Albania Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

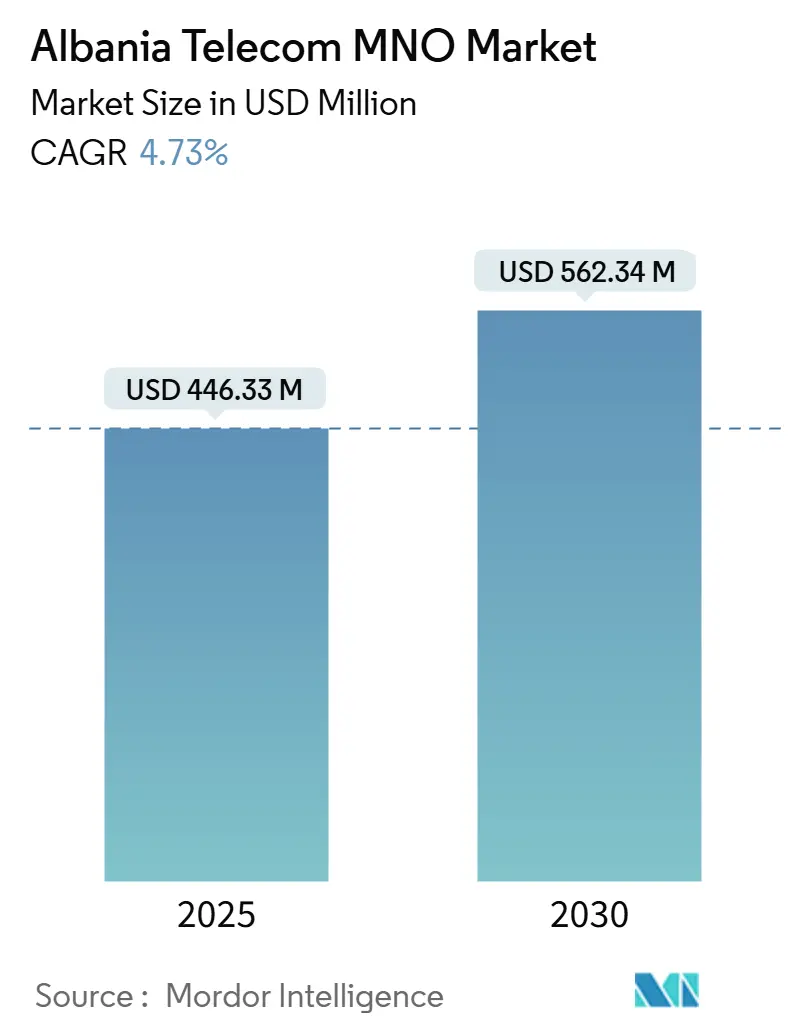

| Market Size (2025) | USD 446.33 Million |

| Market Size (2030) | USD 562.34 Million |

| Growth Rate (2025 - 2030) | 4.73% CAGR |

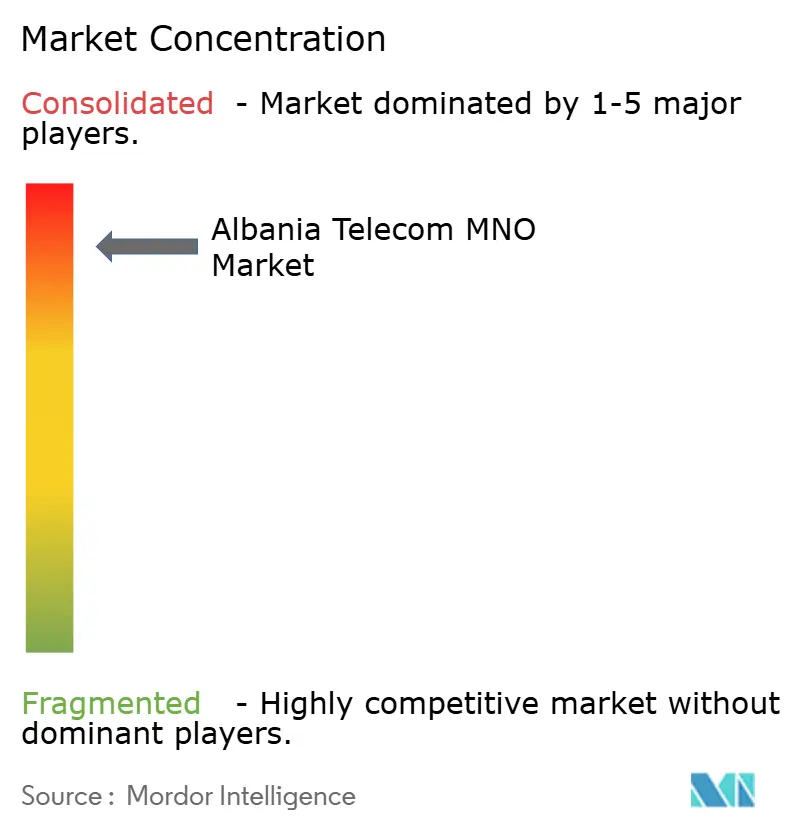

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Albania Telecom MNO Market Analysis by Mordor Intelligence

The Albania Telecom MNO Market size is estimated at USD 446.33 million in 2025, and is expected to reach USD 562.34 million by 2030, at a CAGR of 4.73% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 3.40 million subscribers in 2025 to 4.10 million subscribers by 2030, at a CAGR of 3.71% during the forecast period (2025-2030).

Robust tourism inflows, with more than 10 million international arrivals in 2023, are amplifying mobile data usage and roaming revenues, while enterprise digital-transformation programs are raising demand for high-capacity connectivity. Operators are capitalizing on EU-funded broadband programs, 5G spectrum auctions and an 80% internet-penetration foundation to shift revenue mixes toward data and IoT services. Market consolidation, led by 4iG Group’s creation of ONE Albania, has produced a duopoly that accelerates infrastructure convergence yet intensifies price-based competition. Regulatory alignment with EU standards, together with projects such as the planned Albania-Egypt subsea cable, positions the country as a digital gateway linking Europe with Africa and Asia.

Key Report Takeaways

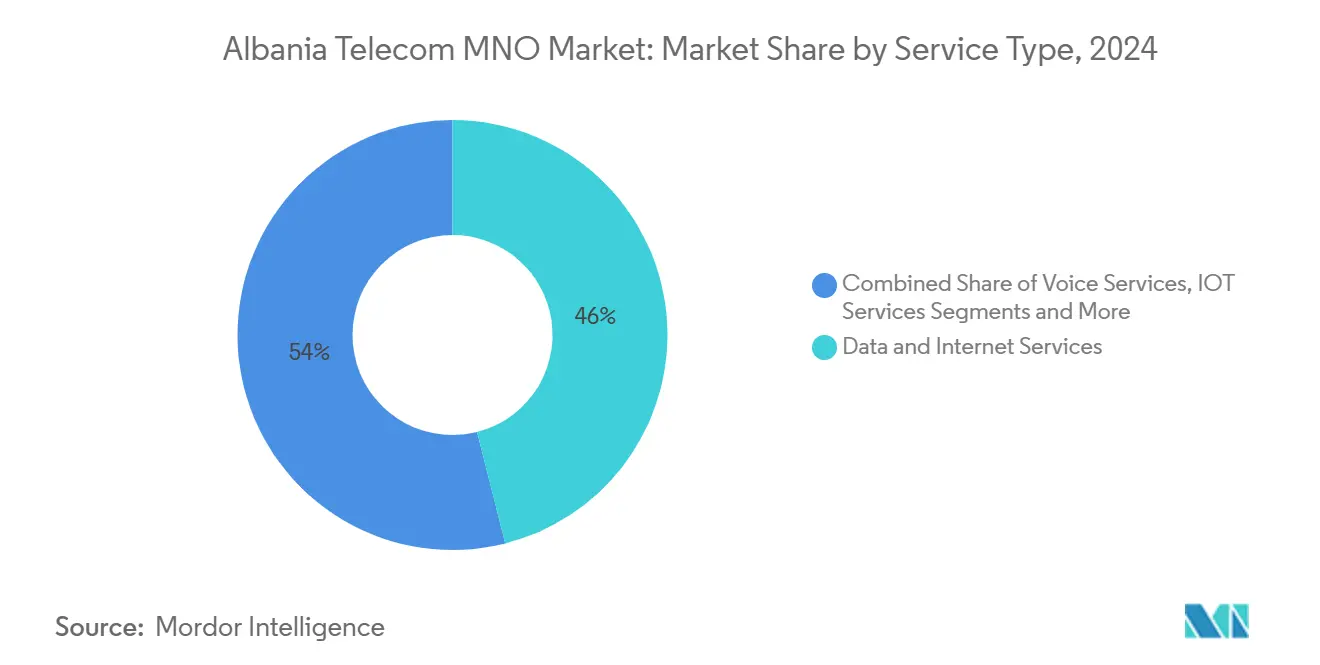

- By service type, data services led with 46.04% of Albania telecom market share in 2024; IoT services are forecast to post the fastest 5.08% CAGR through 2030.

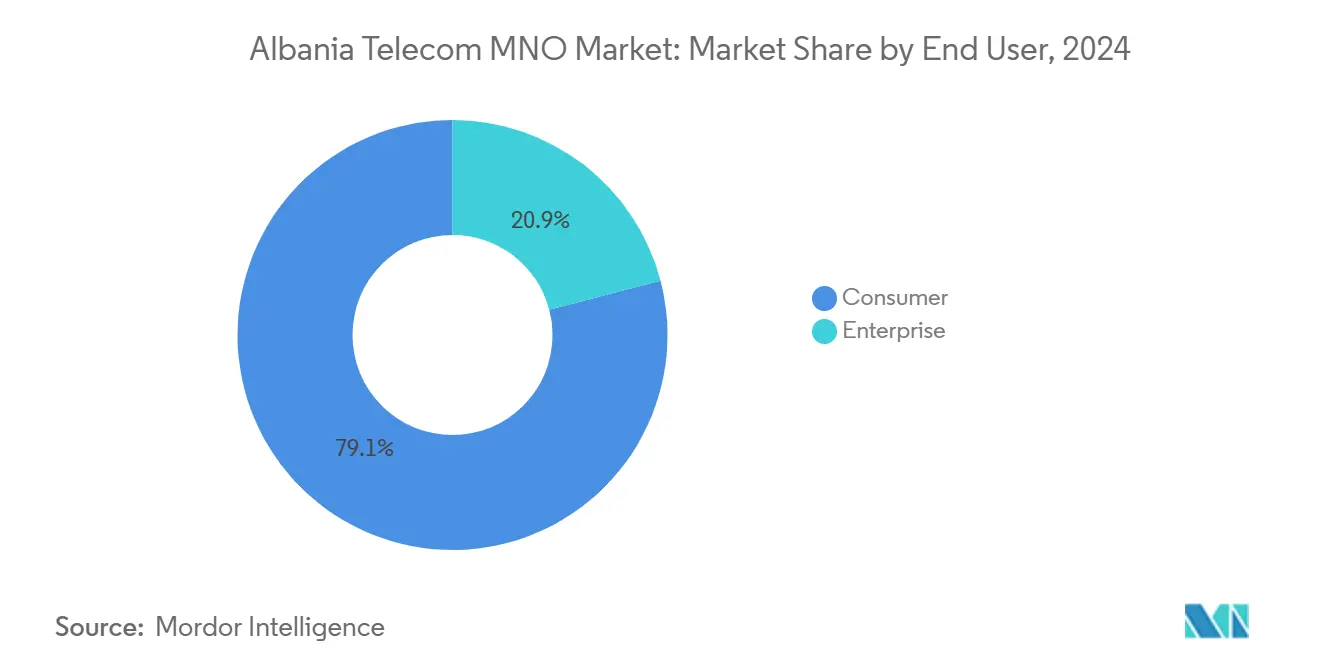

- By end user, the consumer segment accounted for 79.06% share of the Albania telecom market size in 2024, whereas the enterprise segment is projected to expand at a 5.91% CAGR between 2025-2030.

Albania Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging mobile data consumption from video-centric apps | +1.2% | Tirana and coastal tourism hubs | Short term (≤ 2 years) |

| 5G spectrum auctions accelerating network investment | +0.8% | Major cities and transport corridors | Medium term (2-4 years) |

| Enterprise IoT connectivity demand across energy & logistics | +0.6% | National industrial corridors | Long term (≥ 4 years) |

| EU-funded national broadband plan (Digital Agenda 2030) | +0.9% | Rural and underserved municipalities | Long term (≥ 4 years) |

| Tourism boom lifting prepaid SIM & roaming revenues | +0.7% | Coastal resorts and heritage sites | Short term (≤ 2 years) |

| LEO-satellite backhaul lowering rural coverage costs | +0.4% | Mountainous northern and southeastern regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Mobile Data Consumption from Video-Centric Apps

Seasonal tourist traffic is creating concentrated peaks that raised average daily mobile-data throughput by more than 35% during the 2024 summer season.[1]Albanian Daily News, “Albania Reinforces Internet Infrastructure With Starlink Service,” albaniandailynews.com Operators must over-provision coastal cells, which inflates capex yet enables dynamic pricing for roaming packages. Video streaming accounts for more than 70% of the incremental traffic, straining 4G networks and hastening 5G roll-outs. Although Albania’s internet-penetration rate exceeds 80%, the usage gap between urban and rural zones persists, compelling carriers to balance quality-of-experience with profitability targets.

5G Spectrum Auctions Accelerating Network Investment

AKEP’s phased auction plan awarded mid-band spectrum blocks in late 2024 with coverage obligations that include 95% population reach by 2028. ONE Albania committed EUR 92 million (USD 100 million) to meet its licence terms, while Vodafone Albania earmarked EUR 85 million for radio-access upgrades.[2]Vodafone Group, “FY 2024 Results Presentation,” vodafone.com The capex burden is pressuring ARPU, but first-mover operators are positioned to monetize low-latency services for enterprise and tourism segments once retail 5G pricing stabilizes.

Enterprise IoT Connectivity Demand Across Energy & Logistics

Albania’s electricity-distribution operator OSHEE launched a smart-grid pilot that upgraded backbone links from 20 Mbit/s to 10 Gbit/s using Huawei-supplied transport equipment. Parallel projects in seaport logistics and refrigerated truck fleets are driving demand for narrow-band and LTE-M connectivity, shifting operators toward managed-service contracts that bundle data, analytics and device management. Approximately 53,000 smart meters are scheduled for installation by 2026, signalling a multi-year revenue stream for IoT-platform subscriptions.

EU-Funded National Broadband Plan (Digital Agenda 2030)

The European Commission’s EUR 9 billion Western Balkans Investment Plan earmarks grants and concessional loans that offset as much as 40% of rural fiber build costs. ONE Albania’s 5,400-kilometer fiber backbone now spans 55 of 61 municipalities, and the operator targets gigabit service availability for 75% of households by 2027. Public-private co-investment mitigates the economics of low-density deployment, enabling Albania to leapfrog copper-based upgrades and move directly to fiber-to-the-home.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fierce price competition compressing ARPU | -0.9% | Urban prepaid and enterprise markets | Short term (≤ 2 years) |

| Legacy copper limiting fixed-line speeds in rural areas | -0.5% | Mountain villages and border regions | Medium term (2-4 years) |

| Net emigration shrinking long-term subscriber base | -0.3% | Rural counties | Long term (≥ 4 years) |

| Euro-denominated capex exposes operators to FX risk | -0.4% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fierce Price Competition Compressing ARPU

The post-merger duopoly competes aggressively on bundled tariffs: unlimited voice-and-data packs fell 11% year over year in 2024. Seasonal prepaid promotions aimed at tourists set discount benchmarks that ripple through enterprise negotiations. Lower ARPU impedes self-funded network upgrades, pushing carriers toward wholesale fiber partnerships and non-core service diversification.

Legacy Copper Limiting Fixed-Line Speeds in Rural Areas

Historical underinvestment left 28% of households reliant on sub-10 Mbit/s DSL lines as of 2024.[3]One Albania, “One Ultra Fiber,” one.al Fiber trenching in mountainous terrain costs up to EUR 16,000 per kilometer, deterring private-only roll-outs. Capacity constraints restrict cloud adoption among rural SMEs and hold back e-government service uptake, reinforcing a digital divide that curtails revenue expansion potential outside urban centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Market Evolution

Data services held a 46.04% Albania telecom market share in 2024 and are forecast to record a 4.76% CAGR to 2030 as consumer streaming and enterprise VPN demand intensify. Voice services, despite a 36.96% share, will decline toward 4.63% CAGR as OTT alternatives proliferate. IoT captured only 5.02% in 2024 yet leads growth with a 5.08% rate, supported by smart-grid roll-outs and freight-tracking solutions. OTT and Pay-TV offerings commanded 7.81%, reflecting rising household fiber penetration and EU-content licensing alignment. Other services, including messaging, account for 4.17% and remain largely flat. Cross-selling converged fixed-mobile bundles is improving contract ARPU and helps operators counter price erosion in stand-alone data plans.

Operators are packaging cybersecurity, unified-communications and cloud access with primary connectivity to raise switching costs. The first Albanian Open-Banking transaction in 2025 is catalyzing financial-services digitalization that will amplify data-center hosting and MPLS traffic. This momentum underpins long-term upside for the data segment and accelerates migration toward fiber-backed gigabit offers.

By End User: Enterprise Segment Outpaces Consumer Growth

Consumers contributed 79.06% of 2024 revenue but are projected to grow at 4.40% CAGR, driven by tourism-fuelled prepaid SIM uptake and higher video-streaming intensity. The enterprise cohort represented 20.94% yet is on track to grow 5.91% as firms adopt IoT and secure SD-WAN solutions. Manufacturing, logistics and energy-utilities verticals are leading contract volumes, while fintech and shared-services centers emerging in Tirana require SLA-grade international backhaul. The Albania telecom market size attributable to corporate clients could exceed USD 140 million by 2030 (23% of total) if ICT outsourcing inflows continue.

Bundled cloud, security and managed IoT offerings are broadening margins. Regulatory incentives for rural fiber coverage are unlocking EU co-financing that lowers enterprise access costs outside Tirana. Meanwhile, tourism-driven consumer demand remains a buffer against macroeconomic volatility, but ARPU stagnation presses operators to prioritize enterprise solution selling.

Geography Analysis

Tirana’s metropolitan zone generated around 45% of the Albania telecom market in 2024, supported by office clusters and university campuses seeking gigabit links. Coastal districts such as Vlora and Shkodër added nearly 15% on the back of record tourist arrivals. Rural counties collectively contributed 25% yet delivered only 12% of mobile-data traffic because of lower 4G capacity and lingering copper loops. ONE Albania’s fiber build now passes 1.2 million premises, and its rural expansion plan aims for 75% household coverage by 2027, funded partly by EU Structural Instruments.

The Albania-Egypt express subsea-cable joint venture will reduce latency to Asian landing stations and is expected to anchor Tier-3 data-center developments near Durrës, elevating Albania’s role as a transit hub. LEO-satellite service launched in 2024 fills interim coverage gaps across mountain resorts, supporting digital‐nomad visas and remote-work inflows. Government capital spending averaging 6.1% of GDP through 2027 earmarks funds for broadband backbones complementing private roll-outs. Combined, these geography-specific initiatives will expand the Albania telecom market footprint beyond its traditional urban strongholds.

Competitive Landscape

Market concentration tightened after 4iG Group merged ONE Telecommunications with ALBtelecom to form ONE Albania, which controlled 41% of mobile connections in 2024. Vodafone Albania, backed by its AbCom fiber assets covering 460,000 homes, holds roughly 39% share and leverages converged bundles to mitigate churn. AKEP enforces wholesale-access obligations that permit MVNO entrants, though no challenger currently exceeds 2% share. Competitive focus has shifted to quality-of-experience, with both majors trialing 5G fixed-wireless access ahead of commercial launch in 2025.

Strategic moves include ONE Albania’s EUR 100 million multi-year RAN modernization contract and Vodafone Albania’s rollout of edge-computing nodes to support low-latency enterprise applications. Satellite-broadband vendor Starlink entered Albania in 2024, supplying routers at USD 425 and monthly plans at USD 65, creating a niche threat in sparsely populated areas. Overall, the duopoly structure encourages network-sharing talks to curb overlapping capex while preserving service differentiation via content partnerships and enterprise-solution depth.

Albania Telecom MNO Industry Leaders

Vodafone Albania

One Albania

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Albania processed its first Open-Banking transaction via EasyPay and Intesa Sanpaolo Bank Albania, paving the way for API-driven financial-service innovations.

- January 2025: The government released its Economic Reform Programme 2025-2027, allocating 6.1% of GDP annually to capital outlays that include telecom transport links

- July 2024: The European 5G Observatory cited Albania’s alignment with regional 5G-deployment timelines.

Albania Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How fast is enterprise demand growing?

The enterprise segment is forecast to outpace consumers at a 5.91% CAGR, supported by IoT, SD-WAN and cloud-access contracts.

What challenges curb revenue growth?

Price-led ARPU compression, legacy copper in rural areas, subscriber losses from emigration and foreign-exchange exposure on Euro-denominated capex act as key restraints.

How significant is tourism to sector revenue?

More than 10 million visitors in 2023 boosted prepaid and roaming sales, contributing to seasonal traffic peaks that account for up to 20% of annual mobile-data volume.

Who are the main operators?

ONE Albania, holding over 41% mobile share, and Vodafone Albania, with a converged fixed–mobile network, dominate the market.

Page last updated on: