Mexico Paints And Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.61 Billion |

| Market Size (2026) | USD 2.67 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 2.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Paints And Coatings Market Analysis by Mordor Intelligence

The Mexico Paints and Coatings Market size is projected to be USD 2.61 billion in 2025, USD 2.67 billion in 2026, and reach USD 3.01 billion by 2031, growing at a CAGR of 2.36% from 2026 to 2031. A steady pipeline of federal housing, rail, and data-center projects, combined with near-shoring-driven factory construction, anchors long-term demand. Companies are shifting product portfolios toward low-VOC water-borne systems that meet stricter SEMARNAT(Secretariat of Environment and Natural Resources) rules, while raw-material volatility—especially titanium dioxide—forces tighter procurement strategies. Competitive intensity is rising as multinationals expand retail footprints and local firms leverage price advantages, yet capacity additions by global leaders signal confidence in sustained volume growth. Digital retail adoption and a do-it-yourself culture also reshape distribution, boosting premium interior paints and color-matching technologies.

Key Report Takeaways

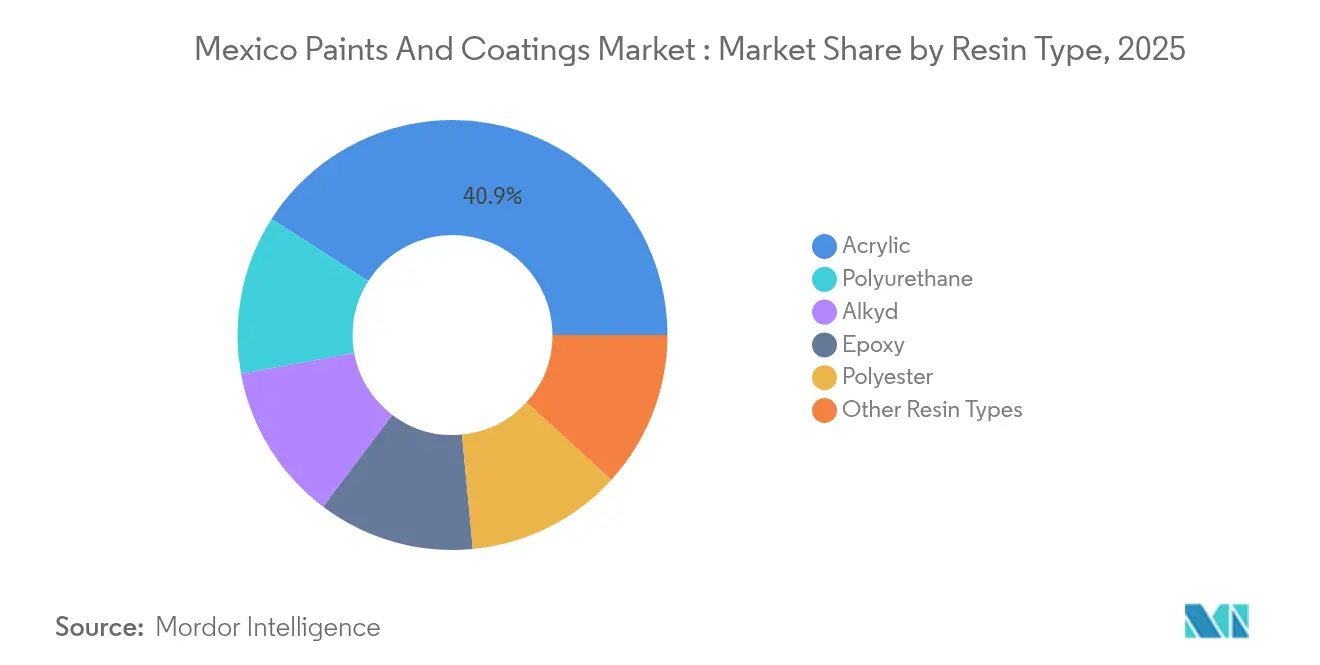

- By resin type, acrylic captured 40.92% of the Mexico paints and coatings market share in 2025, while polyurethane posted the fastest 5.42% CAGR forecast through 2031.

- By technology, water-borne systems commanded 45.98% share of the Mexico paints and coatings market size in 2025 and are set to expand at a 5.39% CAGR to 2031.

- By end-user industry, architectural applications held 51.02% revenue share in 2025; protective coatings are projected to grow at a 5.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Boom Tied to Flagship Federal Housing and Rail Programs | +1.2% | National, concentrated in central and northern states | Medium term (2-4 years) |

| Near-shoring of US Supply Chains Spurs Industrial Building Coatings | +0.9% | Northern border states, Bajío region | Long term (≥4 years) |

| Mexico’s Automotive Repaint Cycle Accelerates with EV Component Exports | +0.7% | Nuevo León, Guanajuato, Coahuila | Medium term (2-4 years) |

| Growing DIY Culture and E-commerce Paint Retail Channels | +0.5% | Urban centers | Short term (≤2 years) |

| Surge in Data-centre Construction | +0.3% | Querétaro, Mexico City area | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Infrastructure boom tied to flagship federal housing and rail programs

Federal housing plans budget MXN 752 billion (USD 37.4 billion) to erect 1.1 million homes, creating a predictable volume for interior and exterior architectural finishes. Parallel rail investments worth USD 58 billion will add more than 3,000 km of passenger lines, each requiring heavy-duty protective and maintenance coatings for tracks, stations, and rolling stock[1]Railway Gazette Editors, “Mexico Approves National Rail Expansion Plan,” railwaygazette.com. Construction employment rose 1.8% by April 2025, accelerating coatings consumption among contractors. Concentrated housing near new rail nodes improves logistics for distributors, cutting lead times and inventory costs. Multi-year program funding ensures visibility, encouraging manufacturers to sign supply agreements that stabilize factory utilization.

Near-shoring of US supply chains spurs industrial building coatings

Foreign direct investment reached USD 32.9 billion through Q3 2023, of which 48% came from first-time entrants that need new plants rather than incremental expansions. Demand for clean-room and chemical-resistant finishes is climbing as electronics and auto-parts makers specify higher performance standards. Northern border industrial absorption exceeded 3.3 million ft² in Monterrey during 2022, with comparable growth in Saltillo. Each USD 1 billion automotive investment adds up to 10 million ft² of logistics space, expanding the addressable market for floor, roof, and equipment coatings. Sustainability commitments by multinationals push low-VOC systems, accelerating technology migration across the Mexico paints and coatings market.

Mexico’s automotive repaint cycle accelerates with EV component exports

Electric-vehicle exports to the United States totaled USD 3.127 billion in H1 2024, up 171.9% year on year. Local production surpassed 250,000 electric units, spurring demand for thermal-management and electrically insulating coatings. BMW’s USD 855 million Nuevo León expansion includes a USD 540 million battery module line that specifies specialized coatings for pack housings. Component-level suppliers secured USD 2.5 billion of FDI in 2024, 35% tied to EV electronics. These shifts translate into premium product mixes and longer development cycles, raising barriers for commodity paint producers.

Growing DIY culture and e-commerce paint retail channels

Home Depot committed USD 1.3 billion to grow its Mexican store base from 138 to 150 and to roll out omnichannel tools such as image search, signaling faith in consumer repaint spending. The retailer has posted double-digit same-store sales for 14 consecutive quarters in the country. Rising disposable income and urbanization underpin a 5.3% retail CAGR forecast over 2025-2035. Paint suppliers respond with user-friendly packaging, tinting apps, and eco-labeled interior ranges that resonate with health-conscious buyers. These innovations deepen the Mexico paints and coatings market within middle-class households.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter SEMARNAT VOC and Lead Limits | -0.8% | National, tighter in major cities | Medium term (2-4 years) |

| Volatility in Titanium-dioxide Import Prices | -0.6% | Nationwide | Short term (≤2 years) |

| Grey-market Low-cost Paints Undercut Branded Margins | -0.4% | Rural and price-sensitive urban areas | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stricter SEMARNAT VOC and lead limits

NOM-172-SEMARNAT-2023 lowered PM2.5 thresholds effective July 2024 and requires further tightening by January 2026, forcing reformulation of solvent-heavy lines. The new Environmental Electronic Platform mandates digital reporting from January 2025, increasing audit frequency[2]Holland & Knight, “Mexico Launches Environmental Electronic Platform,” hklaw.com. Compliance drives capital spending on water-borne upgrades and R&D, straining smaller operators that lack financing. Export-oriented producers face US EPA (United States Environmental Protection Agency) architectural VOC caps of 150-450 g/L, aligning domestic and cross-border standards. The transition accelerates the migration to sustainable chemistries within the Mexico paints and coatings market but compresses margins during the learning curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic versatility sustains leadership

Acrylic grades held 40.92% of the Mexico paints and coatings market share in 2025, buoyed by weatherability across humid coasts and arid northlands. The segment is forecast to grow 5.28% annually to 2031 as builders favor quick-drying, color-stable finishes for large housing tracts. Alkyd products retain niches in cost-sensitive rural markets, yet SEMARNAT rules erode solvent-based demand. Polyurethane adoption is climbing in automotive and industrial floors because of high abrasion resistance. Epoxies dominate marine and petrochemical maintenance along the Gulf coast, while polyester resins underpin appliance powder lines for export. R&D is shifting toward bio-based and recycled content systems to satisfy multinational procurement policies.

Sustainability targets spur migration to water-borne acrylics, driving capital upgrades in domestic plants. Mexico, already the world’s fourth-largest polyurethane consumer, expects 5-7% volume growth in 2025, fed by OEM (original equipment manufacturer) investments that raise the Mexico paints and coatings market size for high-performance resins. Meanwhile, local startups explore soy-oil alkyds and sugar-cane acrylics, using proximity to agricultural feedstocks as a cost hedge. Resin substitution represents risk and opportunity for formulators that balance cost, durability and compliance.

By Technology: Water-borne adoption accelerates

Water-borne systems controlled 45.98% of the Mexico paints and coatings market size in 2025 and are on track for a 5.39% CAGR through 2031, supported by improved resin chemistry and lower application odor. Powder lines expand as appliance and aluminum-extrusion output climb, offering zero-VOC benefits and reclaim efficiency. Solvent-borne coatings remain essential where humidity or cure-time constraints persist, yet their share continues to slide under regulatory pressure. UV-cured products carve a furniture and automotive trim niche, prized for rapid throughput.

PPG’s USD 300 million North American upgrade includes investments at San Juan del Río to boost water-borne capacity and automation, indicating confidence in Mexican demand. Emerging barriers include higher additive costs and microbial control in storage, which require operator training and production monitoring. Nonetheless, end-users widely accept the quality of modern water-borne paints, fostering deeper penetration across the Mexico paints and coatings market.

By End-user Industry: Architectural anchors revenue while protective races ahead

Architectural uses generated 51.02% of 2025 sales, driven by the Vivienda para el Bienestar housing pipeline and continuous home-improvement spending. Protective coatings, however, will post the quickest 5.63% CAGR, fueled by petrochemical refurbishments and rail infrastructure that demands corrosion and fire protection. Automotive coatings diversify as EV battery casings, lightweight metals, and plastics require tailored chemistries. General industrial consumption benefits from near-shoring facilities that need durable floor, roof, and equipment finishes. Wood coatings grow with furniture exports, while packaging grades capture a small, expanding slice tied to food and beverage can production.

Supply-chain synergies shape segment interplay; for instance, powder lines installed for appliance exports can switch to architectural extrusion projects, optimizing capacity. Digital color tools developed for DIY (Do it yourself) retail migrate into automotive refinish, shortening cycle times. Therefore, the Mexico paints and coatings market gains resilience by serving a broad mix of construction and manufacturing end-users.

Geography Analysis

Northern border states accounted for roughly 34.70% of 2025 sales, propelled by automotive clusters in Nuevo León, Coahuila, and Chihuahua that consume specialized polyurethane, epoxy, and powder systems. Monterrey alone absorbed over 3.38 million ft² of industrial space in 2022, providing a stable order book for factory-floor coatings. The region expects a 5.05% CAGR to 2031 as U.S. near-shoring continues.

The Bajío corridor, led by Guanajuato and Querétaro, contributed close to 25.30% of the Mexico paints and coatings market in 2025 and should expand 5.62% annually. Guanajuato houses 145,000 automotive workers, reinforcing demand for OEM and refinish products. Querétaro’s emerging data-center hub layers incremental volumes of fire-resistant and EMI-shielding paints, raising the Mexico paints and coatings market size for high-performance indoor finishes.

Central Mexico—Mexico City, Puebla, and the State of Mexico—held around a 29.40% share and is projected to grow 4.05% through 2031. Passenger rail builds, airport upgrades, and mixed-use real-estate projects sustain architectural and infrastructure coatings. Coastal and southern states remain smaller today but show rising consumption tied to tourism complexes, LNG (Liquefied Natural Gas) terminals and port dredging that need marine-grade systems. Regional diversity reduces national demand volatility and underpins steady nationwide growth of the Mexico paints and coatings market.

Competitive Landscape

The Mexico Paints and Coatings market is moderately concentrated, with multinational leaders complemented by agile regional firms. After recent acquisitions, PPG commands a vast 5,200-location concessionaire network and keeps Latin America within its strategic core. M&A interest persists as entrants pursue instant scale: Neuce plans a USD 600 million powder-paint plant in Tlaxcala to serve automotive and aluminum extrusion sectors. WEG will add a BRL 100 million (USD 18.63 million) liquid-paint plant to export flows to North America. Chinese OEM growth in EVs introduces new specification hurdles, pressuring incumbents to co-develop solutions or risk share erosion. Talent scarcity in formulation science also tilts the advantage to employers with training pipelines.

Mexico Paints And Coatings Industry Leaders

PPG Industries, Inc.

The Sherwin-Williams Company

Akzo Nobel N.V.

Axalta Coating Systems

Berel Mexico

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Neuce, a prominent company in powder paint production and a key player in liquid paint, announced to invest USD 600 million to build a new plant in Tlaxcala. This initiative aligns with Neuce's expansion strategy to cater to rising demands across automotive, aluminum extrusion, steel, Polyvinyl chloride (PVC), and glass sectors.

- December 2024: WEG announced to invest BRL 100 million (USD 18.63 million) to establish a new industrial liquid paints factory in Mexico. This new facility will bolster WEG Coatings' production capacity, targeting the North and Central American markets. Spanning roughly 5,300m² (57,000 ft²), the factory is slated to commence operations in early 2026.

Mexico Paints And Coatings Market Report Scope

General industrial paints and coatings are applied on electrical equipment and appliances, sports/recreation equipment, consumer durables, and other automotive parts (brake lines, wheels, etc.) and are also applied on office buildings, warehouses, retail convenience stores, shopping malls, and residential buildings. They are also applied to wood products, which are used in furniture and fixtures, doors and windows, decks and cabinets, and other products. Similarly, some paints and coatings are used precisely according to end-user industries.

The Mexican paints and coatings market is segmented by resin type, technology, and end-user industry. By resin type, the market is segmented into acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, powder coatings, and other technologies. By end-user industry, the market is segmented into architectural, automotive, wood, protective coating, general industrial, transportation, and packaging. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

| Water-borne |

| Solvent-borne |

| Powder Coatings |

| UV-cured Coating |

| Architectural |

| Automotive |

| Wood |

| Protective Coating |

| General Industrial |

| Transportation |

| Packaging |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| Powder Coatings | |

| UV-cured Coating | |

| By End-user Industry | Architectural |

| Automotive | |

| Wood | |

| Protective Coating | |

| General Industrial | |

| Transportation | |

| Packaging |

Key Questions Answered in the Report

How large is the Mexico paints and coatings market in 2026?

The Mexico paints and coatings market size is USD 2.67 billion in 2026 with a forecast value of USD 3.01 billion by 2031.

What is the expected growth rate for Mexican paint demand through 2031?

Aggregate volume is projected to advance at a 2.36% CAGR, underpinned by housing, rail and manufacturing projects.

Which resin segment leads sales in Mexico?

Acrylic resins hold 40.92% share thanks to versatility across climates and substrates.

Why are water-borne coatings gaining momentum in Mexico?

Stricter SEMARNAT rules on VOCs and corporate sustainability targets are steering users toward low-emission water-borne products.

Where is demand growing fastest geographically?

The Bajío region, especially Guanajuato and Querétaro, shows a projected 5.62% CAGR thanks to automotive and data-center investments.

Page last updated on: