Brazil Protective Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.87 Billion |

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Protective Coatings Market Analysis by Mordor Intelligence

The Brazil Protective Coatings Market size is expected to increase from USD 0.87 billion in 2025 to USD 0.9 billion in 2026 and reach USD 1.08 billion by 2031, growing at a CAGR of 3.64% over 2026-2031. Public-sector infrastructure spending, driven by the extensive Novo Programa de Aceleração do Crescimento initiative and Petrobras’ significant capital plan, is set to bolster long-term demand for high-performance epoxy and polyurethane systems. While short-term compliance costs loom, stricter limits on volatile organic compounds under the National Environmental Council resolution and the emissions-trading framework of recent legislation are steering specifications towards low-volatile organic compound water-borne and powder chemistries. In mining hubs like Pará and Minas Gerais, investments are drawing specialty polyurea and vinyl-ester linings into ore-handling assets. Meanwhile, with numerous offshore wind projects on the auction block, there is a burgeoning demand for advanced, self-healing marine coatings. Today, competitive edge is defined by resin innovation, certified applicators, and collaborative engineering with industry giants like Petrobras, Vale, and local water utilities.

Key Report Takeaways

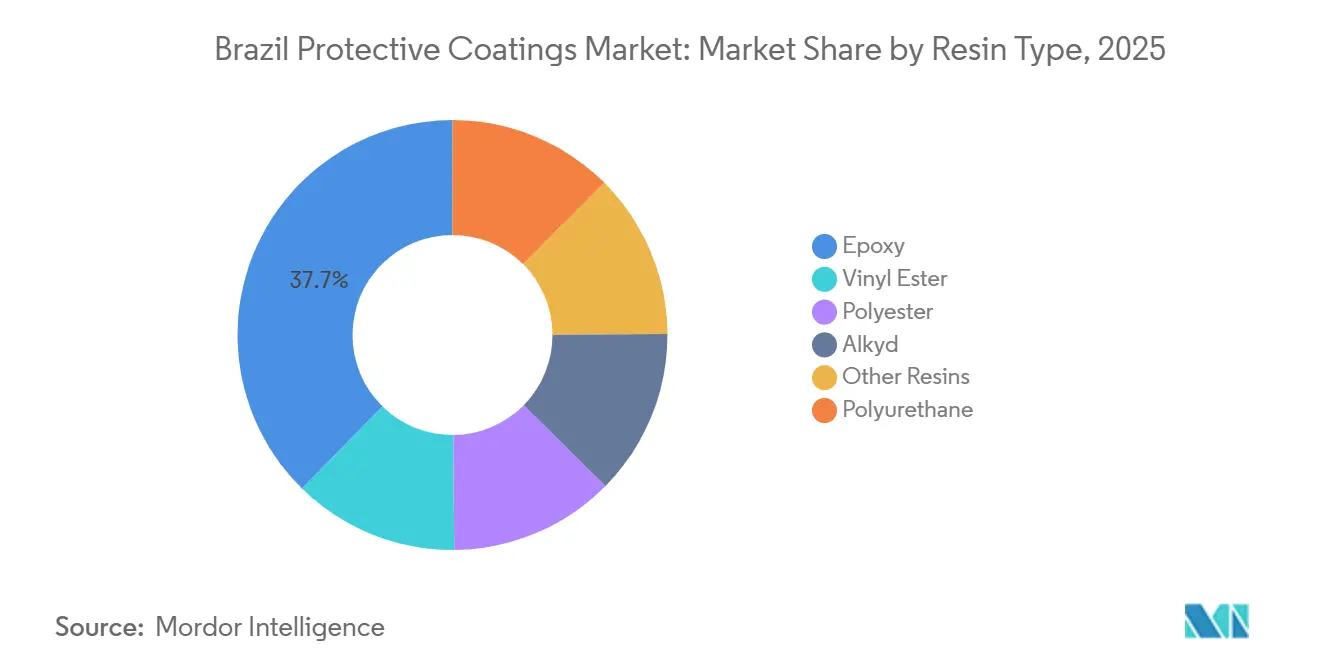

- By resin type, epoxy held 37.66% of the Brazil protective coatings market share in 2025; polyurethane is projected to advance at a 5.13% CAGR over 2026-2031.

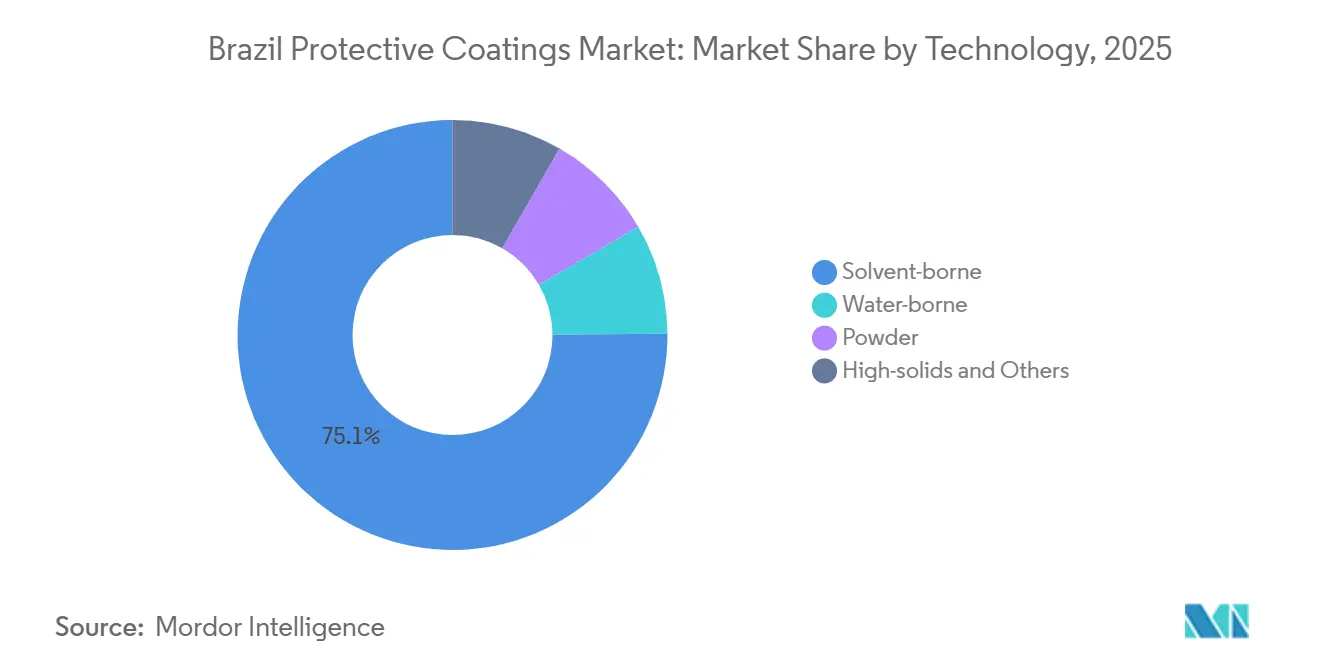

- By technology, solvent-borne products accounted for 75.09% of the Brazil protective coatings market size in 2025, while water-borne systems are forecast to expand at a 4.87% CAGR over 2026-2031.

- By end-user, oil and gas commanded 29.67% share of the Brazil protective coatings market size in 2025, whereas infrastructure and construction are pacing the segment growth at a 4.70% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Protective Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure mega-projects pipeline | +1.20% | National, Southeast and North rail-port corridors | Medium term (2-4 years) |

| Shift to low-VOC water-borne and powder tech | +0.80% | National, early adoption in São Paulo and Rio industrial zones | Short term (≤ 2 years) |

| Maintenance backlog in oil, gas and power | +0.90% | Offshore Santos and Campos basins, onshore refineries | Long term (≥ 4 years) |

| Mining investments in Pará and Minas Gerais | +0.60% | North (Carajás) and Southeast (Quadrilátero Ferrífero) | Medium term (2-4 years) |

| Smart coatings for offshore wind | +0.30% | Coastal Rio Grande do Sul, Rio de Janeiro, Ceará | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Mega-Projects Pipeline Drives Sustained Coating Demand

Brazil's protective coatings market is set to thrive, bolstered by a significant federal commitment through 2025 under the New Growth Acceleration Program initiative. Key investments include substantial funding for railway concessions and highway projects, driving a rush in near-term bidding. Suppliers offering pre-qualified water-borne epoxies and high-solids polyurethanes, meeting the International Organization for Standardization durability standards without ventilation issues, stand to gain. Simultaneously, major investments in iron-ore programs fuel a heightened demand for polyurea and vinyl-ester systems, known for their resistance to acidic slurries and abrasive loads. Modernizations at airports and ports are boosting the demand for marine-grade coatings. This shift is steering specifiers away from traditional solvent-borne alkyds, opting instead for compliant chemistries that promise shorter maintenance cycles. Contractors boasting local stock points and certified applicators by the Brazilian Association of Corrosion are seizing time-sensitive tenders, especially where delays incur liquidated damages.

Low-VOC Water-Borne and Powder Chemistries Gain Traction

Brazil's protective coatings market is transitioning toward water-based and powder systems, driven by the implementation of CONAMA 506/2024, which restricts the use of volatile organic compounds in industrial coatings[1]BASF, “BASF completes the sale of its Brazilian decorative paints business to Sherwin-Williams,” basf.com. Water-borne epoxies and polyurethanes are minimizing worker exposure in tight offshore spaces and curbing rework due to solvent entrapment. PPG's recent significant expansion in powder-coating highlights a global supply surge, but domestic uptake still relies on electrostatic-spray equipment and the training of operators. Addressing this need, ABRACO's coating inspection curriculum is producing inspectors who not only reduce premature failures but also bolster owner confidence. While compliance costs, which account for a portion of project coating expenses, pose challenges for smaller contractors, they simultaneously bolster the market presence of certified applicators, who can spread out their investments in monitoring and waste treatment.

Oil and Gas Maintenance Backlog Fuels Life-Extension Demand

Petrobras plans to allocate a significant portion of its 2026 budget for the maintenance of aging floating production storage and offloading units and pre-salt platforms. This initiative continues a maintenance super-cycle, supporting the use of epoxy and polyurethane. Field specifications require substantial dry-film thickness and long service life, driving the adoption of high-performance novolac epoxies and elastomeric wraps, such as WEG’s WrapX. These solutions significantly extend asset life while reducing downtime considerably. Additionally, hydrogen-pipeline pilots are revealing permeation risks. Current Brazilian codes do not address these challenges, creating opportunities for suppliers experienced with European standards to secure early trials.

Mining Investments in Pará and Minas Gerais Expand Applications

Vale's revamps at Novo Carajás and Minas Gerais are integrating specialty linings into ore tanks, conveyors, and tailings infrastructure. Field data indicates a prolonged absence of metal repairs, bolstering the case for premium polyurea membranes from a total-cost perspective. Concrete waterproofing systems, such as PENETRON CR-90, have successfully undergone extensive inspections on Carajás tailings dams, showcasing a blend of civil engineering and protective coating expertise. Investments in upstream steel coils are driving up resin demand for coil coatings. While this trend slightly reduces field-applied volumes, it simultaneously expands the domestic resin base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petrochemical raw-material prices | -0.60% | National, acute in Southeast petrochemical clusters | Short term (≤ 2 years) |

| Tightening VOC limits raising compliance outlay | -0.40% | National, zones under strict CONAMA oversight | Medium term (2-4 years) |

| Shortage of certified industrial applicators | -0.30% | National, severe in remote and offshore sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petrochemical Feedstock Volatility Compresses Margins

In 2024, Braskem's polyethylene prices experienced a significant increase, highlighting the sensitivity of resin costs to fluctuations in crude oil prices and currency values[2]United States International Trade Commission, “Corrosion-Resistant Steel Products…,” usitc.gov. Smaller manufacturers, without access to hedging tools, often find themselves renegotiating mid-project or absorbing losses. This predicament diminishes their competitiveness in fixed-price infrastructure bids. Additionally, regional freight premiums outside the Southeast further strain applicators in the North and Northeast.

VOC Compliance Costs and Labor Bottlenecks Slow Adoption

To comply with environmental thresholds set by the National Council for the Environment, system prices have increased, necessitating additional investments in new equipment. At the same time, inspectors certified under the National Association of Corrosion Engineers standards are demanding higher wages. This has led some contractors to employ uncertified crews, increasing the risk of failures and warranty claims. In response, asset owners are implementing mandatory pre-qualified applicator lists, effectively narrowing the pool of eligible contractors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance, Polyurethane Momentum

Epoxy captured 37.66% of 2025 value as the default choice for pre-salt splash-zone linings and municipal water tanks, anchoring the Brazil protective coatings market share at asset owners that prize chemical resistance and long immersion stability. Polyurethane’s forecast 5.13% CAGR over 2026 to 2031, stands out for its ultraviolet stability and abrasion resistance, especially on offshore wind towers and hydrogen pipelines. These are areas where traditional epoxies tend to chalk or crack after extended exposure. In the mining and refining sectors, niche vinyl-ester and novolac epoxies are proving their worth, adeptly handling acidic conditions and high temperatures. Meanwhile, the alkyd's market share is dwindling. This decline comes as federal bidders increasingly favor water-borne epoxies, which meet the international standards for corrosion protection service life specifications without incurring penalties related to volatile organic compounds.

Innovation is reshaping the landscape: WEG’s WrapX, a hybrid made of solid polyurethane, boasts the capability for large-area offshore patching in a short time. It also highlights the potential of resin engineering to challenge established epoxy standards. In a proactive move, hydrogen pilots are fast-tracking the qualification of epoxy-novolac and vinyl-ester systems, even in the absence of local codes. This early adoption grants suppliers, familiar with European hydrogen standards, a significant first-mover advantage.

By Technology: Solvent-Borne Legacy Yields to Water-Borne Compliance

Solvent-borne products still held 75.09% of the 2025 value, reflecting legacy Petrobras and Vale standards that reward familiar cure profiles and low equipment barriers. Yet the Brazil protective coatings market size for water-borne systems is climbing at a 4.87% CAGR over 2026 to 2031, As owners take on the costs of ventilation and the liabilities associated with solvent exposure, the powder coating sector, though still modest in size, finds its footing. This is largely due to a surge in demand from appliances and motors, where claims of zero volatile organic compound emissions resonate with Environmental, Social, and Governance objectives. Meanwhile, high-solids single-coat epoxies are emerging as a solution, providing reduced volatile organic compound emissions and sidestepping the humidity challenges faced by water-borne chemistries.

However, challenges persist. Training and equipment remain significant hurdles. To address this, ABRACO has introduced an inspector program designed to expedite the learning process. On another front, Tinôco showcases the potential of localized research and development. Their water-based elastomer, backed by a long-term warranty, demonstrates a durability tailored for tropical climates, outpacing many imported solvent-based coatings. While the adoption of powder coatings in protective applications faces limitations due to constraints in booth size and baking temperatures, there is a notable trend. Pipe mills and modular fabrication yards are venturing into using a dual-layer powder atop fusion-bond epoxy, aiming to meet the specifications for future hydrogen services.

By End-User Industry: Oil and Gas Scale vs. Infrastructure Upswing

Oil and gas generated 29.67% of 2025 demand, led by Petrobras’ life-extension focus and Tenaris’ 81-kilometer coating contract on Mero 4 risers. Infrastructure may trail in absolute size yet is set to outperform at 4.70% CAGR over 2026 to 2031, Rail and highway concessions are driving the demand for epoxy bridge coatings and concrete sealers, especially in humid, high-salinity corridors. Following closely is the mining sector, where the demand for coatings is surging. Every upgrade to slurry tanks and tailings dams now increasingly specifies polyurea membranes, known for their long-term durability in preventing metal repairs.

Water and wastewater projects, supported by significant investments in desalination plants and infrastructure contracts over recent years, are projected to grow steadily through the forecast period. While hydrogen projects are still in their early stages, they hold strategic significance. Early pilot projects are already in need of permeation-resistant linings, drawing interest from European and Asian suppliers eager to establish local production and mitigate currency fluctuations.

Geography Analysis

In 2025, Southeast states accounted for a significant portion of total sales, driven by their strong petrochemical clusters, offshore logistics bases, and extensive infrastructure networks. In the years ahead, growth is anticipated to slow down. The North, supported by Vale’s Carajás corridor and improved rail and port facilities for iron-ore throughput, is expected to experience expansion. This growth is influenced by the maturation of assets and a decline in demand for automotive-related paints due to the increasing adoption of electric vehicles. The northeastern coastal states, which play a key role in Brazil’s offshore wind industry and benefit from desalination and hydrogen hubs, are showing steady progress, supported by financial assistance from multilateral banks.

In the South, growth remains consistent, driven by activities such as port dredging, the establishment of onshore wind farms, and the operation of agricultural-equipment plants. The Center-West region maintains stable growth, supported by infrastructure developments in ethanol and grain silos, which drive demand for polyurethane and epoxy. At the state level, São Paulo benefits from a diverse range of automotive original equipment manufacturers and petrochemical feedstocks, achieving economies of scale. However, localized specialists excel in providing technical services for bridge and metro extensions. Espírito Santo, with its internationally accredited pipe-coating yards and laboratories, has established itself as a technical hub for pre-salt projects. In contrast, Pará, which relies heavily on iron-ore exports, faces cyclical fluctuations, but steady demand for railroad maintenance coatings helps mitigate these challenges.

Competitive Landscape

The brazil protective coatings market is moderately concentrated. The focus in the technology arena is pivoting towards smart and self-healing coatings, especially those tailored for offshore wind applications. While Hempel and Jotun, with their North Sea expertise, are prominent players, local companies that offer applicator-training programs stand to benefit as auctions by the Brazilian Institute of Environment and Renewable Natural Resources ignite domestic content mandates. Sustainability is paramount: Tinôco’s long-term warranty on its water-based elastomers not only aligns with targets set by the National Council for the Environment but also secures its products on coastal steel structures, a feat harder for solvent-based systems under stringent scrutiny.

Brazil Protective Coatings Industry Leaders

Sherwin-Williams (incl. Suvinil/Coral)

Akzo Nobel N.V.

PPG Industries Inc.

Jotun A/S

Hempel A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: BASF had sold its Brazilian decorative paints division to Sherwin-Williams for a hefty USD 1.15 billion. This transaction not only bolstered Sherwin-Williams’ foothold in Brazil's coatings arena but also signified BASF's calculated withdrawal from the region's decorative paints segment. With this acquisition, Sherwin-Williams solidified its leadership stance, heightened market competition, and amplified the supply of decorative coatings, thereby altering the dynamics of the Brazilian Protective Coatings Market.

- September 2024: Vallourec bolstered its thermal-insulation pipe coating portfolio in Espírito Santo by acquiring Thermotite do Brasil for USD 17.5 million. This strategic move not only fortified Vallourec’s industrial framework but also broadened its array of protective coating solutions tailored for offshore and deepwater oil and gas endeavors in Brazil. The acquisition had amplified the local capacity for protective coatings, diversified the available solutions, heightened competition, and underscored the significance of Brazil’s offshore and industrial coatings market.

Brazil Protective Coatings Market Report Scope

Brazil protective coatings refer to specialized industrial coatings designed to protect infrastructure, machinery, pipelines, and marine assets from corrosion, abrasion, and harsh environmental conditions. This market encompasses decorative, industrial, and marine coatings, serving sectors such as oil and gas, construction, mining, and power generation. In Brazil, protective coatings are vital for extending asset lifespans, ensuring safety, and meeting regulatory standards in demanding tropical and offshore environments.

The Brazil Protective Coatings Market is segmented by resin type, technology, and end-user industry. By resin type, the market is segmented into epoxy, polyurethane, vinyl ester, polyester, alkyd, and other resins. By technology, the market is segmented into water-borne, solvent-borne, powder, high-solids, and others. By end-user industry, the market is segmented into oil and gas (upstream, downstream, hydrogen pipeline, and others), mining, power (wind energy and other power segments), infrastructure and construction, water and waste-water treatment (distribution pipeline, desalination and potable water, and industrial water infrastructure). For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Epoxy |

| Polyurethane |

| Vinyl Ester |

| Polyester |

| Alkyd |

| Other Resins |

| Water-borne |

| Solvent-borne |

| Powder |

| High-solids and Others |

| Oil and Gas (Upstream, Downstream, Hydrogen Pipeline, Others) | |

| Mining | |

| Power | Wind Energy |

| Other Power Segments | |

| Infrastructure and Construction | |

| Water and Waste-water Treatment | Distribution Pipeline |

| Desalination and Potable Water | |

| Industrial Water Infrastructure |

| By Resin Type | Epoxy | |

| Polyurethane | ||

| Vinyl Ester | ||

| Polyester | ||

| Alkyd | ||

| Other Resins | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Powder | ||

| High-solids and Others | ||

| By End-user Industry | Oil and Gas (Upstream, Downstream, Hydrogen Pipeline, Others) | |

| Mining | ||

| Power | Wind Energy | |

| Other Power Segments | ||

| Infrastructure and Construction | ||

| Water and Waste-water Treatment | Distribution Pipeline | |

| Desalination and Potable Water | ||

| Industrial Water Infrastructure | ||

Key Questions Answered in the Report

What is the size of the Brazil protective coatings market?

The Brazil protective coatings market is projected at USD 0.9 billion in 2026 and is forecast to reach USD 1.08 billion by 2031 at a 3.64% CAGR from 2026 to 2031.

Which resin is most widely used on Brazilian offshore oil platforms?

Epoxy remains the dominant resin, holding 37.66% share in 2025 thanks to its proven splash-zone and immersion durability on FPSOs and subsea assets.

What VOC regulation is driving formulation changes in Brazil?

CONAMA Resolution 506/2024 imposes stricter national VOC caps, accelerating the shift from solvent-borne to water-borne and high-solids technologies.

Where will offshore-wind projects first lift marine-coating demand?

Coastal states such as Rio Grande do Sul, Rio de Janeiro, and Ceará host the earliest 244 gigawatts of licensed capacity, with auctions slated for 2026.

Page last updated on: