Mobile Data Traffic from Video Streaming and Social Media | +0.6% | Urban centers nationwide | Short term (≤2 years) |

| Rapid FTTH Expansion Enabling Gigabit Broadband | +0.5% | Rural priority zones | Long term (≥4 years) |

| EU RRF Grants for Rural 5G Corridors and Cross-border Transport Routes | +0.4% | Border and transport corridors | Long term (≥4 years) |

| Demand for Private 5G/Network Slicing in Industrial Zones | +0.3% | Industrial zones | Medium term (2-4 years) |

| Near-shoring Boom of IT Services Drives Enterprise IoT and Data Links | +0.2% | Sofia, Plovdiv, Varna | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Spectrum Auctions and Rapid Roll-out by A1, Vivacom, Yettel

In December 2023, regulators made a pivotal decision by granting long-term licenses in the 700 MHz, 800 MHz, and 3.6 GHz bands. This allocation provided operators with the necessary spectrum depth to deploy true standalone 5G networks. Shortly after, A1 launched Bulgaria's first nationwide 5G network, followed closely by Vivacom and Yettel, each emphasizing their strengths in coverage, throughput, and latency. Vivacom now covers 92% of the population, placing Bulgaria among the leading EU nations in 5G adoption. [1]Vivacom, “5G Coverage Map,” vivacom.bg Enterprises have taken notice, with automotive plants near Plovdiv and logistics hubs near Sofia Airport initiating network-slicing trials to secure dedicated bandwidth and reliable performance. Additionally, the auctions have intensified competition in rural fixed-wireless access, where fiber trenching remains cost-prohibitive. Overall, these new spectrum licenses have transitioned next-generation connectivity from a theoretical concept to a nationwide implementation, creating monetization opportunities for operators over the next three years.

Surge in Mobile Data Traffic from Video Streaming and Social Media

Bulgarian consumers discovered binge streaming during the 2020 lockdowns, and network statistics show that the habit has endured; mobile data volumes jumped 17% that year and have continued to rise steadily since then. [2]Kaldata, “Mobile data traffic up 17%,” kaldata.com Unlimited bundles with 4K streaming sweeteners are now the default on post-paid plans, and even prepaid users expect video without throttling. Vivacom leaned into the trend by introducing “truly unlimited” tariffs that remove speed caps for heavy streamers. Traffic patterns have also changed when subscribers catch up on series, forcing operators to add edge servers and increase their backhaul capacity. The same video craze spills into the business world, where remote meetings, cloud collaboration, and security feeds load networks around the clock. The constant demand for bandwidth keeps revenue flowing on premium tiers while simultaneously pushing carriers to invest in extra spectrum and densified cell sites.

Rapid FTTH Expansion Enabling Gigabit Broadband

Fiber networks that once focused on Sofia’s apartment blocks now reach deep into provincial towns, owing to United Group’s plan to knit Southeast Europe into a single optical footprint. Vivacom alone passes 1.6 million homes with fiber and offers residential packages up to 2 Gbps, leveraging speed as a marketing advantage. Rural villages, such as those relying on patchy DSL, can now finally upload compliance data and run smart irrigation apps in real-time. Operators value fiber as it reduces churn when bundled with mobile services, because customers rarely abandon converged contracts. The European FTTH Council’s latest survey even places Bulgaria alongside its wealthier peers in terms of penetration, confirming that aggressive build-outs are paying off in terms of adoption. Over the long haul, the country’s large fiber footprint acts as a stable platform for ultra-HD streaming, cloud gaming, and small-business back-ups, helping revenue grow faster than basic population trends would suggest.

EU RRF Grants for Rural 5G Corridors and Cross-Border Routes

Brussels allocated EUR 270 million from the Recovery and Resilience Facility to extend high-capacity networks to sparsely populated areas and remote transport corridors. Projects range from building new towers along Danube shipping lanes to laying fiber across mountain passes that tourists frequent in winter. Operators tap the grants to reduce payback risk and meet Digital Decade milestones without loading more debt on already thin margins. Farmers in northern provinces are now planning IoT soil-monitoring pilots, while cross-border truckers expect seamless connectivity that eliminates roaming surprises. Municipalities gain significant leverage in public-private partnership negotiations, ensuring that local roads are equipped with small-cell coverage rather than being left in dead zones. With funds disbursed over several years, the grants provide a reliable pipeline of work, keeping contractors engaged and maintaining the digital relevance of rural communities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-war-driven Low ARPU Eroding Margins | −0.4% | Urban markets | Short term (≤2 years) |

| Digital-skills Gap Limiting Advanced Service Uptake | −0.3% | Rural and aging areas | Long term (≥4 years) |

| Population Decline and Emigration Shrinking Consumer Base | −0.2% | Rural regions | Long term (≥4 years) |

| Energy-price Volatility Inflating Network OPEX | −0.2% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-War-Driven Low ARPU Eroding Margins

Bulgaria's three mobile operators have historically engaged in intense price competition, positioning the country near the bottom of the EU rankings for average revenue per user. While this approach earned recognition for offering "Europe's cheapest data," it significantly limited the ability to invest in new 5G infrastructure and improved customer support. Vivacom’s 4.7% tariff increase in early 2024 was the first sign that deep discounts might finally be unsustainable. [3]СЕГА, “Vivacom raises tariffs 4.7%,” segabg.com Even after the hike, monthly bills remain well below the EU average, so operators continue to walk a tightrope between recovering profits and minimizing subscriber churn. Low ARPU also dampens investor appetite as bond markets price Bulgarian telecom debt higher than its regional peers because returns appear thin.

Digital-Skills Gap Limiting Advanced Service Uptake

Only about one-third of Bulgarians possess basic digital skills, a shortfall that significantly hinders the potential of 5G, IoT, and cloud services. Less than 30% of organizations have adopted advanced technologies such as big data analytics or AI, which has tempered their demand for premium connectivity. Rural schools face a shortage of qualified instructors, and many older citizens remain hesitant to engage with online banking or e-government portals. This hesitancy limits the demand for high-bandwidth applications in non-urban areas. The state has allocated EUR 319 million for upskilling programs; however, transforming habits and curricula will require a significant amount of time. Meanwhile, operators encounter delays in the pre-sales phase of sophisticated B2B products, as decision-makers often fail to recognize the return on investment. Addressing the skills gap is crucial, not only to promote social equity but also to unlock the next phase of telecom revenue growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data and Internet Services Drive Revenue Transformation

Data and Internet services generated 44.28% of 2024 revenue, anchoring the Bulgaria telecom MNO market as consumers and enterprises migrate to cloud applications. IoT and M2M services, though still single-digit in value, are projected to compound at 4.75% annually through 2030 as manufacturers, utilities, and municipalities automate asset monitoring. Operators exploit 5G slicing and LPWAN roll-outs to deepen enterprise relationships. Fixed data gains momentum as FTTH coverage expands, offering symmetrical gigabit speeds that enable remote work and cloud back-ups.

A value shift toward data prompts operators to repurpose copper loops for fiber, phase out time-division multiplexing switches, and bundle OTT TV to lift ARPU. Government digitization grants worth EUR 231 million (USD 263.14 million) catalyze e-government workloads, stimulating demand for secure data links. IoT pilots in water utilities demonstrate LoRaWAN cost-efficiency, hinting at broader smart-meter roll-outs. These dynamics lay the groundwork for sustained data-service dominance within the Bulgaria telecom MNO market.

By End User: Enterprise Segment Accelerates Despite Consumer Dominance

Consumers still account for 68.26% of 2024 revenue, yet enterprise spend is growing faster at a 3.82% CAGR. Multinational near-shoring into Sofia, Plovdiv, and Varna demands low-latency links, private VPNs, and secure 5G campus networks, collectively reshaping the Bulgaria telecom MNO market. Enterprise contracts typically bundle fixed Ethernet, mobile data, security, and cloud connectivity, driving higher per-account value than consumer bundles. EU funds for SME digitization and the USD 640 million Economic Transformation Program add extra pull.

Still, demographic decline and out-migration curb long-run retail subscriber growth in rural zones, motivating carriers to deepen enterprise focus. New service teams pitch Industry 4.0 solutions that integrate sensors, analytics, and edge computing. Early adopters include automotive component makers in Plovdiv’s Trakia Economic Zone and logistics hubs near Sofia Airport. As private 5G matures, the Bulgaria telecom MNO market share held by enterprise lines is expected to inch upward each year, offsetting consumer stagnation.

Geography Analysis

Regional imbalance shapes growth prospects inside the Bulgaria telecom MNO market. Sofia, Plovdiv, and Varna drive high-value demand, supported by 10,000 ICT companies that generated EUR 2.5 billion (USD 2.6 billion) in revenue in 2024. These hubs absorb most new data center capacity, cloud on-ramps, and 5G small-cell densification. Vivacom’s 92% population coverage still concentrates on urban clusters and key transport corridors, reinforcing the city-first roll-out bias.

Rural districts trail urban areas by 13% points on high-speed broadband availability, hampering e-commerce and e-health penetration. EU grants bridge cost gaps, yet population decline reduces absolute subscriber counts outside cities. Cross-border corridors with Romania, Serbia, and Turkey gain importance because freight and passenger traffic require seamless roaming. The Communications Regulation Commission targets involuntary roaming fees through new mobile-app alerts, strengthening consumer trust.

The OECD notes that Sofia’s GDP per capita doubles in some rural regions, revealing a stark digital divide. Operators, therefore, weigh fiber trenching costs against limited payback in sparsely populated areas and instead trial fixed wireless access using 5G mid-band spectrum. Along the Black Sea coast, cities like Burgas and Varna, seasonal tourism inflates mobile traffic in summer months, prompting temporary small-cell deployments. As EU-backed corridors fill gaps, the Bulgaria telecom MNO market moves closer to universal service targets.

Competitive Landscape

The Bulgaria telecom MNO market centers on three mobile network operators that are A1 Bulgaria, Vivacom, and Yettel, each defending distinct strengths. Vivacom leads 5G population coverage and posted USD 647 million revenue with USD 119 million profit in 2023. Yettel claims the highest mobile revenue at EUR 536 million and serves 3.2 million active users, supported by parent e&’s investment capacity. A1 tops network performance metrics, delivering 168.1 Mbps downloads and 26 ms latency, a differentiator for enterprise SLAs.

United Group’s Southeast Europe fiber integration raises wholesale competition, while EXA Infrastructure’s acquisition of GCN opens fresh backhaul routes. A1’s roaming test with Vodafone Germany proved 5G standalone interoperability, an early sign that Bulgarian subscribers will access advanced roaming features abroad. Regulatory FDI screening over EUR 2 million introduces an approval layer for foreign capital, adding deal complexity but not halting investment momentum.

Challenger ISPs leverage mandatory open-access fiber rules to lease dark fiber and resell gigabit broadband, intensifying price rivalry. Meanwhile, municipal Wi-Fi projects erode low-tier consumer ARPU but stimulate device usage that indirectly boosts mobile data volumes. As convergence deepens, the competitive playbook shifts toward customer experience, streaming bundles, and enterprise vertical solutions rather than headline price cuts.

Bulgaria Telecom MNO Industry Leaders

A1 Bulgaria

Vivacom

Yettel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Vodafone Group and A1 Group completed a 5G standalone roaming call between Vodafone Germany and A1 Bulgaria, validating next-generation roaming voice features.

- December 2024: e& acquired a majority stake in Yettel and CETIN, injecting fresh capital into 5G expansion.

- September 2024: EXA Infrastructure purchased GCN to bolster fiber capacity across Southeast Europe.

- June 2024: United Group unveiled the largest regional fiber backbone, extending gigabit reach in Bulgaria.

- June 2024: A1 Bulgaria launched VoLTE services, boosting call quality and network efficiency.

Bulgaria Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Bulgaria telecom MNO market?

The Bulgaria telecom MNO market size is USD 2.27 billion in 2025 and is forecast to reach USD 2.72 billion by 2030.

Which service type holds the largest share?

Data and Internet services led with 44.28% revenue share in 2024, reflecting the shift toward mobile and fixed broadband consumption.

How fast is the enterprise segment growing?

Enterprise telecom spend is projected to expand at a 3.82% CAGR between 2025 and 2030, outpacing consumer growth.

What is the main restraint to revenue growth?

Intense price competition keeps ARPU low, trimming margins and limiting funding for rapid network upgrades.

How extensive is 5G coverage in Bulgaria?

Vivacom reports 5G population coverage of 92%, while A1 and Yettel continue to densify networks across major cities and industrial zones.

How is EU funding influencing rural connectivity?

EUR 270 million from the Recovery and Resilience Facility subsidizes 5G corridors and FTTH in underserved rural areas, reducing operator investment risk.

Page last updated on: