Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

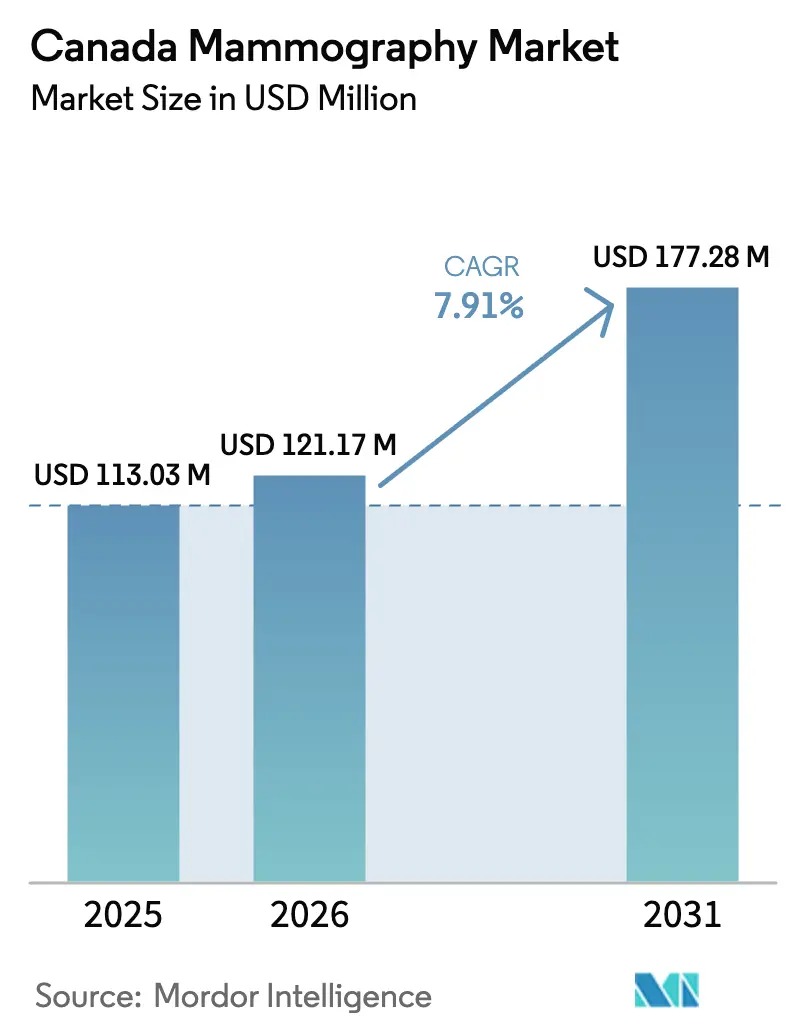

| Base Year Market Size (2025) | USD 113.03 Million |

| Market Size (2026) | USD 121.17 Million |

| Market Size (2031) | USD 177.28 Million |

| Growth Rate (2026 - 2031) | 7.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Mammography Market Analysis by Mordor Intelligence

The Canada Mammography Market size was valued at USD 113.03 million in 2025 and is estimated to grow from USD 121.17 million in 2026 to reach USD 177.28 million by 2031, at a CAGR of 7.91% during the forecast period (2026-2031).

Provincial moves to lower the screening start age to 40 years have expanded the eligible population by roughly 1.2 million women and are pushing up procurement cycles for digital and 3D systems. Federal grants that target artificial-intelligence deployments are changing vendor short-lists, favoring platforms with embedded detection algorithms over bolt-on software. Public bulk-purchase frameworks led by Quebec and Alberta are securing 15-20% discounts on equipment and long, standardized service-level agreements. Finally, cloud picture-archiving contracts such as Quebec’s CAD 405.5 million, 12-year Sectra deal are linking rural and urban sites, easing radiologist shortages and supporting mobile-unit workflows.

Key Report Takeaways

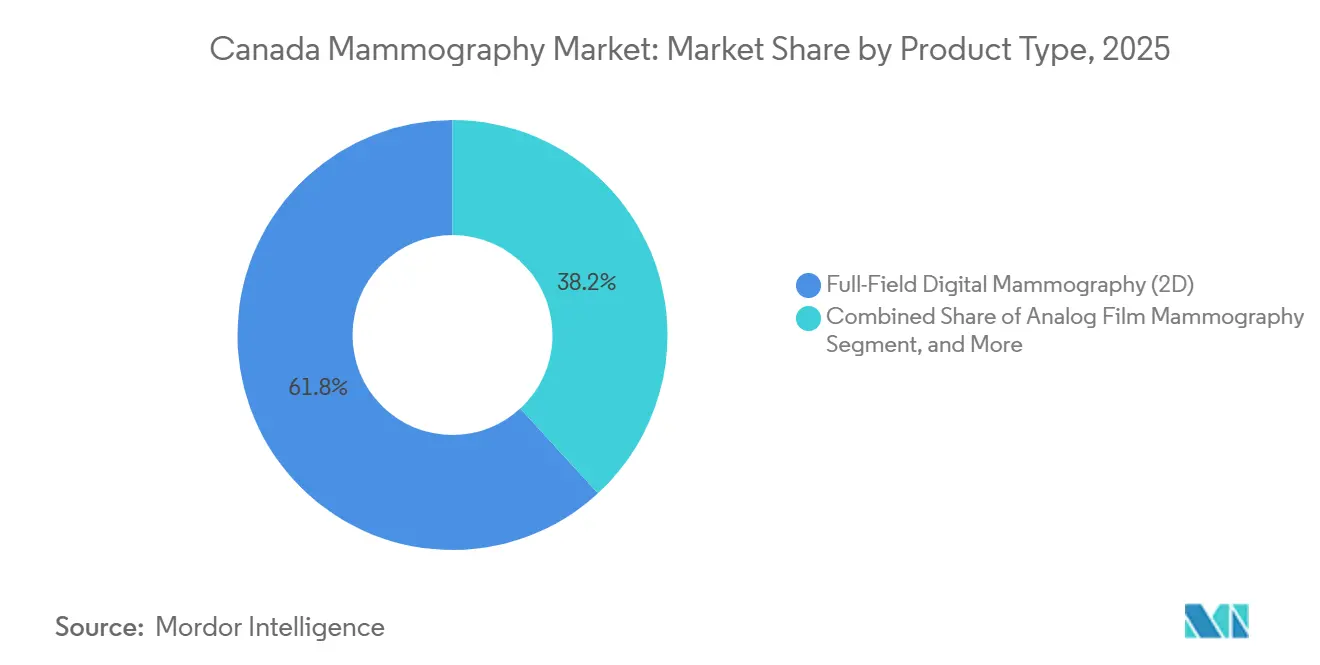

- By technology, full-field digital mammography held 61.83% of the Canada mammography market share in 2025, while AI-assisted 3D platforms are forecast to deliver a 9.78% CAGR through 2031.

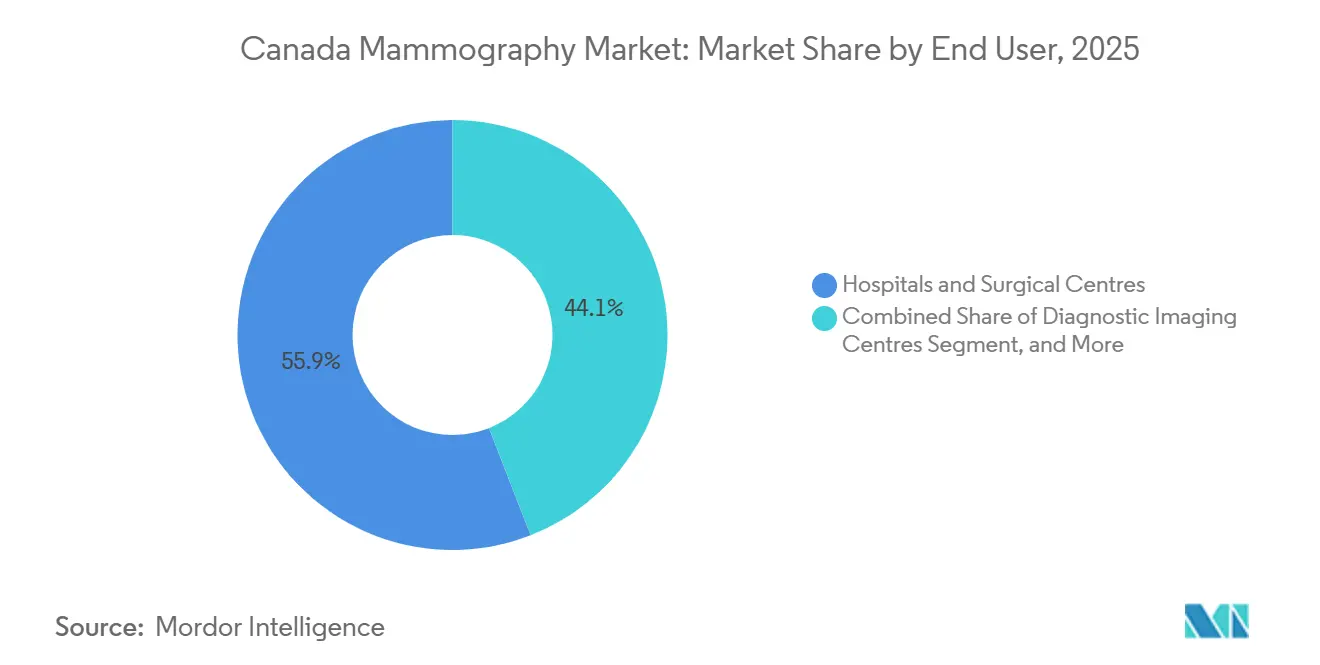

- By end user, hospitals & surgical centres captured 55.93% of the Canada mammography market size in 2025; diagnostic imaging centres are projected to expand at an 11.97% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Replacement of Aging Analog Units | +1.8% | National, concentrated in Ontario, Quebec, Alberta | Medium term (2-4 years) |

| Screening Start-Age Lowered to 40 Years | +2.1% | Six provinces, led by Ontario | Short term (≤ 2 years) |

| Federal AI Funding for Diagnostic Imaging | +1.2% | National pilots in British Columbia and Ontario | Medium term (2-4 years) |

| Bulk-Procurement Frameworks | +1.4% | Quebec, Ontario, Alberta | Short term (≤ 2 years) |

| Cloud PACS & Remote Reading Efficiencies | +0.9% | National, early in Quebec and British Columbia | Medium term (2-4 years) |

| Mobile Units for Indigenous & Rural Screens | +0.7% | Saskatchewan, Alberta, Northern Ontario, territories | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Replacement of Aging Analog Units

Hospitals that delayed digital conversions are now confronting rising service withdrawals from computed radiography hardware, forcing emergency upgrades at premium prices.[1]Institut national de santé publique du Québec, “Contrôle de la qualité des installations de mammographie,” inspq.qc.ca Quebec eliminated its last CR system in 2023, setting a precedent for other provinces to accelerate retirements. The direct-radiography shift reduces acquisition time to 5–7 minutes per exam, boosting daily throughput by 20–25%. Vendors sweeten trade-in allowances up to 30% of the list price to win multi-unit tenders, thereby reinforcing incumbent market positions. These dynamics keep the Canada mammography market on a steady modernization path.

Provincial Moves to Lower Screening Start-Age to 40 Years

Ontario, Manitoba, Saskatchewan, Newfoundland and Labrador, British Columbia, and Nova Scotia now invite average-risk women from age 40, collectively adding an estimated 1.2 million new participants.[2]Government of Canada, “Breast Cancer Screening in Average-Risk Women,” canada.ca Usage at pre-existing centers in Ontario jumped to 92% before the policy shift, so overflow studies are migrating to hospitals and private clinics. Mobile strategies in Manitoba and Saskatchewan favor geographic equity over brick-and-mortar expansions. The resulting capacity squeeze gives AI-triage tools a clear value proposition. Growth pressures, therefore, concentrate demand in the Canada mammography market’s highest-throughput segments.

Federal AI-in-Health-Care Program Funding

More than CAD 50 million in 2024-2025 grants earmark about 18% for diagnostic imaging AI.[3] BC Cancer’s CAD 1.5 million mammography study uses Health Canada–approved Genius AI Detection to cut false negatives in dense-breast populations. Provincial RFPs now stipulate algorithm sensitivity benchmarks, turning embedded AI from an optional add-on into a mandatory spec. Open-source work at the Vector Institute aims to limit bias in Indigenous and immigrant cohorts. While only about 30 radiologists hold formal AI credentials, the funding pipeline signals lasting momentum in the Canada mammography market.

Public Bulk-Procurement Frameworks

Quebec’s CAD 6.8–9.2 million dossier 6768 aggregates 158 installations, yielding double-digit price breaks and uniform 48-hour repair terms. Alberta aligned a CAD 175 million Siemens commitment with its broader oncology build-out, capitalizing on shared maintenance teams to trim lifecycle costs by up to 15%. Grouped contracts increasingly require 3D-readiness, compelling vendors to preload tomosynthesis even where reimbursement remains uncertain. Bulk deals thus accelerate specification creep and reinforce service-centric revenue models across the Canada mammography market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uneven Reimbursement for DBT and CEM | -1.3% | Ontario, Manitoba, Saskatchewan; partial in BC and Quebec | Medium term (2-4 years) |

| Shortage of CCPM-Certified Physicists | -0.8% | National, acute in Atlantic provinces and territories | Short term (≤ 2 years) |

| Fragmented EMR Integration | -0.6% | Highest in Ontario and British Columbia | Medium term (2-4 years) |

| Rising Cyber-Insurance Premiums | -0.4% | National, worst where breaches rose in 2024 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Uneven Provincial Reimbursement for DBT and CEM Modalities

Ontario still lacks a dedicated tomosynthesis fee code, burdening hospitals with an incremental CAD 44 per exam and dampening uptake despite 2.2-point recall-rate gains. Quebec reimburses at flat bilateral rates, while BC’s cost study endorsed DBT, but no schedule change followed. Private clinics charge CAD 150–300 for uncovered 3D exams, cementing a two-tier system. Until fee structures align, reimbursement drag will cap premium-platform penetration in the Canada mammography market.

Shortage of CCPM-Certified Mammography Physicists

Roughly 45 physicists are responsible for accreditation nationwide, resulting in 3- to 6-month waitlists for new-unit certification. Quebec recorded seven temporary service suspensions in 2024 due to inspectors being unavailable. Retirement-driven attrition exceeds new graduates, and private-clinic wage premiums worsen public-sector gaps. Accreditation delays, therefore, slow capital deployment and temper growth expectations for the Canadian mammography market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: AI Platforms Extend Digital Leadership

Full-Field Digital Mammography owned 61.83% of the Canada mammography market share in 2025, benefiting from reimbursement certainty and PACS compatibility. AI-assisted 3D systems are projected to log a 9.78% CAGR through 2031, lifted by Health Canada's 2024 clearance of Genius AI Detection and a 15–20% drop in radiologist reading time. Digital Breast Tomosynthesis occupies a clinical sweet-spot but remains fee-code-constrained in several provinces.

Hospital buyers in centralized provinces have begun specifying 3D-readiness as the default, whereas in decentralized jurisdictions, units are still procured as cost-optimized 2D units, with upgrades planned later. Saskatchewan’s mobile units illustrate a throughput-first mindset, prioritizing direct radiography and satellite transfer over complex 3D stacks. As a result, the Canada mammography market size for AI-enabled 3D equipment will accelerate once fee schedules catch up, but near-term volume remains anchored in 2D replacements.

By End User: Private Centers Soak Up Public Backlogs

Hospitals & Surgical Centres retained 55.93% of the Canada mammography market size in 2025 because they host most provincial screening programs and provide same-day diagnostic work-ups. Diagnostic Imaging Centres, however, are poised for an 11.97% CAGR as private operators monetize wait-list spillover and bundle tomosynthesis as a self-pay upgrade.

Urban regions see 8 to 10 new private sites each year, while low-density provinces rely on mobile fleets that cut fixed-site costs by roughly 70%. Private-equity-backed Canada Diagnostic Centres accelerated acquisitions across the Prairies in 2024-2025, confirming investor appetite for diversified outpatient imaging. With screening eligibility widened to age 40, diagnostic volumes keep climbing, ensuring that every end-user segment feeds growth in the Canada mammography market.

Geography Analysis

Ontario added 800,000 newly eligible women after its April 2024 age change, yet still lacks a DBT code, forcing hospitals to absorb CAD 44 extra per 3D exam and dampening adoption. Quebec’s centralized tender compressed unit prices by up to 20% and mandates tomosynthesis readiness, illustrating how procurement power shapes capital cycles. British Columbia’s dense-breast program exerts additional load on radiologist capacity, boosting AI triage demand.

Saskatchewan and Manitoba emphasize mobile screening to close rural gaps; Saskatchewan’s first two units exceeded utilization forecasts by 28% in their debut month. Atlantic provinces suffer acute physicist shortages, stretching commissioning delays beyond six months. Northern territories rely almost exclusively on visiting units funded through Indigenous Services Canada programs.

Sectra’s province-wide archive now links more than 60 Quebec sites, while OCINet processes 16 million annual images in Ontario, reducing critical-case time-to-read by more than half. Cross-border interoperability remains limited, obliging patients transferred out of province to undergo repeat scans. These provincial contrasts reinforce a multi-speed landscape within the Canadian mammography market.

Competitive Landscape

Hologic, GE HealthCare, and Siemens Healthineers together control a majority of installed systems, leveraging nationwide service footprints to win long-term managed-equipment contracts. Hamilton Health Sciences’ 15-year, CAD 270 million deal with Siemens exemplifies a risk-transfer model that smaller hospitals now emulate.

Emerging players target white-space niches. RamSoft’s cloud PACS undercuts legacy on-premise costs by up to 40%, appealing to new private centers. Mobile manufacturers that integrate satellite transfer gain traction as provinces back rural screening vans. Cybersecurity has become a buying criterion after average breach costs reached CAD 6.32 million in 2024, giving vendors with built-in zero-trust frameworks a procurement edge.

Grouped-purchase tenders tighten entry barriers for small manufacturers lacking pan-Canadian service. As procurement shifts to bundled service economics, incumbents strengthen lock-in, sustaining moderate concentration inside the Canada mammography market.

Canada Mammography Industry Leaders

Hologic Inc.

Planmed OY

GE HealthCare Technologies Inc.

Fujifilm Holdings Corporation

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: iCAD and RamSoft formed a preferred distribution pact integrating the ProFound AI Breast Health Suite into RamSoft’s cloud RIS/PACS across North America.

- April 2024: Bayer and Hologic unveiled a coordinated contrast-enhanced mammography solution at the Society of Breast Imaging Symposium in Montreal.

Canada Mammography Market Report Scope

Mammography is a standard diagnostic and screening technique used to evaluate breast tissue for the presence of a malignant tumor. The process uses low-energy X-rays to detect breast cancer early.

The Canada Mammography Market Report is Segmented by Technology (Analog Film Mammography, Full-Field Digital Mammography (2D), Digital Breast Tomosynthesis (3D), Contrast-Enhanced Spectral Mammography, AI-Assisted 3D Mammography Platforms) and End User (Hospitals & Surgical Centres, Dedicated Breast Screening Centres, Diagnostic Imaging Centres, Mobile Screening Units, Ambulatory Care & Specialty Clinics). The Market Forecasts are Provided in Terms of Value (USD).

By Technology

| Analog Film Mammography |

| Full-Field Digital Mammography (2D) |

| Digital Breast Tomosynthesis (3D) |

| Contrast-Enhanced Spectral Mammography |

| AI-Assisted 3D Mammography Platforms |

By End User

| Hospitals & Surgical Centres |

| Dedicated Breast Screening Centres |

| Diagnostic Imaging Centres |

| Mobile Screening Units |

| Ambulatory Care & Specialty Clinics |

| By Technology | Analog Film Mammography |

| Full-Field Digital Mammography (2D) | |

| Digital Breast Tomosynthesis (3D) | |

| Contrast-Enhanced Spectral Mammography | |

| AI-Assisted 3D Mammography Platforms | |

| By End User | Hospitals & Surgical Centres |

| Dedicated Breast Screening Centres | |

| Diagnostic Imaging Centres | |

| Mobile Screening Units | |

| Ambulatory Care & Specialty Clinics |

Key Questions Answered in the Report

How fast is Canada’s mammography segment expected to grow through 2031?

The market is forecast to climb from USD 0.12 billion in 2026 to USD 0.18 billion by 2031, reflecting a 7.91% CAGR over 2026-2031.

Which provinces lowered the routine breast-screening start age to 40?

Ontario, Manitoba, Saskatchewan, Newfoundland and Labrador, British Columbia and Nova Scotia implemented the age-40 threshold during 2024-2025.

What share of systems did 2D digital mammography hold in 2025?

Full-Field Digital Mammography accounted for 61.83% of installed value in 2025.

How are mobile units addressing rural and Indigenous screening gaps?

Provinces such as Saskatchewan fund direct-radiography vans with satellite image transfer; Saskatchewan’s first two units logged 340 exams in four weeks—28% above projection—by rotating through 42 communities.

Why are AI-assisted 3D platforms gaining traction?

Health Canada’s 2024 clearance of Genius AI Detection and provincial RFPs that now demand embedded algorithms are pushing hospitals toward 3D systems that cut reading time by around 15-20%.

Page last updated on: