Indonesia Satellite Communications Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

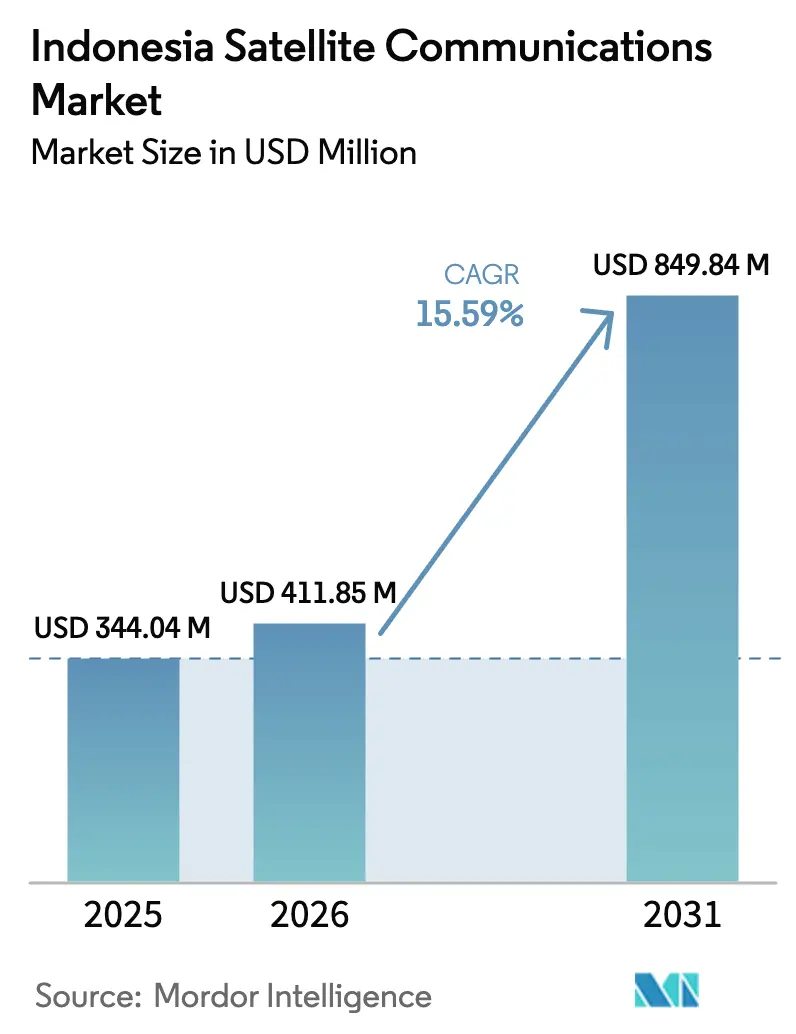

| Base Year Market Size (2025) | USD 344.04 Million |

| Market Size (2026) | USD 411.85 Million |

| Market Size (2031) | USD 849.84 Million |

| Growth Rate (2026 - 2031) | 15.59% CAGR |

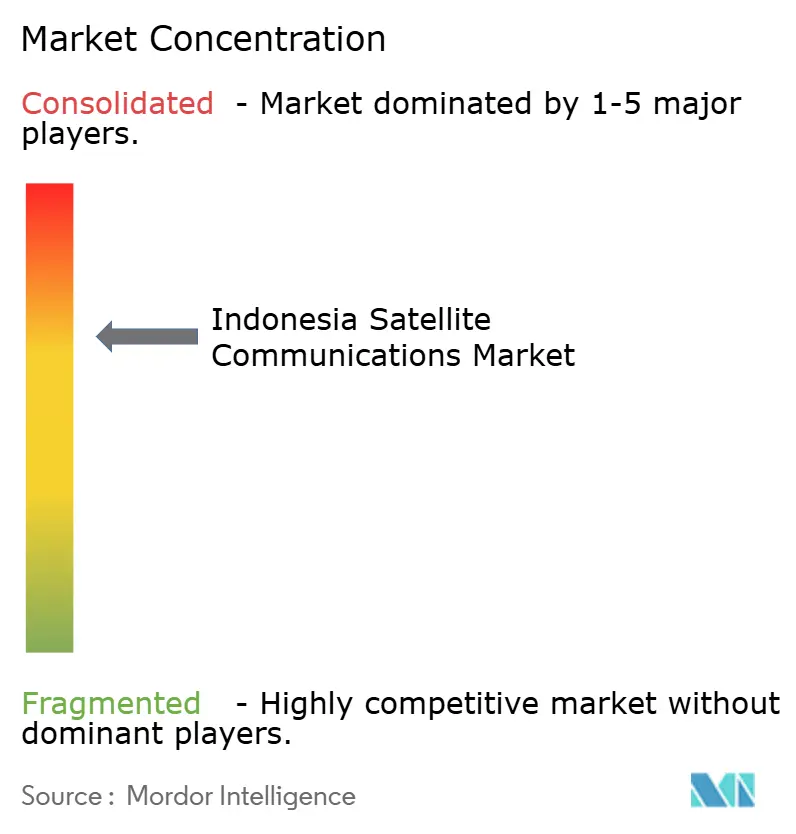

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Satellite Communications Market Analysis by Mordor Intelligence

The Indonesia satellite communications market size is expected to increase from USD 344.04 million in 2025 to USD 411.85 million in 2026 and reach USD 849.84 million by 2031, growing at a CAGR of 15.59% over 2026-2031. Robust momentum stems from an archipelagic landscape where more than 17,000 islands frequently lie beyond the economic reach of fiber and cellular networks, pushing satellite to the forefront of national connectivity strategies. Capacity additions such as SATRIA-1 in 2024 and Nusantara Lima in 2025 have tripled domestic high-throughput supply, enabling government digital-inclusion mandates and catalyzing enterprise digitization across mining, energy, and maritime clusters. Foreign low Earth orbit (LEO) entrants validate the demand for sub-50-millisecond latency applications, while domestic incumbents accelerate hybrid geostationary-LEO rollouts. Investment appetite is reinforced by multilateral financing and by a regulatory roadmap that clears mid-band spectrum for non-terrestrial 5G integration, although capital intensity and licensing friction still temper near-term scalability.

Key Report Takeaways

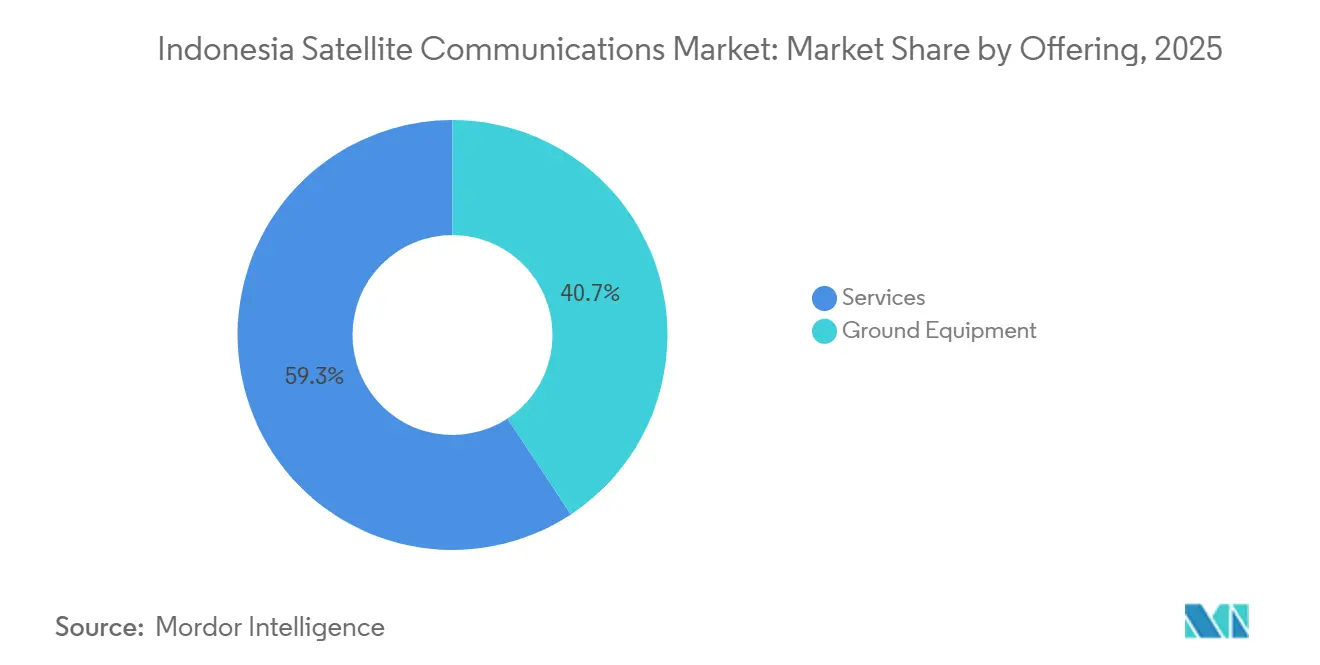

- By offering, services led with 59.28% of 2025 revenue and are advancing at a 15.91% CAGR through 2031.

- By platform, land installations accounted for 43.61% of the Indonesia satellite communications market share in 2025, while portable terminals are expanding at a 16.33% CAGR to 2031.

- By end-user vertical, maritime operations commanded 38.19% of 2025 demand, whereas energy applications are growing the fastest at a 16.71% CAGR through 2031.

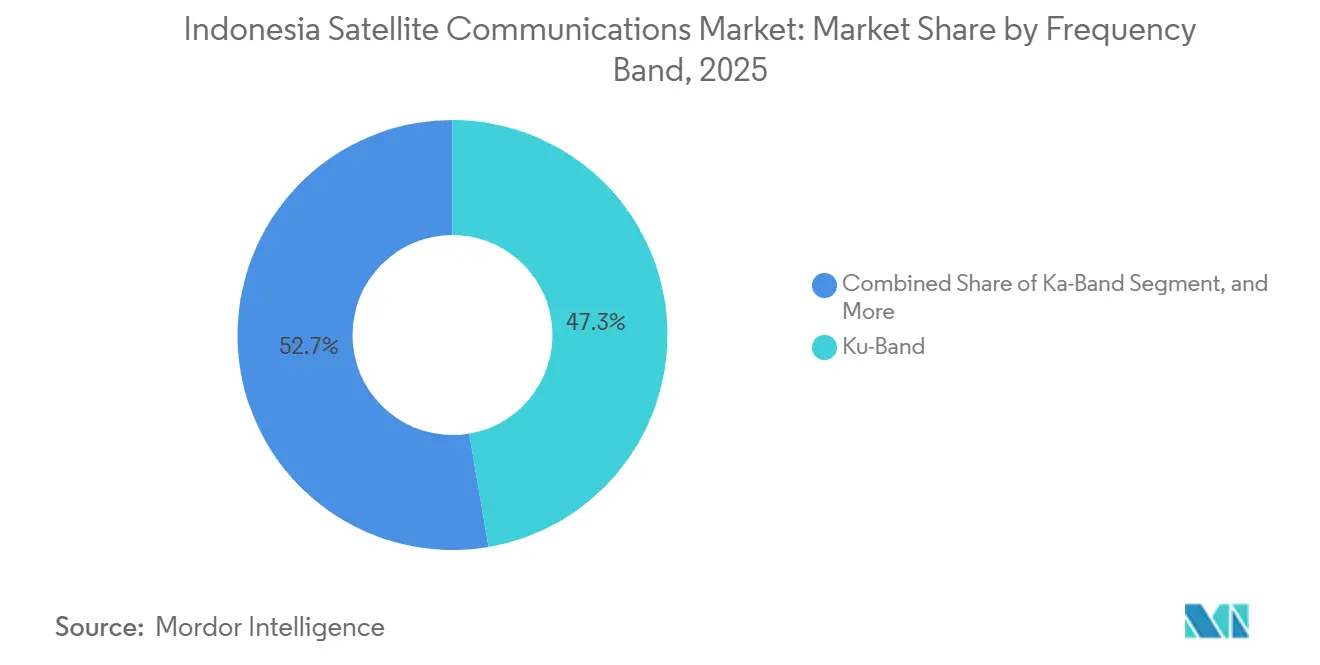

- By frequency band, Ku-band captured 47.32% of 2025 revenue, while Ka-band usage is widening at a 16.39% CAGR to 2031.

- By orbit type, low Earth orbit systems secured 52.67% of 2025 revenue and are projected to grow at a 16.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Satellite Communications Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of 5G Satellite Communication Coverage | +2.1% | National, with early deployments in Jakarta, Surabaya, Bandung, Medan | Medium term (2-4 years) |

| Growing Demand for Broadband Across Remote Islands | +3.4% | Eastern Indonesia (Maluku, Papua, Nusa Tenggara), outer Sumatra, Kalimantan frontier zones | Long term (≥ 4 years) |

| Government-Backed Palapa Ring and SATRIA Projects | +4.2% | National, prioritizing 3T regions (frontier, outermost, disadvantaged areas) | Short term (≤ 2 years) |

| Proliferation of Global Low-Earth-Orbit Constellations | +3.8% | National, with concentration in urban Java and Bali for consumer broadband, remote islands for enterprise | Medium term (2-4 years) |

| Emergence of Biak Spaceport Enabling Local Launches | +0.9% | National strategic infrastructure, initial impact in Papua and eastern logistics | Long term (≥ 4 years) |

| CSR-Led Connectivity Programs by Mining and Agro Firms | +1.1% | Kalimantan (coal, palm oil), Sulawesi (nickel), Papua (copper, gold), Sumatra (rubber, plantations) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-Backed Palapa Ring and SATRIA Projects

The two-satellite program anchors Indonesia’s universal-service objective. SATRIA-1, operational since 2024, delivers 150 Gbps to 150,000 public facilities, narrowing the fixed-broadband gap that left just 27.4% of households connected in 2024.[1]International Trade Administration, “Indonesia - Information and Telecommunications Technology,” trade.gov A blended-finance structure of USD 550 million combined export credits with domestic equity, signaling policy resolve to maintain sovereign capacity. SATRIA-2, budgeted at USD 680-860 million, is scheduled to triple throughput by 2028 and extend maritime reach, lowering per-megabit costs for provincial agencies. Integration with the under-utilized Palapa Ring fiber backbone converts stranded investment into a hybrid terrestrial-satellite grid. Early cross-border leasing, such as the 13.5 Gbps deal with a Philippine operator, demonstrates the potential for spillover monetization.

Proliferation of Global Low-Earth-Orbit Constellations

Starlink’s 2024 debut showed that sub-50 ms latency unlocks telemedicine and e-learning use cases that are impossible with 600 ms geostationary links.[2]Firdia Lisnawati and Niniek Karmini, “Elon Musk launches Starlink internet satellites in Indonesia,” Christian Science Monitor, csmonitor.com A pause in new sign-ups by mid-2025 exposed gateway and spectrum constraints, yet demand indicators remain strong. Kacific’s Ka-band network backhauled 300 4G towers by 2022 and will double capacity once Kacific2 enters service, highlighting competitive optionality. A July 2025 roadmap to pilot non-terrestrial 5G and free the 2.6 GHz band underscores regulatory intent to mainstream satellite into the cellular core. Data-localization and gateway siting rules could tilt approvals toward operators willing to co-invest in local ground assets.

Growing Demand for Broadband Across Remote Islands

National internet reach hit 79.5% in 2024, yet islands outside Java still average speeds below 20 Mbps and remain price-sensitive at tariffs above IDR 100,000 per month. SATRIA-1 and Starlink units deployed during the December 2025 Sumatra floods demonstrated the satellite’s ability to restore connectivity within hours, even as fiber recovery took weeks. Health clinic digitization and school e-learning contracts form a sticky anchor tenancy. A 1.4 GHz auction in October 2025 obliges winners to triple bid outlays on deployment, which strengthens the case for satellite backhaul in low-density provinces. Eight new Ka-band gateways built by Hughes provide nationwide redundancy and sub-100 ms latency to handle future traffic surges.[3]Hughes Network Systems, “Hughes JUPITER System Deployments,” hughes.com

Expansion of 5G Satellite Communication Coverage

The GSMA projects that mid-band 5G will add USD 41 billion to Indonesia’s economy by 2030, provided 200-300 MHz is released, and non-terrestrial networks close rural gaps. July 2025 policy statements paved the way for direct-to-device pilots, which could leapfrog tower builds in Papua and Maluku. Telkomsat’s December 2025 memorandum with Space42 and Viasat hints at hybrid handset messaging offers that counter LEO disruption. Reserve-price discipline aims to avoid 3.5 GHz auction failures seen in 2.3 GHz awards, but spectrum costs still absorb over 12% of operator revenue, so capacity-purchase partnerships remain the preferred risk-sharing model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital-Expenditure Requirements | -2.8% | National, acute for new entrants and second-tier operators lacking balance-sheet depth | Short term (≤ 2 years) |

| Spectrum Allocation and Licensing Delays | -1.9% | National, with procedural bottlenecks in Jakarta regulatory agencies | Medium term (2-4 years) |

| Volcanic-Ash Interference Risk to Ground Stations | -0.7% | Java, Sumatra, Sulawesi, Maluku (127 active volcanoes nationwide) | Long term (≥ 4 years) |

| Limited Domestic Satcom Hardware Manufacturing Base | -1.2% | National, dependency on imported terminals, antennas, modems from North America, Europe, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital-Expenditure Requirements

Flagship satellites cost USD 300-400 million, excluding the eight-site gateway networks, which add tens of millions more. AIIB’s USD 150 million loan to SATRIA-1 and the USD 680-860 million SATRIA-2 budget illustrate reliance on multilateral finance. Spectrum auctions compound the burden; 1.4 GHz bidders must earmark triple the winning price for rollout, effectively locking smaller ISPs out and concentrating power among incumbents. Launch-risk exposure remains material, as Telkom-3’s 2012 loss showed when a USD 170 million asset was written off despite insurance proceeds.

Spectrum Allocation and Licensing Delays

Government Regulation 52/2005 requires foreign players to localize control stations and limits foreign equity to 20%, stretching approval cycles to two years. Starlink cleared licensing in 2024 but hit capacity throttles in 2025 because gateway siting and frequency coordination are subject to separate reviews. Refarming C-band for 5G must compensate incumbents holding rights into the 2030s, yet no relocation fund mechanism exists, creating uncertainty that stalls investment. Historical defaults in the 2.3 GHz band underline execution risk even after auctions conclude.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Managed Services Capture Recurring Revenue

Services contributed 59.28% of 2025 turnover, the dominant slice of the Indonesia satellite communications market. Enterprises and agencies favor turnkey contracts that bundle capacity, terminal upkeep, and network monitoring, shifting technical complexity to providers. Telkomsat reports C-band uptime of 99% and Ku-band uptime of 97%, metrics that underpin multiyear agreements. The equipment cohort ranges from stabilized maritime antennas to ruggedized portable kits, but margins are thinner and tied to lumpy capital cycles. Large one-off procurements, such as 17 portable LEO terminals for the North Sumatra floods, can skew quarterly hardware revenue but usually lead to follow-on service fees. Ground-station builds by Hughes allow operators to resell wholesale bandwidth and launch retail-managed offerings, capturing margin at both levels of the value chain.

Hardware sales also spike after disasters, as illustrated by the army's shipment of 38 portable terminals to West Sumatra in December 2025 for field operations. Intermap’s USD 20 million radar-mapping contract for Sulawesi signals adjacent geospatial revenue streams, but connectivity remains the chief profit engine. Overall, managed services should retain leadership as public-sector digitalization compels long-term service-level agreements and as enterprise cloud adoption deepens.

By Platform: Portable Terminals Surge on Disaster-Response Demand

Land stations accounted for 43.61% of 2025 revenue, yet the portable sub-segment is advancing fastest at a 16.33% CAGR. Disaster agencies, military units, and mobile work crews prize plug-and-play terminals that go live in minutes, without civil works delays. The Indonesian National Agency for Disaster Countermeasures demonstrated this when Starlink kits restored connectivity across flooded areas while fiber remained submerged. Starlink’s three-tier product lineup, from Mini to Performance, offers escalating durability for harsher environments, expanding addressable use cases.

Maritime platforms maintain a large installed base, underpinned by mandatory vessel-monitoring rules for ships above 30 gross tons. Stabilized Ku-band antennas remain the norm at sea, but premium Ka-band packages are gaining traction as fleets demand higher crew-welfare bandwidth. Airborne links are nascent, pending regulator alignment on airborne earth stations, yet global airline adoption trends suggest latent upside once Indonesian low-cost carriers resume fleet expansion.

By End-User Vertical: Energy Sector Digitization Drives Fastest Growth

Energy sites are logging the highest CAGR of 16.71% through 2031 as offshore and remote-site operators automate seismic and production workflows. PwC notes that floating production units and carbon-capture hubs require always-on links for safety-critical systems. Maritime still delivers the single-largest 38.19% share, supported by regulation-linked vessel-tracking demand and crew-welfare mandates. Government and defense share rises as border-surveillance and early-warning initiatives deploy CubeSats alongside leased capacity, diversifying the security communications stack.

Enterprise, media, and other segments remain sensitive to price but shift to satellite for backup and for green-field projects where trenching fiber is prohibitive. While over-the-top platforms challenge direct-to-home broadcasting, hybrid delivery models carve out a profitable niche by combining traditional satellite services with internet-based solutions. This approach is particularly advantageous in remote islands and rural areas where broadband infrastructure remains underdeveloped, ensuring continued access to multi-channel video distribution.

By Frequency Band: Ka-Band’s Rapid Climb Reshapes the Mix

Ku-band accounted for 47.32% of the 2025 Indonesia satellite communications market share, reflecting its entrenched role in maritime links, enterprise broadband, and broadcast feeds. Yet the Ka-band slice of the Indonesia satellite communications market size is projected to expand at a 16.39% CAGR through 2031 as spot-beam architectures on SATRIA-1 and Nusantara Lima deliver higher throughput per square kilometer. Operators favor Ka-band for densely populated Java and for underserved eastern provinces because smaller antennas and dynamic bandwidth allocation squeeze more capacity into scarce orbital slots. Adaptive coding, uplink power control, and gateway diversity help offset heavy tropical rain, keeping link availability near 99% for priority sites. Equipment vendors now bundle cloud-managed radios that switch between Ka and Ku bands, allowing enterprises to hedge weather risk without doubling terminal count. Price per megabit on new Ka satellites has already fallen below legacy Ku rates, narrowing a key adoption barrier. Maritime fleets that once favored Ku for its mature ecosystem are testing Ka packages for crew-welfare streaming, suggesting incremental churn toward the higher band over the forecast horizon.

C-band still serves critical broadcast and offshore energy users thanks to superior rain-fade resilience, but its share will keep sliding as 3.5 GHz mobile refarming advances and forces incumbents to re-pack transponders. Telkomsat’s dual-band service guarantees 99% for C-band and 97% for Ku underscore how service-level priorities differ by vertical, with life-safety and remote-operations contracts likely to keep a residual base on lower frequencies. X-band remains confined to military networks, providing a small yet sticky revenue stream insulated from commercial pricing cycles. Overall, frequency diversity will persist, but the data-hungry edge applications fueling public-sector and enterprise demand favor Ka-band, positioning it as the main growth lever through 2031.

By Orbit Type: Low-Latency LEO Takes the Lead

Low Earth orbit systems captured 52.67% of the 2025 Indonesia satellite communications market share after Starlink’s nationwide rollout proved that sub-50 ms latency unlocks telemedicine and real-time education services that are impossible on 600 ms geostationary links. The LEO segment is set to post a 16.13% CAGR, outpacing all other orbits as continuous satellite replenishment and laser cross-links raise capacity ceilings. Franchise fees are modest compared with building new geostationary birds, which helps smaller internet service providers enter rural markets under wholesale-plus-retail models. Gateway builds in Banda Aceh, Gresik, and Makassar, shortening backhaul hops and supporting data localization rules, removing a prior scaling hurdle. At the same time, falling phased-array antenna prices make multi-orbit terminals viable for provincial clinics and mining camps that value latency and uptime equally.

Geostationary capacity maintains a strong foothold in broadcast distribution, wide-area maritime coverage, and remote energy platforms, where single-antenna tracking and low power draw outweigh latency concerns. SES and Telkomsat have refreshed their fleets with very high-throughput GEO satellites, helping hold revenue steady even as their relative share declines. Medium Earth orbit constellations, led by O3b, offer a latency sweet spot of roughly 150 ms, appealing to cruise ships and offshore rigs that require more bandwidth than GEO can supply cheaply but can tolerate higher delay than LEO. A growing number of enterprises now buy hybrid packages that route interactive traffic over LEO and bulk data over GEO, boosting overall service resilience. As regulators pilot non-terrestrial 5G, dynamic orbit switching is expected to become seamless at the handset layer, entrenching multi-orbit strategies as a hallmark of Indonesia’s connectivity roadmap.

Geography Analysis

Java and Bali, which together account for roughly 56% of the population, still rely on satellite to harden connectivity when fiber backhaul is overloaded or damaged during storms. The Indonesian National Agency for Disaster Countermeasures restored links in North Sumatra and West Sumatra by activating 49 portable LEO terminals in late 2025, demonstrating how flood-prone western provinces treat satellite as a first-response backbone. Urban demand also strains LEO beams, prompting operators to build gateways in Banda Aceh, Gresik, and Makassar to localize traffic and meet data-localization rules. Java’s consumer focus keeps average revenue per user high, yet regulatory pilots of non-terrestrial 5G aim to serve fringe districts where tower economics break down. As a result, even the country’s most connected islands maintain a steady baseline for managed satellite services.

Maluku, Papua, and Nusa Tenggara record the lowest fixed-broadband penetration and often see average speeds below 20 Mbps, positioning them as the fastest-growing regional cluster for capacity uptake. SATRIA-1’s 150 Gbps payload now covers thousands of public schools and clinics across these provinces, cutting reliance on expensive bandwidth leases from foreign operators. Mining and fishing enterprises in eastern waters use Ka-band spot beams to stream seismic data and monitor vessel movements in real time, tasks previously limited by high latency on legacy geostationary links. Government planners expect additional throughput from SATRIA-2 to lower per-megabit costs and spur new community Wi-Fi programs by 2028.

Sumatra, Kalimantan, and Sulawesi sit between the dense west and underserved east, blending resource-driven enterprise demand with growing household adoption. Coal mines, nickel pits, and offshore rigs here account for the bulk of energy-sector bandwidth orders that are expanding at a 16.71% CAGR, the fastest among verticals. Vessel-monitoring mandates keep maritime terminals active along Sumatra’s busy straits, while provincial governments bundle satellite backhaul with fixed-wireless access licenses awarded in the October 2025 1.4 GHz auction. Collectively, these three islands anchor mid-tier growth, smoothing revenue volatility between Java’s consumer peaks and Papua’s frontier projects.

Competitive Landscape

Indonesia’s satellite communications arena is moderately concentrated, with PT Telkom Satelit Indonesia and PT Pasifik Satelit Nusantara together holding roughly 50-60% of domestic capacity through long-standing government contracts and distributor networks. Foreign operators such as Starlink, Kacific, SES, Eutelsat, and Intelsat compete for enterprise, maritime, and consumer broadband niches by leveraging global fleets and reseller alliances. Hughes Network Systems, acting as a neutral ground-segment supplier, underpins multiple players with nationwide gateway deployments that improve latency and redundancy.

Strategic capacity rollouts dominated 2024-2025. Telkomsat launched the 32-Gbps Merah Putih 2 satellite in February 2024 to reinforce C-band and Ku-band coverage at 113° East and safeguard its broadcast and enterprise base. Pasifik Satelit Nusantara followed in September 2025 with Nusantara Lima, a 160-Gbps Ka-band craft equipped with 101 spot beams and eight Indonesian gateways, instantly more than doubling the company’s addressable throughput. In December 2025, Telkomsat signed a memorandum of understanding with Space42 and Viasat to explore direct-to-device messaging, aiming to counter LEO disruption by bundling geostationary broadcast capacity with handset-based services.

Foreign entrants are shaping pricing and service expectations. Starlink’s May 2024 debut offered sub-50 ms latency nationwide, but a July 2025 pause on new sign-ups exposed the need for additional satellites and local gateways to sustain momentum. Kacific expanded its distributor footprint to more than 120 partners, targeting remote islands with prepaid community Wi-Fi packages that tap its forthcoming 150-Gbps Kacific2 satellite. SES and Eutelsat are refreshing their very-high-throughput geostationary fleets, positioning hybrid GEO-LEO bundles that steer latency-sensitive traffic to LEO while offloading bulk video to GEO. Overall, rivalry is intensifying as policy pilots non-terrestrial 5G and as multi-orbit terminals let enterprises switch between operators without costly hardware swaps.

Indonesia Satellite Communications Industry Leaders

PT Pasifik Satelit Nusantara

Indosat Ooredoo Hutchison

PT Telkom Satelit Indonesia

Kacific Broadband Satellites Group

Thaicom Public Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Telkomsat signed an MoU with Space42 and Viasat to explore direct-to-device satellite services.

- December 2025: The Indonesian Army deployed 38 Starlink terminals during West Sumatra flood relief.

- December 2025: The ministry restored 145 base stations and installed 32 Starlink units in West Sumatra.

- December 2025: SATRIA-1 emergency internet points went live in Aceh, North Sumatra, and West Sumatra.

Indonesia Satellite Communications Market Report Scope

The Indonesia Satellite Communications Market Report is Segmented by Offering (Ground Equipment, and Services), Platform (Portable, Land, Maritime, Airborne), End-user Vertical (Maritime, Defense and Government, Enterprises, Media and Entertainment, Energy, Other End-user Verticals), Frequency Band (C-Band, Ku-Band, Ka-Band, X-Band), Orbit Type (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Orbit (GEO)). The Market Forecasts are Provided in Terms of Value (USD).

| Ground Equipment |

| Services |

| Portable |

| Land |

| Maritime |

| Airborne |

| Maritime |

| Defense and Government |

| Enterprises |

| Media and Entertainment |

| Energy |

| Other End-user Verticals |

| C-Band |

| Ku-Band |

| Ka-Band |

| X-Band |

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Geostationary Orbit (GEO) |

| By Offering | Ground Equipment |

| Services | |

| By Platform | Portable |

| Land | |

| Maritime | |

| Airborne | |

| By End-user Vertical | Maritime |

| Defense and Government | |

| Enterprises | |

| Media and Entertainment | |

| Energy | |

| Other End-user Verticals | |

| By Frequency Band | C-Band |

| Ku-Band | |

| Ka-Band | |

| X-Band | |

| By Orbit Type | Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) | |

| Geostationary Orbit (GEO) |

Key Questions Answered in the Report

How fast is revenue growing in the Indonesia satellite communications market?

Between 2026 and 2031 the market is projected to register a 15.59% CAGR, nearly doubling to USD 849.84 million.

Which platform is expanding quickest?

Portable terminals, used for disaster relief and mobile operations, are rising at a 16.33% CAGR through 2031.

What end-user vertical shows the strongest growth momentum?

Energy sites, including offshore rigs and remote mines, lead with a 16.71% CAGR thanks to real-time digitalization needs.

How are Ka-band services performing relative to Ku-band?

Ka-band capacity is expanding at a 16.39% CAGR through 2031 and steadily claiming share from Ku-band despite higher rain-fade risk.

Why did Starlink pause Indonesian sign-ups in 2025?

The company cited local capacity constraints, highlighting the need for additional satellites and gateways to scale service.

What role will non-terrestrial 5G play?

Government pilots aim to integrate satellite directly into 5G cores, enabling direct-to-device links in remote provinces where towers are uneconomical.

Page last updated on: