Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

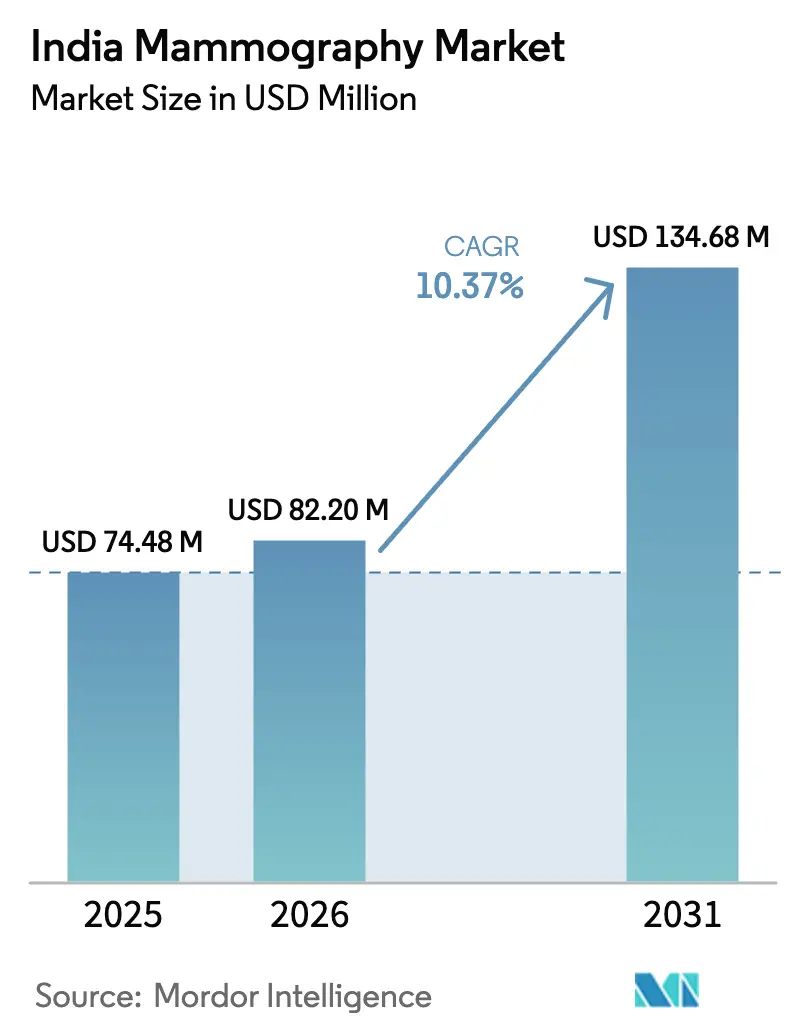

| Base Year Market Size (2025) | USD 74.48 Million |

| Market Size (2026) | USD 82.2 Million |

| Market Size (2031) | USD 134.68 Million |

| Growth Rate (2026 - 2031) | 10.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Mammography Market Analysis by Mordor Intelligence

The India mammography market size is expected to grow from USD 74.48 million in 2025 to USD 82.2 million in 2026 and is forecast to reach USD 134.68 million by 2031 at 10.37% CAGR over 2026-2031. The growth reflects government-funded population screening, hospital upgrades to 3-D systems, and private diagnostic expansion into tier-2 and tier-3 cities. Breast cancer’s 32% share of all female malignancies has moved early detection from an urban concern to a national priority. Domestic manufacturing commitments by Wipro GE Healthcare and Siemens Healthineers are lowering device costs and accelerating technology adoption. Meanwhile, AI-assisted triage solutions address radiologist shortages and improve throughput, further catalyzing the India mammography market.

Key Report Takeaways

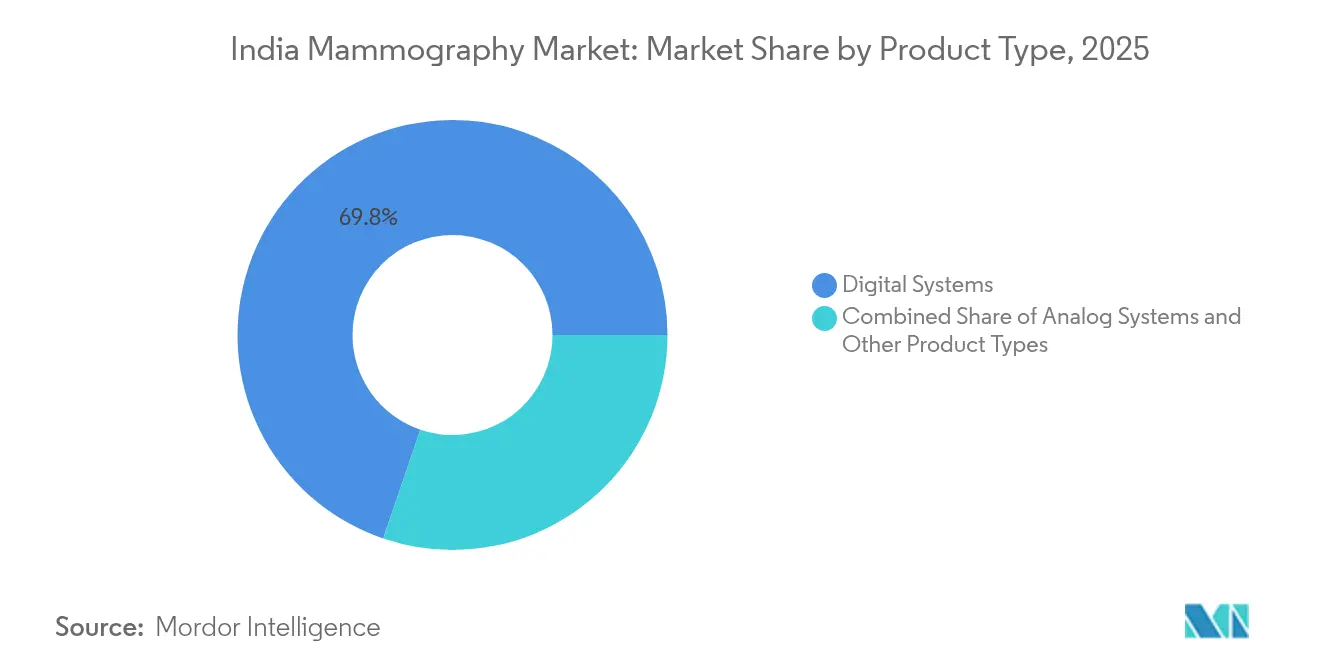

- Digital Systems captured 69.78% of the India mammography market share in 2025, whereas Other Product Types are projected to expand at an 11.22% CAGR through 2031.

- Hospitals accounted for 64.45% of the India mammography market size in 2025, and Specialty Clinics are advancing at an 11.63% CAGR to 2031.

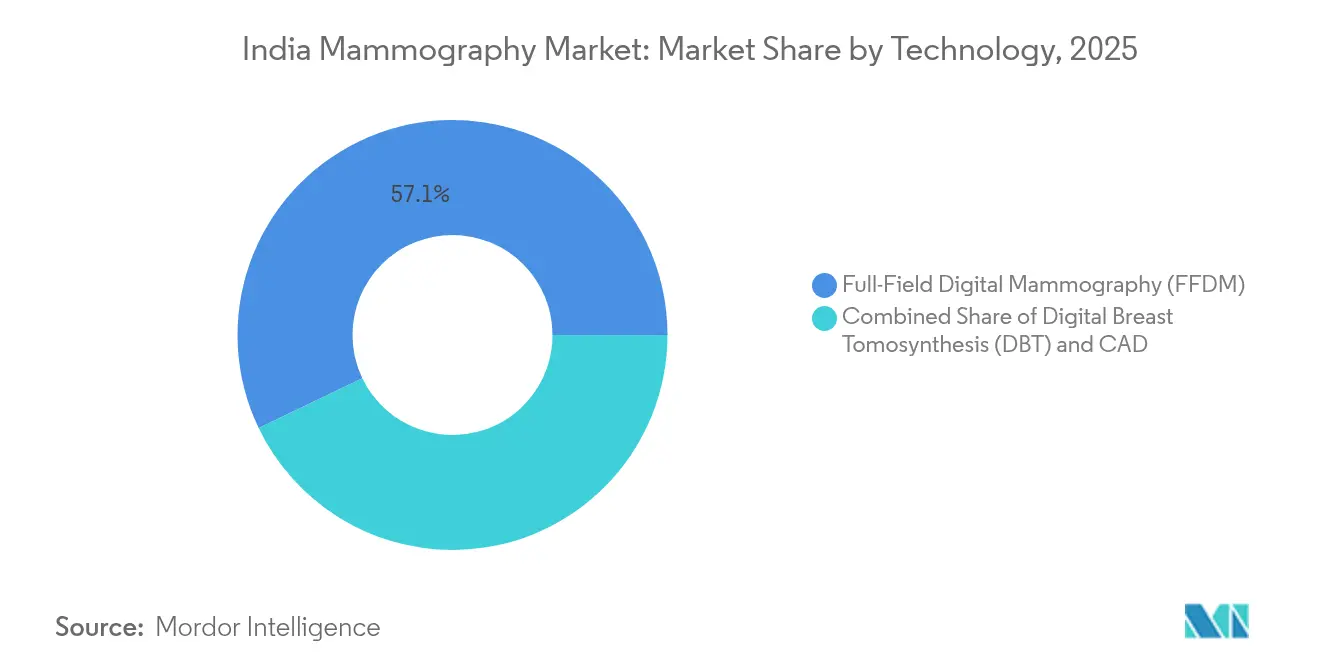

- Full-Field Digital Mammography held 57.12% of the India mammography market share in 2025, while Digital Breast Tomosynthesis is set to grow at an 11.78% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Breast Cancer In Urban & Semi-Urban India | +2.8% | Urban metros and tier-2 cities, with spillover to semi-urban areas | Medium term (2-4 years) |

| Government-Funded Population-Based Screening Roll-Outs | +2.1% | National, with early gains in states with established NPCDCS infrastructure | Long term (≥ 4 years) |

| Expansion Of Large Private Diagnostic Chains Into Tier-2/Tier-3 Cities | +1.9% | Tier-2 and tier-3 cities across major states | Short term (≤ 2 years) |

| Rapid Hospital Adoption Of 3-D/DBT Upgrades As Cap-Ex Costs Fall | +1.7% | Urban hospitals and specialty centers nationwide | Medium term (2-4 years) |

| AI-Enabled Triage Solutions Easing Radiologist Shortage | +1.2% | Major metropolitan areas with advanced healthcare infrastructure | Medium term (2-4 years) |

| Corporate Wellness Programs Boosting Opportunistic Screening | +0.8% | Corporate hubs in major cities and industrial centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Breast-Cancer Burden in Urban & Semi-Urban India

Breast-cancer diagnoses in India are projected to climb from 806,218 in 2025, driven by delayed childbearing and lifestyle changes. Higher awareness campaigns, especially in metros, are prompting earlier self-referral. Economic modeling places the breast-cancer cost burden at USD 13.95 billion by 2030. These pressures drive sustained procurement of digital systems and mobile units, strengthening the India mammography market.

Government-Funded Population-Based Screening Roll-Outs

The NPCDCS now covers more than 400 districts and has screened over 34.39 crore individuals for common cancers. More than 1,72,148 Ayushman Arogya Mandirs perform routine clinical breast examinations, generating predictable equipment demand across public facilities. Duty exemptions on select oncology drugs and the National Cancer Grid’s standardized protocols further reinforce volume certainty [1]Ministry of Health & Family Welfare, “Towards a Cancer-Free India,” pib.gov.in . The program’s expansion into rural health sub-centers anchors the long-term trajectory of the India mammography market.

Expansion of Private Diagnostic Chains into Tier-2/Tier-3 Cities

Organized diagnostic players, holding 16–20% of the broader diagnostics revenue, are growing 8–9% annually. Dr. Lal PathLabs, Metropolis, and Neuberg set up satellite labs and imaging hubs, often bundling mobile mammography vans to widen catchment areas. Tele-radiology link-ups allow sub-10-minute turnaround of scans, mitigating radiologist scarcity. These moves funnel equipment sales toward compact digital units, deepening the India mammography market footprint in emerging towns.

Rapid Hospital Adoption of 3-D/DBT Upgrades

Capital outlays for Digital Breast Tomosynthesis have fallen 18–22% since 2023 as Wipro GE and Fujifilm ramp up local assembly. Apollo Hospitals and PGI Chandigarh publicly inaugurated 3-D suites in 2024, citing lower recall rates and improved dense-breast imaging. Vendor-neutral prior-image comparison and zero-click workflow features boost technologist productivity, sustaining hospital demand for premium upgrades. These trends accelerate the move toward 3-D dominance within the India mammography market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uneven Reimbursement & Low Private Insurance Penetration | -1.8% | National, with acute impact in rural and semi-urban areas | Long term (≥ 4 years) |

| Radiation-Exposure Concerns Among Pre-Menopausal Women | -1.2% | Urban educated populations and health-conscious demographics | Medium term (2-4 years) |

| Scarcity Of Mammography Technicians In Tier-3 Towns | -1.0% | Tier-3 cities and rural healthcare facilities | Long term (≥ 4 years) |

| Import-Duty & GST Structure Inflating Device ASPs | -0.9% | National, affecting all market segments uniformly | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Uneven Reimbursement & Low Private Insurance Penetration

Only 41.2% of households have any insurance cover, and a mere 3.3% rely on private plans, stifling preventive screening uptake. State-level disparities are stark; Rajasthan reports 87.9% coverage while some island territories sit below 2%. Out-of-pocket mammography spending remains high because underwriting rules often treat screening as elective. Despite IRDAI guidance allowing coverage, real-world claims for mammograms stay low [2]IRDAI, “Health Department Circulars,” irdai.gov.in. These gaps defer elective imaging and weigh on the India mammography market.

Radiation-Exposure Concerns Among Pre-Menopausal Women

Modeling estimates 86 induced cancers per 100,000 women screened, a statistic publicized in patient forums. Clinical protocols now recommend starting screening at age 30, intensifying exposure worries among younger cohorts. Dense-breast imaging and overdiagnosis debates circulate widely on social media, prompting some women to postpone scans. Hospitals counter by emphasizing low-dose DBT and AI-based triage, yet lingering perceptions still temper growth momentum in the India mammography market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Dominance Drives Market Evolution

Digital Systems generated 69.78% of the India mammography market share in 2025 and underpin the nationwide shift toward image-rich, radiation-efficient diagnostics. Their cloud connectivity aligns with tele-radiology workflows, enabling remote reads from metro hubs. The India mammography market size for Digital Systems is expected to scale rapidly as state oncology programs mandate DICOM-compliant storage. Analog units are being phased out, often traded in for mobile vans targeting single-day screening camps. Other Product Types—biopsy-guided suites and van-mounted devices—show an 11.22% CAGR, buoyed by rural outreach under the National Health Mission.

Growing preference for base-hospital DBT plus satellite mobile units has widened vendor portfolios. Fujifilm alone has installed more than 50,000 medical devices across India, including FFDM scanners optimized for low-resource settings. Quality-assurance guidelines issued by the Breast Imaging Society of India push for uniform calibration and dose monitoring IJBI.IN. These standards reinforce digital predominance and help maintain consistent imaging quality across the India mammography market.

By End User: Specialty Clinics Narrow the Gap

Hospitals commanded 64.45% of the India mammography market size in 2025 on the back of multispecialty oncology centers and capacity expansions financed through public-private partnerships. Academic institutions anchor clinical trials and often serve as early adopters for AI-enabled diagnostics. Specialty Clinics, however, exhibit the fastest 11.63% CAGR as private chains bundle breast imaging with wellness panels and tele-consults. Their compact center format suits tier-3 cities where floor space is at a premium.

Workflow-enhancement devices such as GE HealthCare’s Pristina Via reduce technologist click counts, an attractive feature for clinics facing an 18% vacancy rate among radiographers. Mobile units parked at industrial sites under CSR initiatives further expand the addressable population. The combined institutional and entrepreneurial demand stabilizes unit shipments and ensures that the India mammography market remains resilient to macroeconomic fluctuations.

By Technology: DBT Innovation Reshapes Diagnostic Capability

FFDM retained 57.12% of the India mammography market share in 2025, yet growth momentum clearly tilts toward Digital Breast Tomosynthesis, forecast at an 11.78% CAGR. DBT’s layered imaging reduces tissue overlap, improving lesion detection in dense breasts and curbing recall anxiety. Computer-Aided Detection algorithms, both embedded and cloud-based, complement DBT and FFDM workflows, offering automated lesion flags within seconds.

A study in Odisha reported 98.7% sensitivity and 87.9% diagnostic accuracy for BI-RADS-guided readings on modern systems. The IAEA’s quality-assurance protocol underscores digital systems’ superiority and supports grant funding for DBT in government hospitals. Regulatory clarity under the Medical Devices Rules, 2017 fast-tracks import licenses for AI-enabled upgrades . Together these factors accelerate the transition toward 3-D, reinforcing the innovation profile of the India mammography market.

Geography Analysis

Metropolitan clusters such as Delhi-NCR, Mumbai-Pune, and Bengaluru host the densest installed base, driven by higher disposable incomes and awareness. Breast-cancer survival reaches 74.9% in Mizoram and 72.7% in Ahmedabad but falls below 42% in Pasighat, exposing stark regional care gaps. Northern and western corridors benefit from oncology hubs and medical-device parks that localize manufacturing, trimming logistics costs.

Southern states, notably Tamil Nadu and Karnataka, leverage strong public-health budgets and CSR-led screening drives. Punjab logged a 7% jump in breast-cancer incidence from 2021–2024, yet screening participation languishes at 0.3%. This gap is spurring mobile-van deployments under programs like Deen Dayal Chalit Aspatal, operating since 2007.

Tier-2/3 cities now anchor the fastest install growth as chain clinics cluster around state-highway spines. Uttar Pradesh, Bihar, and Madhya Pradesh, accounting for nearly half of national cancer cases, form the next frontier for the India mammography market. Indigenous device parks in Himachal Pradesh and Uttar Pradesh promise to shorten supply cycles, driving double-digit shipment growth into interior districts.

Competitive Landscape

The India mammography market is moderately concentrated round a triad of multinationals—Wipro GE Healthcare, Siemens Healthineers, and Hologic—each localizing production to sidestep import duties that can reach 45%. Domestic brands such as BPL Medical Technologies leverage distribution alliances to fill rural demand with cost-optimized units. Competitive positioning centers on AI integration, dose-management features, and patient-comfort design.

Strategic alliances frame recent momentum: GE HealthCare and RadNet signed a multi-year collaboration to embed SmartTechnology AI into workflow stacks. Siemens Healthineers’ Bengaluru site now ships MAMMOMAT units throughout South Asia, slashing lead times. Hologic continues to dominate premium DBT, citing 250 million patients touched by its women’s-health portfolio in FY 2023.

White-space innovators are scaling AI triage: Vara secured USD 8.9 million to deploy cloud-based detection in NM Medical’s network. Thermalytix and Niramai offer thermal-imaging adjuncts aimed at low-resource clinics. The resultant blend of global R&D with local frugality creates a dynamic ecosystem, sustaining healthy rivalry while steadily raising the technology baseline across the India mammography market.

India Mammography Industry Leaders

Siemens AG

Planmed OY

Hologic Inc.

Fujifilm Holdings Corporation

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BPL Medical Technologies partners with Panacea Medical Technologies to distribute advanced mammography solutions nationwide.

- June 2025: Dharamshila Narayana Superspeciality Hospital unveils 3-D mammography and launches a free women’s screening program.

- December 2024: Deepak Phenolics rolls out a mobile mammography van for early detection under its CSR initiative.

- June 2024: Fujifilm India and NM Medical Mumbai inaugurate a skill lab to train radiologists and radiographers on FFDM platforms.

India Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. India Mammography Market is segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis, and Other Product Types), End Users (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Systems |

| Analog Systems |

| Other Product Types (Biopsy-guided, Mobile units) |

By End User

| Hospitals |

| Specialty Clinics |

| Others |

By Technology

| Full-Field Digital Mammography (FFDM) |

| Digital Breast Tomosynthesis (DBT) |

| Computer-Aided Detection (CAD) |

| By Product Type | Digital Systems |

| Analog Systems | |

| Other Product Types (Biopsy-guided, Mobile units) | |

| By End User | Hospitals |

| Specialty Clinics | |

| Others | |

| By Technology | Full-Field Digital Mammography (FFDM) |

| Digital Breast Tomosynthesis (DBT) | |

| Computer-Aided Detection (CAD) |

Key Questions Answered in the Report

How big is the India Mammography Market?

The India Mammography Market size is expected to reach USD 82.2 million in 2026 and grow at a CAGR of 10.37% to reach USD 134.68 million by 2031.

Which product segment leads sales volume?

Digital Systems hold 69.78% of all units sold in 2025.

Who are the key players in India Mammography Market?

Siemens AG, Planmed OY, Hologic Inc., Fujifilm Holdings Corporation and GE Healthcare are the major companies operating in the India Mammography Market.

Why are Specialty Clinics the fastest-growing end users?

Private diagnostic chains are expanding into tier-2/3 cities, boosting clinic demand at an 11.63% CAGR.

Page last updated on: