Brazil Paints and Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.35 Billion |

| Market Size (2026) | USD 4.45 Billion |

| Market Size (2031) | USD 4.97 Billion |

| Growth Rate (2026 - 2031) | 2.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Paints and Coatings Market Analysis by Mordor Intelligence

The Brazil Paints and Coatings Market size is projected to expand from USD 4.35 billion in 2025 and USD 4.45 billion in 2026 to USD 4.97 billion by 2031, registering a CAGR of 2.25% between 2026 to 2031. Federal infrastructure funding under Novo Programa PAC, the rapid electrification of automotive manufacturing, and stricter volatile organic compound (VOC)-related regulations are shifting management focus from volume recovery to value capture. The market is also experiencing a geographic concentration, with Northeast housing and renewable energy projects contributing significantly to incremental demand. Margin pressures are evident as commodity resin inflation has increased input costs more rapidly than price adjustments permitted by competition. Companies with comprehensive low-VOC product portfolios, scalable compliance processes, and differentiated distribution strategies are positioned to maintain profitability as the Brazil paints and coatings market transitions into a quality-driven growth phase.

Key Report Takeaways

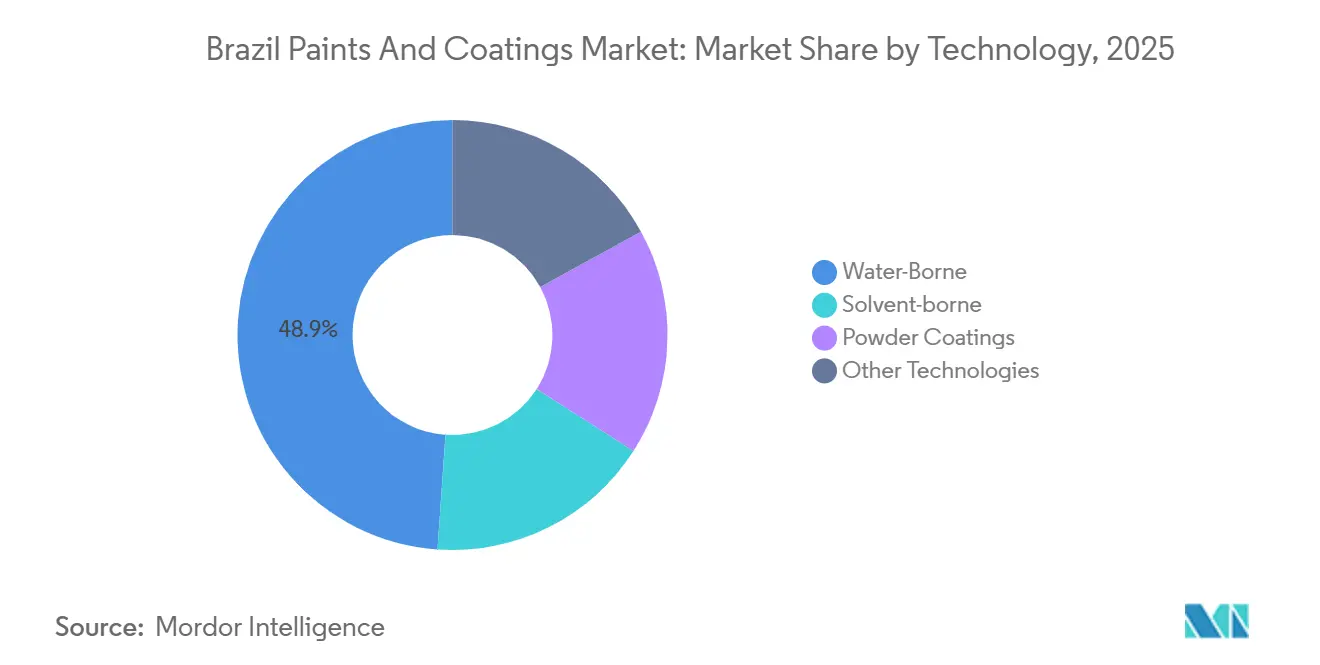

- By technology, water-borne formulations led with 48.89% of Brazil paints and coatings market share in 2025; water-borne is projected to expand at a 2.67% CAGR through 2031.

- By resin type, polyurethane accounted for the highest forecast growth at 2.81% CAGR to 2031, while acrylic dominated the 2025 value with 34.35% of the Brazil paints and coatings market size.

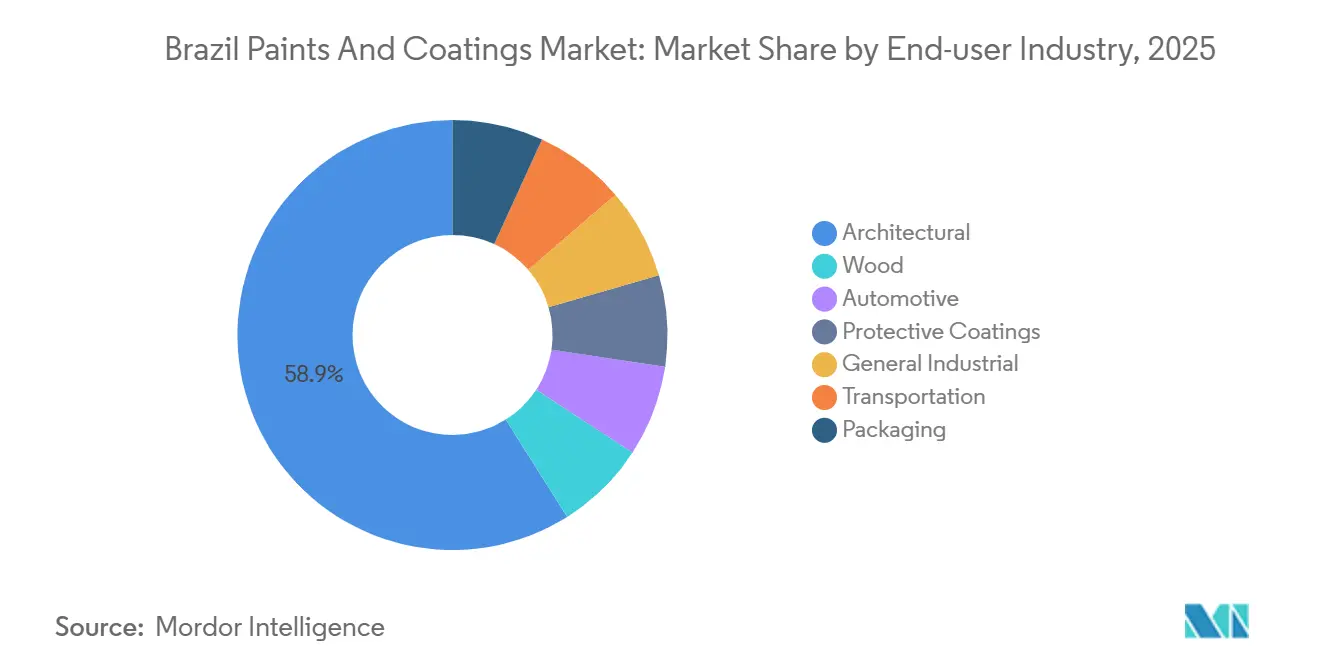

- By end-user industry, architectural coatings held a commanding 58.95% share in 2025 and are anticipated to rise at 2.77% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Paints and Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction and Infrastructure Boom (Novo PAC) | +0.7% | National, with a concentration in the Northeast, North, and Southeast transport corridors | Medium term (2-4 years) |

| Rising Automotive OEM and Electric Vehicle Investments | +0.5% | National, with manufacturing hubs in São Paulo, Minas Gerais, Bahia, and Rio de Janeiro | Medium term (2-4 years) |

| Shift to Water-borne and Powder, Driven by VOC Rules | +0.4% | National, with stricter enforcement in São Paulo, Rio de Janeiro, and industrial zones | Long term (≥ 4 years) |

| Northeast Out-performance via Housing and Renewables | +0.3% | Northeast states (Bahia, Pernambuco, Ceará, Rio Grande do Norte) | Medium term (2-4 years) |

| Expansion of E-commerce Paint Channels | +0.2% | National, with early adoption in metropolitan areas (São Paulo, Rio, Brasília) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Construction and Infrastructure Boom (Novo PAC)

By December 2024, Novo PAC had disbursed USD 142 billion, representing 53.7% of its 2023-2026 allocation. These funds are directed toward projects such as 1.3 million social-housing units, water networks, and highway expansions, all of which require significant volumes of architectural and protective paints. Priority has been given to projects that completed environmental reviews quickly, postponing some larger initiatives to 2027-2028. In response, multinational companies have established inventory hubs in the Northeast to reduce lead times. As licensing delays diminish, the Brazil paints and coatings market is expected to experience a medium-term increase in demand.

Rising Automotive OEM and Electric Vehicle Investments

Stellantis has allocated BRL 32 billion (USD 6.4 billion) through 2030 to electrify Fiat, Jeep, and Peugeot models, while BYD is investing USD 620 million in a Bahia factory capable of assembling 150,000 electric vehicles annually by 2027. Automotive coatings volumes rose by 9.7% to 36 million liters in 2024[1]Abrafati, “Brazilian Coatings Statistics 2024,” abrafati.com.br. Advancements in low-bake water-borne bases and high-solids polyurethane clears from EV production lines are driving innovation across other segments. These automotive investments are contributing to measurable growth in the Brazil paints and coatings market.

Shift to Water-borne and Powder Coatings

Law 15.022/2024 established a national inventory of chemical substances and imposed tiered fees on formulations exceeding 1 ton annually. This has increased compliance costs, encouraging buyers to adopt water-borne and powder coatings that minimize reportable solvent content. Powder coatings, while a smaller segment, benefit from zero-volatile organic compound (VOC) properties and reduced overspray waste, making them suitable for applications in appliances and metal furniture. Although reformulation expenses and applicator training extend the adoption timeline, regulatory changes are driving a sustained shift toward these technologies.

Northeast Out-performance via Housing & Renewables

The Northeast region is a key beneficiary of Novo PAC housing investments and hosts Brazil’s fastest-growing wind farm cluster. These projects require salt-fog-resistant topcoats and ultraviolet (UV)-durable finishes for wind turbine blades and towers. To reduce transportation costs and meet public procurement requirements favoring local production, suppliers are establishing regional blending plants. As a result, the Northeast is advancing faster than the national average, contributing to a positive adjustment in the Brazil paints and coatings market during the forecast period.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental-Compliance Costs | -0.3% | National, with higher impact in São Paulo, Rio de Janeiro, and industrial zones | Long term (≥ 4 years) |

| High Selic Rates Curb Renovation Spending | -0.4% | National, with acute pressure in middle-income urban households | Short term (≤ 2 years) |

| Informal Low-cost Producers Pressure Margins | -0.2% | National, with a concentration in the Northeast, North, and peri-urban self-build markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental-Compliance Costs

Under Law 15.022/2024, registration fees range from BRL 1,000 (USD 200) per substance for low volumes to BRL 50,000 (USD 10,000) for annual tonnages exceeding 1,000 tons, with additional surcharges for hazardous substances. A mid-sized formulator managing 50 raw materials could incur compliance costs of approximately USD 150,000 annually. These fixed costs impact operating margins, prompting smaller players to consider consolidation or exiting the market. In contrast, global companies with established regulatory teams can manage these expenses more effectively, enhancing their scale advantages in the Brazil paints and coatings market.

High Selic Rates Curb Renovation Spending

In June 2025, the Selic benchmark rate reached its highest level since 2016 (Central Bank of Brazil)[2]Banco Central do Brasil, “Selic Target Rate History,” bcb.gov.br. Elevated borrowing costs have discouraged home-improvement financing, leading to delays in repainting cycles and a shift toward lower-margin economy product lines. As a result, architectural revenues declined during 2025-2026, despite an increase in liters sold. With monetary policy trailing inflation, significant rate reductions are unlikely before late 2027. In the interim, sellers are relying on retail installment plans and loyalty programs to maintain their market share in the Brazil paints and coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-borne Leads the Transition

Water-borne coatings accounted for 48.89% of the Brazil paints and coatings market size in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 2.67% by 2031. This growth is supported by local volatile organic compound (VOC) regulations, consumer preference for low-odor finishes, and original equipment manufacturer (OEM) requirements for low-bake cycles. Powder coatings are gaining adoption among appliance and furniture manufacturers due to their efficient processes. Solvent-borne systems are declining in most applications but remain relevant in protective and marine niches due to their film-build and humidity tolerance.

Sherwin-Williams reflected this trend by acquiring BASF’s Suvinil brand for USD 1.15 billion in October 2025, gaining a portfolio with over 70% water-borne decorative paints. While powder coatings face limitations due to the need for curing ovens, they benefit from tax incentives tied to energy efficiency in industrial estates. Ultraviolet (UV)-cured and high-solids coatings remain specialized but command premium pricing in applications such as wood flooring and yacht refinishing, indicating potential for innovative chemistries in the Brazil paints and coatings market.

By Resin Type: Polyurethane Fastest, Acrylic Largest

Polyurethane is projected to grow at the fastest CAGR of 2.81% between 2026 and 2031, supported by the expansion of electric vehicle (EV) assembly lines that require high-gloss, chemical-resistant clear coats. Acrylic resins held a 34.35% revenue share of the Brazil paints and coatings market in 2025, maintaining their leading position due to cost-effective performance in both interior and exterior wall applications. Alkyd resins are declining as solvent restrictions tighten, while epoxy resins continue to see strong demand in flooring, pipelines, and tank linings.

Stellantis is retooling its Betim and Goiana plants to adopt two-component polyurethane systems that cure at lower temperatures, a shift expected to extend into industrial maintenance products. Polyester resins, primarily used in powder coatings, are expected to follow the growth trajectory of that sub-segment. Resin manufacturers are increasingly focusing on bio-based feedstocks, with Suvinil’s research and development (R&D) pipeline testing sugarcane-derived binders aligned with BASF’s global carbon footprint reduction goals.

By End-user Industry: Architectural Still Dominant

Architectural coatings accounted for 58.95% of the Brazil paints and coatings market share in 2025 and are expected to grow at a CAGR of 2.77% through 2031, driven by Novo PAC housing initiatives and green-building regulations in commercial real estate. Automotive coatings recorded a notable increase in volume. While their value share remains limited, this sub-segment serves as an indicator of technological advancements. Protective coatings are experiencing growing demand, supported by infrastructure projects such as bridges, rail viaducts, and offshore rigs under the federal investment plan.

Wood coatings are benefiting from strong furniture exports to North America and the European Union (EU), where buyers demand low-VOC UV systems. General industrial coatings remain highly price-sensitive, allowing regional players to compete with multinationals outside OEM supply chains. The transportation segment, including buses, trucks, and rail, is cyclical, with growth tied to fleet replacement cycles. Packaging coatings remain the smallest segment, as most beverage cans are imported pre-coated.

Geography Analysis

Brazil's paints and coatings market shows significant regional differences. The Southeast region, including São Paulo, Rio de Janeiro, and Minas Gerais, is expected to represent a substantial portion of the market size in 2025, driven by urban density and industrial activity. However, market growth in this region is stabilizing as renovation spending aligns with the Selic interest rate cycle.

The Northeast region is emerging as a key growth area. State-funded housing projects and wind-farm capacity additions are driving volume increases. Cities such as Greater Recife, Salvador, and Fortaleza are experiencing notable growth due to demand for economy water-borne interior paints specified for social housing projects. Informal suppliers face challenges in maintaining consistent quality, leading multinationals to establish blending centers in Bahia. These centers reduce order-to-delivery times, which is critical for contractor bids.

In the Southern states (Rio Grande do Sul, Santa Catarina, Paraná), specialty segments like wood stains for export furniture contribute to the region's share of the national paints and coatings market. Meanwhile, the Center-West region, known for its agribusiness activities, has shown steady growth supported by the construction of grain silos that require heavy-duty epoxy primers.

The Northern states remain less developed in terms of market penetration. Logistics challenges and lower disposable incomes limit per-capita paint consumption to about one-third of the national average. However, the rollout of solar farms near the Equator is creating demand for high-reflectivity roof coatings. This presents opportunities for suppliers capable of addressing the needs of small, dispersed job sites.

Competitive Landscape

The Brazil paints and coatings market is moderately consolidated. Sherwin-Williams’ acquisition of Suvinil increased its market share in the architectural segment, strengthening its position among key players. PPG is expanding its Performance Coatings unit in Sumaré to localize the production of automotive primers for Stellantis, aiming to reduce lead times by approximately four weeks.

In January 2026, Akzo Nobel enhanced its Recife distribution hub by integrating an e-commerce fulfillment center to address the needs of online DIY consumers. Nippon Paint entered a technology licensing agreement with a São Paulo-based powder-coating job shop, focusing on appliance Original Equipment Manufacturers (OEMs) seeking International Organization for Standardization (ISO) 14001 compliance. Domestic competitors are focusing on extensive retail networks and installment-payment options, which appeal to small contractors.

Law 15.022/2024 provides an advantage to larger players capable of managing chemical registration costs. Informal manufacturers remain active in rural markets but face potential enforcement actions as the Brazilian Institute of Environment and Renewable Natural Resources (IBAMA) intensifies digital tracking of solvent purchases. Strategic initiatives include joint Research and Development (R&D) efforts on bio-based resins, expansion into protective coatings for renewable energy assets, and the development of mobile-first color-visualization applications designed to engage homeowners during project planning.

Brazil Paints and Coatings Industry Leaders

The Sherwin-Williams Company

Akzo Nobel N.V.

PPG Industries, Inc.

BASF

WEG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Sherwin-Williams completed the acquisition of BASF's decorative paints business in Brazil, which includes the Suvinil brand. The acquisition covers production facilities in São Paulo and Rio de Janeiro, a distribution network, and a portfolio of low-volatile organic compound (VOC) formulations, strengthening its position in the paints and coatings market.

- December 2024: Brazil's federal government released a draft decree to implement Law 15,022/2024, which introduces a National Inventory of Chemical Substances. Manufacturers in industries such as paints and coatings are required to register substances produced or imported in quantities exceeding 1 ton per year and pay tiered fees determined by volume and hazard classification.

Brazil Paints and Coatings Market Report Scope

Paints and coatings are materials, available in liquid or powder form, applied to surfaces for decoration, protection, or functional purposes such as corrosion resistance or electrical conductivity. Paints are used for aesthetic purposes, whereas coatings are designed to provide durability, performance, and environmental protection, often serving as barriers against damage.

The Brazil paints and coatings market is segmented by technology, resin type, and end-user industry. By technology, the market is segmented into water-borne, solvent-borne, powder coatings, and other technologies. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and others. By end-user industry, the market is segmented into architectural, automotive, wood, protective coatings, general industrial, transportation, and packaging. The market sizes and forecasts are provided in terms of value (USD).

| Water-Borne |

| Solvent-borne |

| Powder Coatings |

| Other Technologies |

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Others |

| Architectural |

| Automotive |

| Wood |

| Protective Coatings |

| General Industrial |

| Transportation |

| Packaging |

| By Technology | Water-Borne |

| Solvent-borne | |

| Powder Coatings | |

| Other Technologies | |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Others | |

| By End-user Industry | Architectural |

| Automotive | |

| Wood | |

| Protective Coatings | |

| General Industrial | |

| Transportation | |

| Packaging |

Key Questions Answered in the Report

What is current market size of Brazil Paints And Coatings Market?

The Brazil Paints And Coatings Market size is projected to expand from USD 4.35 billion in 2025 and USD 4.45 billion in 2026 to USD 4.97 billion by 2031, registering a CAGR of 2.25% between 2026 to 2031.

Which technology segment is expanding fastest?

Water-borne coatings lead, growing at 2.67% CAGR on tightening VOC rules.

How are high Selic rates affecting paint demand?

Elevated borrowing costs delay renovations, shifting purchases toward lower-margin economy products.

Why are polyurethane resins gaining traction?

Automotive electrification and industrial maintenance demand high-gloss, chemical-resistant clear coats that polyurethane delivers.

Page last updated on: