Software Defined Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

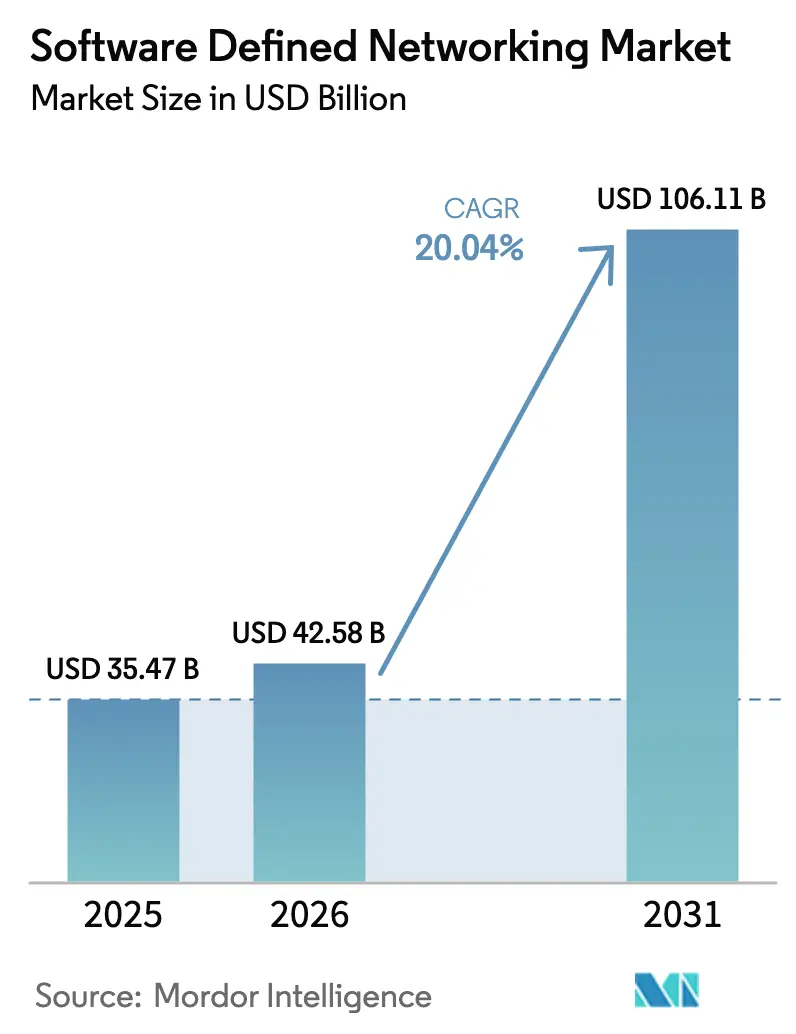

| Market Size (2026) | USD 42.58 Billion |

| Market Size (2031) | USD 106.11 Billion |

| Growth Rate (2026 - 2031) | 20.04% CAGR |

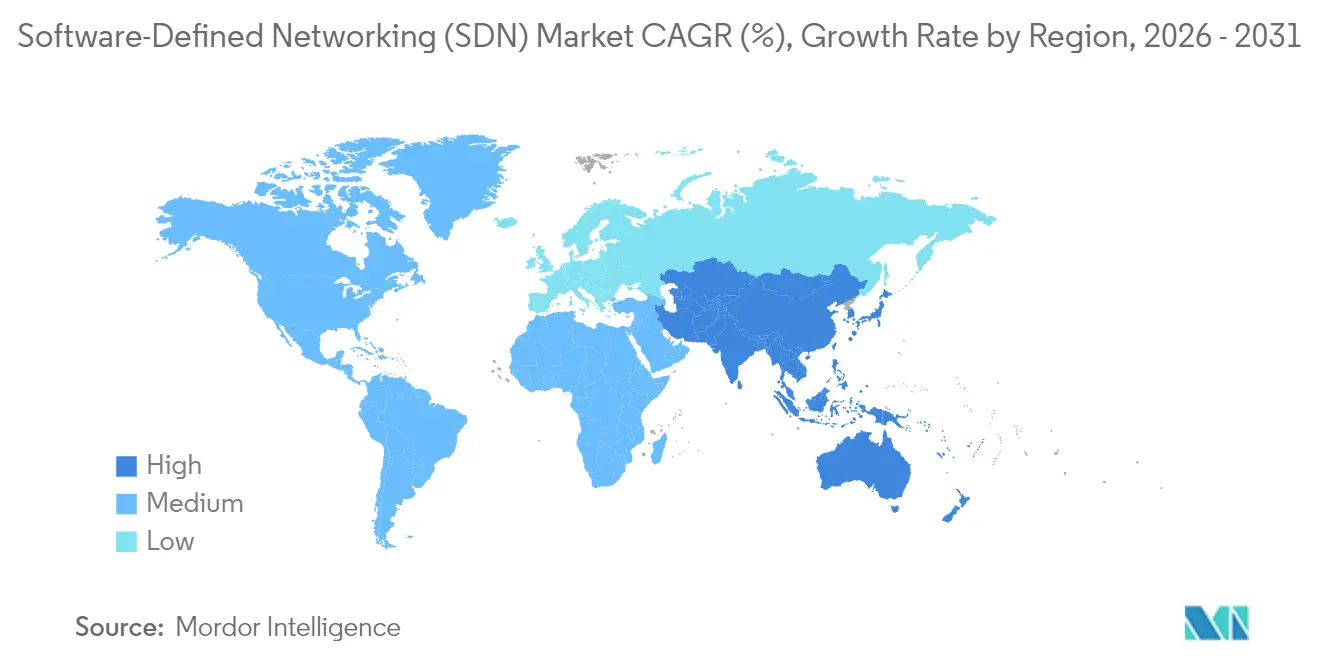

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software Defined Networking Market Analysis by Mordor Intelligence

The software-defined networking market size is expected to grow from USD 35.47 billion in 2025 to USD 42.58 billion in 2026 and is forecast to reach USD 106.11 billion by 2031 at 20.04% CAGR over 2026-2031. Momentum stems from the migration away from fixed-function hardware toward programmable fabrics that support real-time traffic engineering and automated policy enforcement. Large-scale 5G core virtualization, continued cloud migration, and the need to curb network energy consumption all reinforce demand. Government digital-sovereignty laws are amplifying the appeal of open-source controllers, while AI-based telemetry shortens troubleshooting cycles and improves capacity planning. Heightened competitive pressure forces incumbents to blend hardware portfolios with controller software, services, and intent-based orchestration.

Key Report Takeaways

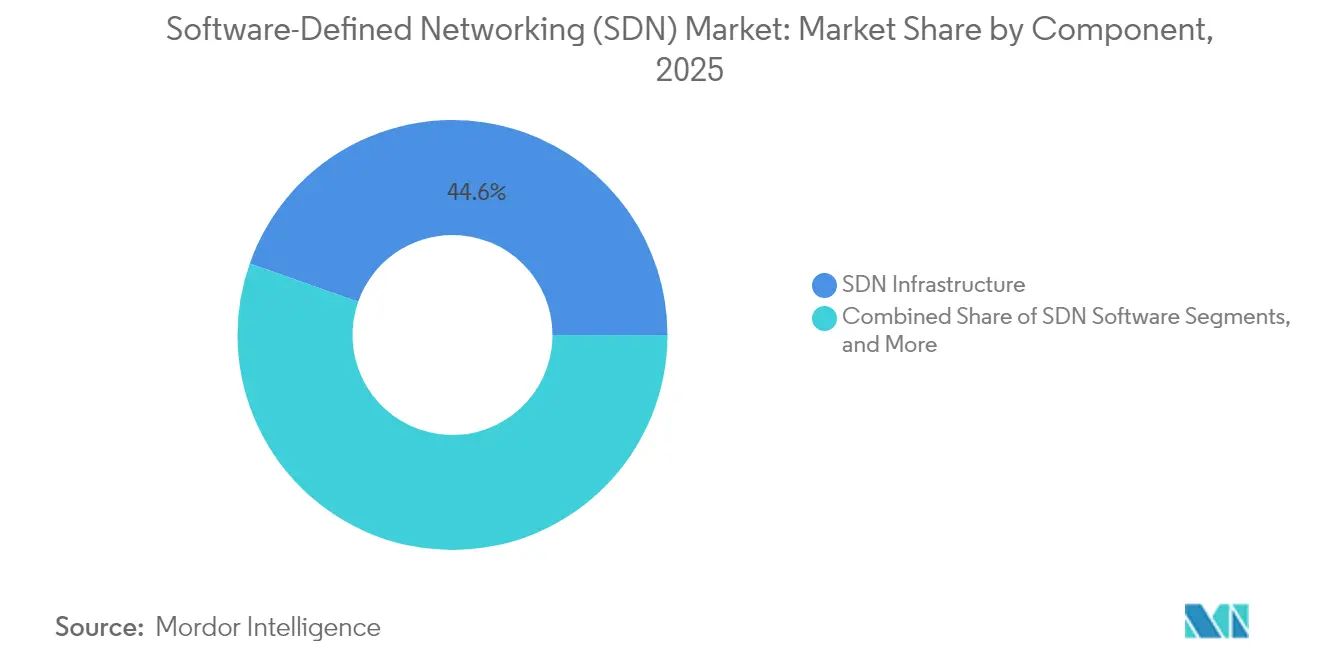

- By component, SDN infrastructure led with 44.60% of software-defined networking market share in 2025; Services and Support is expanding at a 20.78% CAGR to 2031.

- By deployment mode, on-premise retained 53.90% of the software-defined networking market size in 2025, but cloud deployment is poised for 22.3% CAGR through 2031.

- By organization size, large enterprises controlled 61.80% revenue in 2025, while SMEs are projected to compound at 21.7% CAGR.

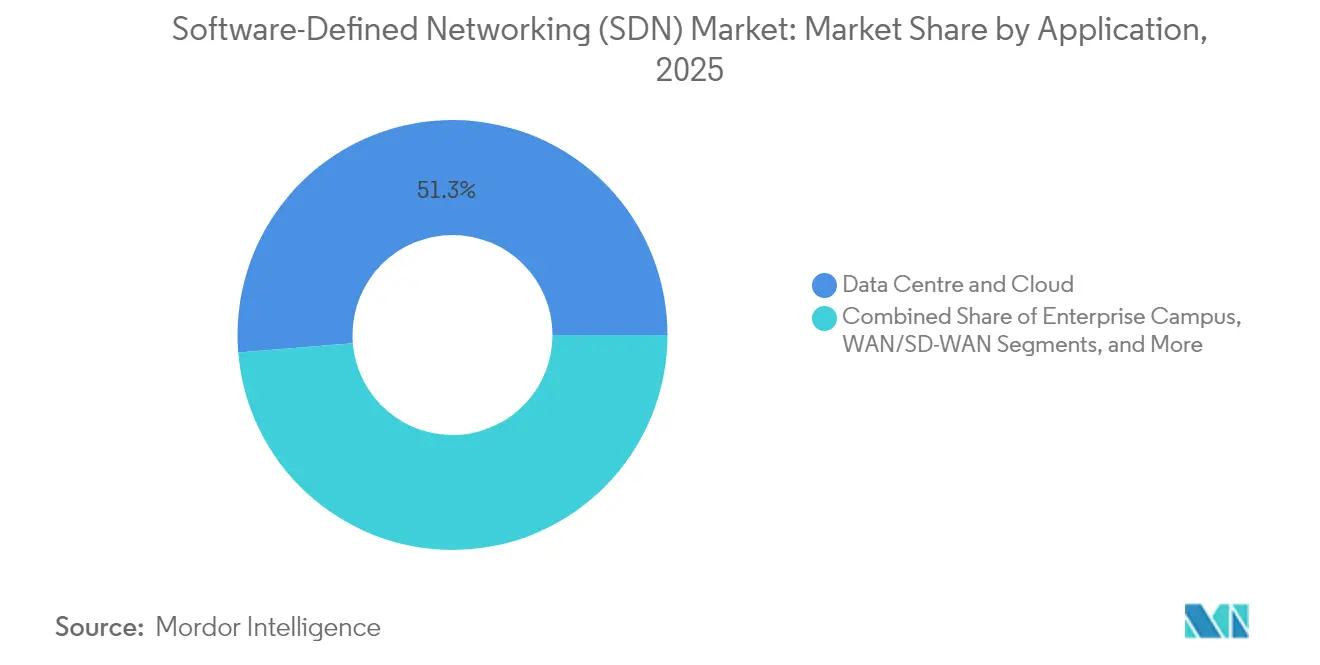

- By application, data-center/cloud captured 51.30% of the software-defined networking market share in 2025, whereas SD-WAN shows a 22.1% CAGR outlook.

- By end user, Telecom and Cloud SPs 32.10% of the software-defined networking market share in 2025, whereas Manufacturing shows a 20.9% CAGR outlook.

- By geography, North America commanded 36.80% revenue in 2025; Asia-Pacific records the fastest 21.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Software Defined Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising investment toward automation of network infrastructure | +3.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing adoption of cloud and IoT-centric services | +4.1% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Proliferation of 5G core virtualization projects | +2.8% | Asia-Pacific core, spill-over to Europe and North America | Medium term (2-4 years) |

| Programmable data-plane (P4) acceleration for ultra-low-latency slicing | +1.9% | North America & Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Sustainability mandates driving energy-optimised SDN fabrics | +2.3% | Europe-led, expanding to North America and Asia-Pacific | Medium term (2-4 years) |

| Sovereign-cloud push for open-source SDN controllers | +1.7% | Europe & North America, selective APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Investment Toward Automation of Network Infrastructure

Enterprises and public agencies are redirecting capex toward programmable fabrics that shrink manual configuration windows. The U.S. Department of Defense earmarked USD 1.355 billion for networking RDT&E programs focused on edge computing and collaborative processes in fiscal 2025. [1]U.S. Department of Defense, “Research, Development, Test & Evaluation FY 2025,” defense.gov Intel’s Network and Edge division generated USD 1.3 billion Q2 2024 revenue from AI-ready Ethernet NICs and infrastructure processing units that underpin self-driving networks. Field studies indicate that SDN-enabled automation can lop up to 40% off operational expenditure and accelerate service rollout by 60%. Financial-services teams illustrate the trend with a 26% rise in GitHub commits targeting Python-based network-automation tools during 2024. Combined, these factors keep automation spending on an upward trajectory through the medium term.

Increasing Adoption of Cloud and IoT-Centric Services

Dynamic multicloud topologies require networks that scale with elastic compute resources. IBM research notes that 60% of communications-service providers already employ AI for performance monitoring in hybrid cloud environments. [2]IBM, “Boost productivity with Responsible AI agents,”ibm.com Manufacturing facilities report a 68% fall in downtime and an 80% rise in continuity after pairing SDN with digital-twin analytics on the production floor. Healthcare providers see comparable gains, using programmable segmentation to protect connected medical devices while sustaining real-time telemetry flows. Such benefits accelerate near-term uptake, especially across Asia-Pacific where cloud traffic volumes are highest.

Proliferation of 5G Core Virtualization Projects

Virtualized 5G cores rely on SDN for network-slice orchestration and ultra-low-latency edge connectivity. Nokia’s bid to purchase Infinera strengthens domestic manufacturing and software-defined radio access offerings in the United States. Research finds that P4-based data planes outperform eBPF alternatives inside standalone 5G cores, particularly in high-throughput scenarios. AT&T’s pledge to virtualize 75% of core functions set the early benchmark for telco SDN deployment. Private-industrial 5G slices now appear in automotive and advanced-manufacturing campuses across Japan and Germany, reinforcing demand for programmable controllers.

Programmable Data-Plane (P4) Acceleration for Ultra-Low-Latency Slicing

P4’s protocol-independent design enables fine-grained packet handling at line-rate. Telefonica Research shows that feature extraction on routers via P4 improves ML-based traffic classification without degrading throughput. Comparative lab work indicates P4Docker can slash latency by 50% and lift throughput 25% versus Mininet simulation. High-frequency trading desks see direct monetary returns from microsecond improvements. Switch silicon vendors now embed PISA pipelines, making P4 adoption practical for mainstream enterprises by the late 2020s.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of SDN-skilled professionals | -2.1% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Rising sophistication of SDN-targeted cyber-attacks | -1.8% | Global, concentrated in high-value targets | Medium term (2-4 years) |

| Multi-vendor P4/eBPF interoperability gaps | -1.3% | North America and Europe primarily | Medium term (2-4 years) |

| Business-critical outages from intent-based control-plane failures | -1.6% | Global, enterprise-focused | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of SDN-Skilled Professionals

Demand for personnel who can code-switch between networking, DevOps, and cloud disciplines exceeds supply. EU research highlights uneven digital-skills development among member states, delaying advanced-network rollouts. Enterprises respond with certification programs, yet P4 and intent-based orchestration remain niche competencies drawing premium salaries. The talent deficit inflates project timelines and advisory-services costs, particularly for brownfield upgrades.

Rising Sophistication of SDN-Targeted Cyber-Attacks

Centralized controllers present lucrative attack surfaces. Vulnerability assessments of OpenDaylight and Floodlight show exposure to LLDP replay and ARP-poison attacks, whereas ONOS fares better but remains imperfect. ENISA warns that cross-border digital infrastructure requires stronger information-sharing frameworks to counter evolving threats. [3]ENISA, “Threat Landscape for 5G Networks,” enisa.europa.eu Financial institutions are especially sensitive because single-controller compromise can reverberate across entire trading platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Infrastructure Dominance Amid Services Acceleration

SDN infrastructure contributed 44.60% of 2025 revenue, anchoring the software-defined networking market size at the hardware layer where programmable ASICs replace legacy switches. Capital-intensive refresh projects remain a prerequisite for controller adoption, sustaining hardware spend into the late 2020s. However, Services and Support postings show the steepest 20.78% CAGR, as enterprises outsource design, deployment, and lifecycle management. Providers like HCLTech widened managed-SDN offerings that bundle AI orchestration and multicloud visibility, underpinning repeatable revenue streams.

Software-controller ecosystems form the decision plane. Open-source frameworks such as ONOS and OpenDaylight temper the risk of vendor lock-in while fostering community-driven innovation. Comparative testing finds ONOS delivers stronger forwarding throughput, whereas OpenDaylight excels in topology discovery and policy distribution. The bifurcation spurs vendors to integrate proprietary value AI-assisted policy engines, zero-trust extensions on top of hardened upstream code.

By Deployment Mode: Cloud Transformation Accelerates

On-premise installations held 53.90% of 2025 revenue as many regulated sectors insist on in-house control. Yet cloud-hosted controllers compound at 22.3% through 2031 as CIOs pivot from capital budgets to opex models. The shift couples with elastic compute tenancy; enterprises spin up controller clusters alongside virtualized workloads, trimming underutilized capacity when demand ebbs. Hybrid topologies emerge as a pragmatic compromise, letting operators preserve sensitive flows on-site while leveraging hyperscale fabrics for burst traffic. A Futuriom survey reveals that 95% of network leaders view multi-cloud connectivity as mission-critical, a stance that reinforces cloud SDN adoption.

Total cost-of-ownership calculations favor cloud for greenfield rollouts under 100 sites, while large campus estates still justify amortized appliance spend. Vendors now bundle controller-as-a-service tiers with traffic-analysis dashboards, easing SME onboarding. Inter-cloud policy alignment remains a friction point; standards groups push for open API schemas to share intent metadata across Amazon, Microsoft, and Google realms.

By Organization Size: Enterprise Leadership Faces SME Disruption

Large enterprises accounted for 61.80% of 2025 spend, leveraging scale budgets to modernize data-center, campus, and WAN domains. Their deployments merge SDN with IT-service-management platforms, feeding topology insights into ITIL workflows for automated trouble-ticket routing. In contrast, SMEs inject momentum, posting a 21.7% CAGR as turnkey SD-WAN subscriptions negate the need for specialist staff. They often start with cloud-hosted vCPE that offers point-and-click segmentation for branch offices.

Price elasticity favors pay-as-you-grow tiers; providers package bandwidth, cloud egress, and security under a unified SLA. Vendors build simplified dashboards that abstract away topology complexity, positioning SME solutions as “consumer-grade UX inside enterprise networks”. The rapid scale of SME logos sharpens channel competition and compresses margins for mid-tier resellers.

By Application: Data Center Maturity Contrasts SD-WAN Growth

Data-center and cloud fabrics delivered 51.30% of 2025 sales, underpinned by well-documented ROI. Cohesive east-west traffic engineering and serverless orchestration keep this slice of the software-defined networking market resilient. Yet SD-WAN registers the quickest 22.1% CAGR amid pandemic-driven hybrid-work norms. Direct cloud handoffs reduce trombone latency, and application-aware routing boosts SaaS performance.

Campus SDN adoption trails but accelerates as organizations unify access-edge and core policies. Vendors now ship Wi-Fi APs that natively tag flows for controller-driven micro-segmentation. In WAN domains, MPLS fade-out continues; intent-based overlay fabrics promise 10-minute branch turn-ups compared with weeks under legacy ordering cycles.

By End User: Telecom Leadership Amid Manufacturing Surge

Telecom and cloud service providers retained 32.10% of 2025 turnover, harnessing SDN to enable 5G slicing, NFV, and edge MEC nodes. Their requirements push scalability thresholds into millions of end points, steering product roadmaps toward P4 pipelines and AI-root-cause engines. Manufacturing vaults forward with a 20.9% CAGR, embedding SDN in Industry 4.0 settings to guarantee deterministic latency between robots, sensors, and analytics hubs. Semiconductor fabs attribute uptime gains to programmable fabrics that isolate clean-room machinery from office traffic.

BFSI modernization trails telcos yet accelerates thanks to low-latency trading and regulatory audit mandates. Healthcare players lean on controller APIs to enforce HIPAA-aligned segmentation across multicloud workloads. Retail chains pursue omnichannel consistency, shifting POS and inventory platforms onto SD-WAN for resilient site connectivity.

Geography Analysis

North America generated 36.80% of 2025 revenue, buoyed by enterprise cloud migration and federal Research and Development outlays. The U.S. Department of Defense alone invested more than USD 1.3 billion in software-centric networking projects, forging demand for secure, programmable fabrics in classified environments. Start-up density around Silicon Valley, Austin, and Toronto accelerates controller innovation, while open-source stewardship by the Linux Foundation fosters multivendor interoperability.

Europe ranks second, driven by sustainability mandates and digital-sovereignty statutes that advocate open-source adoption. EU firms bear bureaucratic costs equal to 1.8% of turnover, incentivizing automated network operations that curb compliance overhead. Regulators promote competition by obligating wholesale access and monitoring oligopolistic tendencies within telecom backbones. Simultaneously, national 5G rollout targets spur carrier investment in SDN-controlled RAN slicing for enterprise verticals, aligning with energy-efficiency commitments.

Asia-Pacific is the fastest-growing locale, posting a 21.1% CAGR through 2031. China’s Digital Silk Road has driven nearly USD 23 billion into ICT projects across 24 Indo-Pacific states since 2017, catalyzing wide-area SDN deployments for cross-border data corridors. Japanese smart-manufacturing consortia deploy private 5G and time-sensitive networking overlays, while India’s IT-services giants integrate SDN into managed campus solutions for domestic enterprises. Rapid urbanization and a swelling base of mobile-first consumers enlarge edge-traffic volumes, making programmable congestion control a necessity rather than a luxury.

Competitive Landscape

Competition remains restless as legacy hardware vendors race to infuse software, while cloud-native entrants weaponize agile release cycles. Cisco and Juniper still dominate chassis share, yet revenue reliance shifts toward recurring licenses, controller subscriptions, and automation packages.

Arista Networks epitomizes disruptive ascent, surpassing USD 7 billion in FY 2024 revenue by tailoring data-center switches for AI cluster fabrics. Broadcom’s Tomahawk 6 silicon pushes 102.4 Tbps and 1,024×100 Gbps SerDes into a single device, catering to hyperscale build-outs where microburst buffering and congestion telemetry are must-haves. Open-source controller communities create further headwinds, giving enterprises cheaper entry paths and heightening price sensitivity.

Services specialists carve value by bridging skill gaps. Global system integrators develop turnkey playbooks that meld P4 data planes with zero-trust overlays. Meanwhile, telco NEPs chase vertical solutions in manufacturing, healthcare, and smart cities, where domain know-how offsets commoditizing hardware economics. Vendor differentiation now gravitates to AI-assisted operations, sovereign-cloud compliance, and energy-optimized forwarding.

Software Defined Networking Industry Leaders

Ciena

Dell Technologies

Palo Alto Networks

NEC Corporation

AT&T Business

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Arista Networks acquired VeloCloud from Broadcom for about USD 1 billion, adding mature SD-WAN technology and broadening its campus-to-cloud portfolio

- June 2025: Broadcom debuted Tomahawk 6 switches delivering 102.4 Tbps throughput with Ultra Ethernet Consortium compliance, boosting AI fabric scalability

- April 2025: HPE closed its USD 14 billion purchase of Juniper Networks, uniting Marvis AI with HPE compute to form a top-to-bottom SDN stack

- February 2025: Cisco introduced UCS C845A M8 servers and N9300 Smart Switches featuring Hypershield for AI-ready security and universal ZTNA

- January 2025: Network World highlighted a surge of AI-first acquisitions as SASE consolidation shapes 2025 networking strategy

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the software-defined networking (SDN) market as the worldwide revenue earned from software controllers, programmable switches, orchestration tools, and implementation services that virtualize and centrally manage data-center, campus, and carrier networks.

Scope exclusion: Pure SD-WAN overlay subscriptions, legacy hardware-only routing devices, and private microwave backhaul links are left outside this boundary.

Segmentation Overview

- By Component

- SDN Infrastructure (Switching, Routers, NICs)

- SDN Software / Controllers

- Services and Support

- By Deployment Mode

- On-premise

- Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Application

- Data Centre and Cloud

- Enterprise Campus

- WAN / SD-WAN

- Others

- By End User

- Telecom and Cloud Service Providers

- BFSI

- Healthcare

- Retail and E-commerce

- Manufacturing and Industrial

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Discussions with network architects, hyperscale procurement leads, regional carriers, and value-added resellers across North America, Europe, and Asia helped us test price bands, migration timelines, and controller adoption hurdles that secondary data could not reveal.

Desk Research

We first gathered foundational figures from open datasets such as the US Federal Communications Commission fixed-broadband trends, Eurostat ICT enterprise surveys, Japan's MIC telecommunication statistics, and UN Comtrade router exports. We then matched them with white papers issued by the Linux Foundation, ETSI NFV forum, and major vendor 10-Ks. To size spending pockets by vertical, our team checked traffic growth disclosures in cloud provider filings and reviewed carrier capex trackers released by the GSMA. For financial benchmarks and news flow calibration, Mordor analysts leaned on curated feeds from D&B Hoovers, Dow Jones Factiva, and patent pools in Questel. The sources listed here are illustrative; numerous additional publications and databases were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

A top-down model begins with global data-center port counts and carrier edge node inventories, which are then overlaid with controller penetration ratios, average license fees, and annual maintenance factors. Sampled supplier roll-ups and channel checks serve as a bottom-up sense test before final adjustment. Key variables include 5G core virtualization share, cloud VM growth, switch silicon ASP curves, regulatory zero-trust mandates, and trained-engineer headcount. Forecasts employ multivariate regression paired with scenario analysis so our base case aligns with consensus views gathered during interviews while flagging upside from AI-driven telemetry demand.

Data Validation & Update Cycle

Outputs pass anomaly screens, peer review, and senior-analyst sign-off. Models refresh yearly, with interim revisions triggered by material M&A, spectrum auctions, or policy shifts. A fresh validation sweep precedes every client delivery.

Why Mordor's Software Defined Networking Baseline Commands Unmatched Reliability

Published SDN values often diverge because each firm tweaks scope, base year, and price assumptions. We disclose every inclusion, refresh annually, and, importantly, validate license and support fees against live quotes, which many studies omit.

Gaps typically stem from folding SD-WAN or data-center hardware into totals, applying one global ASP, or extrapolating from limited vendor shipment data. Our method filters these pitfalls through geography-specific pricing, service-mix splits, and interview-backed penetration ratios.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 35.47 bn (2025) | Mordor Intelligence | |

| USD 37.66 bn (2024) | Global Consultancy A | Bundles SD-WAN revenue and counts full-term MSP contracts as software ARR |

| USD 24.50 bn (2023) | Industry Tracker B | Excludes professional services and uses an older base year |

| USD 39.10 bn (2025) | Research Firm C | Relies on uniform ASP applied to top vendor shipments without regional calibration |

Taken together, the comparison shows that when scope clarity, region-level pricing, and mixed-method validation come together, Mordor's figures provide a balanced, transparent baseline that decision-makers can trace back to explicit variables and reproducible steps.

Key Questions Answered in the Report

What is the current size of the software-defined networking market?

The market is worth USD 42.58 billion in 2026 and is projected to rise to USD 106.11 billion by 2031.

Which region shows the highest growth potential?

Asia-Pacific posts a 21.1% CAGR through 2031, propelled by large-scale 5G rollouts and manufacturing digitization.

Why is SD-WAN growing faster than data-center SDN?

Remote-work patterns and cloud-first application delivery favor SD-WAN overlays that improve SaaS performance and reduce branch latency.

What skills are most in demand for SDN careers?

Expertise in P4 programming, DevOps automation, and multicloud networking is scarce and commands premium salaries.

How vulnerable are SDN controllers to cyber-attacks?

Centralized controllers can be single points of failure; studies reveal replay and poisoning exploits, underscoring the need for layered security and continuous patching.

Page last updated on: