Carbonated Beverage Processing Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

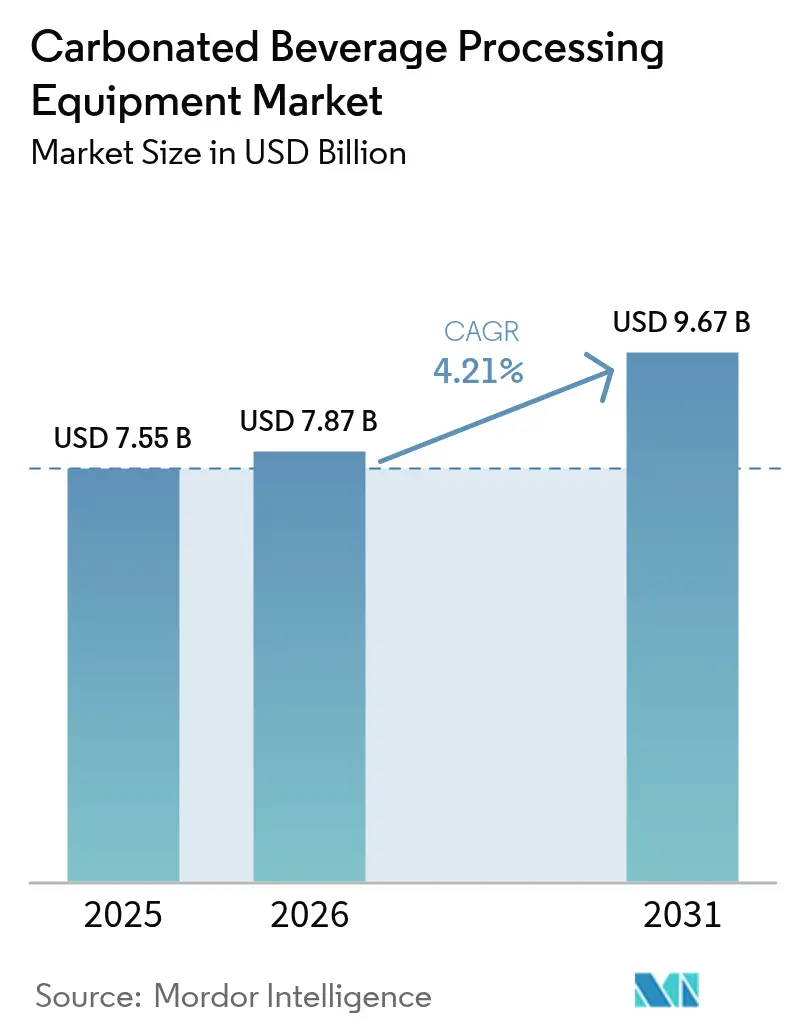

| Market Size (2026) | USD 7.87 Billion |

| Market Size (2031) | USD 9.67 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Carbonated Beverage Processing Equipment Market Analysis by Mordor Intelligence

The carbonated beverage processing equipment market size was valued at USD 7.55 billion in 2025 and estimated to grow from USD 7.87 billion in 2026 to reach USD 9.67 billion by 2031, at a CAGR of 4.21% during the forecast period (2026-2031). The market growth is driven by increased investments in the beverage industry, strict food safety regulations, and sustainability requirements. Equipment manufacturers are integrating IoT sensors, predictive maintenance software, and energy recovery systems to reduce operational downtime and energy consumption. These technological integrations enable real-time monitoring of production processes, early detection of potential equipment failures, and optimization of energy usage across the manufacturing line. While North American beverage companies upgrade their existing production lines to improve efficiency and meet modern manufacturing standards, Asia-Pacific manufacturers are establishing new facilities to address growing urban consumption patterns and changing consumer preferences. The increasing demand for premium craft sodas and functional carbonated beverages is driving manufacturers to develop modular, compact equipment that efficiently manages smaller production batches. These flexible systems allow producers to quickly switch between different product formulations and package sizes while maintaining optimal production efficiency and quality standards.

Key Report Takeaways

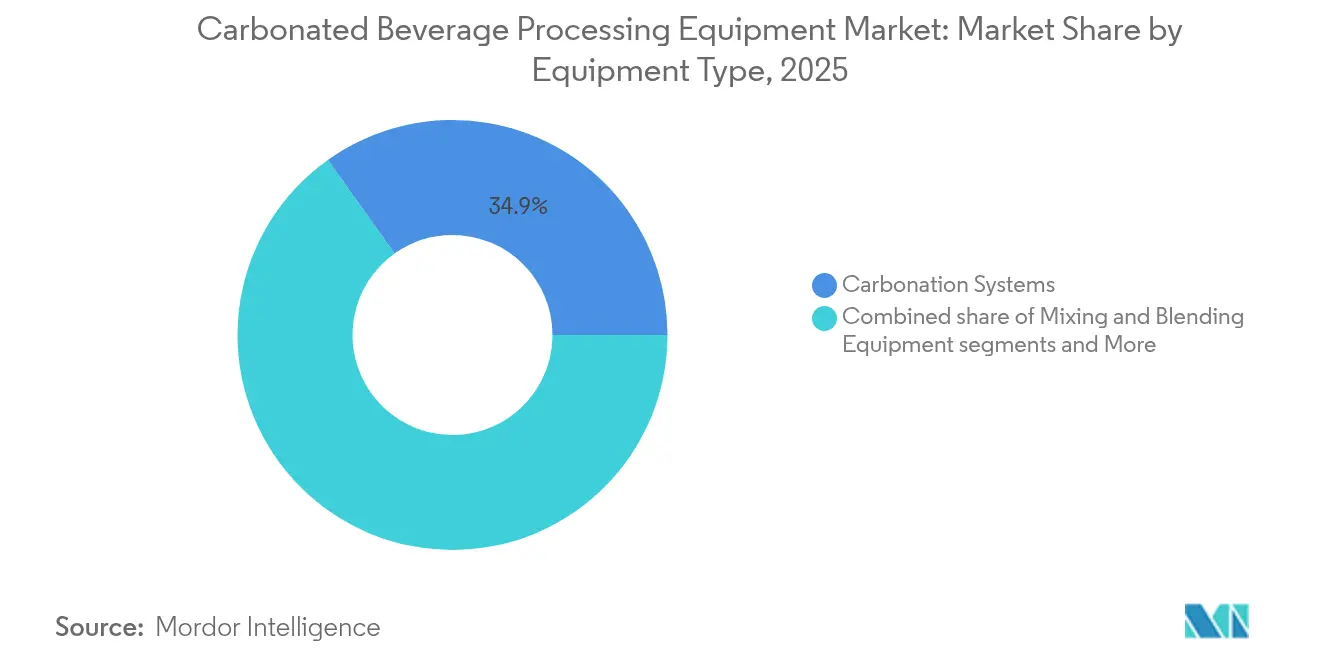

- By equipment type, carbonation systems led with 34.85% revenue share in 2025, whereas sugar dissolution systems are forecast to expand at a 4.92% CAGR through 2031.

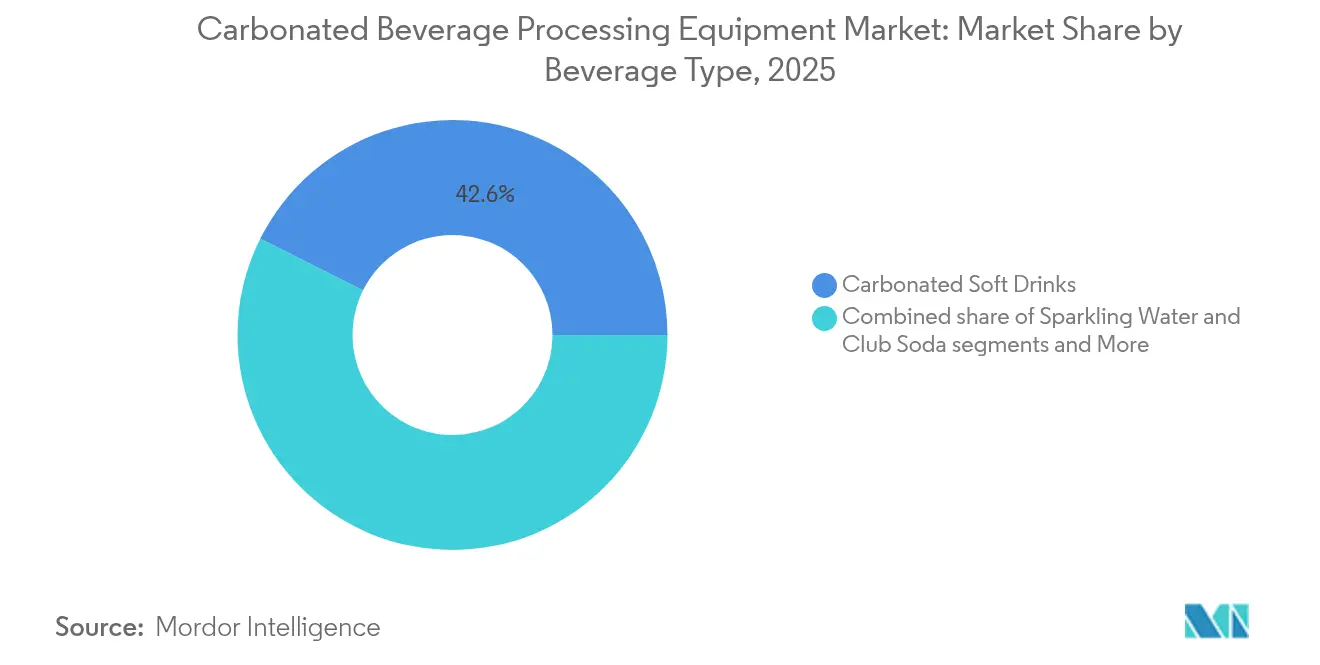

- By beverage type, carbonated soft drinks captured 42.62% of the carbonated beverage processing equipment market share in 2025, carbonated functional beverages are advancing at a 5.41% CAGR to 2031.

- By automation level, fully automatic processing equipment accounted for 54.60% of the carbonated beverage processing equipment market size in 2025 and is set to grow at a 5.55% CAGR through 2031.

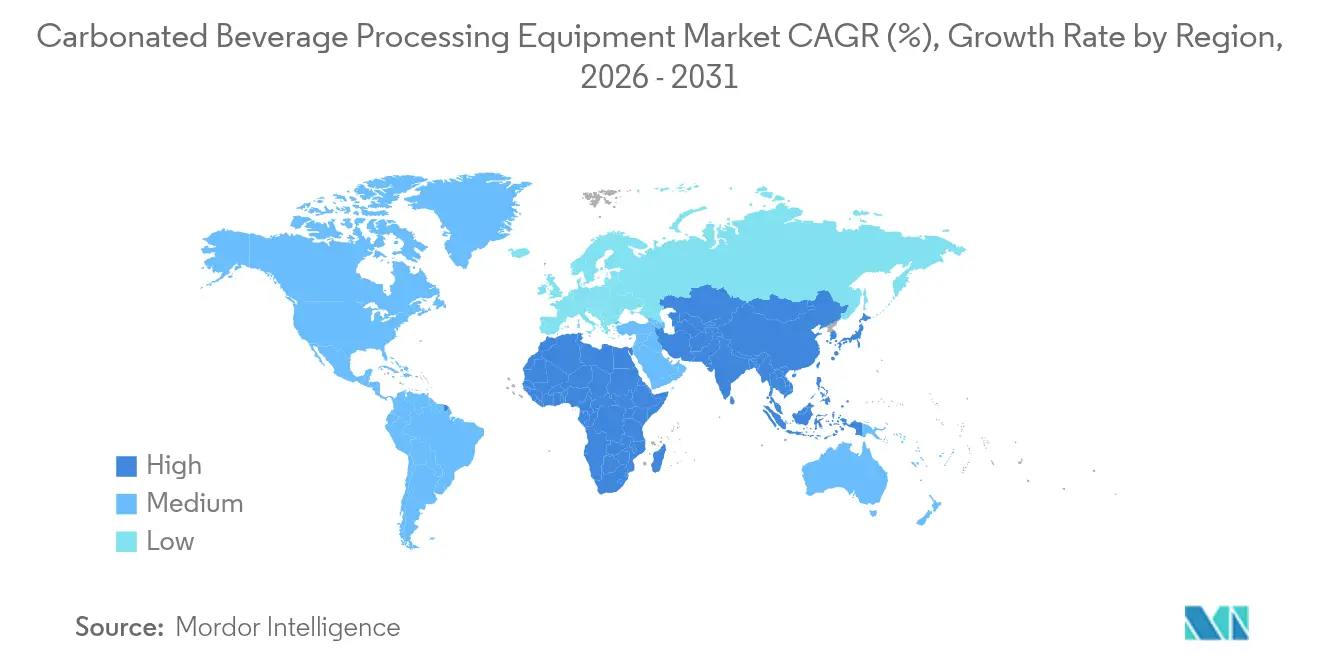

- By geography, North America held 34.75% revenue share in 2025, while Asia-Pacific is projected to post the fastest regional CAGR at 5.44% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carbonated Beverage Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising carbonated soft drink consumption | +1.2% | Global, with strongest impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Growing preference for automated and energy-efficient beverage processing systems | +0.9% | North America and Europe leading, Asia-Pacific following | Long term (≥ 4 years) |

| Advances in carbonation and packaging technologies enhancing efficiency and quality | +0.8% | Global, with technology hubs in Germany, United States, and Japan | Medium term (2-4 years) |

| Increasing use of pet bottles and cans in carbonated beverage packaging | +0.6% | Global, particularly strong in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Growth of craft soda startups driving demand for modular and scalable equipment | +0.4% | North America and Europe core, expanding to urban centers globally | Long term (≥ 4 years) |

| Integration of IOT and smart sensors for real-time monitoring and predictive maintenance | +0.7% | Advanced markets initially, scaling to developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising carbonated soft drink consumption

Global demand for carbonated beverages continues to grow despite increasing sugar-reduction initiatives worldwide. In the Asia-Pacific region, bottling companies are installing new high-speed production lines to meet the rising demand from urban consumers who prefer portable packaging formats for their daily consumption. These advanced production systems require sophisticated carbonation units that can maintain consistent CO₂ levels across varying temperature ranges, leading equipment manufacturers to enhance their inline-blending systems and develop more efficient sanitary valve technologies. The expanding consumption patterns in both developed and emerging markets are generating increased demand for specialized processing equipment that can handle multiple beverage formulations, including traditional carbonated soft drinks, reduced-sugar options, natural sweetener variants, and functional sparkling beverages with added nutrients and supplements. According to the data from the British Soft Drinks Association, an increase from 2023, approximately 5.9 billion liters of carbonates were consumed in the United Kingdom.[1]Source: British Soft Drinks Association, "BSDA Annual Report 2024 UK Soft Drinks Report", britishsoftdrinks.com

Growing preference for automated and energy-efficient beverage processing systems

Beverage manufacturers are increasing automation and energy efficiency to address labor shortages, reduce operational costs, and meet sustainability goals. Equipment manufacturers are developing integrated systems that combine multiple processing steps, including filling, capping, labeling, and packaging, while reducing energy consumption through advanced heat recovery technologies and minimizing water usage with sophisticated cleaning-in-place systems. Heat-recovery exchangers capture and reuse thermal energy from processing operations, dry-lubrication conveyors eliminate the need for water-based lubricants, and AI-based cleaning-in-place cycles optimize cleaning schedules and chemical usage to reduce water and detergent consumption. With return-on-investment periods now under four years, mid-sized bottlers are transitioning from semi-automatic systems to fully automated operations, enabling 24/7 production with minimal human intervention. These automated systems incorporate sensors and monitoring equipment to track production metrics, maintain quality control, and predict maintenance needs, while advanced robotics handle material movement and packaging tasks traditionally performed by human operators.

Advances in carbonation and packaging technologies enhancing efficiency and quality

Carbonation technology advances have transformed beverage manufacturing through sophisticated CO2 dissolution control systems that precisely regulate gas-to-liquid ratios, advanced inline blending capabilities that ensure homogeneous mixing of ingredients, and state-of-the-art aseptic processing methods that significantly extend product shelf life while preserving taste profiles and nutritional integrity. Equipment manufacturers now integrate comprehensive digital monitoring systems featuring real-time sensors and automated controls that continuously track carbonation levels, temperature profiles, and pressure variations throughout the production process, ensuring batch-to-batch consistency and minimizing material waste through predictive maintenance algorithms. Packaging technology improvements have revolutionized the industry with innovative lightweight materials incorporating nano-engineered barrier properties, smart packaging features for enhanced product protection, and advanced recyclability characteristics that align with circular economy principles while optimizing transportation efficiency and reducing overall logistics costs.

Increasing use of PET bottles and cans in carbonated beverage packaging

The beverage industry's transition to PET bottles and aluminum cans increases equipment demand as producers modify their packaging operations to maintain efficiency and market competitiveness. Equipment manufacturers now offer advanced filling systems that handle both PET and aluminum containers, allowing producers to adjust packaging strategies based on market dynamics, consumer preferences, and production costs. The ongoing aluminum can shortage creates significant opportunities for flexible equipment solutions that enable seamless transitions between container types while maintaining production efficiency. Processing systems must comprehensively address specific requirements for each packaging format, including precise fill rates, reliable sealing methods, and comprehensive quality verification protocols. This diversification in packaging drives the need for sophisticated modular equipment that can rapidly adapt to various container sizes and materials, helping producers effectively manage supply chain disruptions, meet changing consumer demands, and capitalize on emerging market opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital investment and operating costs | -0.8% | Global, particularly impacting emerging markets and SMEs | Short term (≤ 2 years) |

| Strict food safety and equipment sanitation regulations increasing complexity | -0.5% | Advanced markets with stringent regulatory frameworks | Medium term (2-4 years) |

| Rising consumer shift toward healthier, non-carbonated beverages reducing carbonation demand | -0.6% | North America and Europe leading, spreading globally | Long term (≥ 4 years) |

| Fluctuating raw material costs and supply chain disruptions affecting equipment production | -0.4% | Global, with particular impact on steel and aluminum-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High initial capital investment and operating costs

The high costs of equipment procurement and installation present major barriers for beverage producers, especially small manufacturers and new market entrants looking to establish or expand carbonated beverage production. Equipment manufacturers offer modular systems for phased implementation, enabling beverage producers to begin with basic configurations and expand as production volumes increase. These financing challenges particularly affect craft beverage startups and regional producers who compete with multinational corporations but have limited financial resources. As a result, the market sees increased demand for used equipment and equipment-as-a-service options that lower initial capital requirements while providing access to advanced processing technologies.

Strict food safety and equipment sanitation regulations increasing complexity

The 2022 US FDA Food Code revision strengthened requirements for active managerial control, requiring fillers to incorporate electropolished surfaces, tool-less disassembly, and validation-ready CIP cycles.[2]Source: US Food & Drug Administration, “Food Code 2022,” fda.gov Equipment manufacturers must comply with strict sanitation standards, including specific food-contact surface requirements, cleaning-in-place systems, and documentation protocols that align with HACCP principles. The increased regulatory requirements drive up equipment costs as manufacturers integrate additional sensors, monitoring systems, and documentation features to meet current standards. Processing equipment requires design elements that enable frequent cleaning while maintaining production efficiency, including appropriate materials, protective coatings, and automated cleaning systems that reduce manual cleaning while ensuring sanitation standards. These requirements create significant challenges for smaller equipment manufacturers and beverage producers who do not have dedicated compliance departments and must depend on equipment vendors for regulatory compliance support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Precision Modules Define Next-Generation Lines

Carbonation systems dominated with a 34.85% share of the carbonated beverage processing equipment market in 2025, maintaining their essential position in ensuring consistent taste profiles across beverage production lines. Sugar dissolution systems recorded a significant 4.92% CAGR, primarily driven by increased production demands for low-Brix colas and zero-sugar sodas that require precise micron-level dosing capabilities. Manufacturers are strategically integrating mixing, deaeration, and carbonation functions into comprehensive unified systems to minimize facility footprint requirements and enhance cleaning efficiency across production cycles. Pentair's advanced CO₂-recovery system demonstrates sustainable manufacturing design by capturing and purifying fermentation gas at 99.998% purity for direct reuse in soft-drink production lines, substantially reducing external CO₂ requirements by up to 60%.

Heat exchangers and membrane filters maintain robust market performance, with technological developments focusing on advanced regenerative plate packs and sophisticated back-pulseable cartridges that significantly extend cleaning intervals in production environments. The market for mixing and blending equipment continues to expand as manufacturers increase production of sparkling functional beverages containing complex botanical ingredients that require specialized high-speed agitation processes. Equipment manufacturers are strategically incorporating advanced low-RPM magnetic mixers and precision in-tank ultrasound emulsifiers to maintain and protect the effectiveness of sensitive bioactive ingredients throughout the production process.

By Level of Automation: Digital Twins and Lights-Out Operations

Fully automatic processing equipment accounted for 54.60% of the carbonated beverage processing equipment market size in 2025 and is likely to grow at a CAGR of 5.55% through 2026-2031. These systems are experiencing rapid growth due to advancements in robotics and artificial intelligence platforms. The integrated control systems now manage complex recipe formulations, monitor Overall Equipment Effectiveness (OEE), and implement predictive maintenance ordering protocols. This comprehensive automation enables real-time data collection, analysis, and optimization across bottling facilities, improving operational efficiency and product consistency.

Semi-automatic modules maintain strong demand among regional bottlers seeking lower capital expenditure while meeting hygiene standards. These systems offer a balance between manual control and automated processes, allowing operators to maintain quality while reducing labor costs. While craft soda manufacturers prefer batch carbonation vessels for precise production control and customization capabilities, many integrate cloud-connected flowmeters for remote diagnostics and quality assurance. This transition enables smaller manufacturers to achieve higher production efficiency while retaining their artisanal production methods.

By Beverage Type: Functional Formulations Accelerate Equipment Upgrades

Carbonated soft drinks maintain market dominance with 42.62% market share, while carbonated functional beverages grow at a 5.41% CAGR, influencing equipment specifications. The production of probiotic sodas, vitamin-fortified seltzers, and plant-based energy drinks requires aseptic fillers with specialized carbonation loops to minimize oxygen pick-up. Manufacturers now implement dual-zone tunnel pasteurizers for precise heat treatment to preserve live cultures. Sparkling water production lines increasingly utilize glass packaging for premium products, requiring rinser-filler-capper monoblocks that process 60,000 bottles per hour across various neck finishes.

While carbonated isotonic and energy drink equipment market share remains stable, higher caffeine concentrations necessitate seamers to maintain dissolved-oxygen levels under 0.5 ppm. Equipment manufacturers address this through long-stem vent tubes and in-line deaeration membranes, enabling shelf stability without preservatives. The market demands flexible production lines capable of handling multiple beverage types and packaging formats. Manufacturers incorporate quick-changeover systems and modular equipment to minimize production downtime. Advanced control systems with recipe management ensure product consistency across beverage varieties. IoT sensors and real-time monitoring systems enable predictive maintenance and production optimization.

Geography Analysis

North America held 34.75% of global revenue in 2025, driven by retrofit programs replacing older fillers with servo-driven monoblocks that enable faster changeovers. Manufacturers have adopted energy-recovery systems and low-lubrication conveyors to meet corporate environmental, social, and governance (ESG) targets. The market growth continues through the craft-soda segment, which requires compact, easily configurable production lines, supporting aftermarket parts and service revenue.

Asia-Pacific is projected to achieve a 5.44% CAGR through 2031, leading global growth rates. Increasing disposable income, urbanization, and changing consumer preferences drive local companies to expand production capacity. Chinese and Indian manufacturers are adopting Western hygiene standards, creating opportunities for European equipment manufacturers to license designs for regional production. Government incentives support the adoption of heat-pump pasteurization systems that reduce greenhouse gas emissions.

Europe maintains steady growth as packaging regulations drive the adoption of lightweight bottles and tethered caps. Equipment updates emphasize quick-release filler valves and water recycling systems. Eastern European developments, including Krombacher's EUR 100 million bottling facility upgrade in November 2024, demonstrate regional manufacturers' commitment to expanding capacity while meeting EU carbon regulations. South America and the Middle East and Africa regions are investing in modular PET lines connected to solar-powered systems, indicating a direct transition to modern beverage production methods.

Competitive Landscape

The market maintains moderate concentration, with major players like Krones AG, GEA Group AG, KHS GmbH, and Tetra Laval (Tetra Pak). Competing through comprehensive solutions, including turnkey operations, lifecycle service contracts, and digital platforms. Krones has enhanced its PET preform capabilities through the acquisition of Netstal, an injection molding technology company. GEA Group has specialized in hygienic valves and heat-pump pasteurization, offering carbon-footprint calculators to demonstrate customer cost savings.

Challenger companies focus on specialized technologies. Omnia Technologies has consolidated ACMI and SACMI Beverage into a high-speed bottling division, offering canning capabilities of 90,000 bottles per hour with 30% reduced energy consumption, launched in May 2024. Pentair targets sustainability-focused brewers and soda manufacturers through its gas-recovery technology. The expanding aftermarket for predictive maintenance upgrades has created opportunities for software companies to collaborate with original equipment manufacturers (OEMs), generating revenue from equipment data throughout the product lifecycle.

Competition has evolved from mechanical performance to comprehensive cost-of-ownership solutions that incorporate energy efficiency, operational uptime, and regulatory compliance. Companies establish regional technology centers to reduce service response times and conduct customer recipe testing. The carbonated beverage processing equipment market expansion is likely to drive increased merger activities, particularly in automation software and recyclable packaging technologies.

Carbonated Beverage Processing Equipment Industry Leaders

-

Krones AG

-

GEA Group AG

-

KHS GmbH

-

Tetra Laval (Tetra Pak)

-

Goma Engineering Pvt. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sojo Industries, an industrial automation company, has secured USD 40 million in funding from S2G Investments to expand its modular robotic packaging systems and track-and-trace software.

- October 2024: Thermal Kitchen, a food and beverage co-manufacturer, introduced its beverage canning line. The line processes pasteurized carbonated and non-carbonated beverages, expanding the company's production capacity to serve beverage manufacturers and national brands with enhanced efficiency and quality.

- April 2024: Rotarex Solutions introduces the BubbleBox Carbo Pro, an inline carbonation system for the hospitality industry. The system provides a continuous carbonated water supply from the tap and can be installed in back rooms, under counters, or connected to existing coolers.

- January 2024: Krones inked a deal to take over the entirety of Netstal Maschinen AG (Netstal), a key player in molding machines for the beverage sector, from its current owner, KraussMaffei.

Global Carbonated Beverage Processing Equipment Market Report Scope

The scope of the carbonated beverage processing market includes segmentation of the market by equipment type, which includes Sugar Dissolver, Carbonation Equipment, Blenders and Mixers, Heat Exchanger, and Other Equipment. Further segmentation is done under the type of beverage, which includes Flavored Drinks, Functional Drinks, and Club Soda and Sparkling Water. Lastly, the market is segmented by geography, covering all the regions across the world.

| Carbonation Systems |

| Mixing and Blending Equipment |

| Heat Exchangers |

| Sugar Dissolution Systems |

| Filtration and Clarification Equipment |

| Other Equipment |

| Carbonated Soft Drinks (CSDs) |

| Carbonated Functional Beverages |

| Sparkling Water and Club Soda |

| Carbonated Energy and Isotonic Drinks |

| Fully Automatic Processing Equipment |

| Semi-Automatic Processing Equipment |

| Manual or Batch-Scale Processing Equipment |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Equipment Type | Carbonation Systems | |

| Mixing and Blending Equipment | ||

| Heat Exchangers | ||

| Sugar Dissolution Systems | ||

| Filtration and Clarification Equipment | ||

| Other Equipment | ||

| By Beverage Type | Carbonated Soft Drinks (CSDs) | |

| Carbonated Functional Beverages | ||

| Sparkling Water and Club Soda | ||

| Carbonated Energy and Isotonic Drinks | ||

| By Level of Automation | Fully Automatic Processing Equipment | |

| Semi-Automatic Processing Equipment | ||

| Manual or Batch-Scale Processing Equipment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the carbonated beverage processing equipment market?

The market is valued at USD 7.87 billion in 2026 and is forecast to reach USD 9.67 billion by 2031.

Which equipment type holds the largest market share?

Carbonation systems command 34.85% revenue share due to their pivotal role in product quality control.

Why are fully automatic lines growing fastest?

They deliver higher uptime, lower labor costs, and energy savings, which translate into a 5.55% CAGR through 2031.

Which region is expanding most rapidly?

Asia-Pacific is projected to post a 5.44% CAGR as urbanization and income growth boost soft-drink demand.

Page last updated on: