Russia Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

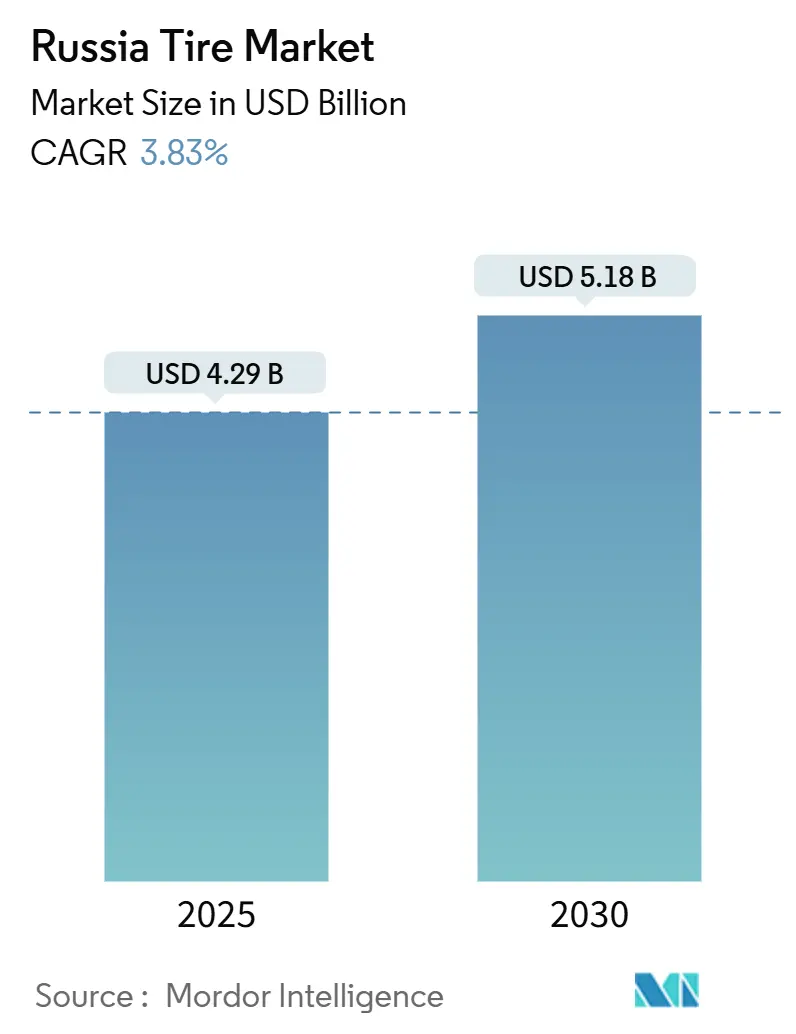

| Market Size (2025) | USD 4.29 Billion |

| Market Size (2030) | USD 5.18 Billion |

| Growth Rate (2025 - 2030) | 3.83% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Russia Tire Market Analysis by Mordor Intelligence

The Russian tire market size stands at USD 4.29 billion in 2025 and is projected to reach USD 5.18 billion by 2030, advancing at a CAGR of 3.83% during 2025-2030. Market expansion mirrors structural realignments after Western brand exits, with domestic players filling supply gaps and benefiting from import-substitution policies. Mandatory winter-tire enforcement, sustained electrification of bus and passenger fleets, and e-commerce–driven last-mile delivery collectively underpin unit demand even as high interest rates temper new-vehicle sales. Accelerated capacity additions in Kaluga, Tatarstan, and Yaroslavl secure raw-material supply, while procurement preferences under Resolution 1875 guarantee public-sector offtake[1]""Decree of the Government of the Russian Federation" GARANT-SERVIS, garant.ru. Persistent rouble volatility lifts production costs, yet localization shelters margins and keeps retail price inflation below broader automotive inflation.

Key Report Takeaways

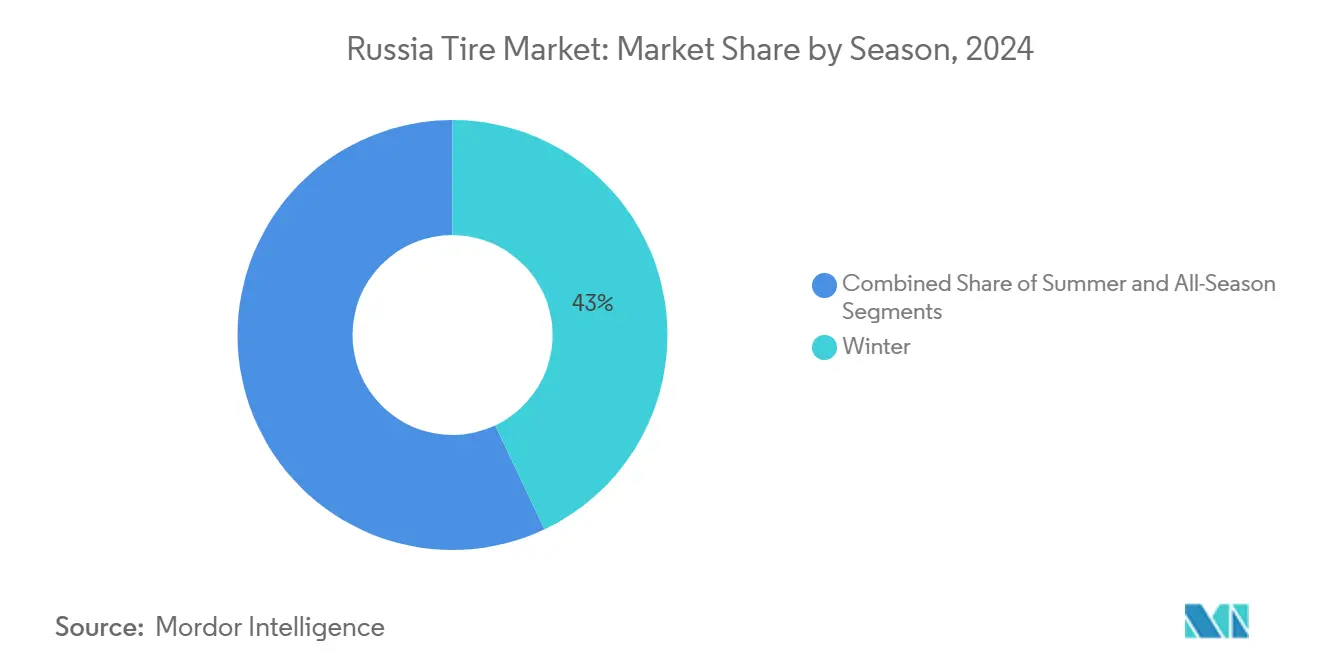

- By season, winter tires represented 42.97% of the Russian tire market share in 2024, whereas all-season tires are forecasted to expand at a 4.01% CAGR through 2030.

- By tire design, radial formats held 94.13% share of the Russian tire market size in 2024; non-pneumatic/airless products are projected to record the fastest 8.01% CAGR to 2030.

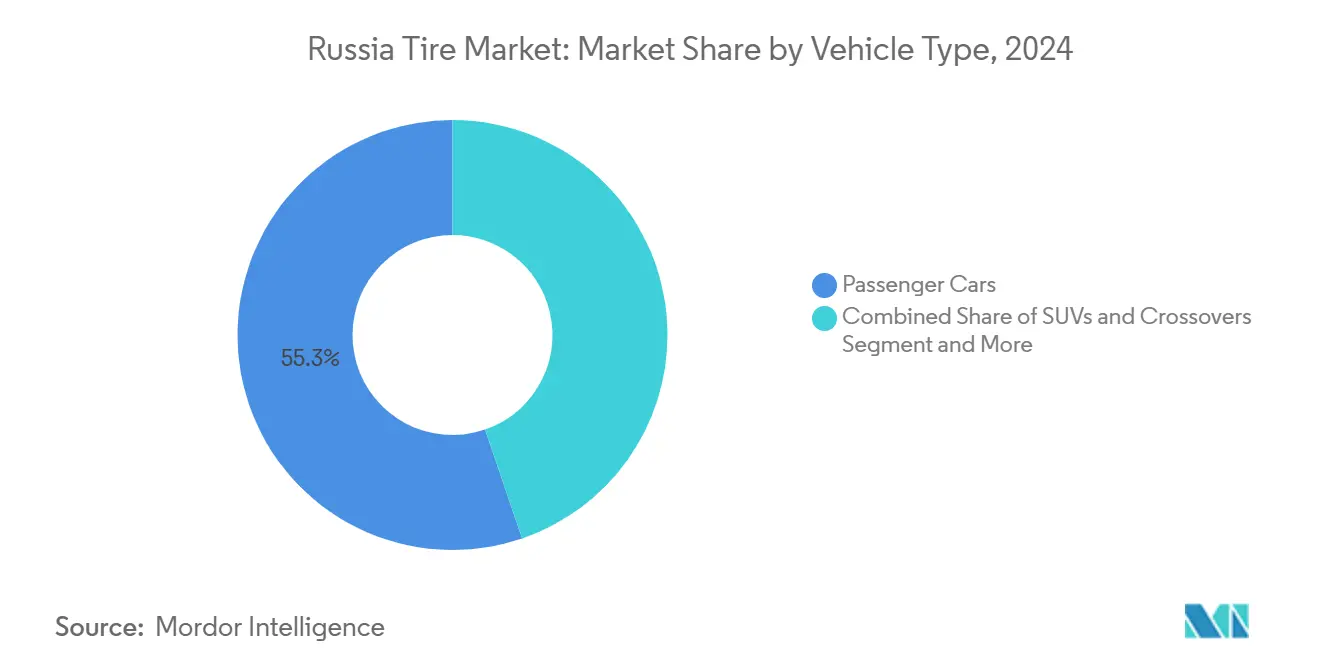

- By vehicle type, passenger cars led with 55.25% revenue share of the Russian tire market size in 2024, while SUVs and crossovers are projected to grow at 5.75% CAGR.

- By application, on-road demand accounted for 78.78% of the Russian tire market size in 2024, whereas off-road demand is projected to advance at a 4.85% CAGR.

- By end user, the aftermarket segment captured 64.46% share of the Russian tire market size in 2024 and is growing at 3.81% CAGR to 2030.

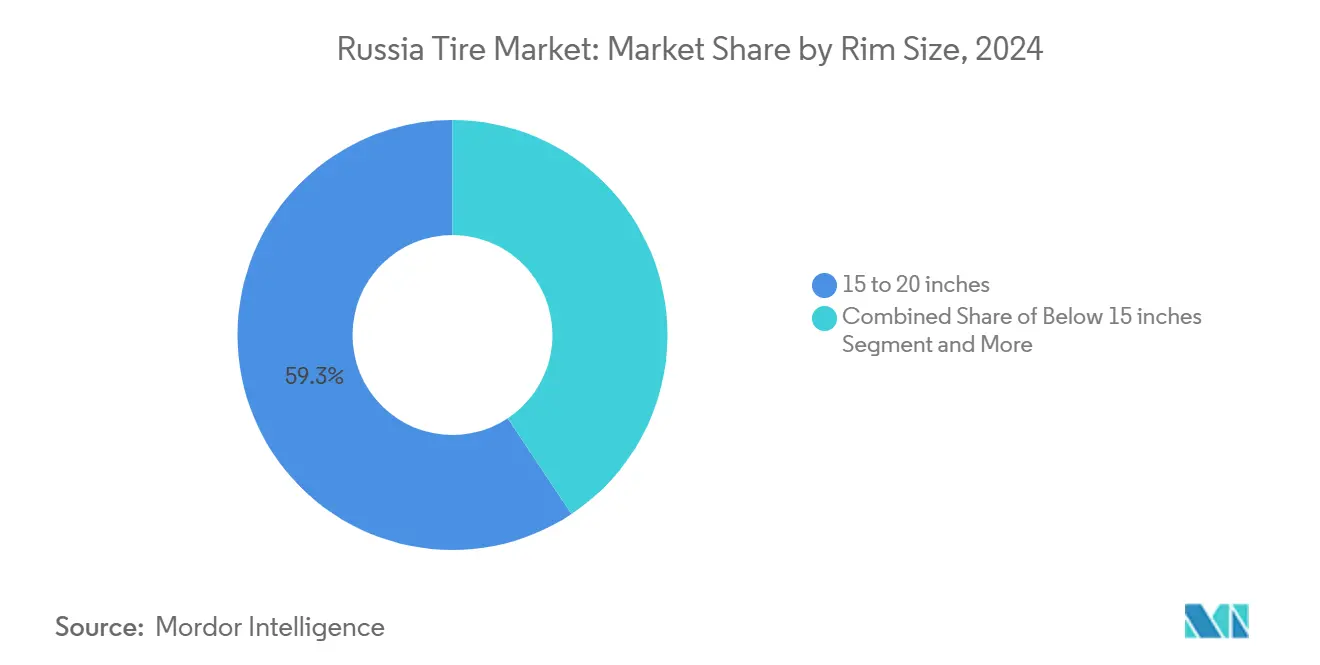

- By rim size, 15-20 inch tires commanded 59.34% share of the Russian tire market size in 2024; above-20-inch fitments are projected to post the highest 6.59% CAGR.

- By propulsion, internal-combustion vehicles dominated with 91.06% share of the Russian tire market size in 2024, yet battery-electric vehicles are projected to climb at 12.09% CAGR.

Russia Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of Buses and Cars | +1.2% | Moscow Oblast, St. Petersburg, Tatarstan | Medium term (2-4 years) |

| Domestic Tire Manufacturing Capacity | +1.0% | Kaluga Oblast, Tatarstan, Yaroslavl Oblast | Long term (≥ 4 years) |

| Surge in Last-mile E-commerce | +0.8% | Moscow Oblast, St. Petersburg, Krasnodar Krai | Short term (≤ 2 years) |

| Winter-tire Legislation and Enforcement | +0.6% | All Russian regions | Short term (≤ 2 years) |

| Adoption of All-season Tires | +0.4% | Moscow, St. Petersburg, Novosibirsk | Medium term (2-4 years) |

| Local Synthetic-rubber Output | +0.3% | Tatarstan, Bashkortostan, Omsk Oblast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Buses and Cars Needs Low-RR Tires

Electric vehicle growth in Russia is creating a new demand for tires designed specifically for EVs, even as the broader auto market slows. These tires need to perform well in cold climates and help extend driving range. Government plans to increase EV adoption are expected to further boost demand for such specialized products. Domestic battery production and expanding charging infrastructure are also supporting this shift, creating consistent opportunities for tire manufacturers. As EV usage becomes more concentrated along major travel routes, regional demand for replacement tires is likely to rise.

Expansion of Domestic Tire Manufacturing Capacity

Russia’s domestic tire manufacturing sector is expanding rapidly, driven by efforts to reduce reliance on imports. Companies like Cordiant have revived and scaled up existing facilities, benefiting from inherited infrastructure. Government policies that favor local suppliers are helping ensure steady demand for domestically produced tires. This stable order flow is encouraging investment in advanced tire segments, including those for winter and electric vehicles. Upstream growth in rubber and plastic production is also supporting this momentum.

Surge in Last-mile E-commerce Boosting LCV Tire Demand

E-commerce parcel volume continues double-digit growth, pressuring delivery fleets to expand light commercial vehicle use despite freight-rate softness. Carriers respond by maximizing asset utilization, which lengthens tire replacement intervals but raises demand for high-durability tread designs. Newly launched city-delivery crossovers improve cargo flexibility yet require performance-oriented tread patterns matched to stop-and-go wear. OEM fitments benefiting domestic producers strengthen alliances with Chinese assemblers establishing Russian CKD facilities.

Mandatory Winter-Tire Legislation and Enforcement

Federal regulations make winter compounds compulsory between December and March. Enforcement cameras now automatically identify non-compliant vehicles, boosting compliance rates and reducing seasonal inventory carryover. Technical Regulation TR TS 014/2011 stipulates minimum performance standards for winter compounds, establishing clear benchmarks for manufacturers. Extreme temperature variations across Russia's climate zones necessitate specialized formulations for different regions, supporting price premiums for locally optimized products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| International Sanctions | -1.5% | All Russian regions | Short term (≤ 2 years) |

| Rouble Volatility | -0.8% | All Russian regions | Short term (≤ 2 years) |

| Down-trading to Budget Tires | -0.6% | Siberian Federal District, Far Eastern Federal District | Medium term (2-4 years) |

| Ageing Road Infrastructure | -0.4% | Regional and municipal roads across all federal districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

International Sanctions Limiting Raw-Material Imports

EU restrictions on carbon-black and synthetic rubber imports disrupt established supply chains for key tire components. Western manufacturers, including Bridgestone, Michelin, and Continental, have completed asset sales and terminated direct relationships, complicating procurement networks. Natural rubber faces global supply constraints with production rising steadily, creating structural deficits. Alternative supply routes through Asian and Central Asian partners partially offset Western disruptions but introduce higher transaction costs, longer lead times, and quality-control challenges that compress margins.

Rouble Volatility Inflating Production Costs

Currency fluctuations against major trading partners elevate costs for imported raw materials, machinery components, and specialized additives. Automotive price increases of around 10-20% for 2025 indicate similar pressures on tire pricing and demand elasticity. Commercial fleet operators report fuel costs consuming approximately 30-35% of operating budgets while driver wages climb 20% annually, constraining discretionary spending on premium tire categories. Domestic petrochemical output growth in 2024 provides some input cost stability, though specialized compounds remain import-dependent and subject to currency-driven inflation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: Winter Dominance Reflects Climate Imperatives

Winter tires command 42.97% of the Russian tire market share in 2024, reflecting mandatory legislation and climate necessities across diverse geographic regions. The segment's dominance stems from regulatory requirements and practical necessity in a country where temperatures reach -50°C in northern regions, creating distinct seasonal replacement cycles. Summer tires maintain steady demand in southern regions and urban centers where seasonal temperature variations are less extreme, though market share faces pressure from all-season alternatives offering operational convenience.

All-season tires emerge as the fastest-growing segment at 4.01% CAGR through 2030, gaining traction among urban commercial fleets seeking to reduce inventory complexity and seasonal changeover costs. Fleet operators report total cost increases for 2025, creating pressure to consolidate tire specifications and reduce labor costs. Winter road maintenance standards under GOST 33181-2014 define five maintenance levels that influence tire performance requirements, with chemical de-icing agents used on Category I-II roads and frictional materials on Category III-V roads affecting compound selection and wear patterns.[2]"GOST 33181-2014" RGTT, russiangost.com

By Tire Design: Radial Technology Maintains Overwhelming Dominance

Radial tires capture 94.13% of the Russian tire market size in 2024, demonstrating established superiority in performance, durability, and fuel efficiency. Non-pneumatic/airless tires represent the fastest-growing design category at 8.01% CAGR through 2030, though from a minimal base, as specialized applications in construction, mining, and military vehicles drive adoption. Bias tires retain niche applications in agricultural and off-road segments where cost considerations favor traditional construction methods, though market share continues declining as radial technology costs decrease.

The overwhelming radial dominance reflects decades of technology maturation and supply chain optimization, favoring established manufacturing processes. Russian tire production demonstrates domestic manufacturing capacity focused on radial technology platforms. Airless tire development gains momentum in specialized applications where puncture resistance justifies higher initial costs, particularly in mining and construction sectors. Technical Regulation TR TS 014/2011 establishes safety requirements influencing tire performance standards, creating compliance frameworks that favor proven radial technologies over experimental designs.

By Vehicle Type: Passenger Cars Lead While SUVs Drive Growth

Passenger cars maintain 55.25% of the Russian tire market share in 2024. In contrast, SUVs and crossovers emerge as the fastest-growing category at 5.75% CAGR through 2030, driven by new model introductions and consumer preferences. Heavy commercial trucks and buses face declining tire demand as fleet operators extend replacement cycles amid elevated financing costs, with bus/truck tire production falling despite overall market growth.

New vehicle introductions for 2025 include numerous crossover and SUV models from Chinese manufacturers, including GAC GS4, Chery Tiggo 7 Pro, Omoda C7, and domestic offerings like Moskvich 8, creating replacement demand for larger wheel sizes. The commercial vehicle market experienced structural disruption, creating oversupply conditions that delay fleet renewal. Two-wheeler and specialty tire segments, including agricultural, mining, and racing applications, maintain stable niche demand, witnessing a downward trend year-over-year as farming equipment renewal slowed.

By Application: On-road Dominance with Off-road Growth Potential

In 2024, on-road applications commanded 78.78% of the Russian tire market, reflecting the predominance of passenger and commercial vehicle usage on paved networks. Off-road applications grew at a 4.85% CAGR through 2030, driven by construction, mining, and agricultural sector expansion. The on-road segment benefits from mandatory winter tire legislation and seasonal replacement cycles that create predictable demand patterns. However, it faces challenges from extended replacement intervals as consumers manage elevated tire costs.

Regional infrastructure development creates off-road tire opportunities, particularly in Siberian and Far Eastern regions, where resource extraction requires specialized compounds for extreme conditions. Defense-oriented industrial expansion in the Central, Volga, and Ural Federal Districts drives demand for construction and industrial vehicle tires as military production facilities expand. Spring road weight restrictions implemented across Russian regions from March through July create seasonal demand patterns for both on-road and off-road applications, as vehicles must obtain special permits during thaw periods. Agricultural tire demand faces headwinds from reduced equipment investment, though long-term food security priorities support eventual recovery.

By End User: Aftermarket Dominance Reflects Extended Lifecycles

The aftermarket segment captures 64.46% of the Russian tire market share in 2024 and is anticipated to grow at a 3.81% CAGR through 2030, reflecting extended vehicle lifecycles and delayed replacement patterns. OEM tire demand correlates with new vehicle production, which increased significantly in 2024, though it faces moderation from high financing costs and recycling fee increases. The aftermarket's dominance demonstrates the importance of replacement tire networks and inventory management systems serving Russia's aging vehicle fleet.

Aftermarket growth drivers include mandatory tire marking regulations effective September 2025 that require digital labeling for traceability and anti-counterfeit measures, potentially creating replacement demand as older inventory clears distribution channels. Government procurement preferences established in Resolution 1875 create protected aftermarket demand for domestic tire manufacturers serving state and municipal vehicle fleets. Retreading and tire recycling activities expand as circular economy initiatives gain momentum, with rubber crumb production facilities opening in the Moscow region. These facilities process automotive tires into construction materials, creating value recovery opportunities that extend tire lifecycle economics.

By Rim Size: Mid-range Sizes Dominate with Premium Growth

Tires for 15-20 inch rims command 59.34% of the Russian tire market size in 2024, reflecting the predominant fitment sizes for passenger cars and light commercial vehicles. Above 20-inch rim size tires grow fastest at 6.59% CAGR through 2030, driven by premium vehicle adoption and performance tire demand. Below 15-inch applications maintain steady demand in budget vehicle segments and older fleet vehicles, though market share declines as vehicle manufacturers standardize on larger wheel sizes for improved performance and aesthetic appeal.

Large rim size growth correlates with new vehicle introductions, including premium crossovers and SUVs from Chinese manufacturers, as well as domestic models like the planned Lada Iskra and Vesta-based crossover scheduled for summer 2025 presentation. Premium tire demand faces constraints from consumer down-trading amid income pressures, though specific market segments, including luxury vehicles, maintain demand for larger rim size fitments. Tire wear studies indicate urban driving conditions create higher abrasion rates compared to highway driving, with larger rim sizes potentially experiencing different wear patterns due to lower sidewall profiles and increased road contact pressures.

By Propulsion: ICE Dominance with EV Specialization Emerging

Internal-combustion vehicles maintain 91.06% of the Russian tire market share in 2024, reflecting the continued dominance of traditional powertrains. Battery-electric vehicles represent the fastest-growing propulsion segment at 12.09% CAGR through 2030. Hybrid and fuel-cell vehicles occupy a small but stable market position as transitional technologies, though they face regulatory challenges as government support measures target pure electric vehicles rather than hybrid powertrains.

EV tire demand specialization emerges despite overall market contraction, as registered electric vehicles require low rolling resistance compounds and specialized load ratings to accommodate heavier battery packs. Recycling fee increases per vehicle, effective January 2025, have priced out mass-market EV adoption while creating niche demand for specialized tires among premium buyers. Charging infrastructure expansion will concentrate replacement tire demand around major corridors and urban centers where EV adoption clusters.

Geography Analysis

Russia's tire market demonstrates pronounced regional concentration patterns reflecting economic activity, industrial development, and infrastructure investment priorities. Defense-oriented regions in the Central, Volga, and Ural Federal Districts have experienced vigorous growth as state-driven import substitution and military production expansion have created localized demand for vehicle tires and industrial rubber products. Moscow and the Central Federal District maintain the largest Russia tire market share due to population density, commercial activity, and proximity to major tire manufacturing facilities, including Cordiant's expanded Kaluga operation, at the former Continental plant. Regional procurement preferences and logistics optimization favor domestic suppliers who can provide reliable delivery across Russia's challenging geographic distances.

The Siberian and Far Eastern regions present growth opportunities driven by resource extraction, infrastructure development, and proximity to Asian supply chains, though they face constraints from transportation costs and seasonal accessibility. Tatarstan emerges as a significant regional market demonstrating regional preferences for locally-produced vehicles and tires. Spring road weight restrictions implemented across regions from March through July create seasonal demand variations, with different federal districts applying varying axle load limits that influence tire selection and replacement timing. The concentration of electric vehicle ownership in 10 regions creates geographic clustering of specialized tire demand that requires targeted distribution strategies.

Southern regions including Krasnodar Krai benefit from agricultural activity, port operations, and milder climate conditions that reduce winter tire requirements while supporting year-round commercial vehicle operations. The regional distribution of tire manufacturing capacity, with major facilities concentrated in Tatarstan, Kaluga Oblast, and Yaroslavl Oblast, creates logistics advantages for nearby markets while requiring longer supply chains for distant regions. Government industrial policy prioritizes regional development through targeted investment incentives and procurement preferences that favor domestic manufacturers with local production capabilities, creating protected market segments where regional tire demand can support capacity utilization and employment objectives in strategically important industrial centers.

Competitive Landscape

The Russian tire market exhibits moderate concentration with domestic leaders LLC TD KAMA and Cordiant Capital Inc.. At the same time, the competitive landscape undergoes a structural transformation as Western manufacturers exit and Chinese brands expand their presence. Market dynamics favor companies with domestic production capabilities, established distribution networks, and government relationships that enable participation in protected procurement channels. Strategic positioning increasingly emphasizes supply chain localization, product portfolio breadth across seasonal and vehicle segments, and service network density to serve Russia's geographic expanse and infrastructure constraints.

Technology adoption focuses on manufacturing efficiency improvements, product quality enhancement, and supply chain resilience rather than breakthrough innovations, as companies prioritize market share capture and operational stability over R&D investment. White-space opportunities emerge in specialized segments, including electric vehicle tires, premium winter compounds, and industrial applications, where technical expertise and niche positioning can command margin premiums despite overall market price pressures. Emerging disruptors include Chinese tire manufacturers who leverage cost advantages and established Asian supply chains to compete in volume segments, while domestic players defend market position through government relationships and local service capabilities.

Cordiant's acquisition and restart of former Western manufacturing facilities demonstrates consolidation strategies that leverage existing infrastructure while expanding domestic production capacity. The company's resumption of operations at the former Bridgestone factory in Ulyanovsk in early 2025 follows similar moves at Continental's Kaluga plant, establishing multi-site production capabilities that reduce logistics costs and improve regional market coverage. Domestic manufacturers benefit from preferential treatment in government procurement processes, creating protected demand channels that support capacity utilization and investment planning. The competitive environment increasingly rewards companies with integrated value chains from raw material sourcing through distribution and service, as supply chain resilience becomes a competitive differentiator amid continued international trade restrictions.

Russia Tire Industry Leaders

-

LLC TD KAMA

-

Cordiant Capital Inc.

-

Sumitomo Rubber Industries, Ltd.

-

The Goodyear Tire & Rubber Company

-

The Yokohama Rubber Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Russian tire maker JSC Cordiant announced that it has resumed commercial production at the former Bridgestone factory in Ulyanovsk.

- January 2025: Nokian Tyres returned to the Ultra High-Performance (UHP) all-season category with the launch of the Nokian Tyres Surpass AS01.

Russia Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| SUVs and Crossovers |

| Light Commercial Vehicles |

| Heavy Commercial Trucks and Buses |

| Off-the-Road and Specialty (OTR, Agri, Mining, Racing) |

| On-Road |

| Off-Road (Construction, Mining, Agriculture) |

| OEM |

| Aftermarket (Replacement and Retread) |

| Below 15 inches |

| 15 to 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| SUVs and Crossovers | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks and Buses | |

| Off-the-Road and Specialty (OTR, Agri, Mining, Racing) | |

| By Application | On-Road |

| Off-Road (Construction, Mining, Agriculture) | |

| By End User | OEM |

| Aftermarket (Replacement and Retread) | |

| By Rim Size | Below 15 inches |

| 15 to 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid and Fuel-Cell Vehicles |

Key Questions Answered in the Report

What is driving growth in the Russian tire market?

The market is primarily driven by domestic manufacturing expansion, mandatory winter tire legislation, e-commerce growth boosting light commercial vehicle demand, and specialized needs for electric vehicles requiring low rolling resistance tires.

Which tire segment has the largest market share in Russia?

Winter tires dominate with 42.97% market share due to mandatory legislation and extreme climate conditions across most Russian regions.

How have sanctions affected the Russian tire industry?

Sanctions have disrupted raw material imports and caused Western manufacturers to exit, creating opportunities for domestic producers like Cordiant and KAMA to expand market share, while also increasing production costs.

What is the forecast CAGR for the Russian tire market?

The market is projected to grow at 3.83% CAGR from 2025 to 2030, reaching USD 5.18 billion by the end of the forecast period.

Which vehicle segment shows the fastest growth for tire demand?

SUVs and crossovers represent the fastest-growing category at 5.75% CAGR through 2030, driven by new model introductions from Chinese manufacturers and domestic production expansion.

How is electrification affecting the Russian tire market?

Despite EV sales declining in 2025, the battery-electric vehicle segment shows the fastest growth at 12.09% CAGR, creating specialized demand for low rolling resistance tires that can maximize range efficiency in harsh climate conditions.

Page last updated on: