Optical Wavelength Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

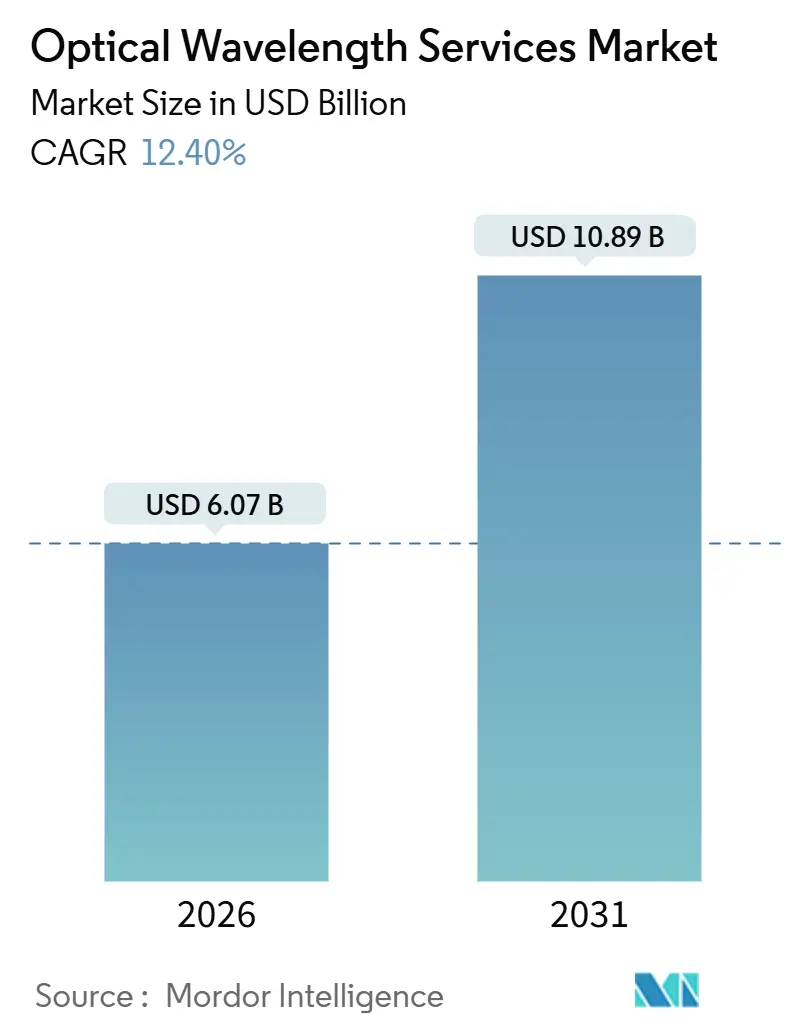

| Market Size (2026) | USD 6.07 Billion |

| Market Size (2031) | USD 10.89 Billion |

| Growth Rate (2026 - 2031) | 12.40% CAGR |

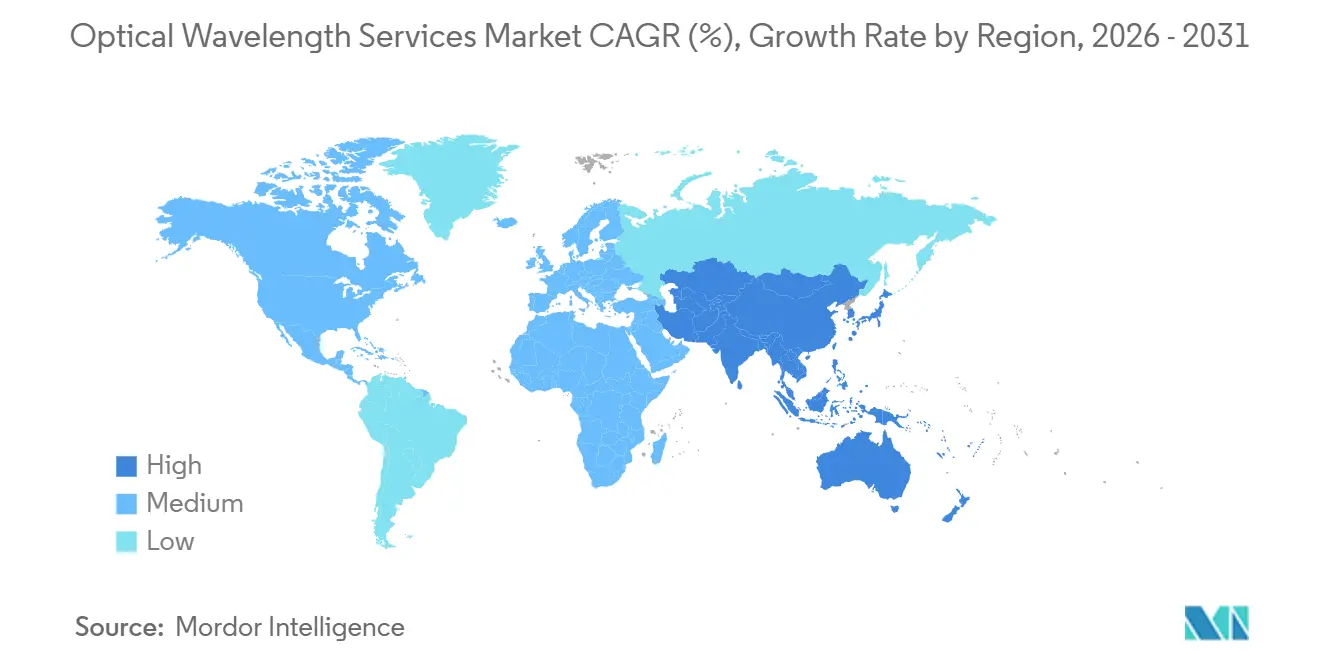

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optical Wavelength Services Market Analysis by Mordor Intelligence

The optical wavelength services market size stands at USD 6.07 billion in 2026 and is projected to reach USD 10.89 billion by 2031, registering a 12.40% CAGR over the period. The robust adoption of coherent 800 G and 1.6 T transmission, large-scale metro fiber refreshes, and widespread hyperscale data center interconnect (DCI) build-outs underpin this trajectory. Competitive differentiation increasingly revolves around automated service provisioning, open-line-system architectures, and bundled edge-compute offerings. Submarine upgrade cycles, 5G transport densification, and AI-optimized traffic engineering augment near-term demand, while sizable whitespace opportunities across Africa and secondary U.S. metros keep long-run growth prospects intact. Margin pressure for incumbents persists, however, as cloud providers self-provision dark fiber and pursue vertical integration.

Key Report Takeaways

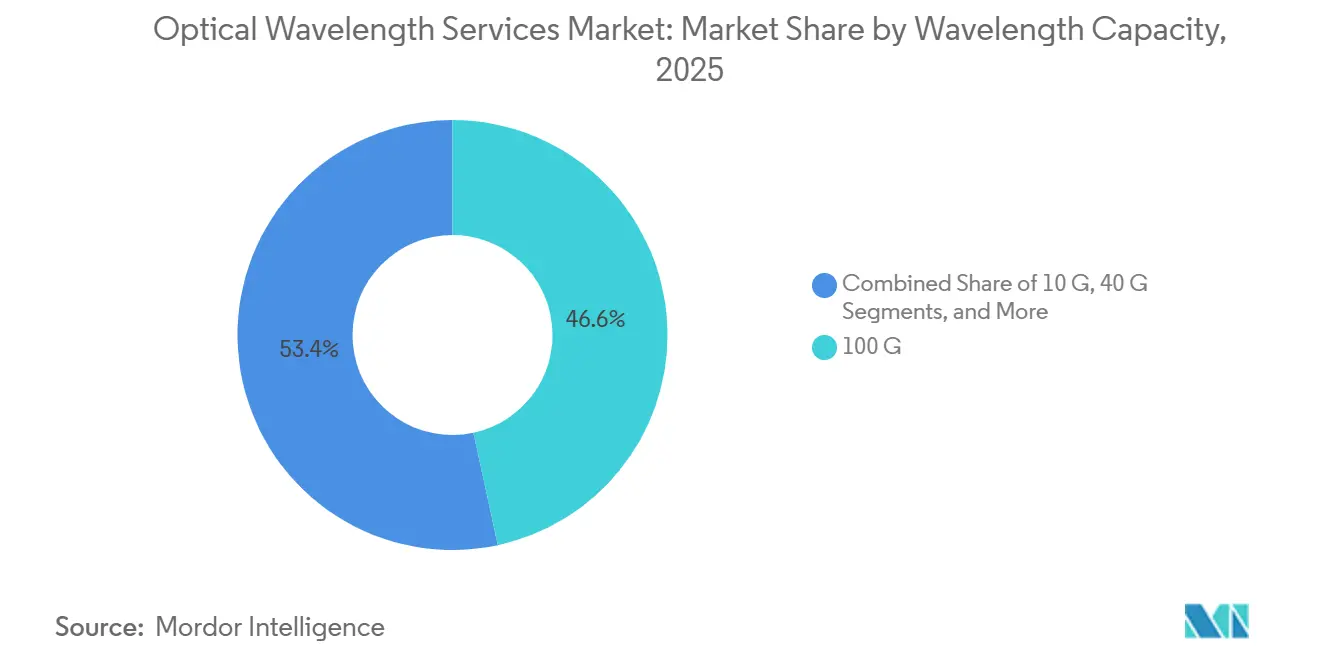

- By wavelength capacity, 100 G interfaces led with 46.63% of the optical wavelength services market share in 2025, while 800 G-and-above channels are advancing at a 13.34% CAGR to 2031.

- By service type, managed lit offerings captured 54.73% of revenue in 2025 in the optical wavelength services market; dark fiber and spectrum leasing are climbing 13.76% annually through 2031.

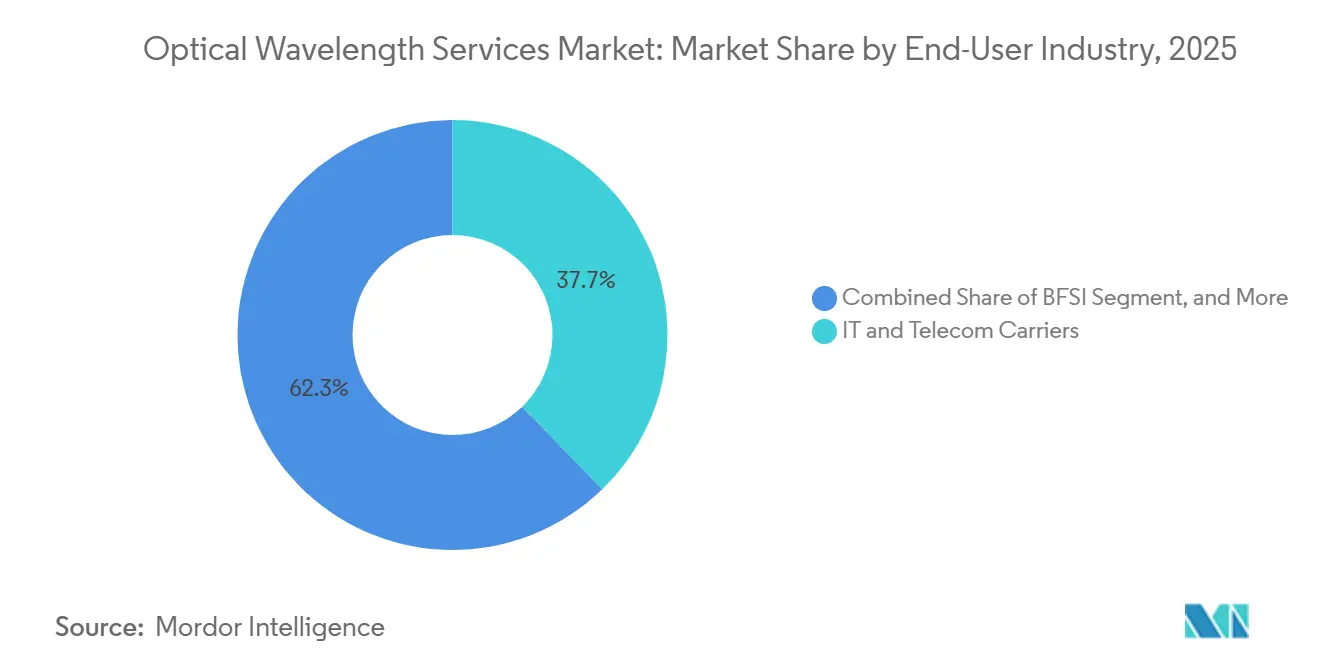

- By end-user, IT and telecom carriers held 37.73% share in 2025 in the optical wavelength services market, whereas cloud and hyperscale providers log the fastest 13.11% CAGR to 2031.

- By application, metro and access accounted for 41.82% of spending in 2025 in the optical wavelength services market; edge and inter-data-center links are scaling at a 13.33% CAGR through 2031.

- By geography, North America commanded 38.73% of revenue in 2025 in the optical wavelength services market; Asia Pacific is expanding at 13.56% a year to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Optical Wavelength Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing data traffic and bandwidth demand | +2.8% | Global | Long term (≥ 4 years) |

| Surge in hyperscale and cloud DC footprints | +2.3% | North America and Asia Pacific | Medium term (2-4 years) |

| 5G backhaul and fronthaul densification | +1.9% | Global with Asia Pacific and Europe lead | Medium term (2-4 years) |

| AI-driven traffic pattern optimization | +1.2% | North America and Europe | Short term (≤ 2 years) |

| Growth of low-latency edge interconnect sites | +1.6% | Global with metro concentration | Medium term (2-4 years) |

| Sub-sea upgrade cycles to 800G-1.6T channels | +1.1% | Global submarine routes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Data Traffic and Bandwidth Demand

Global IP traffic jumped from 4.8 zettabytes in 2025 to a forecast 8.2 zettabytes by 2030, pushing operators to migrate from 100 G to 400 G and 800 G coherent optics that multiply spectral efficiency.[1]Cisco Systems, “Annual Internet Report 2025,” cisco.com Video streaming, cloud gaming, and generative-AI inference already constitute 82% of consumer traffic, while enterprise replication workloads maintain 35% annual inter-DC bandwidth growth.[2]Akamai Technologies, “State of the Internet Report,” akamai.com Operators that guarantee sub-5 ms latency and 99.99% uptime, notably Lumen Technologies and Telia Carrier, are winning financial-services contracts across New York, London, and Tokyo. Deployments of Ciena WaveLogic 6 Extreme enable 1.6 Tb/s per wavelength, slashing cost per bit by 40% and reinforcing the optical wavelength services market’s value proposition. Looming 8K video, VR conferencing, and autonomous-vehicle telemetry will drive further uptake through 2031.

Surge in Hyperscale and Cloud DC Footprints

Hyperscalers commissioned 128 new data-center sites in 2025, raising the global count to 1,042 and jointly controlling 68% installed capacity. Each facility demands dedicated 400 G-800 G links for availability-zone replication and AI training clusters, compelling AWS to invest USD 15 billion, Microsoft Azure USD 12 billion, and Google Cloud in extensive subsea assets. Their vertical integration squeezes carrier margins and accelerates adoption of API-driven, on-demand wavelength platforms that the optical wavelength services market continues to monetize via value-added analytics and hybrid colocation bundles.

5G Backhaul and Fronthaul Densification

Operators deployed 2.8 million 5G base stations in 2025, a 47% lift over 2024, with each site requiring 10-100 Gb/s optical backhaul. Open RAN architectures demand sub-1 ms fronthaul, prompting Verizon, Vodafone, and China Mobile to secure 100 G-400 G wavelengths across metro fiber routes. Cost-sharing consortia in Europe and spectrum leasing in the United States shorten payback horizons and keep long-haul utilization high, supporting the optical wavelength services market’s sustained growth trajectory.

AI-Driven Traffic Pattern Optimization

Machine-learning platforms now govern 34% of optical capacity in North America and Europe, dynamically tuning modulation formats and rerouting traffic around impairments. Nokia’s Network Services Platform and Ciena’s Adaptive Network cut OPEX by up to 30%, while boosting throughput 12-18%, underscoring automation’s contribution to the optical wavelength services industry’s operating leverage. Early adopters in finance and content delivery report latency reductions below 10 ms, validating AI-optimized wavelengths as a differentiator in competitive bids.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for long-haul builds | -1.5% | Emerging markets and rural corridors | Long term (≥ 4 years) |

| Rapid wavelength-rate obsolescence | -1.0% | Global with legacy network concentration | Short to Medium term (≤ 4 years) |

| Scarcity of metro-core conduit in Tier-1 cities | -0.8% | North America, Europe, Asia Pacific metros | Medium term (2-4 years) |

| Lengthy rights-of-way permitting in emerging markets | -0.6% | Africa, South America, South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Long-Haul Builds

A 1,000 km terrestrial route demands USD 80,000-120,000 per km in developed markets and USD 50,000-90,000 in emerging economies, while a transoceanic cable exceeds USD 300 million. Financing is becoming more challenging as the weighted average capital cost rose from 6.2% in 2023 to 8.7% in 2025, steering operators toward metro builds and slowing underserved corridor expansion. The USD 1 billion 2Africa cable, for instance, will not be cash-positive until 2029, highlighting the financing pressures in the optical wavelength services market. Vertical integration by hyperscalers further reduces addressable wholesale demand, and regulatory ambiguities in India, Brazil, and Nigeria extend permitting by up to 24 months.

Rapid Wavelength-Rate Obsolescence

The refresh cycle compressed to 5-7 years as carriers migrate from 100 G to 400 G and 800 G, stranding older assets and eroding ROI. Windstream reports 38% of its network still on sub-100 G speeds, requiring USD 1.2 billion to upgrade. With 1.6 T optics entering trials, smaller carriers risk stranded CAPEX if traffic fails to scale as projected, putting margin compression pressure on the optical wavelength services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wavelength Capacity: Coherent 800 G Pluggables Reshape Economics

The 100 G tier held 46.63% of optical wavelength services market share in 2025, reflecting its entrenched installed base. The 800 G and above cohort, however, is rising 13.34% annually, fueled by submarine upgrades and AI-centric DCI fabrics. The optical wavelength services market size, attributable to 400 G ports, captured 18% of shipments in 2025 and is now the de facto backbone for 5G transport. Meanwhile, 10 G and 40 G links continue a 4-6% annual decline as SONET and SDH systems are retired. The shift toward 1.6 T optics by 2028, already demonstrated on Southern Cross NEXT, suggests further suppression of legacy platform economics. Smaller operators weigh leasing wholesale 400 G-800 G wavelengths against upfront investment, tailoring decisions to traffic density and access to capital.

Upgrades are also aided by regulatory support, for instance, the FCC’s 2025 pole-attachment reforms reduced deployment costs and expedited fiber strand additions, indirectly accelerating the adoption of next-gen optics. Hyperscalers’ insatiable demand for AI training bandwidth has shifted the threshold of economic viability: capacity-hungry clusters can now justify premium coherent pluggables, solidifying 800 G as the new standard within the optical wavelength services market.

By Service Type: Dark Fiber Gains as Hyperscalers Self-Provision

Managed lit wavelengths delivered 54.73% of revenue in 2025 but are losing share to dark fiber and spectrum leasing, which grow 13.76% annually as cloud giants favor control over optical line systems. The optical wavelength services market size tied to Ethernet-over-wave and optical VPN offerings remains stable, catering to enterprises needing Layer-2 flexibility and hardware-level encryption.

Open-line-system advocacy from the Telecom Infra Project reduces vendor lock-in, allowing carriers to mix equipment and shave CAPEX 20-30%. Zayo’s spectrum-as-a-service and Lumen’s bundled edge colocation exemplify how incumbents innovate to retain clientele. For customers with fewer than ten sites, operational complexity keeps managed services compelling, but hyperscalers and large banks increasingly view dark fiber as strategic, accelerating vertical integration within the optical wavelength services market.

By End-User Industry: Cloud Providers Outpace Telcos

IT and telecom carriers held 37.73% demand share in 2025, yet cloud providers record the fastest 13.11% expansion as AWS, Google, and Microsoft lease or buy fiber outright. BFSI institutions, which represented 14% of revenue in 2025, deploy dedicated wavelength services to connect trading floors in New York, London, Hong Kong, and Tokyo with sub-5-millisecond latency, enabling high-frequency trading algorithms to execute arbitrage strategies across global equity and derivatives markets.

Healthcare’s tele-imaging needs and government supercomputing projects add steady incremental growth. Media players, led by Netflix and Disney, invest in dedicated routes for 4K-8K distribution, underscoring the optical wavelength services industry’s role in content delivery. Cloud players’ aggressive fiber buys foreshadow additional margin compression for traditional carriers but simultaneously enlarge the overall optical wavelength services market size as traffic scales.

By Application: Edge Interconnect Surges Amid AI Inference Demand

Metro and access use cases commanded 41.82% spending in 2025, supplying last-mile links to enterprises and 5G small cells. Edge and inter-data-center connections, however, grow 13.33% annually as AI inference workloads and CDNs migrate nearer to users. Regional and long-haul routes, which connect major metropolitan areas and cross national borders, captured most of revenue in 2025, with Telia Carrier's trans-Atlantic fiber network carrying an estimated 18% of all IP traffic between North America and Europe.

Submarine cable applications, representing 12% of demand, experienced accelerated investment in 2025, as Meta, Google, and Microsoft co-financed the Apricot subsea system, which links Japan, Taiwan, Guam, the Philippines, and Indonesia with 800G coherent transmission capability. Edge and inter-data-center wavelengths, which interconnect colocation facilities, cloud on-ramps, and distributed GPU clusters, accounted for 14% of revenue in 2025 but are expanding rapidly as generative-AI inference workloads require sustained multi-terabit bandwidth between model-serving endpoints and vector databases.

Geography Analysis

North America’s 38.73% revenue share in 2025 rests on dense hyperscale footprints and 5G deployment. Verizon’s 15,000 C-band cell sites consumed around 22% of metro capacity, while AWS, Azure, and Google Cloud jointly leased more than 80,000 fiber-pair-kilometers across U.S. regions. Charter and Comcast expanded enterprise fiber routes by double digits, and Mexico’s near-shoring boom drove 9% optical growth in 2025. FCC pole-attachment reforms further bolster rural rollouts, keeping the optical wavelength services market resilient.

Asia Pacific, forecast at a 13.56% CAGR through 2031, benefits from China Telecom’s CNY 180 billion (USD 25 billion) 400 G-800 G upgrade plan and India’s INR 120 billion (USD 1.44 billion) BharatNet Phase III builds. Japan’s JPY 220 billion (USD 1.63 billion) urban deployments and twin SEA-H2X/Asia Link cables double regional subsea capacity, while South Korea’s AI-anchored data-centers escalate intra-DCI demand. Collectively, these initiatives reinforce Asia Pacific as the fastest-growing optical wavelength services market globally.

Europe’s 24% share in 2025 hinges on BT, Orange, and Telia Carrier’s metro extensions to serve 5G and cloud interconnects. The Gigabit Infrastructure Act, effective June 2025, simplifies rights-of-way and mandates infrastructure sharing, slashing project costs 18%.[3]European Commission, “Gigabit Infrastructure Act,” digital-strategy.ec.europa.eu Colt and euNetworks injected EUR 480 million (USD 542.4 million) into Frankfurt-Amsterdam-London-Paris routes, securing sub-5 ms latency for financial clients. Together, policy harmonization and private investments promise steady expansion for the region’s optical wavelength services market.

Middle East and Africa represents 7% revenue but registers outsized momentum after 2Africa’s April 2025 launch. Saudi Arabia’s USD 6.4 billion national 400 G project, UAE’s AED 2.8 billion (USD 756 million) 5G backhaul investment, and Liquid Intelligent Technologies’ 22,000 km network extension collectively raise capacity and catalyze terrestrial build-outs. South America’s 6% share stems from Brazil’s 8,400 km metro expansions and Argentina’s USD 420 million Buenos Aires upgrade, illustrating spreading demand across the Southern Hemisphere.

Competitive Landscape

The optical wavelength services market exhibits moderate fragmentation, with the top 10 providers, including Lumen Technologies, Verizon, AT&T, Zayo Group, and Telia Carrier, collectively controlling approximately half of global revenue in 2025, while regional operators, municipal fiber networks, and hyperscale operators' private backbones account for the remainder. Incumbent carriers face intensifying pressure from vertically integrated hyperscalers that now operate private optical networks spanning multiple continents, bypassing traditional wholesale wavelength services and compressing margins for Tier-1 providers. Lumen Technologies responded by bundling managed wavelength offerings with edge colocation and cloud on-ramp connectivity, targeting hybrid-cloud deployments that require seamless integration between on-premises data centers and public cloud regions.

Smaller pure-play fiber operators such as euNetworks and Colt Technology Services differentiate by offering sub-10-millisecond latency guarantees between financial hubs, capturing high-value accounts from investment banks and hedge funds executing high-frequency trading strategies.

White-space opportunities persist in underserved corridors, particularly intra-Africa routes where the 2Africa submarine cable's activation in 2025 opened demand for terrestrial wavelength extensions into landlocked markets, and secondary U.S. metro areas where municipal fiber networks compete with incumbent cable operators for enterprise accounts. Equipment vendors such as Nokia and Ciena are pivoting toward software-defined optical platforms and AI-driven network automation, filing over 180 patents related to coherent optics and machine-learning-based traffic engineering between 2024 and 2025.

Optical Wavelength Services Industry Leaders

Nokia Corporation

Zayo Group Holdings, Inc.

Verizon Communications Inc.

GTT Communications, Inc.

AT&T Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ciena’s WaveLogic 6 Extreme entered commercial service on Southern Cross NEXT, hitting 1 Tb/s per wavelength.

- December 2025: Microsoft Azure earmarked USD 12 billion for 16 new European availability zones with 400 G interconnects.

- November 2025: Verizon finalized 15,000 U.S. C-band sites using 100 G metro backhaul.

- Oct 2025: Google Cloud bought dark-fiber routes from Zayo to extend its North America-Europe backbone.

- September 2025: DigitalBridge acquired Vantage Data Centers’ 18,000 km fiber portfolio for USD 2.1 billion.

Global Optical Wavelength Services Market Report Scope

The Optical Wavelength Services Market Report is Segmented by Wavelength Capacity (10G, 40G, 100G, 200G, 400G and above), Service Type (Managed Lit Wavelength, Dark Fiber/Spectrum, Ethernet-over-Wave, Optical VPN), End-user Industry (IT and Telecom Carriers, Cloud and Hyperscale Providers, BFSI, Healthcare and Life Sciences, Government and Public Sector, Media and Entertainment), Application (Metro/Access, Regional/Long-haul, Sub-sea, Edge/Inter-DC), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 10 G |

| 40 G |

| 100 G |

| 200 G |

| 400 G and above |

| Managed (Lit) Wavelength |

| Dark Fiber / Spectrum |

| Ethernet‐over-Wave |

| Optical VPN |

| IT and Telecom Carriers |

| Cloud and Hyperscale Providers |

| BFSI |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Media and Entertainment |

| Metro/Access |

| Regional/Long-haul |

| Sub-sea |

| Edge/Inter-DC |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Wavelength Capacity | 10 G | ||

| 40 G | |||

| 100 G | |||

| 200 G | |||

| 400 G and above | |||

| By Service Type | Managed (Lit) Wavelength | ||

| Dark Fiber / Spectrum | |||

| Ethernet‐over-Wave | |||

| Optical VPN | |||

| By End-user Industry | IT and Telecom Carriers | ||

| Cloud and Hyperscale Providers | |||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Government and Public Sector | |||

| Media and Entertainment | |||

| By Application | Metro/Access | ||

| Regional/Long-haul | |||

| Sub-sea | |||

| Edge/Inter-DC | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving 12.40% CAGR for the optical wavelength services market through 2031?

Migration to 800 G-1.6 T optics, hyperscale DCI build-outs, 5G transport densification, and AI-driven automation collectively expand addressable demand.

Which regions will register the fastest growth?

Asia Pacific is projected at a 13.56% CAGR, led by China, India, Japan, and Southeast Asian submarine upgrades.

How are cloud providers changing procurement patterns?

AWS, Microsoft, and Google increasingly lease or acquire dark fiber, pushing carriers to offer flexible spectrum leasing and bundled edge services.

What risks could dampen deployments?

High long-haul CAPEX, rapid equipment obsolescence, metro conduit scarcity in Tier-1 cities, and slow permitting in emerging markets restrain rollouts.

Which capacity tier is growing the quickest?

800 G-and-above coherent pluggables, expanding 13.34% annually as operators refresh legacy 100 G networks.

Page last updated on: