Breast Biopsy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

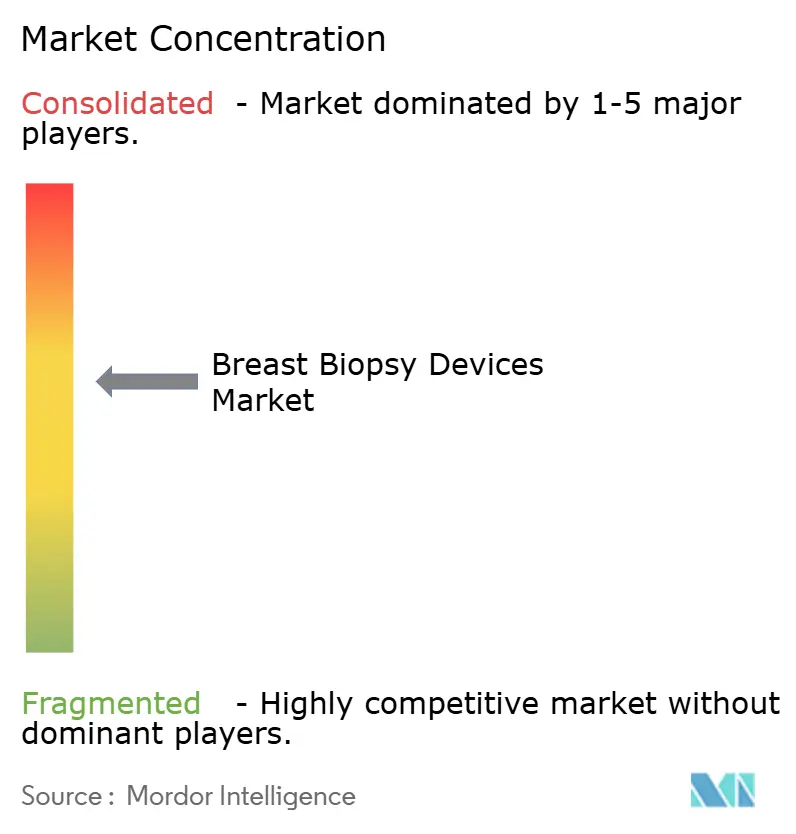

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Biopsy Devices Market Analysis by Mordor Intelligence

The breast biopsy devices market size is expected to grow from USD 1.29 billion in 2025 to USD 1.35 billion in 2026 and is forecast to reach USD 1.72 billion by 2031 at 4.95% CAGR over 2026-2031. Demand rises as health systems move from traditional tissue sampling toward AI-enabled, image-guided precision diagnostics that shorten procedure time and improve lesion targeting. Higher breast-cancer incidence among women under 55 and broader screening access in emerging economies heighten the need for minimally invasive sampling. Vacuum-assisted platforms gain traction because they deliver larger cores with fewer passes, while liquid-based techniques open a pathway to real-time molecular profiling that guides targeted therapy. Together, shifting clinical guidelines, growing reimbursement for percutaneous approaches and the rollout of AI-driven 3-D imaging keep the breast biopsy devices market on a steady growth trajectory.

Key Report Takeaways

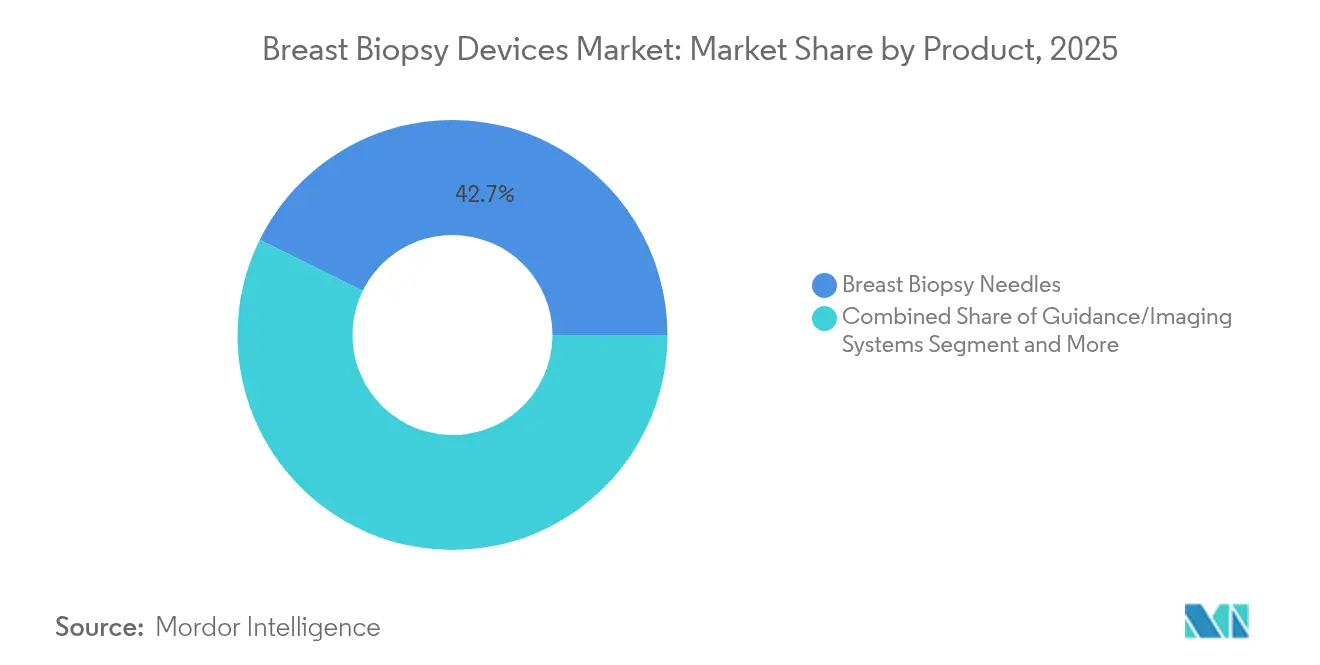

- By product category, breast-biopsy needles led with 42.70% of breast biopsy devices market share in 2025; guidance and imaging systems are projected to expand at a 9.85% CAGR to 2031.

- By procedure, vacuum-assisted biopsy held 35.10% revenue share in 2025, while fine-needle aspiration biopsy records the highest projected CAGR at 9.05% through 2031.

- By technique, image-guided sampling captured 68.10% of the breast biopsy devices market size in 2025 and liquid biopsy is advancing at a 10.15% CAGR through 2031.

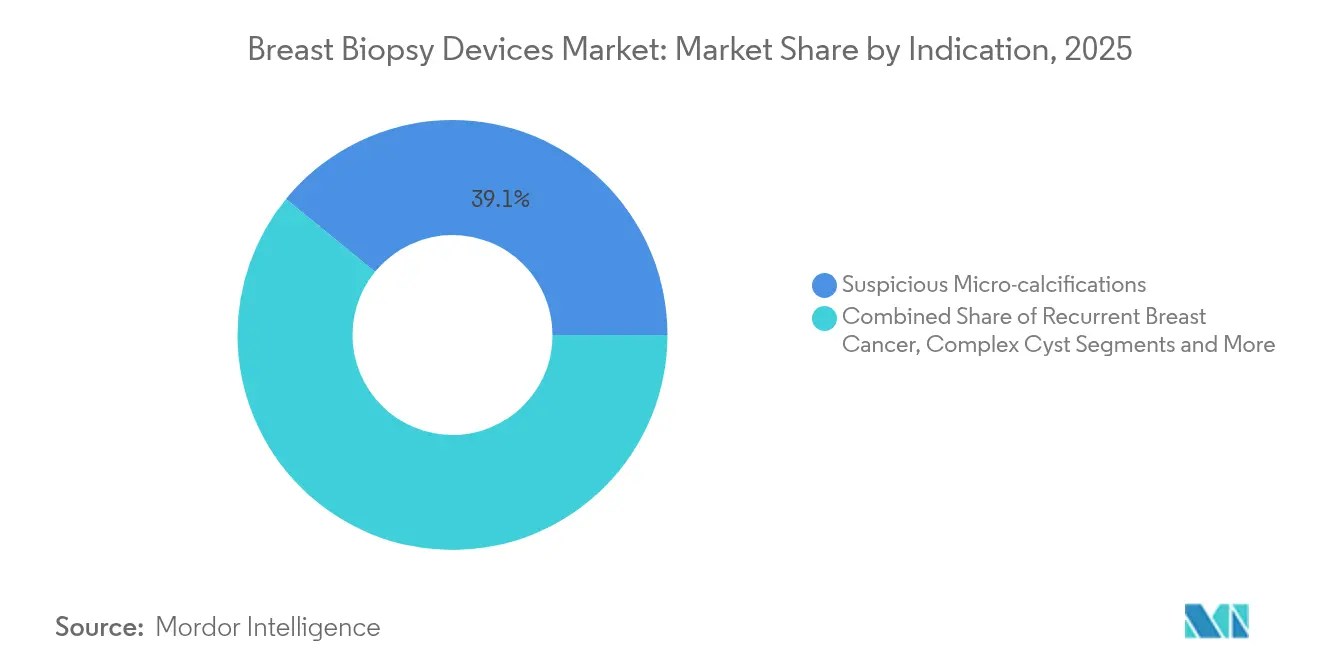

- By indication, suspicious microcalcifications accounted for 39.10% share of the breast biopsy devices market size in 2025, whereas recurrent breast cancer is tracking an 11.05% CAGR to 2031.

- By end user, hospitals and clinics held 52.30% revenue share in 2025; independent diagnostic centers are set to grow fastest at 9.20% CAGR through 2031.

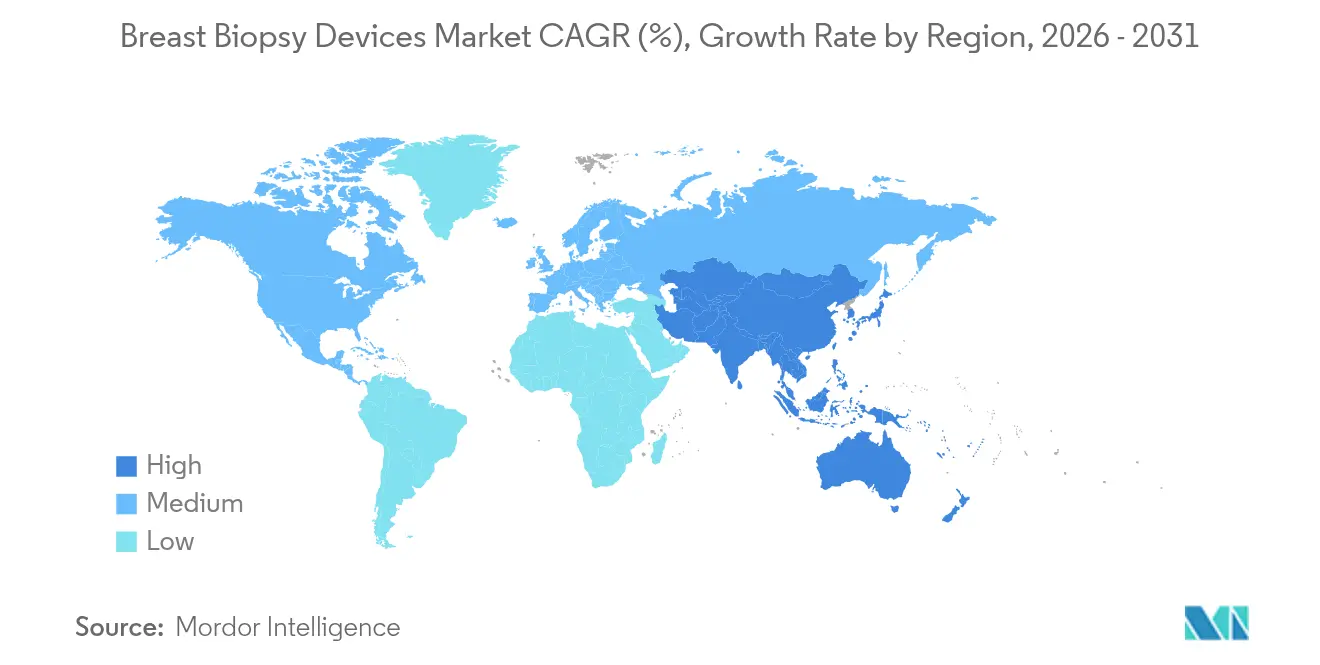

- By geography, North America commanded 42.30% share of the breast biopsy devices market in 2025, while Asia-Pacific posts the highest 9.35% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breast Biopsy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence & awareness of breast cancer | +1.8% | Global, strongest in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Expanding reimbursement for image-guided biopsies | +1.2% | North America and Europe, extending into Asia-Pacific | Short term (≤ 2 years) |

| Accelerating shift toward vacuum-assisted systems | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| AI-enabled 3-D imaging and liquid-biopsy adoption | +1.1% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Growing demand for liquid-biopsy companion diagnostics | +0.8% | Early uptake in developed markets, global potential | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence & Awareness of Breast Cancer

Breast-cancer incidence is climbing in younger cohorts, especially in Asia where median onset now falls between ages 50-54, five to seven years earlier than in Western nations[1]Rui Ding, “Breast Cancer Screening and Early Diagnosis in Chinese Women,” Cancer Biology & Medicine, cancerbiomed.org. National screening programs broaden the candidate pool for biopsy, yet China’s participation rate remains 21.7%, signaling significant unmet need. Urban–rural disparity boosts demand for portable, cost-efficient equipment that can operate in secondary hospitals. Lower fertility rates and lifestyle shifts further elevate risk, making continual growth in biopsy procedures likely irrespective of population aging. Governments in India and Southeast Asia amplify awareness campaigns, accelerating equipment turnover as outpatient facilities invest in automated, AI-assisted systems to meet rising case volumes.

Expanding Reimbursement for Image-Guided Biopsies

Medicare covers percutaneous image-guided breast biopsy for BIRADS III–V lesions, providing a template many private payers and foreign insurers now follow. Vacuum-assisted stereotactic biopsies save USD 741 per case compared with surgical excision, strengthening the economic case for minimally invasive options[2]Carol H. Lee, “Cost-Effectiveness of Stereotactic Core Needle Biopsy,” Radiology, pubs.rsna.org. Europe’s diagnosis-related groups also reward percutaneous sampling, while early directives in Japan and South Korea mirror the U.S. model. AI-based 3-D imaging tools remain variably covered, so vendors that secure billing codes gain a head start. Private-equity-funded imaging chains rely on stable reimbursement streams to finance center expansion and new equipment.

Accelerating Shift Toward Vacuum-Assisted Systems

Clinical studies show 99.2% sensitivity for vacuum-assisted stereotactic biopsy versus 97.7% for automated core needles, driving practitioner preference. Eleven-gauge directional devices avoid surgery in 76% of eligible cases and cut diagnostic costs by USD 264 per patient. Product refinements such as hydrogel-based markers that cling to tissue surfaces improve post-biopsy localization accuracy. When paired with digital breast tomosynthesis, vacuum-assisted kits detect lesions invisible on full-field mammography, extending the addressable population and propelling the breast biopsy devices market forward.

AI-Enabled 3-D Imaging and Liquid-Biopsy Adoption

Hologic’s Genius AI Detection 2.0 decreases false-positive flags and streamlines radiologist workflow. Virtual biopsy algorithms achieve 0.88 AUC while maintaining 99% sensitivity, potentially avoiding 13% of unnecessary procedures. Robotic needle steering for MRI-guided interventions limits targeting error to 2.2 mm, addressing breast deformation challenges[3]Marta Lagomarsino, “Image-Guided Breast Biopsy with a Hand-Mounted Motorised Needle Tool,” arxiv.org. Regulatory momentum continues: the FDA authorized liquid-biopsy companion tests such as FoundationOne Liquid CDx and Guardant360 CDx for breast indications, catalyzing investment in circulating-tumor-DNA assays. These advances reinforce a precision-medicine model where imaging and molecular tools converge, accelerating the breast biopsy devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Biopsy Infection & Hematoma Risk | -0.7% | Global, with higher impact in resource-constrained settings | Short term (≤ 2 years) |

| High Capital Cost Of Stereotactic Tables | -0.9% | Emerging markets and smaller healthcare facilities | Medium term (2-4 years) |

| Limited Radiology Capacity In Low-Income Regions | -0.6% | Sub-Saharan Africa, rural Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Biopsy Infection & Hematoma Risk

Hematomas develop in up to 94% of patients one week after vacuum-assisted biopsy, though most resolve within 21 days. Clinically significant bleeding affects 6.7% of stereotactic cases, with 96.2% classified as mild. Even minor events fuel patient anxiety and can deter follow-up screening. Infection rates remain low in high-income settings but rise where sterile protocols are inconsistent, prompting cautious rollout of advanced equipment in underserved regions.

Capital Cost & Limited Radiology Capacity

Prone stereotactic tables require high upfront spending and dedicated floor space, hampering adoption by rural hospitals and smaller diagnostics centers. Maintenance contracts and technologist training add to the total cost of ownership. Hub-and-spoke service models proposed for India mitigate some barriers but extend patient travel time. Workforce shortages compound the issue; Sub-Saharan Africa has fewer than one radiologist per 1 million inhabitants, limiting procedure capacity even when equipment is available. Collectively, capital constraints slow penetration of the breast biopsy devices market in emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Guidance Systems Scale Fast as Needles Dominate Volume

Breast-biopsy needles retained 42.70% revenue in 2025, a testament to their consumable nature and essential role across every intervention. The breast biopsy devices market size for guidance and imaging systems, although smaller, is forecast to climb at 9.85% CAGR due to AI overlays, robotic controllers and multimodal 3-D visualization that shorten learning curves. Hospitals adopt integrated consoles that combine stereotactic, ultrasound and tomosynthesis modules, allowing seamless switching mid-procedure. Vendors differentiate through user-friendly dashboards, cloud-linked analytics and smaller form factors that fit outpatient suites. Single-use accessory kits are gaining favor among infection-prevention teams, pointing to resilient demand for disposable components linked to each guidance platform.

Healthcare enterprises value the revenue predictability of re-orderable needles but increasingly bundle those consumables with subscription software for workflow analytics. For example, an institution deploying AI-assisted consoles reports a 14% reduction in repeat biopsies, boosting payer confidence and broadening reimbursement eligibility. As guidance platforms carve out larger budgets, cross-selling opportunities multiply, reinforcing a virtuous cycle within the breast biopsy devices market.

By Procedure: Vacuum-Assisted Biopsy Holds Leadership as FNAB Accelerates

Vacuum-assisted biopsy (VAB) commanded 35.10% of breast biopsy devices market share in 2025, prized for extracting contiguous tissue cylinders that support histologic and molecular tests. Cost-effective kits with integrated clip-deployment mechanisms enable in-procedure marking, reducing recalls. Fine-needle aspiration biopsy (FNAB) logs the swiftest growth at 9.05% CAGR, fueled by its role in axillary-node staging and reduced anesthesia requirements. In low-resource settings, FNAB’s minimal consumable demand and short dwell time appeal to budget-conscious providers.

Future protocols combine FNAB with rapid onsite cytology to deliver same-day results, trimming surgical waitlists. Early adopters also explore molecular profiling from residual FNAB samples, extending clinical utility beyond cytology and expanding the breast biopsy devices market size attributed to disposables and ancillary reagents.

By Technique: Image-Guided Sampling Dominates, Liquid Biopsy Gains Ground

Image-guided approaches comprised 68.10% of overall sales in 2025. The breast biopsy devices market thrives on stereotactic, ultrasound and MRI targeting because precise localization curbs repeat procedures. Ultrasound guidance remains the workhorse for palpable or cystic masses, whereas tomosynthesis solves lesion overlap in dense breasts. Simultaneously, liquid biopsy posts a 10.15% CAGR as clinicians adopt circulating-tumor-DNA assays for refractory or metastatic disease, supported by FDA-cleared companion diagnostics. Blockchain-ready cloud platforms now link pathology labs with imaging centers to route plasma-based reports into electronic medical records, streamlining multidisciplinary decisions.

Automation stands out: robotic arms anchored to gantries can reposition in 3 seconds, empowering single-operator suites and raising weekly throughput by 18%. These efficiency gains keep image-guidance at the core of the breast biopsy devices market while liquid biopsy expands the use-case spectrum.

By Indication: Microcalcifications Lead; Recurrent Cancer Surges

Suspicious microcalcifications represented 39.10% of biopsy volume in 2025, largely because widespread screening mammography detects clustered foci that require histologic verification. Recurrent breast cancer grows at 11.05% CAGR, reflecting longer survivorship and the need for biomarker testing when disease resurfaces. HER2 re-assessment using freshly sampled tissue drives repeat interventions, especially after therapies such as trastuzumab deruxtecan gain indications for ultralow HER2 expression Roche. Vacuum-assisted excision protocols for low-grade ductal carcinoma in situ also emerge, replacing lumpectomy in select cohorts and lowering hospitalization costs.

As precision oncology matures, clinicians request repeat biopsies to confirm evolving molecular profiles, enlarging the breast biopsy devices market. Companies integrating instant immunohistochemistry into core-sample workflows will benefit from this trend.

By End User: Diagnostic Centers Close Gap on Hospitals

Hospitals held 52.30% revenue in 2025, reflecting established referral networks and the convenience of on-site pathology. Yet independent diagnostic centers demonstrate a 9.20% CAGR by offering streamlined scheduling, faster reporting and spa-like environments that ease patient anxiety. Private-equity-backed chains scale rapidly, using centralized purchasing to standardize equipment and negotiate bulk rates. Cloud-based AI decision-support tools let radiologists in regional hubs supervise multiple satellite sites, shrinking skill-gap barriers in rural regions and expanding the breast biopsy devices market.

Hospital outpatient departments respond by spinning off breast-care boutiques that mirror stand-alone centers’ efficiency while retaining brand loyalty. Strategic joint ventures, such as those between large hospital systems and specialty imaging networks, indicate the line between provider types will blur over the forecast horizon.

Geography Analysis

North America commanded 42.30% of 2025 revenue behind comprehensive Medicare coverage and a dense network of fellowship-trained breast radiologists. Widely available tomosynthesis, high AI acceptance and payer willingness to reimburse liquid-biopsy companion diagnostics strengthen the region’s dominance. Consolidation accelerates innovation: RadNet’s acquisition of iCAD channels AI resources into 363 imaging centers, establishing data pipelines to refine algorithm accuracy and maintain the region’s technological edge.

Asia-Pacific is the fastest-growing territory at 9.35% CAGR because governments subsidize nationwide screening programs and younger median onset mandates earlier intervention. China’s goal to screen 6 million women per year opens a vast addressable population while revealing logistic gaps that favor portable biopsy carts. Japan pilots magnetic seed localization and low-dose tomosynthesis to reduce radiation anxiety, while South Korea extends national insurance to AI-assisted ultrasound, stimulating equipment upgrades. As middle-income economies scale digital health platforms, regional suppliers collaborate with Western OEMs to customize low-footprint devices, ensuring sustained growth for the breast biopsy devices market.

Europe records steady gains thanks to CE-marked innovations and diagnosis-related group payments that reward minimally invasive therapy. Germany expands outpatient quotas for stereotactic procedures, freeing inpatient capacity. Meanwhile, Eastern European countries tap EU structural funds to modernize imaging suites, narrowing technology gaps within the bloc.

South America and the Middle East & Africa trail but exhibit pockets of acceleration. Brazil introduces tele-pathology pilots that shorten report cycles, whereas Gulf Cooperation Council states subsidize tomosynthesis for nationals. Infrastructure constraints and currency volatility remain hurdles, yet creative financing—such as pay-per-use models—shows promise for broadening access and nurturing the breast biopsy devices market.

Competitive Landscape

Competition is moderate, with top players integrating hardware, AI software and service contracts to secure critical mass. Hologic’s USD 310 million acquisition of Endomagnetics augments its biopsy line with magnetic seed localization, allowing a contiguous workflow from detection to surgery. GE HealthCare scales its Serena Bright platform to integrate contrast-enhanced mammography and same-session biopsy, positioning itself as a one-stop diagnostic shop.

RadNet’s all-stock purchase of iCAD for USD 103 million marries a national imaging footprint with FDA-cleared algorithms, shifting bargaining power toward providers that control both data and devices. Smaller innovators focus on niche enhancements: Merit Medical’s SCOUT Mini reflector trims overall length by 33%, catering to lymph-node targeting, while robotic-arm developers refine motion stabilization for MRI suites.

Differentiation hinges on user-experience metrics—procedure time, false-positive reduction and workflow interoperability. Vendors that wrap disposables into subscription-based AI analytics lock in recurring revenue and deepen customer stickiness. Price-sensitive markets welcome stripped-down variants, but the long-term prize lies with modular ecosystems that allow incremental add-ons, keeping the breast biopsy devices market dynamic.

Breast Biopsy Devices Industry Leaders

Hologic Inc.

Becton Dickinson & Co

Danaher Corp.

Argon Medical Devices

Merit Medical Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: GE HealthCare unveiled Serena Bright contrast-guided biopsy at the Society of Breast Imaging Symposium, boosting lesion visualization during contrast-enhanced mammography.

- September 2024: Mammotome added the Hummingbird shape to its HydroMARK Plus marker portfolio, using hydrogel wings for ultrasound visibility up to 12 months.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysis defines the breast biopsy devices market as every dedicated instrument or accessory that helps clinicians remove breast tissue or fluid for histologic or molecular evaluation. The scope therefore covers vacuum-assisted and spring-loaded needles, biopsy guns, procedure-specific tables, real-time imaging or guidance consoles, localization wires or clips, and assay or reagent kits sold expressly for breast sampling.

Scope exclusion: General radiology systems not bundled with biopsy hardware, open-surgical excision devices, and liquid-biopsy reagents marketed for multi-cancer screening are left out.

Segmentation Overview

- By Product

- Breast Biopsy Needles

- Breast Biopsy Tables

- Guidance/Imaging Systems

- Localization Wires

- Assay & Reagent Kits

- Others

- By Procedure

- Vacuum-Assisted Biopsy (VAB)

- Core Needle Biopsy (CNB)

- Fine Needle Aspiration Biopsy (FNAB)

- Others

- By Technique

- Image-Guided Biopsy

- Stereotactic-Guided

- Ultrasound-Guided

- CT-Guided

- MRI-Guided

- Liquid-Biopsy Techniques

- Next-Generation Sequencing

- PCR-Based

- Microarray-Based

- Image-Guided Biopsy

- By Indication

- Fibroadenoma

- Suspicious Micro-calcifications

- Complex Cyst

- Recurrent Breast Cancer

- Invasive Lobular Carcinoma

- Other Indications

- By End User

- Breast Care Centres

- Hospitals & Clinics

- Diagnostic Centres

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing radiologists, interventional breast surgeons, procurement heads at hospitals, and distributors across North America, Europe, and high-growth Asia. Conversations clarified real-world device utilization rates, average selling prices, and emerging preferences (for example, clip-based marker kits), enabling us to fine-tune assumptions and stress-test early desk findings.

Desk Research

We mapped the demand pool through publicly available datasets such as WHO-GLOBOCAN cancer registries, CDC SEER incidence files, and FDA 510(k) device approvals, complemented by industry statistics from the American College of Radiology and national health ministries. Company filings and investor decks were pulled from D&B Hoovers, while patent-flow insights came through Questel to trace technology adoption curves. These sources offered baseline prevalence, installed-base clues, and pricing guardrails. The list above is illustrative; many more repositories informed the desk work.

Market-Sizing & Forecasting

A top-down prevalence-to-procedure model converts diagnosed breast-cancer and BIRADS 4-5 screening volumes into addressable biopsies, which are then matched with device penetration ratios from primary interviews. Supplier roll-ups and sampled ASP × unit checks provide a bottom-up cross-check before totals are locked. Key inputs include screening program coverage, repeat-biopsy share, hospital capital budgets, average procedure mix shift toward vacuum-assisted systems, and currency-adjusted ASP trajectories. Forecasts run on multivariate regression with scenario analysis around screening uptake and ASP erosion, giving us a transparent five-year view. Data gaps, typically around private clinic volumes, are bridged by triangulating distributor shipment proxies and regional tender notices.

Data Validation & Update Cycle

Outputs pass variance checks versus historical series, peer literature, and anonymized hospital purchase orders. Senior reviewers audit formulas, and outliers trigger re-contacts with experts. The model refreshes annually, with interim amendments if regulatory or reimbursement shifts materially affect volumes or prices.

Why Mordor's Breast Biopsy Devices Baseline Commands Reliability

Published numbers differ because market trackers vary in scope choices, assumption rigor, and update cadence.

Device inclusion rules, ASP derivation, and whether liquid-biopsy platforms are folded into totals often drive the widest gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.29 B | Mordor Intelligence | - |

| USD 2.38 B | Global Consultancy A | Counts broad liquid-biopsy analyzers and service revenues |

| USD 2.70 B | Regional Consultancy B | Uses aspirational screening uptake and list-price ASPs |

| USD 1.13 B | Trade Journal C | Omits guidance consoles and reagent kits from device pool |

The comparison shows how scope creep or omission can swing values by over a billion dollars. By anchoring on clearly disclosed device classes, validated utilization ratios, and annually refreshed pricing, Mordor delivers a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the breast biopsy devices market?

The breast biopsy devices market is valued at USD 1.35 billion in 2026.

Which product type grows fastest through 2031?

Guidance and imaging systems show the highest 9.85% CAGR as AI integration accelerates through 2031.

Why is Asia-Pacific the quickest-expanding region?

Government-funded screening programs and a younger median age of onset drive a 9.35% regional CAGR.

How does vacuum-assisted biopsy outperform other techniques?

It offers 99.2% sensitivity, larger single-pass samples and avoids surgery in 76% of eligible cases.

Are liquid biopsies replacing tissue sampling?

No; they complement image-guided biopsies by providing molecular insights, but tissue remains essential for histology and microenvironment assessment.

What limits adoption in emerging markets?

High capital cost of stereotactic tables and limited radiology capacity slow installation rates despite strong demand.

Page last updated on: