Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

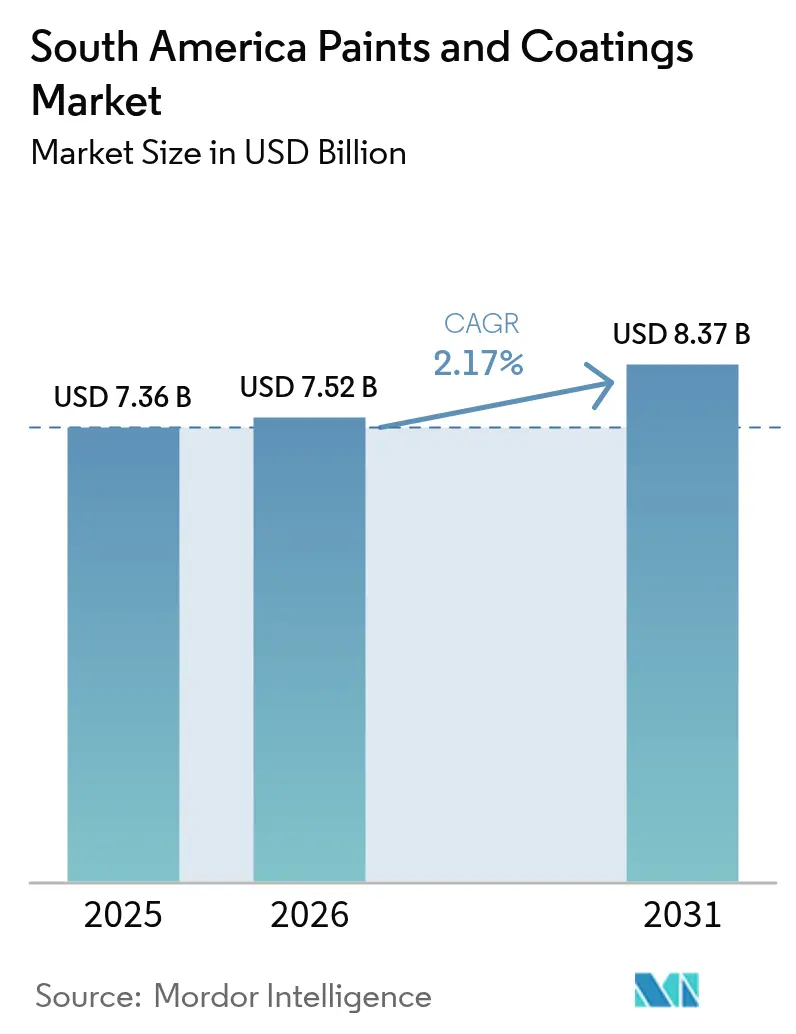

| Base Year Market Size (2025) | USD 7.36 Billion |

| Market Size (2026) | USD 7.52 Billion |

| Market Size (2031) | USD 8.37 Billion |

| Growth Rate (2026 - 2031) | 2.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Paints And Coatings Market Analysis by Mordor Intelligence

The South America Paints and Coatings Market size was valued at USD 7.36 billion in 2025 and estimated to grow from USD 7.52 billion in 2026 to reach USD 8.37 billion by 2031, at a CAGR of 2.17% during the forecast period (2026-2031). Architectural demand, tied to residential and commercial construction, continues to anchor volume; however, the automotive, battery, and cool-roof segments are expanding more rapidly and reshaping supplier priorities. Currency volatility remains the largest short-term risk, as higher import taxes on polymers inflate raw material costs and pressure margins, while stricter Mercosur VOC (Volatile Organic Compound) regulations accelerate the shift toward waterborne and powder technologies. Multinational manufacturers expand their regional footprints through mergers and production upgrades, whereas local players utilize last-mile distribution and custom color services to maintain their share in price-sensitive decorative categories. Against this backdrop, specialty opportunities emerge in lithium-processing plants, reflective roof systems for tropical cities, and digital color-matching services targeting urban DIY (Do-It-Yourself) customers.

Key Report Takeaways

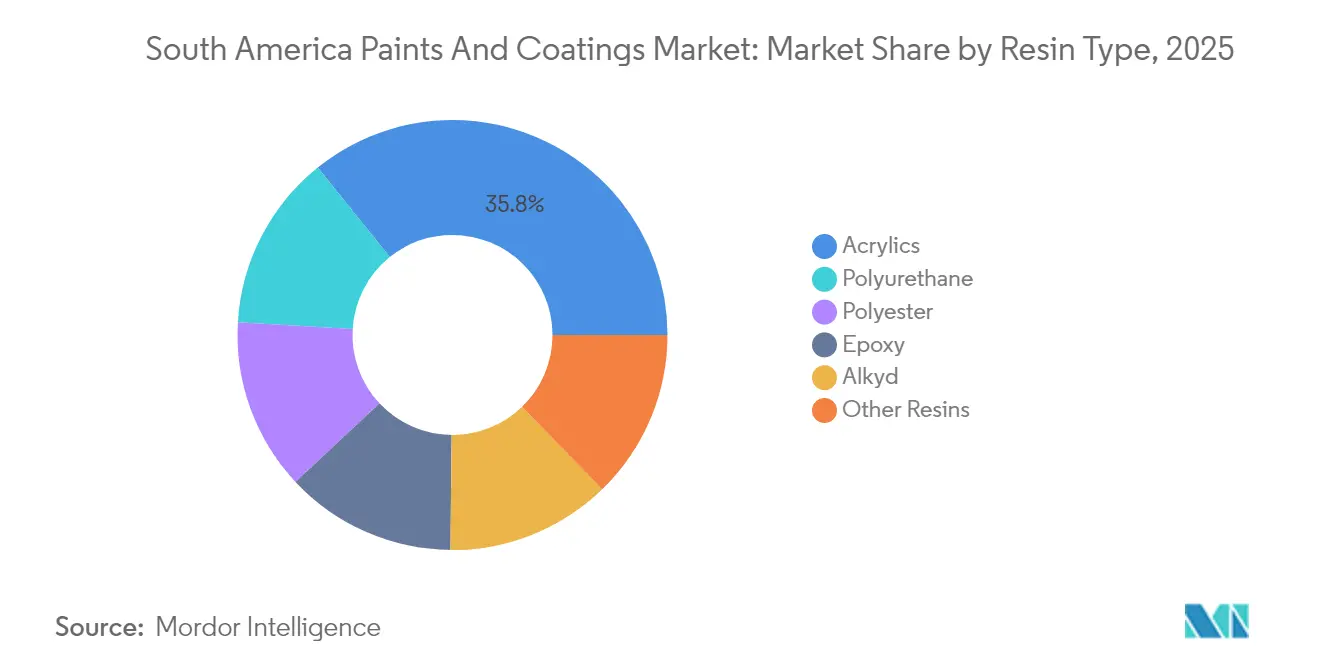

- By resin type, acrylics led with a 35.78% share of the South American paints and coatings market in 2025, while polyurethane resins are forecast to expand at a 5.62% CAGR through 2031.

- By technology, solvent-borne products accounted for 62.10% of the South American paints and coatings market size in 2025; water-borne systems are projected to post the highest CAGR at 5.85% from 2025 to 2031.

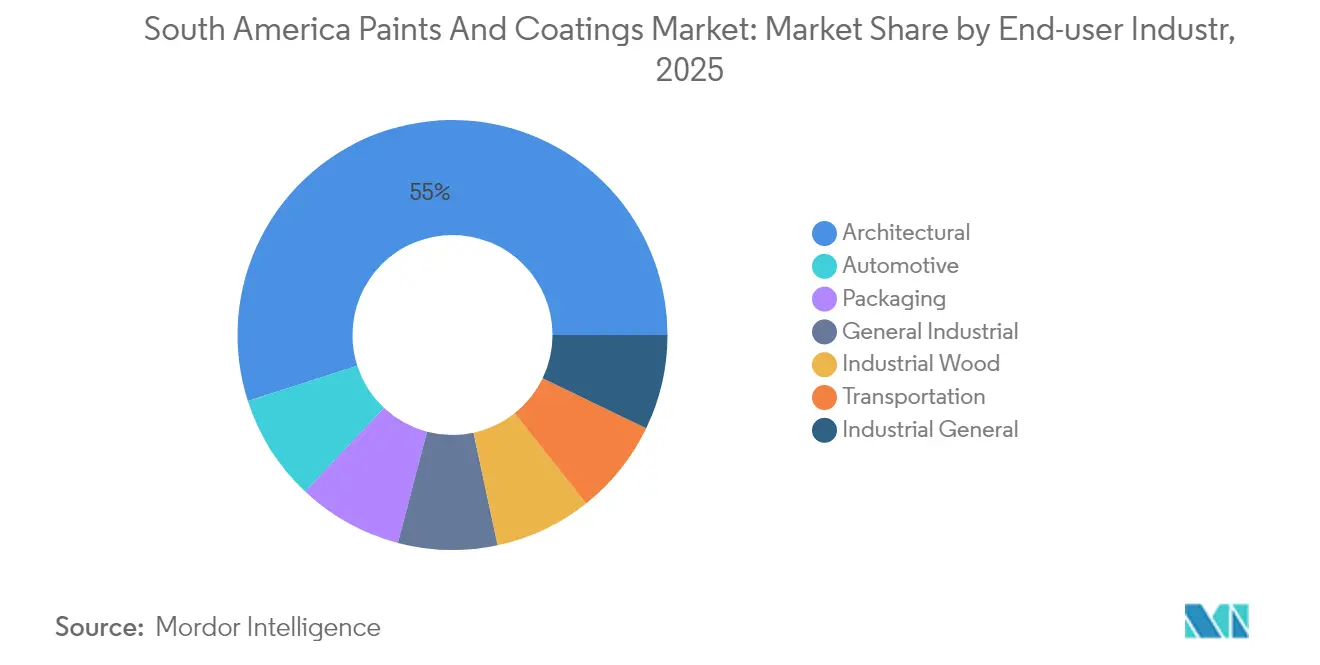

- By end-user industry, architectural applications captured 54.96% of the 2025 revenue, whereas automotive coatings are expected to advance at a 5.78% CAGR through 2031.

- By geography, Brazil held a 47.65% revenue share in 2025, while Colombia is projected to achieve a 5.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Residential and Commercial Construction Projects | +0.8% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Recovery of Regional Automotive Production and Exports | +0.6% | Brazil, Argentina, Mexico border regions | Short term (≤ 2 years) |

| Rapid Adoption of Cool-roof Reflective Coatings in Tropical Cities | +0.3% | Brazil, Colombia, Venezuela | Long term (≥ 4 years) |

| Lithium-ion Battery Gigafactory Build-outs Demanding Specialty Coatings | +0.4% | Argentina, Chile lithium triangle | Medium term (2-4 years) |

| Rise of Online DIY Micro-brands for Decorative Paints | +0.2% | Urban centers across South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Residential and Commercial Construction Projects

Elevated housing and infrastructure spending in Colombia and Chile offset Brazil’s early-2025 slowdown and underpin steady architectural volume. Social-housing programs favor low-cost acrylic emulsions, whereas commercial builders increasingly require low-emission, mold-resistant interior finishes that meet green-building criteria. Water-borne acrylic systems share the win because Brazilian life-cycle studies show superior performance in seven of eight environmental metrics compared to solvent-borne coatings[1]Federal University of Santa Catarina, “Life-Cycle Assessment of Water-borne vs. Solvent-borne Paints,” ufsc.br. Government procurements also prioritize bio-based and recycled-content formulas, prompting suppliers to broaden sustainable product lines.

Recovery of Regional Automotive Production and Exports

Brazil produced 2.5 million vehicles in 2024, a 9.7% increase, reviving OEM (Original Equipment Manufacturer) basecoat and refinish consumption. Automakers demand durable, low-VOC finishes that comply with stricter emission rules and withstand tropical climates, spurring investment in water-borne basecoats and high-solid clearcoats. PPG’s Latin America sales climbed 14.1% in 2024, driven largely by automotive OEM and refinish lines. Mexico-border assembly plants that export to North America require coatings certified to US quality standards, widening the addressable market for premium chemistries.

Rapid Adoption of Cool-Roof Reflective Coatings in Tropical Cities

Brazilian field trials confirm that high-reflectance roof coatings sustain energy savings over multiple years, though tropical humidity necessitates periodic maintenance. Utility rebates and municipal heat-island mitigation policies accelerate demand in Rio de Janeiro, Medellín, and Caracas. Suppliers formulate acrylic- and silicone-modified membranes that resist algae, maintain adhesion under high humidity, and endure intense UV (Ultraviolet) exposure. Multinationals adapt global cool-roof platforms to local substrates, while regional brands capture niche demand via cost-effective acrylic elastomers.

Lithium-ion Battery Gigafactory Build-outs Demanding Specialty Coatings

Posco’s USD 800 million lithium-hydroxide plant in Argentina exemplifies chemical-processing facilities that require low-outgassing, solvent-resistant floor and equipment coatings. Argentina’s Mining Secretariat projects that eight lithium exporters will be in operation by 2030, doubling sodium-carbonate demand and broadening the need for chemical-resistant linings. Suppliers winning this segment pair corrosion-control expertise with clean-room compliance, targeting battery and cathode-active-material lines across the lithium triangle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter VOC and Solvent-emission Limits Across Mercosur | -0.40% | Brazil, Argentina, Uruguay, Paraguay | Medium term (2-4 years) |

| Currency Volatility Inflating Imported Raw-material Costs | -0.60% | Argentina, Brazil, Colombia | Short term (≤ 2 years) |

| Shift to Composite Façade Panels Reducing Paint Demand in Premium Offices | -0.30% | Brazil, Chile, Colombia urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter VOC and Solvent-Emission Limits Across Mercosur

Regulators enforce tighter limits on architectural and industrial coatings, mirroring US Rule 1113 benchmarks[2]South Coast Air Quality Management District, “Rule 1113 Architectural Coatings,” aqmd.gov. Larger suppliers leverage global R&D to launch ultra-low-VOC lines, while smaller firms struggle with the costs of reformulation. Compliance spurs demand for water-borne and powder technologies but introduces transitional dual inventories as legacy solvent grades sell through.

Currency Volatility Inflating Imported Raw-Material Costs

Peso and real devaluations lift prices for imported pigments, additives, and resins, compressing margins and delaying projects. PPG Industries, Inc. booked a USD 20 million foreign-exchange loss in Argentina in December 2024, illustrating exposure to sudden shifts. Manufacturers hedge against currency fluctuations and localize sourcing where feasible; however, limited regional petrochemical capacity restricts substitution options for high-performance inputs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylics Dominate, Polyurethane Gains Momentum

Acrylics retained a 35.78% revenue share in 2025, anchoring the South America paints and coatings market through their versatility in water-borne architectural finishes. Polyurethane volumes are climbing at a 5.62% CAGR as lithium battery and automotive customers favor superior chemical and abrasion resistance. Epoxies serve as a protective coating for marine and metal-fabrication assets exposed to corrosive environments, whereas alkyds are being replaced by cost-competitive acrylic emulsions that now meet mid-tier durability needs. Polyester resins support growing powder-coating output for appliances and automotive trim, helping Brazil emerge as one of the fastest-expanding powder pretreatment hubs outside Asia. Specialty silicone and fluoropolymer chemistries fill niches requiring extreme UV or chemical protection on reflective roofs and process equipment.

Market momentum indicates that acrylic-emulsion suppliers are investing in bio-based monomers to differentiate themselves amid tightening VOC rules. Meanwhile, polyurethane formulators add UV-stable aliphatic systems tailored to lithium-hydroxide facilities. Epoxy vendors emphasize rapid-cure novolac blends for minimizing downtime in bulk cargo port maintenance. Thus, resin demand patterns mirror the region’s shifting industrial mix while aligning with environmental policy trajectories.

By Technology: Water-borne Shift Accelerates Regulatory Compliance

Solvent-borne products still accounted for 62.10% of 2025 revenue, yet water-borne technologies are expanding at a 5.85% CAGR, outpacing the overall South American paints and coatings market. Architectural buyers adopt water-borne acrylics that match solvent performance without odor or flammability hazards, and industrial users trial high-solid and self-crosslinking emulsions to reduce energy consumption during the baking process. Powder coatings are gaining traction in appliances and wheels, as their zero-VOC credentials align with corporate sustainability goals. UV-cured finishes remain niche but grow where faster throughput offsets higher equipment costs. Suppliers focus on rheology modifiers and reactive diluents optimized for tropical humidity, ensuring leveling and early rain resistance.

Regulators reinforce the water-borne pivot; Brazilian life-cycle assessments confirmed lower ecotoxicity and carbon intensity for aqueous products. Investment, therefore, concentrates on emulsion-polymer capacity and water-compatible metallic flakes for automotive topcoats. Concurrently, solvent-borne lines remain relevant in the refinish and heavy-duty sectors, where immediate hardness and chemical resistance remain paramount.

By End-User Industry: Automotive Challenges Architectural Dominance

Architectural demand accounted for 54.96% of 2025 sales and underpins volume leadership; however, the automotive segment is expanding at a 5.78% CAGR, driven by Brazil’s vehicle recovery and border-region export assembly. OEMs specify multi-layer water-borne systems that meet global quality and emission benchmarks. Industrial wood coatings are expected to benefit from USD 136 million in plywood and OSB (Oriented Strand Board) capacity additions, which will require UV-curable and waterborne topcoats for furniture exports. General industrial users, ranging from metal furniture to farm machinery, require anti-corrosion primers that are compatible with humid tropical storage conditions. Transportation coatings protect marine hulls and railcars that operate in coastal climates, while packaging lines utilize Bisphenol A (BPA)-free interior lacquers to comply with food-contact regulations. This diverse end-user spread cushions suppliers from cyclical swings in any single sector.

Geography Analysis

Brazil remains the anchor of the South America paints and coatings market, supported by localized resin plants, a 2.5 million-unit vehicle output in 2024, and thousands of branded retail outlets. Yet a high 15% Selic rate raises borrowing costs for developers, tempering architectural momentum. Environmental regulators intensify VOC enforcement, encouraging multinationals to introduce next-generation water-borne lines from global platforms.

Colombia posts the fastest CAGR as public–private partnerships deliver highways and social housing, and as DIY activity rises in expanding urban centers. Local distributors import colorants and additives through Atlantic ports and deliver rapid-mix services to job sites, improving supply responsiveness. Government green-building incentives reward low-emission paints, accelerating the transition to water-borne acrylics.

Argentina’s peso depreciation and inflation strain consumer budgets, but lithium project investments in Salta and Catamarca provinces require chemical-resistant floor and tank linings. Multinationals hedge FX exposure by invoicing in US dollars where permitted and by sourcing solvents from regional petrochemical complexes when available.

Chile’s copper and lithium extraction drives protective-coating needs on pipelines and tank farms in the Atacama Desert. Peru revamps Lima’s metro and port infrastructure, generating architectural and industrial demand despite modest GDP growth. Smaller economies such as Uruguay and Paraguay benefit from cross-border trade and agro-processing facilities that require durable epoxy and polyurethane finishes.

Regulatory Landscape

Across South America, tightening chemical safety and product-composition rules are shaping formulation, labeling, and documentation requirements for paints and coatings. In Brazil, Anvisa RDC No. 847 (effective April 1, 2024) introduced mandatory registration for paints and varnishes with sanitizing action (for example, products making antimicrobial or pest-control claims for real estate use). This raises the bar for substantiation and regulatory dossiers for specialty architectural SKUs.

Brazil also advanced hazardous-substance and heavy-metal compliance requirements that apply to both locally produced and imported coatings. Law No. 15.441 (June 26, 2026) sets a 90 ppm maximum lead concentration for paints and similar surface-coating materials, with limited exemptions up to 600 ppm for specific industrial or maritime uses. The law enters into force 12 months after publication, prompting accelerated reformulation and supply-chain testing. In Chile, the REACH-inspired chemicals framework under Supreme Decree No. 57/2019 continues to expand via the national chemical inventory process, including Exempt Resolution No. 9,425 (December 22, 2025) and an August 30, 2026 deadline for updating registration information for certain hazardous substances previously registered in 2024.

Value Chain Analysis

The South America paints and coatings value chain begins with raw-material inputs (resins, pigments, solvents, additives, and packaging) supplied through a mix of regional production and imports. It then progresses through formulation, blending, tinting, quality control, and filling at manufacturing sites. Brazil functions as the main regional hub for production and consumption, supported by a large domestic manufacturing base. Trade bodies such as ABRAFATI help coordinate technical standards and sector data, and Brazilian industry crossed 2.005 billion liters of production in 2025, reflecting downstream demand for binders, pigments, and packaging.

Downstream, distribution spans professional contractor channels, branded retail, home-improvement partners, and industrial direct sales for OEM and maintenance coatings. Architectural coatings dominate physical volumes in key markets, which increases the importance of tinting systems, last-mile logistics, and rapid color-mix services. Digital tools and technical service are increasingly embedded in the channel, exemplified by Sinteplast updating product recommendation tools to support distribution and selection. Regional and Ibero-American associations such as LATINPIN and ATIPAT also provide technical linkage and knowledge transfer across markets.

Competitive Landscape

The South America Paints and Coatings market is moderately consolidated. The Sherwin-Williams Company deepened its regional reach by acquiring BASF’s Suvinil decorative brand for USD 1.15 billion, adding a portfolio of color stores and contractor relationships. Strategic moves center on water-borne technology transfers, digital color platforms, and joint manufacturing to offset currency risk. Lubrizol’s USD 20 million acrylic-emulsion expansion bolsters regional binder capacity and underpins local supply of advanced low-VOC products. Suppliers are eyeing emerging niches, such as cool-roof membranes, powder primers for appliance exports, and epoxy novolac systems for lithium brine equipment.

South America Paints And Coatings Industry Leaders

PPG Industries, Inc.

Akzo Nobel N.V.

The Sherwin William Company

BASF

Renner Herrmann SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven reformulation and documentation create whitespace for suppliers that can deliver compliant, low-emission portfolios along with robust product dossiers across multiple jurisdictions. Brazil is a focal point as chemical governance moves toward a registration-based model for substances (Law No. 15.022, November 13, 2024, establishing a National Inventory of Chemical Substances with mandatory registration for substances produced or imported at 1 ton per year or more). Product-level constraints are tightening as well, including Brazil Law No. 15.441 (June 26, 2026) on lead limits in paints. Together, these changes raise demand for local technical centers, analytical testing capability, and reformulation support, especially for decorative SKUs and specialty products making sanitizing claims under Anvisa.

Consolidation and portfolio reshaping in Brazil also create avenues to gain share through channel strategy, local production, and niche industrial positions. Sherwin-Williams adjusted its Brazil operating model after the Suvinil acquisition, including the closure of over 100 company-owned stores (reported May 2026), indicating active channel redesign and potential room for distributors, independents, and alternative retail formats in decorative paints. In industrial and packaging-related coatings, capability expansion through M&A supports opportunities tied to local manufacturing footprints, as Stahl signed an agreement (June 2026) to acquire Weilburger Coatings graphics coatings business in Brazil, with plans to progressively insource production at its local site. Renner Coatings acquired Mekal Tintas (July 2026) to strengthen industrial coatings in Rio Grande do Sul, reinforcing momentum toward specialized, service-led industrial platforms.

Recent Industry Developments

- May 2026: The Sherwin-Williams Company reported ongoing integration actions in Brazil following its Suvinil acquisition, including a commercial strategy overhaul and the closure of over 100 company-owned stores. The closure reshapes route-to-market coverage and shifts competitive pressure toward distributors, contractor-focused outlets, and differentiated product and service bundles in decorative coatings.

- October 2025: Sherwin-Williams completed the acquisition of BASF's Brazilian architectural paints business (Suvinil) for USD 1.15 billion, adding production sites and an established decorative brand platform in Brazil. The transaction increased scale in the region and accelerated consolidation dynamics among multinational and local paint players.

- March 2025: Kolor Paints, Homecenter's exclusive brand, partnered with Glasst-Unpaint to launch Kolor-Unpaint in Colombia, introducing a removable decorative paint concept. The launch targeted consumer-led renovation cycles and supported higher product differentiation in a price-sensitive retail channel through new performance attributes beyond standard acrylic emulsions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of paints and coatings sold for use across South America, measured in USD and tracked across common coating types and applications where coatings are applied to protect or decorate a surface.

Scope exclusions: This sizing excludes raw materials and intermediates that are not sold as finished paints or coatings (for example, standalone pigments, resins, and solvents).

Segmentation Overview

- By Resin Type

- Acrylics

- Epoxy

- Alkyd

- Polyester

- Polyurethane

- Other Resins (Silicone, Fluoropolymer, etc.)

- By Technology

- Water-borne

- Solvent-borne

- Powder

- UV-cured

- By End-User Industry

- Architectural

- Automotive

- Industrial Wood

- Industrial General

- General Industrial

- Transportation

- Packaging

- By Geography

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building the country demand context and the main end-use signals that move coatings consumption in South America. We used public sources such as national statistics offices, customs and trade portals, central bank releases for inflation and FX, and construction and automotive associations that publish activity indicators.

To keep assumptions practical, we also reviewed listed-company filings and investor presentations that describe regional sales mix, capacity plans, and technology shifts. Patent databases and selected peer-reviewed papers helped sanity check the direction of adoption for water-borne, powder, and UV-cured systems, and an import/export shipment-level database was used selectively to cross-check trade flows when public tables were too aggregated. The sources listed above are illustrative, and many other public documents and datasets were also used for collection, validation, and clarifications.

Primary Interviews and Surveys

Primary calls and structured surveys were used to pressure test desk assumptions on price movement, mix by technology, and the split between architectural and industrial demand. Interviews included manufacturers, formulators, distributors, and large applicator and contractor-type buyers across the larger South American economies, and inputs were revisited when desk indicators and field feedback did not line up.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | APAC: 52% |

| Mid tier: 49% | Functional/Unit leaders: 42% | EMEA: 29% |

| Smaller Players: 14% | Managers: 46% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where macro demand pools were first reconstructed and then cross-checked with supplier-side reality. On the top-down side, construction activity, housing completion trends, industrial output, and vehicle production and refinish signals were translated into coating demand intensity by country, then converted to value using price and mix assumptions.

For corroboration, we ran selective bottom-up approximations using sampled supplier revenues, channel checks on distributor throughput, and typical price-per-kilogram ranges applied to estimated volumes. Totals were adjusted only when the two views diverged beyond a reasonable band. Inputs that mattered most in this market included the share shift toward water-borne systems, relative growth of architectural demand versus industrial maintenance coatings, imported product availability from trade data, and local currency depreciation patterns that change USD pricing. Forecasting used scenario analysis supported by simple trend models, where key variables such as construction spending direction, automotive build outlook, and inflation-linked price updates were confirmed with primary respondents before the final curve was locked.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, and outliers were investigated at the country and end-use level before conclusions were finalized. When a large variance showed up, we rechecked unit prices, technology mix, and whether a temporary trade spike or a short-term construction slowdown was distorting the view.

A second analyst review was used to check arithmetic consistency, year-on-year movement, and whether assumptions matched what was heard in interviews. The report is refreshed annually, and interim updates are triggered when material events occur, such as sharp FX shifts, major capacity changes, or policy moves affecting VOC compliance. Before delivery, a final pass is completed so clients receive the most current model output and narrative alignment.

Mordor Intelligence's South America Paints and Coatings Market Market Sizing Compared With Other Published Estimates

Published market values for South America paints and coatings can look far apart because the scope line is not always drawn the same way, and because price and currency handling can change the USD number materially. Timing also matters, since some publishers refresh their base year earlier than others, and that base-year choice carries into the forecast.

The table points to a wide spread that usually comes from what is counted as finished coatings, how architectural versus industrial mixes are treated, and whether importer margins and distributor markups are included in the value. Some estimates also use a single regional growth assumption, while others build country-level demand drivers that react differently to construction cycles and FX moves.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.36 B (2025) | |

| Regional Consultancy A | USD 11.45 B (2023) | Uses an earlier base year and a broader value chain cut, and the scope appears to blend in wider application value effects alongside coatings sales, which lifts the USD total versus a finished-product-only view. |

| Industry Publisher B | USD 12.42 M (2025) | Unit definition and scaling look inconsistent, since the published figure is in million USD for a market that is typically reported in billions, which makes it hard to reconcile with country demand and trade signals. |

The comparison mainly shows that scope boundaries and unit handling can move the headline number more than the underlying demand trend. The table shows that, in Mordor Intelligence's model, only finished paints and coatings revenues within South America are counted in USD terms, and pricing is tied back to country demand indicators and interview-validated mix shifts, which helps avoid inflating the total with adjacent value layers.

Key Questions Answered in the Report

How large is the South America paints and coatings market in 2026?

The market stands at USD 7.52 billion in 2026 and is projected to reach USD 8.37 billion by 2031.

Which segment is growing fastest within South America paints and coatings?

Automotive coatings exhibit the highest growth, posting a 5.78% CAGR through 2031.

Why are water-borne coatings gaining share in South America?

Stricter Mercosur VOC regulations and proven life-cycle benefits are driving a 5.85% CAGR for water-borne systems.

Which country offers the strongest growth outlook?

Colombia is forecast to grow at a 5.35% CAGR thanks to infrastructure investment and housing programs.

How is consolidation altering competitive dynamics?

Sherwin-Williams’ USD 1.15 billion purchase of BASF’s Suvinil brand and PPG’s organic expansion illustrate a trend toward greater regional scale and technology depth among multinationals.

Page last updated on: