Breast Implants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

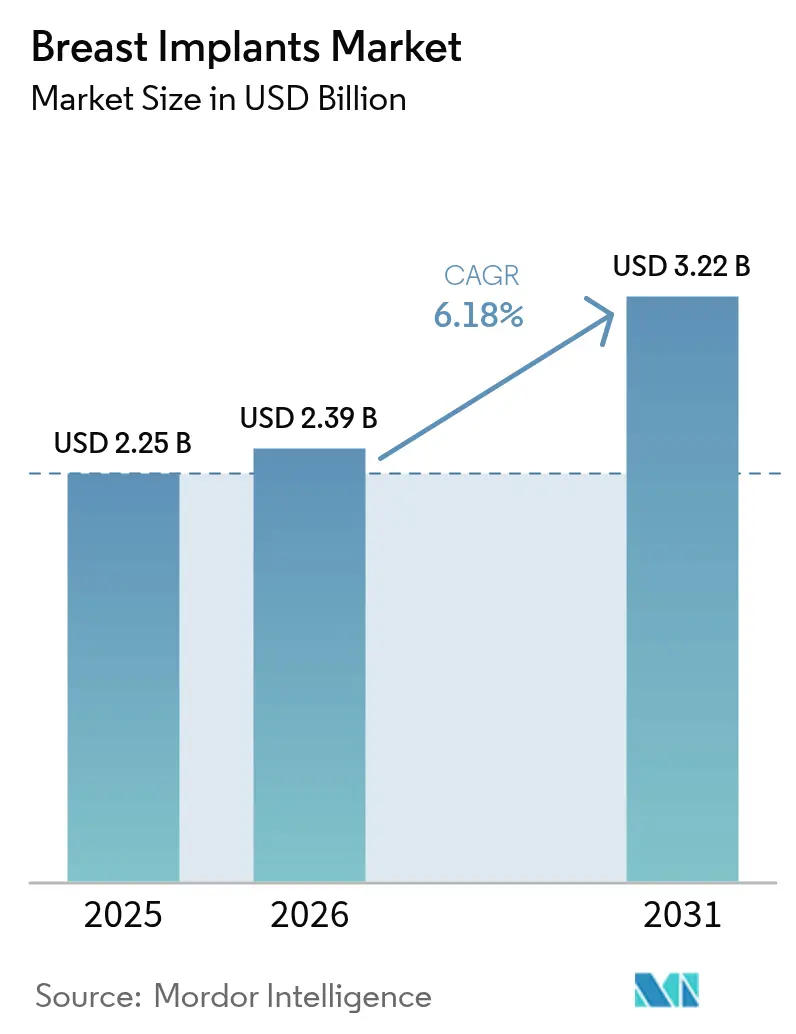

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 3.22 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

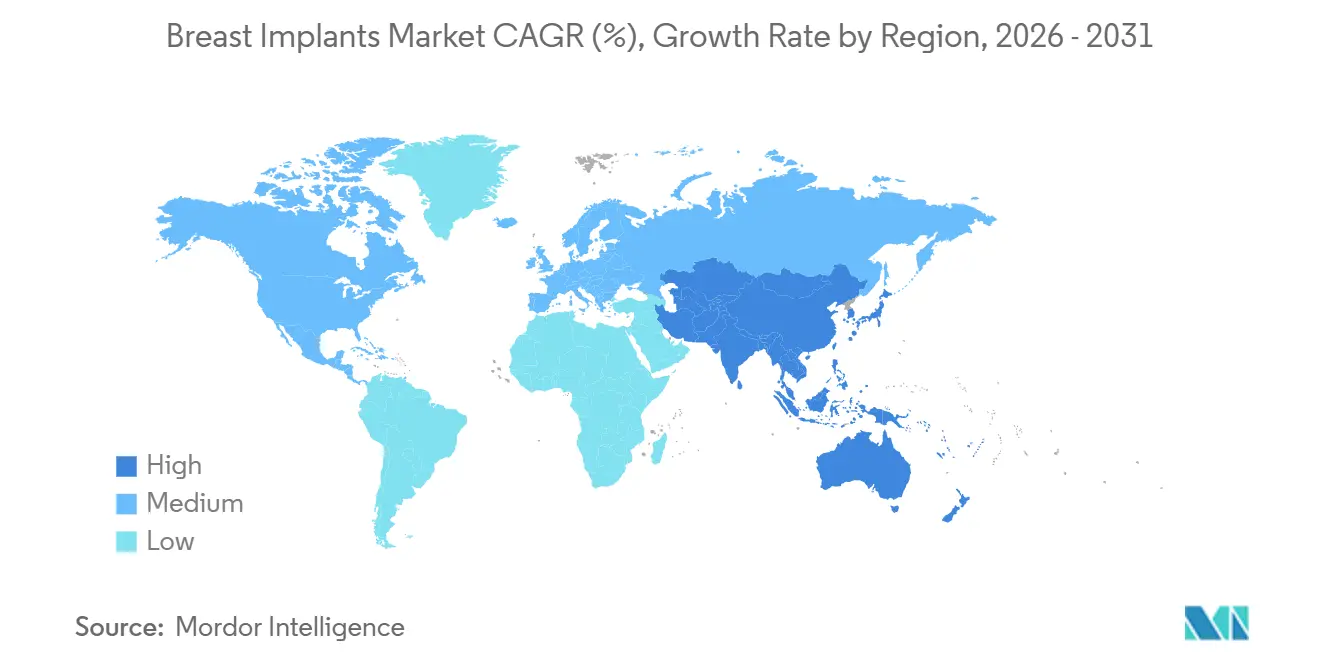

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Implants Market Analysis by Mordor Intelligence

The Breast Implants Market size is projected to be USD 2.25 billion in 2025, USD 2.39 billion in 2026, and reach USD 3.22 billion by 2031, growing at a CAGR of 6.18% from 2026 to 2031.

The expansion reflects a combination of rising post-mastectomy reconstruction volumes, wider social acceptance of cosmetic augmentation, and rapid product innovation. Silicone devices continue to dominate overall unit demand, but structured saline implants are gaining momentum because they eliminate silent-rupture concerns while offering a silicone-like feel. Across regions, Asia Pacific is the fastest-growing arena, powered by medical tourism hubs, accelerating middle-class spending, and a surge of new approvals, whereas North America maintains its leadership position through mature reimbursement pathways and advanced surgeon expertise. Heightened geopolitical disruptions have exposed raw-material vulnerabilities, prompting manufacturers to earmark 3-5% of annual revenue for supply-chain resiliency, contract flexibility, and dual-sourcing strategies.

Key Report Takeaways

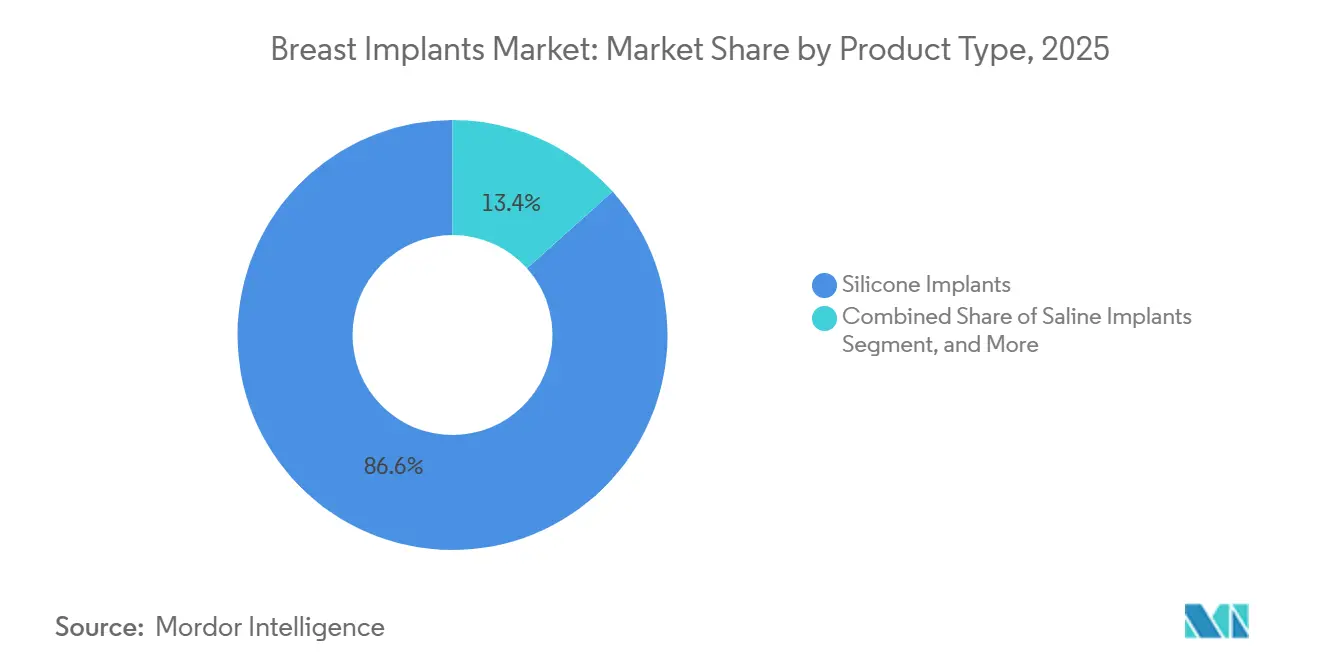

- By product type: silicone implants captured 86.62% of the breast implants market share in 2025, while structured saline devices are forecast to record a 7.34% CAGR through 2031.

- By shape, round profiles accounted for 82.88% of the breast implant market in 2025; anatomical (teardrop) options are projected to grow at a 6.54% CAGR over the same period.

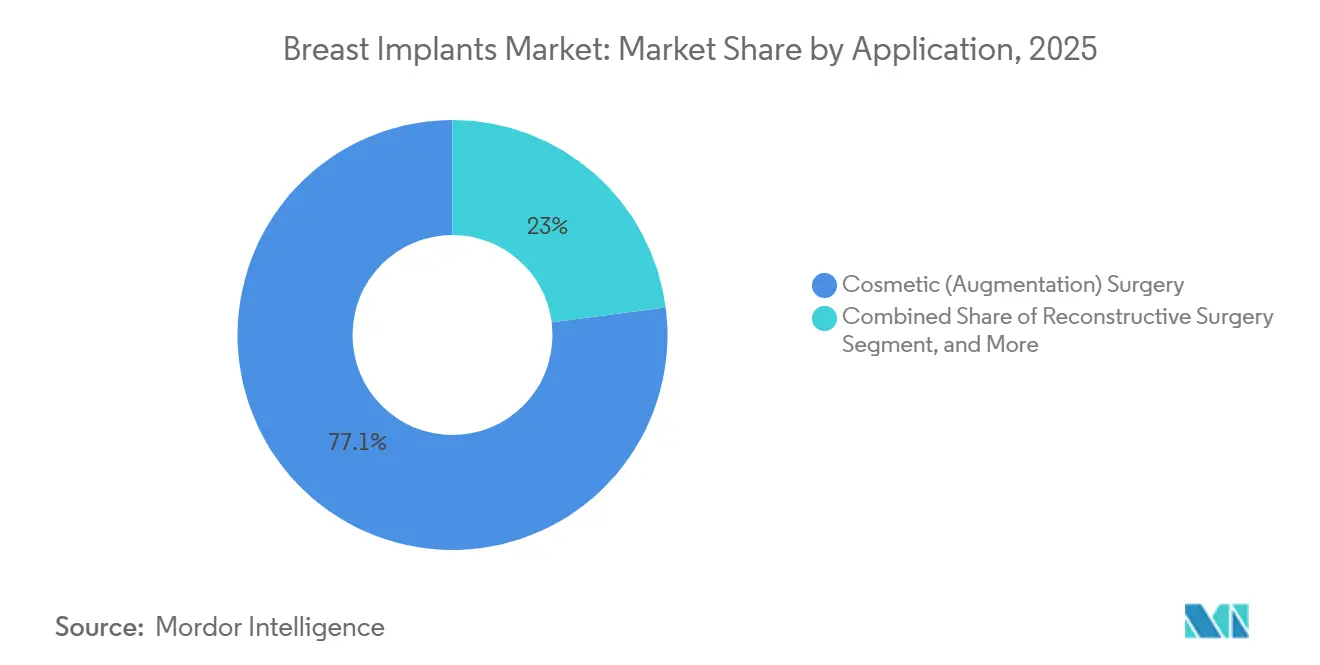

- By application, cosmetic uses accounted for 77.05% of the breast implants market in 2025 and are set to grow at a 6.71% CAGR by 2031.

- By end user, ASCs held 43.62% of the breast implants market in 2025, but cosmetology clinics and medical spas are anticipated to grow at a 6.86% CAGR through 2031.

- By geography, North America captured 40.68% of the breast implants market share in 2025; Asia Pacific is forecast to accelerate at a 7.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breast Implants Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High burden of breast cancer | +1.2% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Surge in demand for breast surgery | +1.4% | Global, led by North America, Asia-Pacific, Latin America | Medium term (2-4 years) |

| Technological advancement in breast implants | +0.9% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| 3-D imaging & simulation tools raising patient conversion rates | +0.7% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Rise in medical tourism for breast surgeries coupled with increased awareness | +1.1% | Asia-Pacific core, Latin America, Middle East | Medium term (2-4 years) |

| Accelerating adoption of advanced implants and direct-to-consumer marketing | +0.8% | Global, strongest in North America and urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Burden of Breast Cancer

New invasive cancer diagnoses in the United States are expected to reach 316,950 in 2025, a 2% increase from 2024, reinforcing sustained reconstruction demand.[1]American Cancer Society, “Cancer Facts & Figures 2025,” American Cancer Society, cancer.org Global breast cancer cases are increasing steadily, with projections indicating a rise from 2.3 million cases in 2020 to 3 million by 2040. However, immediate reconstruction remains underutilized, with 162,579 reconstructions performed in 2024, significantly fewer than mastectomies, particularly in rural areas compared to metropolitan regions. Broader payer coverage, advancements in prepectoral techniques, and the growing adoption of direct-to-implant pathways, now accounting for 25% of all reconstructions, are helping to address this disparity. As these systemic barriers are reduced, the previously unmet demand is expected to drive growth in the breast implant market volumes.

Surge in Demand for Breast Surgery

Consumer preference has shifted toward “undetectable” augmentations that mirror natural breast aesthetics. Motiva’s SmoothSilk shell and similarly advanced textures reduce capsular-contracture incidence, capturing surgeon endorsement. Simultaneously, breast-lift procedures rose 6% in the United States in 2024, supported by advances in skin-tightening technology. In 2024, cosmetic augmentation procedures in the United States increased to 306,196, continuing a decade-long upward trend. Individuals aged 18-35 account for 42% of these cases, a demographic heavily influenced by social media and demonstrating limited price sensitivity. Globally, medical tourism significantly contributes to this growth. For example, Turkey performed over 553,000 aesthetic surgeries in 2023, with breast procedures comprising 18%. Additionally, 42% of United States augmentations now occur in office-based operating rooms. This shift reflects a transition away from traditional hospital settings, enabling providers to grow in lower-cost, higher-margin environments. Collectively, these factors drive the expansion of the breast implant market.

Technological advancement in breast implants

Structured implants such as the IDEAL IMPLANT combine baffle chambers with saline fill, leading to a 92.7% satisfaction rate after 10 years and capsular-contracture rates of 6.6%, markedly below silicone norms.[2]William P. Nichter, “Ten-Year Outcomes of IDEAL IMPLANT Structured Saline Breast Implants,” Plastic and Reconstructive Surgery, pubmed.ncbi.nlm.nih.gov Lightweight variants like POLYTECH’s B-Lite shrink overall implant mass by 30%. 3-piece RFID chips now facilitate non-invasive serial-number checks, bolstering post-market surveillance and warranty validation. In September 2024, the FDA approved Motiva implants, which now feature radio-frequency identification (RFID) chips. This advancement enables lifelong traceability, representing a significant breakthrough for registries and surveillance. Three-year data indicate a 0.5% rate of capsular contracture and a 0.6% rupture rate, both outperforming traditional standards. In December 2024, Mentor received FDA clearance for its MemoryGel Enhance, expanding the volume range to 1,445 cc to address the growing demand for revision surgeries. Investigational bioabsorbable scaffolds, such as BellaSeno’s silk-fibroin matrix and CEREPLAS’s polycaprolactone structure, demonstrated promising tissue ingrowth over 12 months. This shift toward advanced material science is evident, although commercialization is expected beyond 2028. These innovation cycles support premium pricing strategies and drive interest from new patient segments in the breast implant market.

3-D Imaging & Simulation Tools Raising Patient Conversion Rates

By 2024, 68% of United States plastic-surgery practices had adopted three-dimensional consultation platforms, up from 42% in 2020. Practices implementing these systems reported a 23% increase in consultation-to-procedure conversions and a 31% decline in early revision requests. Consumer-facing applications, such as Allergan’s Natrelle Visualizer, achieved over 1.2 million downloads in 2024, enabling patients to preview surgical outcomes from their homes. The integration of artificial intelligence to predict optimal implant sizes has enhanced decision-making confidence, streamlined the sales cycle, and improved operational efficiency for surgeons, driving growth in the breast implant market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Post complications and risks associated with breast implant | -0.8% | Global, heightened scrutiny in North America and Europe | Long term (≥ 4 years) |

| Supply shortages for medical grade material | -0.5% | Global, acute in Asia-Pacific hubs | Short term (≤ 2 years) |

| Stringent regulations and availability of alternatives | -0.6% | North America and Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Rise in product-liability insurance premiums for surgeons | -0.4% | North America, spill-over Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post Complications and Risks Associated with Breast Implant

Global reporting registers 1,290 confirmed BIA-ALCL cases, mostly linked to textured shells.[3]U.S. Food and Drug Administration, “Breast Implant Premarket Approvals,” fda.gov In 2024 the FDA mandated boxed warnings and patient checklists, elevating compliance costs yet encouraging transparent risk discussion. Smooth-surface implants and nanotexturing techniques address these concerns, but litigation trends are elevating surgeon insurance premiums; in some U.S. states, premiums rose 15% year-over-year in 2024. Key challenges in the breast implant market include capsular contracture, rupture, and the rare breast-implant-associated anaplastic large-cell lymphoma (BIA-ALCL). Sientra’s six-year post-approval study reported a 4.1% incidence of grade III/IV contracture and an 11.6% reoperation rate among recipients. These figures align with industry averages but highlight a persistent risk. The 2019 BIOCELL recall, which targeted macro-textured lines, was a significant industry event. As of 2024, the FDA had recorded over 1,290 reports of BIA-ALCL, with more than 900 cases linked to Allergan. Further increasing caution among surgeons, new FDA safety notices in 2024 linked textured implants to additional lymphoma cases. In response, some practitioners are transitioning to smooth or saline devices, which is tempering growth in specific segments of the breast implant market.

Supply Shortages for Medical Grade Material

In 2024, competition among semiconductor manufacturers for the same chemical feedstock doubled lead times for medical-grade silicone to 16 weeks. Consequently, spot prices increased by 15-25%. Adding to the challenges, Chinese export restrictions on catalyst metals and gas curtailments in Europe further tightened the market. Smaller OEMs faced significant difficulties, with Sientra citing raw-material shortages as a factor contributing to its bankruptcy. While supply chains began to stabilize, the situation highlighted structural vulnerabilities, resulting in modest price inflation in the breast implant market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Silicone Dominance Masks Saline Revival

Silicone implants retained an 86.62% share of the breast implant market in 2025, favored for their cohesive-gel stability and soft-tissue mimicry. The breast implant market size for silicone lines will continue to expand; however, structured saline’s 7.34% CAGR indicates accelerating uptake. Structured devices avoid MRI monitoring, appeal to safety-conscious consumers, and allow intra-operative fill adjustment to refine symmetry. Gummy-bear cohesive implants still appeal through shape memory and lower leak risk, but structured saline’s transparent rupture profile garners support among revision-surgery candidates.

Silicone implant manufacturers respond with warranty extensions covering capsule contracture and rupture replacement for the implant’s lifetime. Digital breast sizers that overlay 3-D imaging onto patient anatomy improve pre-procedure planning, further reinforcing silicone incumbency despite saline’s momentum in the breast implant market.

By Shape: Anatomical Gains Ground as Prepectoral Placement Rises

Round implants accounted for 82.88% of the breast implant market in 2025, yet anatomical units will grow more rapidly due to a significantly lower capsular contracture rate of 3.4% vs. 11.3% for rounds. East Asian and European patients, who often prefer a modest upper-pole projection, gravitate toward teardrop geometrics. Smooth-surface anatomical models launched in 2025 tackle historical rotation concerns, aided by laser-etched texturing that stabilizes pocket positioning without aggressive roughness linked to ALCL risk.

Hybrid gel-fill patents blend dual-viscosity layers- a firmer base for shape and a softer outer layer for palpability, allowing anatomical implants to compete with rounds on tactile authenticity. Promotional campaigns highlight these innovations, propelling surgeon adoption and nudging market share toward anatomical categories.

By Application: Cosmetic Augmentation Sustains Lead Despite Reconstructive Momentum

In 2025, cosmetic indications accounted for 77.05% of the breast implants market, and are predicted to rise at a 6.71% CAGR through 2031. Within cosmetic demand, augmentation-mastopexy procedures (simultaneous lift and augmentation) are increasing, fueled by the broad adoption of GLP-1 weight-loss medications that accentuate deflation in breast envelopes. Vendors that supply smaller-volume, low-profile implants rank well for these nuanced corrections, sharpening competitive segmentation within the breast implants market.

The driving factors of the reconstructive surgery segment include earlier detection, national screening programs, and financially accessible mastectomy coverage. Immediate breast reconstruction garners surgeon preference due to its single-stage operative workflow, despite a recognized 18% increase in revision risk compared with delayed approaches. Prepectoral placement techniques improve postoperative comfort and maintain pectoralis muscle integrity, though they slightly increase seroma incidence. Device makers have responded with fenestrated meshes that facilitate fluid drainage and integrate with host tissue.

By End User: Medical Spas Emerge as Fastest-Growing Channel

ASCs commanded a 43.62% share of the breast implant market in 2025, driven by expanding operating room capacity. Cosmetology clinics and medical spas, however, are expected to grow at a 6.86% CAGR to 2031. Patients appreciate extended office hours, boutique recovery lounges, and bundled aesthetic offerings (e.g., dermal fillers). Manufacturers deploy “practice-builder” toolkits that cover online booking engines, social media content calendars, and staff-training modules to embed product loyalty. Clinics using Allergan’s Natrelle line, for instance, receive conversion-optimized patient-education videos alongside inventory replenishment discounts.

Hospitals, despite having a lower share, counter by establishing dedicated aesthetic suites and leveraging cross-specialty consults, such as combining prophylactic mastectomy with reconstructive augmentation during the same inpatient stay. Integrated electronic medical record systems enable seamless oncology-to-plastic surgery referrals, helping hospitals defend their share within the evolving breast implant market.

Geography Analysis

North America maintained a 40.68% share of the breast implants market in 2025. The FDA’s September 2024 approval of Motiva SmoothSilk introduced the first non-textured nano-surface implant in the United States, intensifying device choice competition. Regulatory updates impose black-box warnings on all implants and require patient decision checklists, fostering informed choice yet adding administrative overhead for providers. U.S. surgeons exhibit distinctive practice patterns, often selecting higher-projection implants relative to their European peers, reflecting regional aesthetic ideals.

Asia Pacific is forecast to be the fastest-growing region at a 7.48% CAGR to 2031. Medical-tourism corridors funnel thousands of patients annually into Thailand and South Korea for cut-price augmentations bundled with post-operative spa care. China’s NMPA authorization of Motiva implants in late 2024-China’s first breast-implant clearance in a decade-unleashes pent-up demand among private-clinic networks. Australia’s clinical trials of PCL scaffold-based, fully resorbable implants reported zero major complications at 12-month follow-up, indicating a pipeline of alternatives that could eventually disrupt silicone incumbency. In Indonesia, outbound medical tourism remains prevalent because of limited specialist availability, revealing regional service-capacity gaps that international clinic chains aim to fill.

Europe accounts for a substantial slice of global sales but confronts stricter regulation. The Medical Device Regulation (MDR) compels breast-implant recertification by 2027, and GC Aesthetics met the milestone early by launching the first MDR-approved implant in 2022 gcaesthetics.com. The U.K. tallied 5,202 cosmetic breast procedures in 2024, representing a 6% increase in aesthetic demand despite macroeconomic headwinds. Textured-implant recall aftermath lingers, nudging surgeons toward smooth or micro-textured alternatives. Meanwhile, insurers in Germany and France expanding reimbursement for prophylactic mastectomy with immediate reconstruction support reconstructive volume growth.

Mordor Intelligence provides coverage of the breast implants market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The breast implants market exhibits moderate concentration. AbbVie’s Natrelle, Johnson & Johnson’s Mentor, and Establishment Labs hold global scale, while POLYTECH, GC Aesthetics, and Silimed serve regional niches. Innovation pipelines concentrate on surface engineering. Mentor’s SPECTRUM Adjustable Saline system permits postoperative size tweaks for six months, affording patients greater personalization. POLYTECH’s Opticon Plus i2024 launch layers multi-density cohesive gels, tailoring projection to individual chest widths. Lightweight constructs that reduce strain on pectoral ligaments appeal to physically active populations and older patients concerned about long-term ptosis.

Environmental sustainability forms an emerging competitive axis. A recent academic review quantified greenhouse gas intensity at 4.25 MTCO2e per USD 1 million in revenue for one major manufacturer, half that of a rival, granting procurement advantage to hospital systems that factor ESG performance into their decisions. Blockchain-enabled supply systems enable cradle-to-grave traceability, satisfying MDR provenance mandates and supporting circular-economy initiatives, such as retrieval-and-recycling schemes for removed implants.

M&A activity continues. Tiger Aesthetics Medical purchased Sientra’s breast-implant assets for USD 42.5 million in April 2024, safeguarding continuity of supply for Sientra’s existing customer base. Analysts anticipate further consolidation as MDR costs squeeze smaller brands. Venture-capital interest shifts toward bio-resorbable implants and AI-based sizing tools that combine chest-wall morphometry with machine-learning prediction of tissue dynamics.

Breast Implants Industry Leaders

AbbVie Inc. (Allergan Aesthetics)

GC Aesthetics

HansBiomed Co. Ltd.

Johnson & Johnson Services, Inc.

Establishment Labs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Allergan Aesthetics launched the Faces of Natrelle testimonial program to crowdsource patient stories and strengthen community outreach.

- February 2026: Applied Medical Technology, Inc. (AMT) has introduced the Explant Express to the U.S. market. This innovative device is engineered to streamline the removal of ruptured breast implants during explant and revision procedures.

- October 2025: Allergan Aesthetics secured supplier status with Vizient, linking Natrelle implants to more than half of United States healthcare organizations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global breast implant market as all factory-made silicone, cohesive-gel, form-stable, and saline devices that surgeons permanently place for cosmetic augmentation or post-mastectomy reconstruction and that are sold through hospitals, ambulatory surgery centers, and accredited cosmetic clinics.

Scope Exclusions: Tissue expanders, acellular dermal matrices, fat-graft kits, external breast prostheses, and revision accessories are deliberately left outside the sizing.

Segmentation Overview

- By Product Type

- Silicone Implants

- Cohesive Gel / Form-Stable Implants

- Saline Implants

- Structured Saline Implants

- Hydrogel & Other Novel Fillers

- By Shape

- Round

- Anatomical

- Hybrid Adjustable

- By Application

- Reconstructive Surgery

- Cosmetic (Augmentation) Surgery

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Cosmetology Clinics & Medical Spas

- Physician-Owned Office-Based ORs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts hold structured interviews with plastic surgeons, distributor managers, and hospital buyers across North America, Europe, Brazil, and key Asia-Pacific markets.

These conversations confirm real selling prices, revision ratios, and adoption barriers that documents alone cannot capture, letting us triangulate assumptions with front-line reality.

Desk Research

We begin with high-credibility public data, US FDA 510(k) approvals, CE-MDR listings, HS-code 902190 customs flows, GLOBOCAN cancer incidence, and annual procedure counts from the American Society of Plastic Surgeons and ISAPS.

Company 10-Ks, investor decks, and respected journals such as Plastic and Reconstructive Surgery enrich technology and pricing insight.

Where deeper firm-level intelligence is required, analysts access D&B Hoovers and Dow Jones Factiva.

The sources cited here are illustrative; numerous additional open and paid references inform data gathering, validation, and clarification.

Market-Sizing & Forecasting

A top-down build links country-level augmentation and reconstruction procedure counts to average implants per surgery, then prices them with region-specific ASP curves.

Select bottom-up checks, sampled manufacturer revenue roll-ups and channel inventory sweeps, calibrate totals.

Variables woven into the model include silicone penetration, regulatory approval cadence, elective-surgery deferral rates, currency shifts, and device recalls.

A multivariate regression, run under conservative, base, and optimistic scenarios, extends the view through 2030 while handling gaps where granular shipment data are unavailable.

Data Validation & Update Cycle

Outputs pass two analyst reviews; anomalies trigger rapid callbacks with primary contacts and cross-checks against import datasets.

Reports refresh annually, and mid-cycle updates follow major recalls or policy moves so clients receive the latest view.

Why Mordor's Breast Implant Baseline Commands Reliability

Published figures often diverge because providers mix device baskets, apply uniform global prices, or retain pre-COVID baselines.

By anchoring estimates to verified surgery volumes and live ASP feedback, our baseline stays close to operating-room reality.

Key gap drivers include some publishers folding tissue expanders and biomaterials into the same pool, others applying single-region prices worldwide, and a few ignoring the lingering elective-procedure lag seen post-pandemic.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.25 B | Mordor Intelligence | - |

| USD 2.89 B | Global Consultancy A | Includes expanders and adjunct biomaterials; uses blended ASP across regions |

| USD 3.49 B (2024) | Trade Journal B | Counts premium procedure fees and accessories; older baseline and no elective-surgery lag adjustment |

Years shown reflect each publisher's latest publicly available base. The comparison underscores that Mordor's disciplined scope, variable selection, and yearly refresh give decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current size of the breast implants market and what growth rate is expected?

The market stands at USD 2.39 billion in 2026 and is forecast to reach USD 3.22 billion by 2031, reflecting a 6.18% CAGR

Which implant material holds the leading market share?

Silicone devices led with 86.62% of the breast implants market share in 2025, driven by their cohesive-gel stability and natural feel.

Why is Asia Pacific projected to be the fastest-growing region?

Rising medical tourism, expanding middle-class spending, and recent product approvals position Asia Pacific to advance at a 7.48% CAGR through 2031.

How are new regulations influencing the market?

In the United States, the FDA now mandates boxed warnings and patient decision checklists, while Europe’s Medical Device Regulation requires full implant recertification by 2027, raising compliance costs but enhancing patient safety

What supply-chain challenges do manufacturers face?

Geopolitical disruptions and silicone feedstock shortages have pushed companies to allocate 3-5% of annual revenue to resiliency measures such as dual sourcing and regional warehousing

Which technological advances are shaping next-generation implants?

Structured saline designs that allow visible rupture detection, lightweight gel matrices that cut implant weight by 30%, and RFID-enabled shells for non-invasive device tracking are redefining product differentiation.

Page last updated on: