Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Intent Based Networking Market is Segmented by Component (Hardware, Software, and Services), by Deployment (Cloud, On-Premises), by End-User Industry (IT and Telecom, BFSI, Government and Public Sector, and More), End-User Enterprise Size (Large Enterprises, and More), Network Domain (Campus / Enterprise LAN, Data Center, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

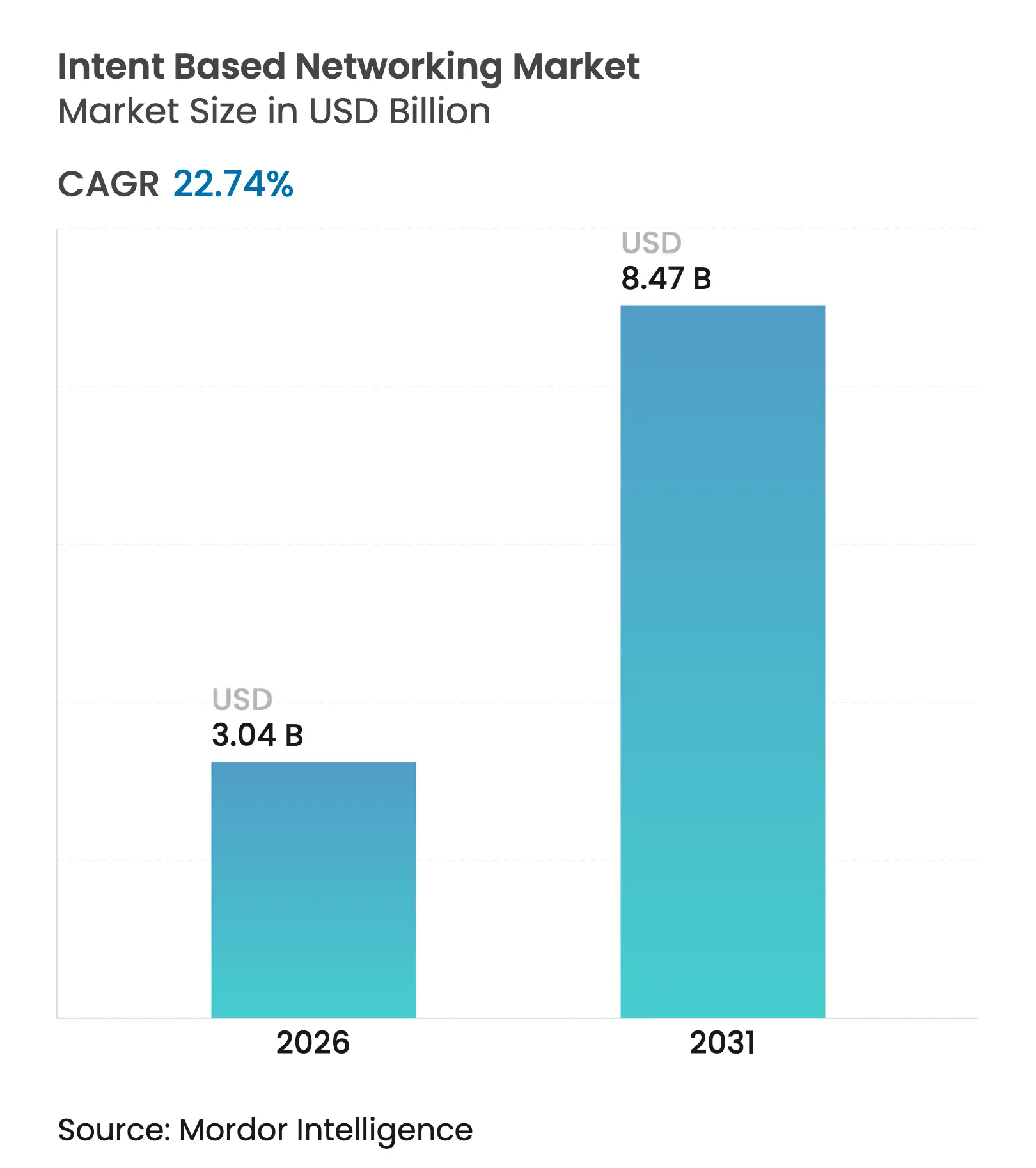

| Market Size (2026) | USD 3.04 Billion |

| Market Size (2031) | USD 8.47 Billion |

| Growth Rate (2026 - 2031) | 22.74 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The intent based networking market size was valued at USD 2.48 billion in 2025 and estimated to grow from USD 3.04 billion in 2026 to reach USD 8.47 billion by 2031, at a CAGR of 22.74% during the forecast period (2026-2031). Enterprises increasingly view the network as a revenue-critical platform instead of a cost center, and 72% of IT leaders intend to deploy unified platform architectures across multiple network domains within the next two years. Early rollouts highlight how predictive automation, AI-driven security, and policy abstraction remove configuration bottlenecks while cutting downtime. Vendors accelerate innovation by embedding artificial intelligence into switching silicon and orchestration software, allowing operators to translate high-level business intent into low-level configurations. At the same time, the rise of cloud-native architectures, edge computing, and distributed AI workloads opens new revenue opportunities for service providers that package intent-based capabilities as managed services.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing demand for network automation

Growing demand for network automation

| +4.2% | Global | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+4.2%

|

Geographic Relevance

:

Global

|

Impact Timeline

:

Medium term (2-4 years)

|

Rising network complexity and data traffic

Rising network complexity and data traffic

| +5.8% | North America and Asia-Pacific | Short term (≤ 2 years) | |||

Shift to cloud-first and multicloud strategies

Shift to cloud-first and multicloud strategies

| +3.9% | North America and Europe | Medium term (2-4 years) | |||

GenAI-driven predictive intent policies

GenAI-driven predictive intent policies

| +2.7% | North America and Europe, Asia-Pacific follow-on | Long term (≥ 4 years) | |||

Telco network-as-code monetization push

Telco network-as-code monetization push

| +3.1% | Asia-Pacific and Global Tier-1 operators | Medium term (2-4 years) | |||

ESG-focused “green-traffic” routing

ESG-focused “green-traffic” routing

| +1.8% | Europe leads | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Demand for Network Automation

Hybrid infrastructures now span data centers, multiple public clouds, and a widening edge footprint. Six in ten IT leaders already plan to adopt AI-enabled predictive automation that proactively adjusts policies before service degradation occurs. DENSO’s global factory network shows the payoff, using Cisco DNA Center to orchestrate remote updates and shrink routine maintenance tasks from hours to minutes. As more industrial IoT endpoints stream real-time data, operations teams depend on machine reasoning engines that correlate telemetry, automate compliance, and guarantee SLA adherence without manual CLI work. The result is a decisive shift from reactive workflows to policy-driven uptime, a priority that underpins long-run growth in the intent based networking market.

Rising Network Complexity and Data Traffic

Generative AI training and inference routinely spike east-west traffic and demand lossless transport. Meta upgraded its backbone from 10 GbE links in 2010 to 400 GbE leaf-spine fabrics in 2024 to sustain model throughput. Similar architectural overhauls cascade into the enterprise segment, where single-hop fabrics, ultra-deep buffers, and flow-aware load balancing are now table-stakes. Predictive path-finding engines inside intent platforms select optimal routes in real time, preventing congestion before users notice latency. These capabilities deliver measurable efficiency gains, supporting the continued 23.25% CAGR projected for the intent based networking market.

Shift to Cloud-First and Multicloud Strategies

By 2030, three in four enterprises across the European Union will host workloads on at least two public clouds [1]European Parliament, “Digital Decade Policy Programme 2030,” europarl.europa.eu. With data sovereignty and cost control top of mind, network leaders demand end-to-end policy consistency across on-premises, colocation, and cloud enclaves. Intent frameworks meet this need by abstracting heterogenous infrastructure and letting administrators enforce a single security posture regardless of where the application lives. T-Mobile’s managed SASE service built with Palo Alto Networks demonstrates how telecom carriers monetize this requirement, pairing 5G Advanced connectivity with policy-based routing to deliver zero-trust access for mobile workforces.

GenAI-Driven Predictive Intent Policies

Large language models interpret natural-language goals—“Prioritize radiology PACS over guest Wi-Fi”—and then synthesize thousands of device-level commands. IBM and Juniper validated this concept by linking Mist AI telemetry to IBM watsonx, slashing wireless help-desk tickets across 44 campuses and 13,000 guest passes [2]IBM Corporation, “IBM and Juniper Expand Partnership with Generative AI,” ibm.com. Over time, intent engines will ingest business KPIs, recommend policy tweaks, and automatically verify results, unlocking self-optimizing networks that anticipate shifts in demand. Continuous learning loops strengthen vendor lock-in, further expanding the long-run revenue potential of the intent based networking market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High upfront investment and integration cost

High upfront investment and integration cost

| -2.8% | Emerging markets hardest hit | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-2.8%

|

Geographic Relevance

:

Emerging markets hardest hit

|

Impact Timeline

:

Short term (≤ 2 years)

|

Skill-set shortage in NetOps and SecOps

Skill-set shortage in NetOps and SecOps

| -3.4% | Asia-Pacific and Europe | Medium term (2-4 years) | |||

Vendor lock-in in closed IBN fabrics

Vendor lock-in in closed IBN fabrics

| -1.9% | Global | Medium term (2-4 years) | |||

Regulatory uncertainty over AI policy engines

Regulatory uncertainty over AI policy engines

| -1.2% | Europe and Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Upfront Investment and Integration Cost

Fully realized deployments blend high-performance switching, subscription software, and professional services. IDC’s assessment of intent-based verification platforms records USD 14.2 million in annual benefits, yet CFOs remain wary of capex peaks that arrive before productivity gains materialize. SMEs are particularly price-sensitive, even as cloud-delivered Network-as-a-Service options convert capital spend to pay-as-you-go opex. Maturity in consumption pricing models is therefore a gating factor for broader penetration of the intent based networking market.

Skill-Set Shortage in NetOps and SecOps

Only 42% of global organizations currently say their network operations teams meet business expectations. In Europe, just 8% of enterprises consider themselves AI-ready, compared with 15% worldwide. The gap forces buyers to lean on vendor-managed services, driving up lifetime costs and slowing customization. Until universities and professional programs produce more NetDevOps talent, the intent based networking industry will depend heavily on automation to mask human shortfalls.

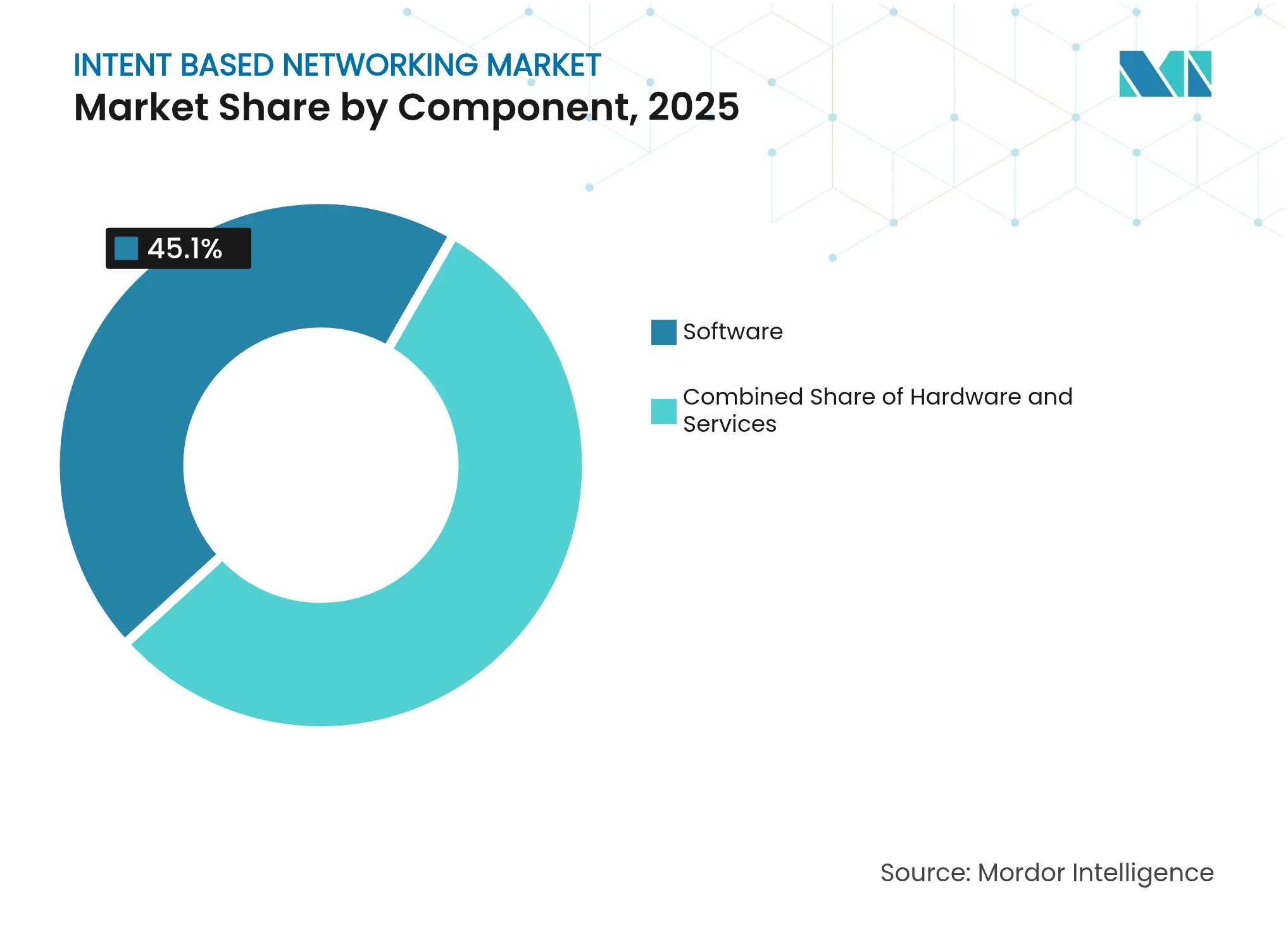

By Component: Software Leadership Drives Service Innovation

Software platforms delivered 45.10% of 2025 revenue, underscoring their role as the decision-making core of the intent based networking market. They provide single-pane visibility, intent capture, and closed-loop assurance covering campus, data center, WAN, and cloud domains. Hardware supplies the packet-pushing horsepower—especially as 400 GbE ports become mainstream—but the value migrates to the algorithms that interpret telemetry in real time. Services meanwhile expand fastest at 22.18% CAGR, a pattern that highlights growing demand for outcome-based engagements where providers assume operational accountability.

Professional service catalogs now include design blueprints, brownfield migrations, and AI-assisted runbooks. TCS, for example, spent USD 29.1 billion in the past fiscal year to bolster its cloud and networking practice, allowing customers to outsource day-two lifecycle management while preserving policy control. As more workloads execute at the edge, enterprises will favor consumption models bundling software licenses, support, and remote operations into a predictable monthly fee, widening both the revenue pool and the stickiness of the intent based networking market.

Note: Segment shares of all individual segments available upon report purchase

By Deployment: Cloud-Native Architecture Accelerates Adoption

Cloud deployments captured 57.65% of total spend in 2025 and are slated for a 24.95% CAGR, the fastest of any delivery model. This ascent mirrors the way CIOs swap capex peaks for opex curves, take advantage of global availability zones, and gain immediate access to the latest AI features. Cisco’s Nexus HyperFabric AI cluster illustrates the trend, combining silicon, optics, and SaaS management in one subscription so operators focus on policy outcomes rather than box-level upgrades. On-premises remains relevant for data-sovereignty-sensitive industries such as public sector and financial services, but hybrid control planes increasingly knit both worlds together into a unified operational fabric.

Put differently, the intent based networking market size for cloud-hosted control planes is poised to eclipse on-premises rivals as network leaders chase continuous innovation. The deeper these platforms integrate with hyperscaler APIs, the harder it becomes for competitors to dislodge incumbents, reinforcing a virtuous cycle that fuels above-market growth.

By End-User Industry: IT and Telecom Lead Healthcare Surge

IT and telecom operators commanded 31.05% of 2025 revenue by leveraging autonomous provisioning across backbone, metro, and access layers. 5G slicing, low-latency URLLC services, and network-as-code monetization each require fine-grained policy control that intent frameworks furnish out of the box. Manufacturing follows, as DENSO and other industrial majors retrofit plants with smart sensors whose traffic must be segmented and prioritized in real time.

Healthcare, however, is pacing fastest at a 23.10% CAGR, driven by digital front doors, telemetry-rich diagnostics, and tele-ICU. Rady Children’s Hospital demonstrated a seamless cut-over to 900 AI-enabled access points without disrupting patient care, confirming that always-on connectivity equates to clinical safety. As regulatory mandates tighten and patient volumes rise, the intent based networking market will find steady demand across hospitals, life-science campuses, and telehealth providers who cannot afford service-affecting mis-configurations.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

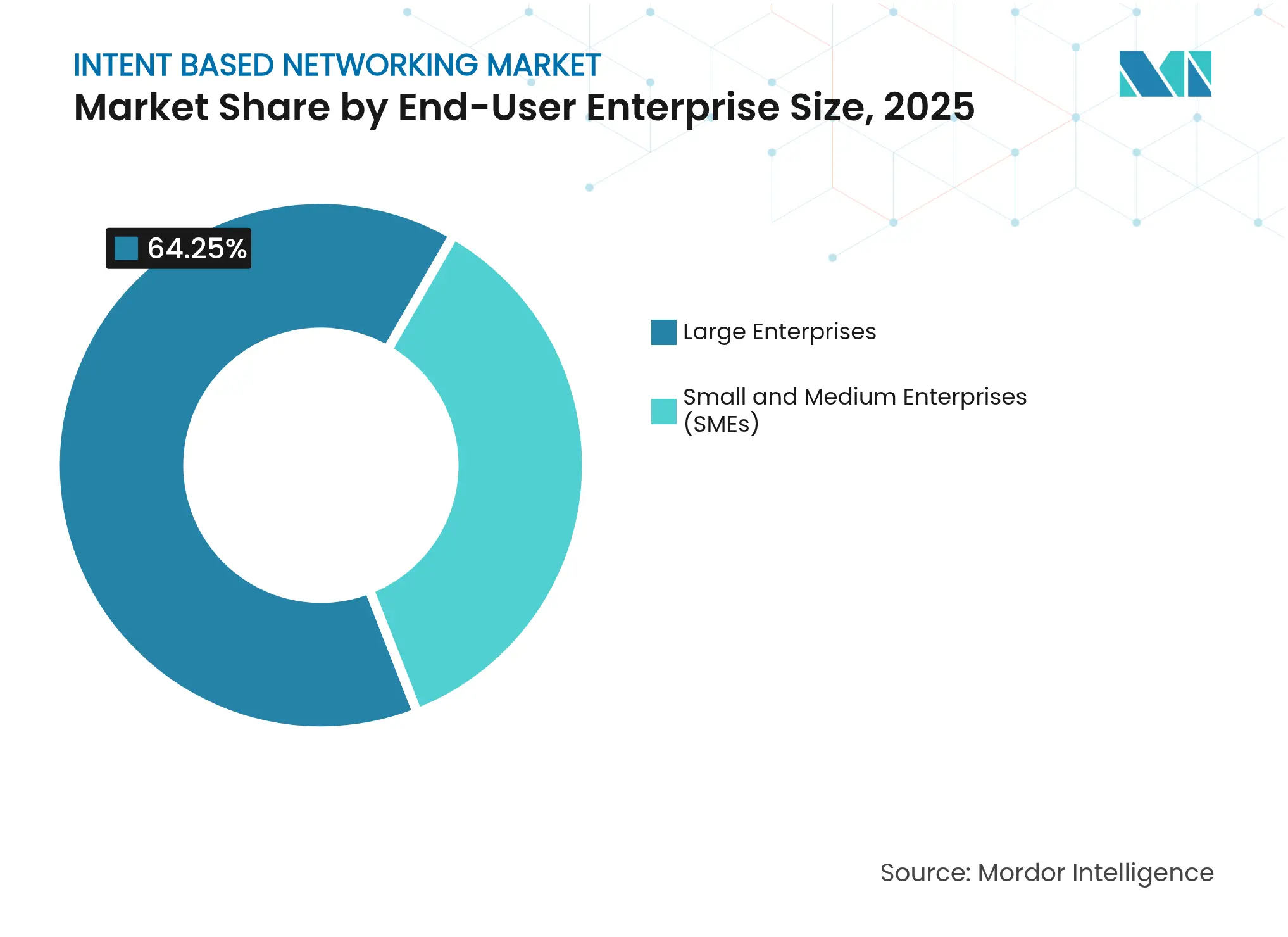

By End-User Enterprise Size: SME Growth Democratizes Advanced Networking

Large enterprises generated 64.25% of 2025 sales, bolstered by deep IT benches and multiyear framework agreements with strategic suppliers. Their rollouts span campus, data center, and multicloud, requiring policy federation that only high-end intent engines currently deliver. Budget commit is rarely the barrier; change-management complexity is. Yet vendors have streamlined migrations with digital twins and staged enforcement modes, lowering risk and shortening payback periods.

SMEs, meanwhile, expand at a 25.90% CAGR, the clearest sign of democratization in the intent based networking industry. Consumption-based bundles wrap switching hardware, SaaS control planes, and 24×7 operations into per-port fees palatable to firms lacking full-time NetOps staff. As edge use cases—from smart retail to micro-factories—proliferate, these smaller buyers will accelerate overall market penetration by opting straight for autonomous cloud paths rather than building legacy networks first.

Note: Segment shares of all individual segments available upon report purchase

By Network Domain : Data Center Dominance with WAN Surge

Data center networks contributed 41.10% of the intent based networking market share in 2025, reflecting their role as the control hub for AI training clusters, high-performance analytics, and mission-critical applications. Continuous verification loops inside these platforms reduce troubleshooting time and prevent mis-configurations that previously led to costly outages. As enterprises modernize to 400 GbE and 800 GbE fabrics, policy abstraction becomes even more valuable, pushing the intent based networking market size for this segment steadily higher over the forecast horizon.

WAN and SD-WAN implementations, while smaller today, are forecast to post a rapid 26.20% CAGR through 2031 as hybrid workforces, edge analytics, and cloud bursting expand traffic well beyond the traditional branch perimeter. Intent-driven WAN controllers continuously assess link health, cost, and security posture, then reroute flows in real time to uphold SLA commitments without manual intervention. Remote work accelerates this migration because home-office traffic now competes with corporate data center loads, forcing IT teams to automate path selection and zero-trust policies across MPLS, broadband, and 5G links.

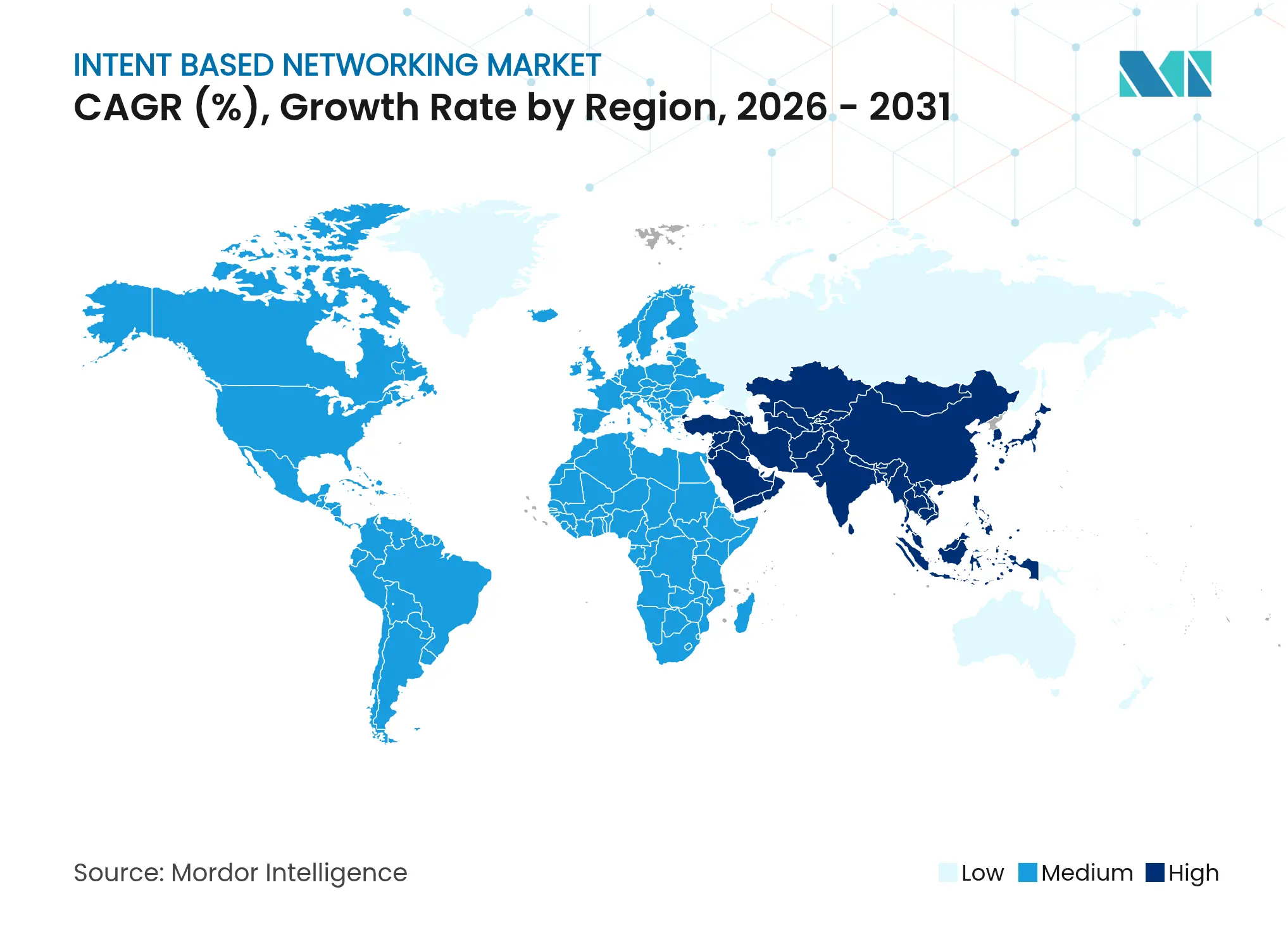

North America retained leadership with 38.20% of 2025 revenue, buoyed by aggressive AI infrastructure investments from hyperscalers and Fortune 500 enterprises. Financial institutions upgrade low-latency trading backbones, while cloud providers pioneer 800 GbE links that later cascade into enterprise portfolios. Regulatory clarity around cloud security frameworks further reduces deployment friction. As a result, the intent based networking market size in the region is projected to climb steadily even as penetration nears maturity.

Asia-Pacific logs the most vigorous trajectory at 21.65% CAGR through 2031 thanks to large-scale digital initiatives funded by sovereign programs. Indonesia’s Vision 2045 roadmap, Singapore’s Digital Enterprise Blueprint, and Vietnam’s 5G-led smart-city mandate each earmark budget for intelligent transport and e-government services that depend on autonomous networks. Domestic telecom operators also look to monetize network programmability by exposing APIs to software developers, a model that should lift regional share of the intent based networking market.

Europe shows solid momentum under the EUR 1 trillion Digital Europe Programme that funds supercomputing, cybersecurity, and AI skills . Although only 8% of firms today feel AI-ready, Brussels enforces sustainability reporting and energy-efficient IT targets that intent engines can satisfy via dynamic traffic shaping. Consequently, the region represents an attractive mid-term opportunity where ESG compliance dovetails with network modernization.

Market Concentration

Incumbent switch makers are reinventing themselves as AI-native platform providers. Cisco seeded a USD 1 billion fund and became the exclusive silicon partner for NVIDIA’s Spectrum-X enterprise Ethernet suite, blending Silicon One ASICs with cloud-grade telemetry to tame AI east-west spikes. HPE’s USD 14 billion bid for Juniper would fold Mist AI into Aruba CX fabrics, giving the combined entity end-to-end control from compute through network. If regulators approve, the merged portfolio could double HPE’s networking revenue and put pressure on pure-play rivals.

Arista counters with its EOS Smart AI Suite that unifies cluster load balancing and job-centric observability, cementing its beachhead inside mega-scale data centers. At the emerging tier, Selector secured USD 33 million in Series B funding to refine AIOps correlation algorithms, while Ciroos.AI amassed USD 21 million for agentic troubleshooting bots. The moderate concentration seen today reflects high switching-silicon barriers yet leaves room for cloud startups to differentiate on software velocity. Together these dynamics ensure vibrant competition and ongoing product innovation within the intent based networking market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Market Definitions and Key Coverage

Our study defines the intent-based networking (IBN) market as all software, embedded intelligence, and related services that translate high-level business intent into automated network policies, verify compliance in real time, and self-remediate across campus, data-center, WAN, and cloud domains.

Scope Exclusion: Traditional script-driven network automation tools that lack closed-loop verification and AI/ML policy translation are excluded.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with network architects at hyperscalers, CIOs in banking and healthcare, Tier-1 telecom planners, and specialized channel partners across North America, Europe, and Asia-Pacific. These interviews test adoption thresholds, license fee corridors, and deployment pain points, filling data gaps that published statistics rarely cover.

Desk Research

We begin with public datasets that anchor demand fundamentals: global IP traffic levels from the International Telecommunication Union, enterprise cloud migration statistics from the U.S. Census's ICT surveys, and device penetration tallies issued by GSMA. Trade association white papers such as MEF's lifecycle-service-orchestration briefs and IEEE journals on autonomous networking provide technical context, while patent analytics from Questel highlight innovation velocity in intent engines.

Company 10-Ks, vendor road maps accessed via Dow Jones Factiva, and customs shipment records compiled in Volza give granular clues on hardware attach rates, which are then blended with pricing insights extracted from D&B Hoovers profiles. The sources cited above are illustrative; many additional open datasets and paid repositories informed desk validation.

Market-Sizing & Forecasting

A top-down model starts with enterprise and operator networking spend, reconstructing the IBN opportunity by applying verified penetration rates by domain and vertical. Select bottom-up roll-ups, sampled annual subscription fees multiplied by installed nodes, serve as guardrails. Key inputs include average policy verification cycles per site, cloud workload proliferation, SD-WAN installed base, and network downtime cost benchmarks. Multivariate regression links these drivers to historical IBN uptake; a scenario-weighted ARIMA forecast projects values through 2030. Where supplier counts are partial, missing nodes are bridged using region-specific capacity utilization factors vetted with experts.

Data Validation & Update Cycle

Outputs pass a two-analyst variance review, after which anomalies trigger a revisit of source assumptions. Models refresh each year, and interim updates are issued when material events, such as major vendor acquisitions or regulatory shifts, alter demand curves. A final pre-publication sweep ensures clients receive the latest calibrated view.

Why Mordor's Intent Based Networking Baseline Commands Reliability

Benchmark comparison

Published estimates often differ because firms slice the domain in distinct ways, convert currencies on varying dates, and refresh models at unequal intervals.

Key gap drivers include whether adjacent network automation licenses are folded in, how aggressively SME uptake is projected, and the cadence at which price erosion is baked into forecasts. Mordor's numbers reflect only AI-enabled, closed-loop platforms, apply blended regional ASPs validated quarterly, and draw on the most recent fiscal year spend disclosures; this disciplined scope keeps our baseline steady yet responsive.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 2.48 B | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 2.90 B | Global Consultancy A | Includes broader network automation suites and license renewals | ||

USD 2.73 B | Regional Consultancy B | Adds professional service revenues and private 5G automation spend | ||

USD 2.26 B | Industry Think-Tank C | Excludes SME deployments and uses lower price erosion factors |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.