Europe Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

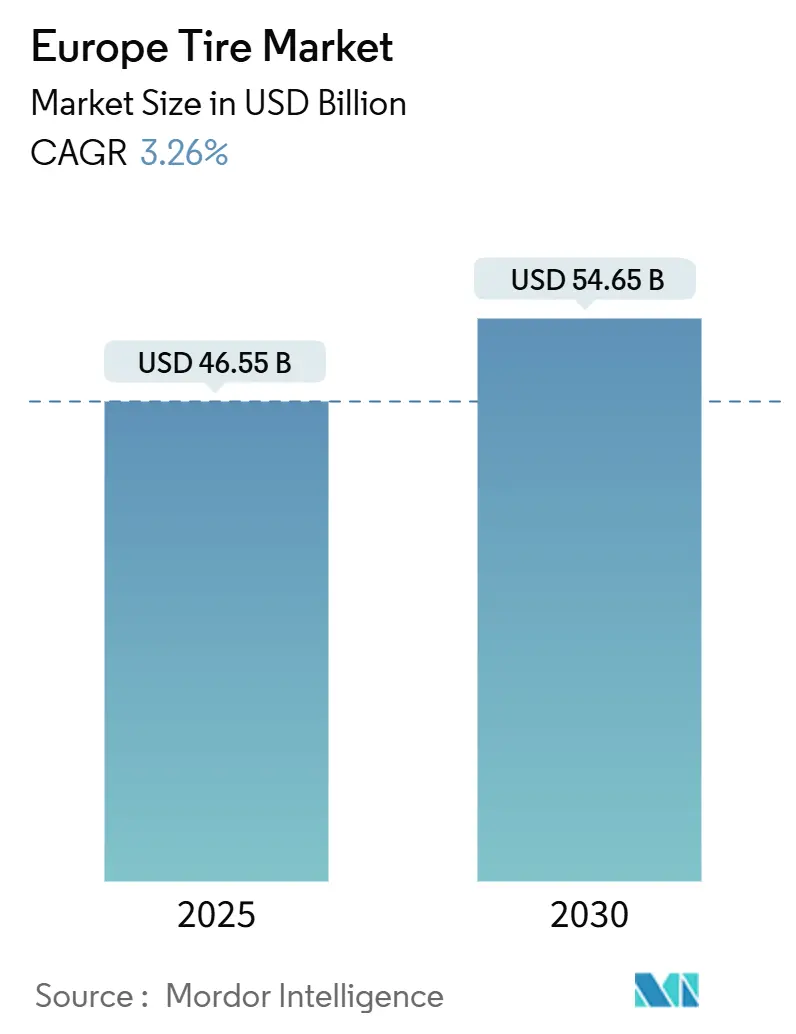

| Market Size (2025) | USD 46.55 Billion |

| Market Size (2030) | USD 54.65 Billion |

| Growth Rate (2025 - 2030) | 3.26% CAGR |

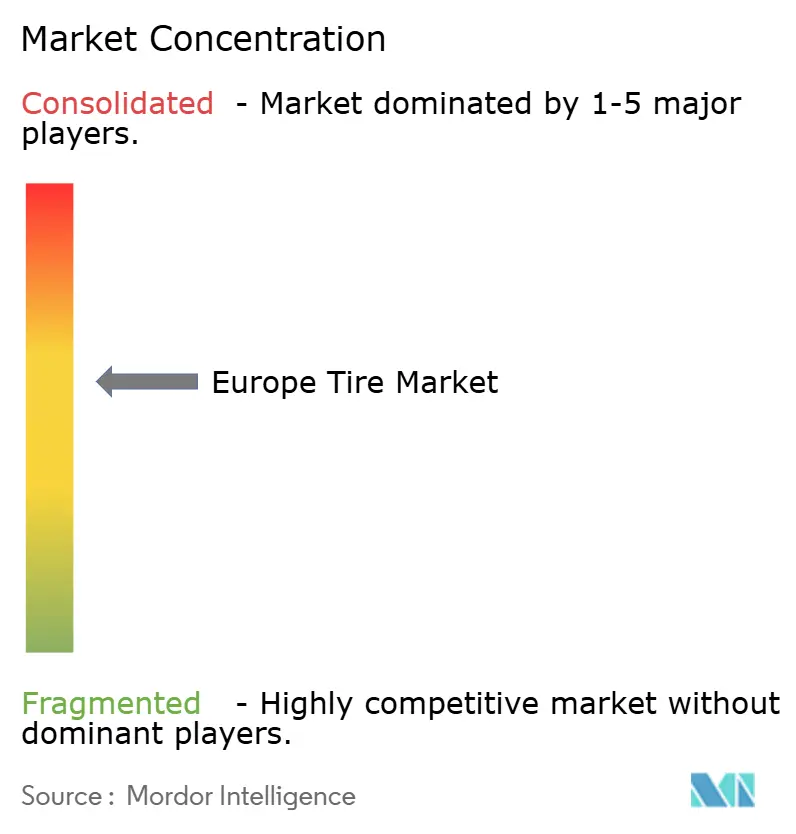

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Tire Market Analysis by Mordor Intelligence

Europe's tire market size stands at USD 46.55 billion in 2025 and is projected to reach USD 54.65 billion by 2030, translating to a 3.26% CAGR over the forecast period. Mature demand across passenger and commercial segments co-exists with fresh opportunities created by electrification, sustainability mandates, and digital retail models. Low-rolling-resistance technology, mandated under the European Green Deal, is lowering fleet fuel use and steering material innovation toward silica-rich compounds. All-season fitment continues to displace the traditional summer-winter rotation in Central and Western Europe as consumers favor convenience. Specialized EV tires with higher load indices and noise-damping liners now secure premium pricing as battery-electric vehicles expand rapidly. Supply-side risks remain natural rubber cost volatility, and new EU anti-dumping duties on Chinese imports are tightening margins even as OEMs demand greater recycled and bio-based content.

Key Report Takeaways

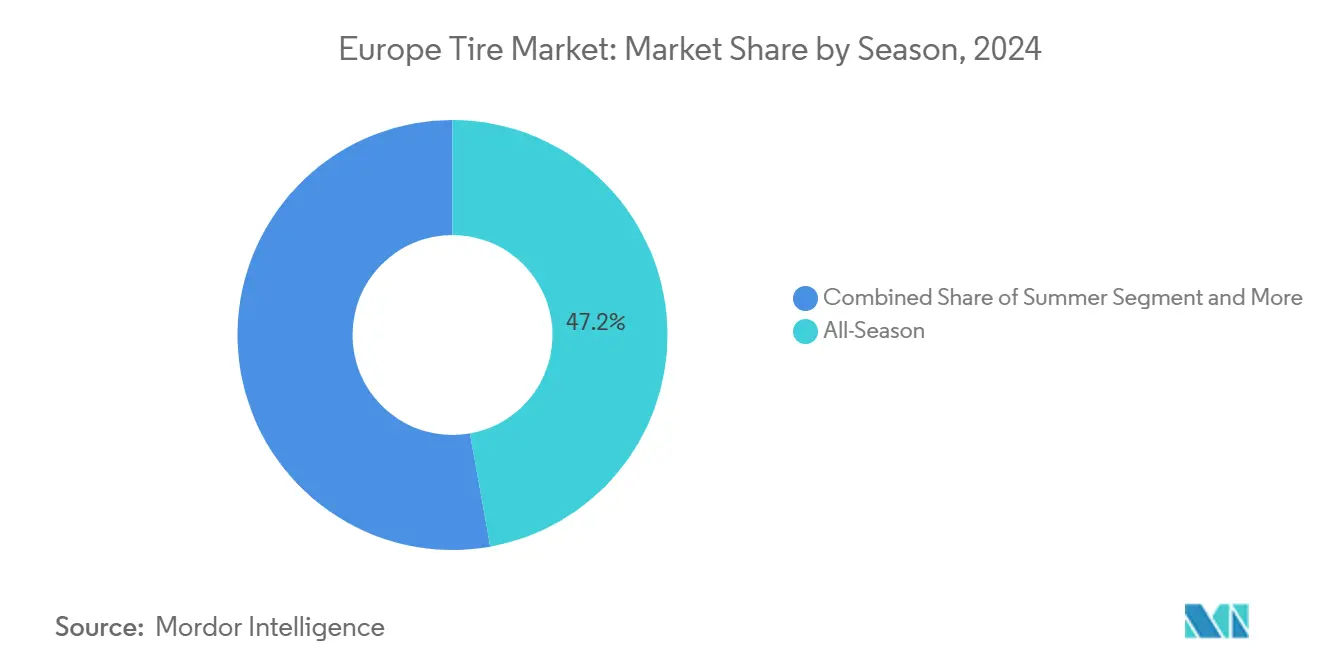

- By season, all-season tires held 47.15% of the European tire market share in 2024, and will continue to grow with a CAGR of 3.88% during 2025-2030.

- By tire design, radial tires held 94.16% of the European tire market share in 2024, while non-pneumatic/airless designs are projected to grow with a CAGR of 5.56% through 2030.

- By vehicle type, passenger cars held 58.33% of the European tire market share in 2024, and will continue to grow with a CAGR of 4.11% during 2025-2030.

- By application, on-road tires held 83.25% of the European tire market share in 2024, while off-road models are tracking the fastest 5.18% CAGR through 2030.

- By end user, the aftermarket held 69.04% of the European tire market share in 2024 and will continue to grow at a CAGR of 4.55% from 2025 to 2030.

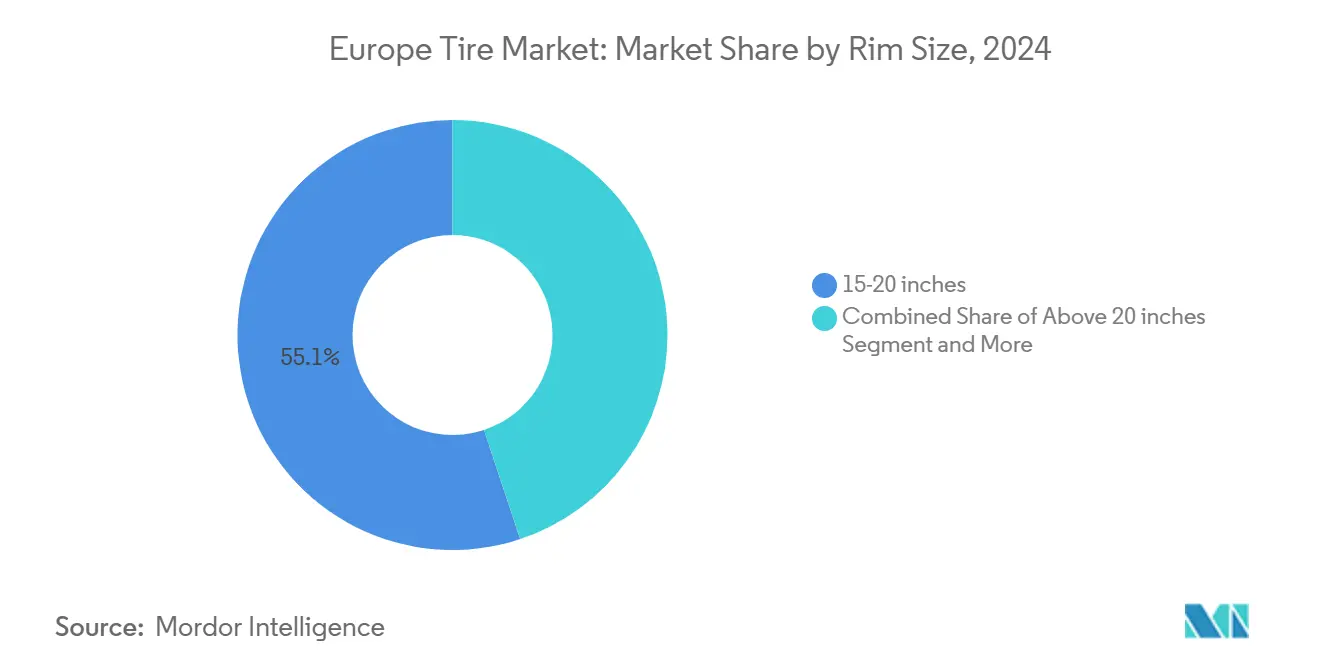

- By rim size, tires of 15-20 inches accounted for 55.13% of the European tire market revenue in 2024, whereas tires above 20 inches are forecast to grow with 6.44% CAGR through 2030.

- By propulsion, internal-combustion vehicles dominated the European tire market revenue with 75.22% share in 2024, while battery-electric-vehicle tires are tracking the fastest 7.13% CAGR through 2030.

- By country, Germany led with 21.33% of the European tire market share in 2024; Spain is forecast to register a 6.18% CAGR to 2030.

Europe Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand Rises For EV Tires | +0.9% | Germany, UK, France, Nordics | Long term (≥ 4 years) |

| Green Deal Pushes Low-Resistance Tires | +0.8% | EU-wide; strongest in Germany and France | Medium term (2-4 years) |

| All-Season Tire Fitment Surges | +0.6% | Central and Western Europe | Short term (≤ 2 years) |

| E-commerce Drives DTC Growth | +0.4% | UK, Germany, France, Netherlands | Medium term (2-4 years) |

| OEMs Mandate Sustainable Compounds | +0.3% | EU-wide; led by Germany and France | Long term (≥ 4 years) |

| AI Enables Predictive Maintenance | +0.2% | Germany, UK, Netherlands, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification-Specific Tire Demand (Low Noise, Higher Load Index)

Battery packs add 150-200 kg to curb weight and increase torque, shortening tread life by up to 20% on conventional compounds. Acoustic foam liners inside Hankook’s iON series cut cabin noise by 9.2 dB without sacrificing rolling resistance[1]“iON Acoustic Engineering,” Hankook Tire, hankooktire.com. Premium pricing offsets higher R&D and specialized molding costs; consequently, the segment posts significant growth, the highest among propulsion categories.

Green-Deal Push for Low-Rolling-Resistance Tires

EU decarbonization targets have made low-rolling-resistance performance a minimum requirement. Class A tires can cut vehicle fuel use, adding up to 57 TWh of annual savings by 2030 across the bloc [2]“EU Tire Labelling Initiative,” European Commission, ec.europa.eu. Manufacturers balance wet grip and tread life by combining advanced tread designs with rice-husk-ash silica, an approach already commercialized in Pirelli’s sustainable range. Fleet buyers track total cost of ownership more closely, accelerating adoption where payback periods fall below two years.

Surge in All-Season Tire Fitment Across Central and Western Europe

All-season products captured a significant share of the 2024 demand as urban drivers avoid seasonal storage and mounting fees. Temperature-adaptive polymers keep tread pliable from mild winters to warm summers. Goodyear and Nokian launched ranges with sipes that reopen under braking, preserving safety across varying climates [3]“All-Season Growth in Europe,” Goodyear EMEA, goodyear.eu. Retailers benefit from simpler inventories while producers streamline SKU counts and production planning.

E-Commerce and Direct-to-Consumer Tire Retail Growth

Online penetration rises as standardized sizing simplifies comparison shopping. Blackcircles integrates over 2,000 U.K. fitting locations and reports 1 million monthly visits, offering delivered-and-fitted packages priced 20% below many brick-and-mortar outlets. Data-driven recommendation engines schedule replacements proactively, elevating customer lifetime value and smoothing demand for distributors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility | -0.7% | Heavy on European makers | Short term (≤ 2 years) |

| EU Anti-Dumping Duties On Tires | -0.4% | EU-wide; acute in Germany and Eastern Europe | Medium term (2-4 years) |

| EV Curb Weight Causes Treadwear | -0.3% | Germany, UK, Nordics | Long term (≥ 4 years) |

| Slow Permitting For Pyrolysis Plants | -0.2% | EU-wide; notably Germany and Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Raw-Material Price Volatility (Natural and Synthetic Rubber

Natural rubber prices rose significantly quarter-on-quarter in 2024, while synthetic rubber indices hit 120.2 in February 2025. Leaf-fall disease in Southeast Asia curtailed supply just as freight rates on Asia-to-Europe lanes tripled, raising delivered costs. OEM pricing contracts prevent full pass-through, compressing margins and prompting producers to diversify feedstocks.

EU Anti-Dumping Duties on Chinese Truck/Bus Tires Pressuring Import Mix

Tariffs implemented in 2025 elevate import costs and disrupt supply chains that had relied on lower-priced Chinese products. Domestic manufacturers gain temporary pricing leverage yet face volume swings as distributors seek alternate sources. Chinese firms may respond by building capacity within Europe to bypass duties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: Convenience Fuels All-Season Leadership

All-season tires held a 47.15% share of the European tire market in 2024 and will expand at a 3.88% CAGR to 2030. Consumers in metropolitan Germany, France, and Poland increasingly value one-set convenience and lower storage fees. Manufacturers employ adaptive silica-rich compounds that stay flexible below 7 °C yet resist deformation above 30 °C. Summer tires retain popularity among performance enthusiasts in Spain and Italy who demand high-temperature grip, while winter tires remain compulsory in Nordic regions. All-season dominance simplifies retailer inventory, an advantage as e-commerce grows. The resulting demand stability helps plants run closer to capacity, improving cost profiles for major players.

When negotiating supply contracts, OEMs evaluate the European tire market size contributions from all-season lines. Nokian reports double-digit growth in its Seasonproof range after embedding 38% sustainable material content. As labeling regulations emphasize snowflake markings and wet-grip scores, suppliers refine tread patterns to earn superior classifications, reinforcing competitive differentiation.

By Tire Design: Radial Reigns While Airless Emerges

Radial construction accounted for 94.16% of the European tire market in 2024. Its steel-belted architecture maximizes tread stability and fuel economy, aligning with EU efficiency goals. Bias designs survive mainly in agriculture, where low speed mitigates heat build-up. Non-pneumatic prototypes, such as Michelin–GM UPTIS, register a 5.56% CAGR to 2030 on pilot programs with urban shuttle fleets. These airless units promise puncture immunity and lower maintenance, traits autonomous-vehicle developers value.

Technology hurdles remain. Designers must counter vibration and noise from spoke structures to satisfy ride-comfort norms. Cost parity with radial alternatives depends on scalable molding of complex polyurethane composites. Nevertheless, the public demonstrations at the 2024 Munich IAA signaled growing OEM interest, suggesting airless adoption may follow EV market expansion curves.

By Vehicle Type: Passenger Cars Dominate but LCVs Accelerate

Passenger cars held a 58.33% of the European tire market share in 2024, aided by a European car parc. Electrification augments premium demand, as EV owners choose low-noise, high-load tires. Light commercial vehicles benefit from e-commerce delivery growth, driving replacement cycles that outpace heavy trucks. Motorcycles remain integral to mobility in Italy and Spain, supporting stable two-wheeler demand.

Europe's tire market size for passenger applications is forecast to rise at a 4.11% CAGR through 2030. OEMs specify larger rim diameters, pushing tire makers into more sophisticated reinforcing fabrics and bead profiles. Fleet buyers of vans seek high-wear compounds and RFID-enabled tracking to minimize downtime, a niche where Continental and Bridgestone pilot subscription models bundling tires, sensors, and maintenance.

By Application: On-Road Share High While Off-Road Gathers Pace

In 2024, on-road usage captured 83.25% of the European tire market share. Passenger cars, buses, and freight trucks dominate paved networks across the EU. Off-road tires supporting infrastructure projects record a 5.18% CAGR thanks to renewable-energy construction and agricultural mechanization. OEM earthmover loaders specify radial deep-tread designs capable of handling abrasive soils while preserving fuel efficiency.

Europe's tire market share gains in off-road segments encourage localized production. Michelin invests in Hungarian agricultural tire capacity to shorten delivery times. Meanwhile, smart tire sensors for quarry hauling trucks feed telematics dashboards, letting site managers plan replacements before catastrophic failures.

By End User: Aftermarket Commands Volumes

Aftermarket (replacement and retread) channels represented 69.04% of the European tire market share in 2024 sales and will climb at a 4.55% CAGR. Aging vehicles and better road networks lengthen annual mileage, raising replacement rates. Predictive algorithms in connected cars schedule service appointments, smoothing seasonal spikes traditionally seen before holiday travel periods.

OEM deliveries fluctuate with light-vehicle production cycles but increasingly feature sustainable compounds to satisfy automaker ESG dashboards. Retreads maintain presence in commercial fleets where cost per mile is scrutinized; EU standards ensure performance parity, bolstering acceptance among logistics firms seeking emissions credits.

By Rim Size: Mid-Range Rules as Aesthetics Upsize Wheels

Rims between 15 to 20 inches held 55.13% of the European tire market share in 2024, balancing comfort and affordability. Above-20-inch fitments rose 6.44% CAGR on SUVs and luxury EVs, emphasizing visual impact. Below-15-inch demand declined as compact-car designs adopted larger wheel wells for styling.

Upsizing challenges engineers to maintain ride compliance. Sidewall heights shrink, requiring higher cord-tension control and advanced bead fillers. Europe's tire market size for large-diameter categories benefits suppliers with low-profile expertise; Pirelli’s P-Zero Elect exemplifies growth in 22-inch EV specifications.

By Propulsion: ICE Still Leads Amid EV Upswing

Internal-combustion vehicles held 75.22% of the European tire market share in 2024. Nevertheless, battery-electric cars lead growth at a 7.13% CAGR through 2030 as stricter CO₂ rules bite. Hybrids bridge the transition, demanding low rolling resistance yet robust grip under regenerative braking.

Tire makers segment the European tire industry portfolios with EV-only sub-brands carrying foam inserts and RFID tags. Hankook’s Optimo line launches in 2025 to address middle-price tiers previously underserved, broadening consumer choice while allowing differentiated marketing.

Geography Analysis

Germany contributed 21.33% of Europe's tire market revenue in 2024 owing to its concentrated auto manufacturing base, premium-car mix, and strong replacement spending. Domestic firms such as Continental and Pirelli’s German plants capitalize on proximity to OEMs while R&D centers in Hanover and Aachen accelerate deployment of sustainable compounds. Germany’s federal programs incentivizing EV adoption underpin early demand for specialized iON and e.Primacy lines. Retail networks integrate digital scheduling that ties tire change reminders to vehicle telematics, reinforcing aftermarket stability.

Spain records the fastest 6.18% CAGR across 2025-2030. Economic rebound supports vehicle sales and the country’s export hub for Ford and Seat, boosting factory-fill volumes. Warmer winters spur all-season uptake among commuters in Madrid and Barcelona. National tourism rebounds to pre-pandemic levels, lifting rental-fleet replacement cycles. Spanish distributor alliances expand warehouse capacity near Valencia port to mitigate customs delays on Asia-origin tires.

France, Italy, and the United Kingdom each sustain high replacement demand rooted in sizeable aging car fleets. France sees rapid policy-driven EV penetration, prompting Michelin to retool Clermont-Ferrand lines toward low-noise compounds. Italy’s performance-car culture preserves summer-tire share though convenience trends chip away at seasonal changeovers. The U.K. e-commerce channel leads Europe with click-to-fit platforms capturing double-digit share. Eastern European members, notably Romania and Poland, attract fresh production investments. Nokian’s zero-emission Oradea plant will supply Central European winter tire demand and reduce lead times compared with Finnish output.

Competitive Landscape

Europe's tire market competition centers on global incumbents investing heavily in R&D while nurturing direct-to-consumer channels. Michelin, Continental, Bridgestone, and Goodyear hold the lion’s share, benefiting from iconic brands and broad OE approvals. Each pursues sustainability through internal carbon-neutral roadmaps, recycled-material targets, and transparent labeling. Continental upgrades its Portuguese Lousado plant to integrate smart sensors at scale, while Michelin codes RFID chips into every passenger tire from 2025.

Strategic divestments and brand tiering sharpen focus. Goodyear sold Dunlop rights in certain regions for USD 701 million, funding EV tire development and debt reduction. Hankook introduces the Optimo sub-brand in mid-2025 to span second-line slots without diluting flagship positioning. Chinese entrants signal plans for European production to skirt anti-dumping duties, heightening cost pressure at the budget end.

Digital disruption reshapes retail economics. Blackcircles and Delticom aggregate supply from multiple manufacturers, influencing price transparency. Manufacturers respond by launching factory-direct web shops bundled with partner fitting. Predictive-maintenance platforms such as ContiConnect deepen fleet relationships, potentially converting one-time sales into service subscriptions. Suppliers able to fuse material science, data analytics and omnichannel delivery are positioned to defend market share while capturing emerging EV and circular-economy opportunities.

Europe Tire Industry Leaders

Michelin

Continental AG

Bridgestone Corporation

The Goodyear Tire & Rubber Company

Pirelli & C. S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nokian Tyres shipped first volumes from its EUR 650 million zero-emission Oradea, Romania factory, focusing on winter and all-season lines for Central and Southern Europe.

- January 2025: Hankook announced the Optimo sub-brand launch in Q2 2025, expanding its European second-line range below premium tiers.

- June 2024: Firestone introduced the Roadhawk Winter truck range for fleets seeking lower total ownership costs.

- April 2024: Giti Tire released the Ecoroad truck and bus line featuring improved rolling-resistance coefficients.

Europe Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 – 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Off-the-Road and Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 – 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe tire market in 2025?

Europe tire market size is USD 46.55 billion in 2025 and is set to grow at a 3.26% CAGR to 2030.

Which tire type is most popular among European consumers?

All-season tires lead demand, accounting for 47.15% of 2024 volume due to convenience and milder winters.

What is driving premium pricing for EV tires?

Added vehicle weight and amplified road noise necessitate higher load indices and acoustic liners, creating a differentiated EV tire segment growing at 7.13% CAGR.

Which country is the fastest-growing European tire market to 2030?

Spain posts the highest projected CAGR of 6.18%, supported by automotive production gains and tourism-linked replacement demand.

Page last updated on: