Brazil Tractors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

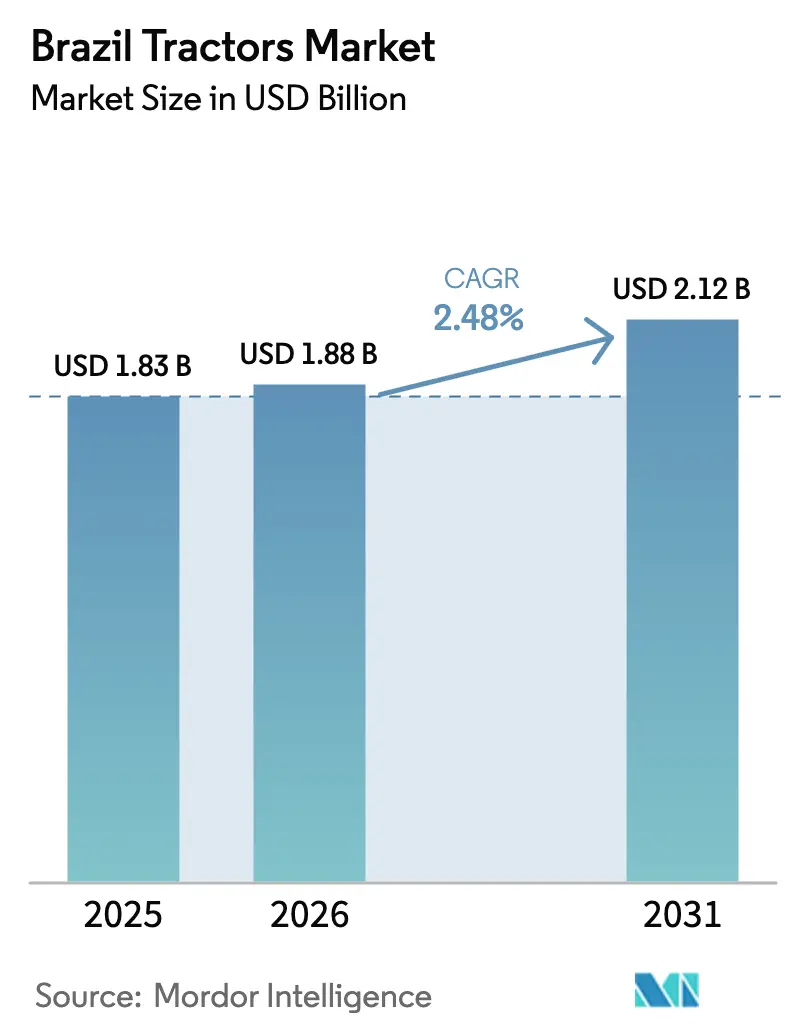

| Base Year Market Size (2025) | USD 1.83 Billion |

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 2.48% CAGR |

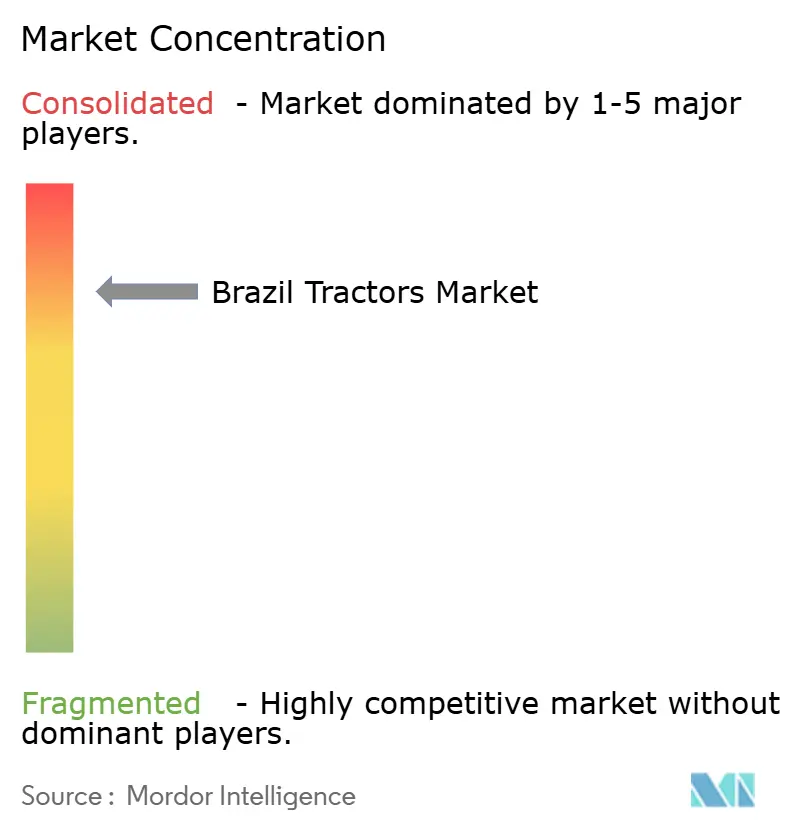

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Tractors Market Analysis by Mordor Intelligence

Brazil tractor market size in 2026 is estimated at USD 1.88 billion, growing from 2025 value of USD 1.83 billion with 2031 projections showing USD 2.12 billion, growing at 2.48% CAGR over 2026-2031. Demand growth rests on the country’s stature as South America’s largest agricultural economy and status as a top global food exporter. Widespread adoption of precision agriculture, the continued advance of large-scale farming in the Cerrado, and the spread of embedded-finance offerings reshape equipment procurement. At the same time, credit cost volatility and tariff structures that favor local assembly temper spending and keep the growth curve modest. Structural change is already evident in horsepower, drive-type, and power-source choices, indicating that the Brazil tractor market is evolving toward higher-capacity, digitally enabled machinery while retaining a deep base of low-horsepower units suited to smallholders.

Key Report Takeaways

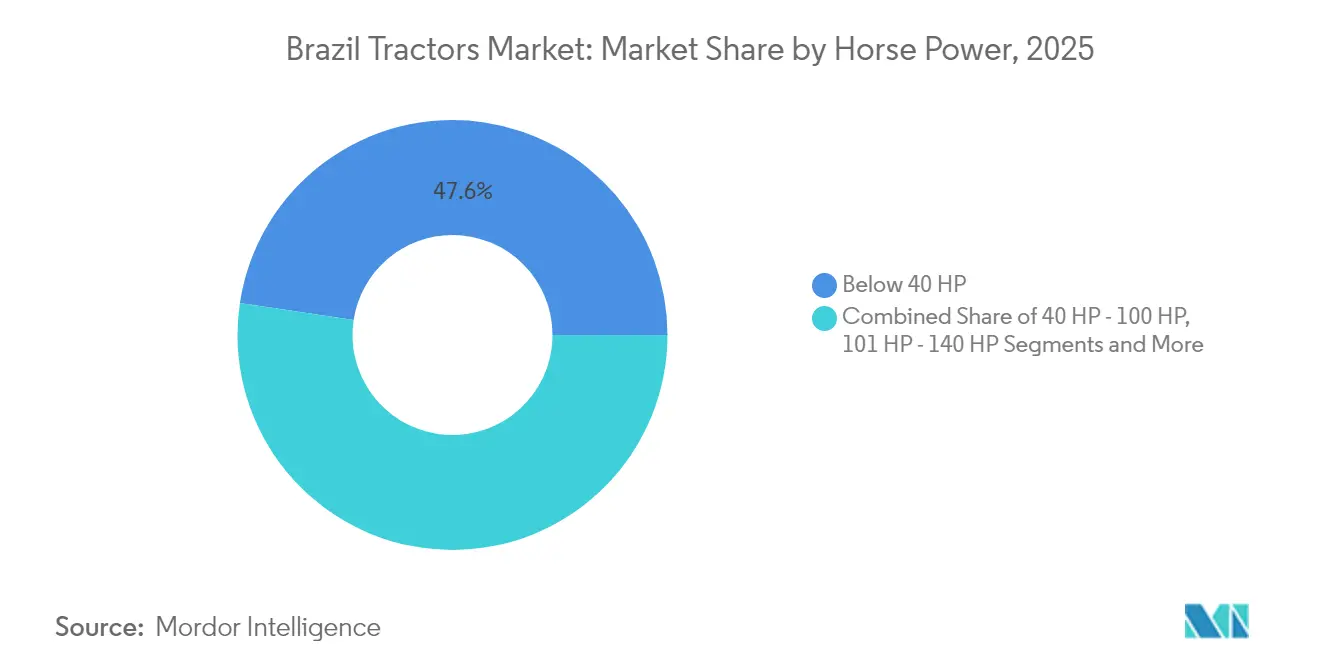

- By horsepower, below-40 HP units led with 47.62% of Brazil tractor market share in 2025, whereas above-140 HP tractors are projected to expand at 6.93% CAGR through 2031.

- By drive type, Two-Wheel Drive systems held 62.41% of the Brazil tractor market in 2025, yet Four-Wheel Drive is the fastest-growing segment, with a 7.42% CAGR to 2031.

- By application, row-crop configurations captured a 56.88% revenue share in 2025; the fully electric retrofit subsegment is poised for a 8.71% CAGR to 2031.

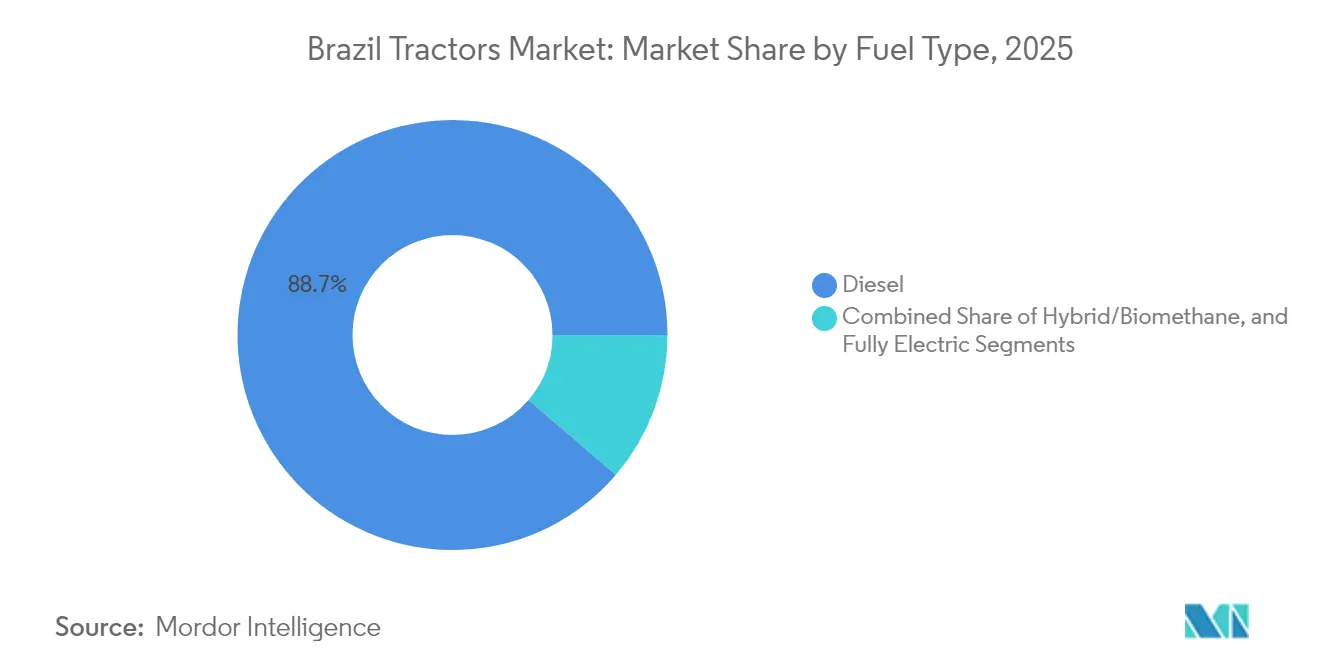

- By fuel type, diesel models accounted for 88.74% of the Brazil tractor market size in 2025, though electric variants are set to grow at 9.06% CAGR.

- Mechanical gearboxes accounted 63.66% of the Brazil tractor market sales in 2025, whereas CVT and hydrostatic models are growing at 8.24% CAGR by 2031.

- By region, the South commanded 33.84% share of the Brazil tractor market size in 2025, while the Central-West is forecast to post a 5.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Brazil representing one among them. The global report on tractor market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Brazil Tractors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Precision-ag Mechanisation | +0.8% | South, Southeast, Central-West | Medium term (2-4 years) |

| Expansion of Large-Scale Cash-Crop Farms in Carrado | +0.6% | Central-West, North | Long term (≥ 4 years) |

| OEM Embedded-Finance Models Lowering Up-Front Cost | +0.5% | National | Medium term (2-4 years) |

| Integration of Telematics and Remote Diagnostics | +0.4% | South, Southeast | Short term (≤ 2 years) |

| Growth in Biomethane and Hybrid Tractor Pilots | +0.3% | South, Central-West | Long term (≥ 4 years) |

| Carbon-Credit Revenue Streams for Low-HP Electric Tractors | +0.2% | South, Southeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Precision-Ag Mechanisation

Connectivity partnerships between equipment makers and satellite providers are closing Brazil’s rural internet gap and lifting demand for sensor-equipped tractors. CNH Industrial’s deal with Intelsat enables satellite broadband in areas where only 19% of fields have coverage[1]“CNH and Intelsat Bring Satellite Internet to Brazilian Farms,” AgWeb Staff, agweb.com. Solar-powered SOLIX field robots from Solinftec add real-time weed detection without continuous connectivity[2]“Solar-Powered SOLIX Robot Targets Herbicide Reduction,” AgroPages Editorial, agropages.com. Bosch’s R $700 million smart-farming outlay in Campinas, backed by Finep and BNDES, will deepen local R&D capability. These moves accelerate precision-ag take-up, encouraging upgrades toward tractors with advanced guidance and data-logging features across the Brazilian tractor market.

Expansion of Large-Scale Cash-Crop Farms in Cerrado

Soybean output in the Cerrado climbed from under 1 million t in 1974 to more than 56 million t, reflecting government research and land-use policy that turned acidic savanna soils into productive farmland. The 70 million acres of degraded pasture can still be used for crops, mostly in Mato Grosso, Goiás, and Mato Grosso do Sul. Such expansion calls for high-horsepower units and large implements to work wide tracts efficiently. Consequently, demand for above-140 HP tractors in the Brazilian market continues to exceed the average.

OEM Embedded-Finance Models Lowering Up-Front Cost

Manufacturers increasingly blend equipment sales with in-house credit. John Deere’s venture with Bradesco links a R$17.4 billion agribusiness loan book to branded machinery finance, shielding farmers from soaring Selic rates[3]“Bradesco Acquires Stake in Banco John Deere,” Valor Econômico Reporters, valor.com.br. Similar offerings by CNH Capital and AGCO Finance smooth cash-flow pressures after the 2024 pause in federal subsidies. Flexible financing expands the reachable customer base, particularly among family farms in the South and Southeast, supporting steady turnover of mid-horsepower machines across the Brazil tractor market.

Integration of Telematics and Remote Diagnostics

John Deere’s R $180 million innovation center focuses on low-connectivity telematics suited to Brazil’s vast interior. AGCO’s FarmerCore mobile store pilot in Paraná leverages connected machines to schedule preventive maintenance visits[4]“John Deere Opens Innovation Hub in SP,” Estadão Conteúdo, estadao.com.br. Predictive diagnostics limit downtime during peak planting and harvest, providing tangible ROI for premium tractor models. As dealers roll out subscription-based support, telematics capabilities become a major purchase criterion, nudging farmers toward newer units within the Brazil tractor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Selic-Linked Credit Costs Post-2024 Subsidy Pause | -0.9% | National | Short term (≤ 2 years) |

| High Import Tariffs on Power-train Components | -0.4% | National | Medium term (2-4 years) |

| Dealer-Network Gaps in North and Northeast Regions | -0.3% | North, Northeast | Medium term (2-4 years) |

| Safety Non-Compliance Among Low-Cost Grey-Market Imports | -0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Selic-Linked Credit Costs Post-2024 Subsidy Pause

Suspension of new federally subsidized Crop Plan loans and a Selic jump to 13.25% raised borrowing costs, stalling nearly R$50 billion of agricultural funding. Only PRONAF programs remain, preserving R$5.6 billion for smallholder lending. With many farmers delaying equipment replacement, short-term demand in the Brazil tractor market has softened, especially for mid-size models.

High Import Tariffs on Power-Train Components

Import duty, IPI, and ICMS taxes can add 30% or more to the landed cost of advanced engines and transmissions[5]“Brazil – Agricultural Equipment Import Duties,” International Trade Administration, trade.gov. While ex-tariff waivers exist, approval delays deter rapid technology refresh. Local-content mandates tied to BNDES credit further complicate sourcing. The result is slower diffusion of high-spec drivetrains within the Brazil tractor market and persistent price gaps versus imported machinery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Horsepower: Demand Splits Between Family Farms and Large Estates

Below-40 HP units held 47.62% of the Brazil tractor market share in 2025, serving smallholders who grow diversified crops on limited acreage. In value terms, this bracket anchors recurring revenue as replacement cycles average 15 years. Mid-range 40–100 HP models form the core equipment pool for mixed-grain farms in the South and Southeast. Above-140 HP machines represented a smaller base but posted the fastest growth at 6.93% CAGR, fueled by Cerrado grain estates expanding double-cropping.

Precision guidance, variable-rate seeding, and high-capacity planters pull demand toward stronger tractors on frontier farms. Conversely, compact 20–70 HP 4WD tractors launched under Mahindra’s OJA platform target orchard and vegetable growers seeking maneuverability and lower total cost Mahindra. Such divergence underscores a two-speed Brazil tractor market where power needs and affordability define purchase choices. Spending constraints amid elevated interest rates could extend the life of under-40 HP fleets, yet operational scale economics favor continued up-take of premium power units among commercial crop producers.

By Drive Type: Four-Wheel Drive Gains Traction on Challenging Terrain

Two-Wheel Drive retained 62.41% of Brazil's tractor market share in 2025, mainly in the South and coastal Southeast, where soils are deep and field slopes are gentle. Adoption, familiarity, and lower purchase price keep replacement demand steady. Four-Wheel Drive’s 7.42% CAGR through 2031 mirrors land conversion in the Central West, North, and parts of the Northeast, where sandier soils and rolling ground demand extra traction.

Front-axle assist systems paired with higher horsepower enable wider implements, cutting passes per field, and saving diesel. OEMs now offer entry-level 4WD packages on 75–120 HP chassis, helping small growers accelerate the technology curve. Regional mechanization studies show large farms already operate with high tech adoption, while many small farms still lack 4WD access, SciELO. Dealer pilots that bundle tires, GPS kits, and remote support aim to shrink that gap, gradually shifting the drive-type mix across the Brazil tractor market.

By Application: Row-Crop Dominance Meets Electric Retrofit Potential

Row-crop units secured a 56.88% share in 2025, reflecting soybeans, corn, and cotton’s central role in export earnings. Orchard and specialty tractors carve out a resilient niche in citrus and coffee belts where canopy clearance and turning radius matter. Though starting from a low base, fully electric retrofit kits are forecast to rise at 8.71% CAGR, propelled by carbon-credit revenue and battery subsidy pilots.

Municipalities are also testing electric conversions for light-duty utility work. With its Fendt e100 Vario proof-of-concept, OEMs such as AGCO illustrate growing confidence in battery technology. If charging infrastructure expands alongside rural solar micro-grids, electric solutions could reach a tipping point in low-horsepower segments of the Brazilian tractor market

By Fuel Type: Diesel Still Rules, but Alternatives Gain Policy Tailwind

Diesel engines powered 88.74% of tractors sold in 2025, a share that underscores mature supply chains and robust torque delivery. Yet, electric, hybrid, and biomethane formats collectively are progressing at 9.06% CAGR. RenovaBio certificates and sugarcane-linked biomethane prospects give Brazil a unique platform for low-carbon mechanisation. Combined with investment in green hydrogen pilot plants at sugar mills, stakeholders anticipate alternative fuel penetration first in fleets that log predictable daily hours close to biofuel supply points.

Case IH’s Sorocaba hub will build energy-transition tractor lines for global markets, confirming Brazil’s role as a testbed. As battery pack prices trend down and carbon accounting tightens, the proportion of non-diesel units in the Brazil tractor market is set to climb, albeit from a low starting base.

By Transmission Type: Mechanical Simplicity Faces CVT Uptake

Mechanical gearboxes commanded 63.66% of sales in 2025, valued for durability and easy servicing in regions with sparse technicians. Still, CVT and hydrostatic models are growing at 8.24% CAGR, largely in tractors above 117 kW where fuel savings and operator comfort justify price premiums. The Brazil tractor market size tied to CVT systems is anticipated to double by 2031, aided by manufacturer financing bundles that highlight lower life-cycle costs.

Semi-powershift remains popular in mid-range tractors where farmers desire speed matching without the full CVT investment. CVT capability gains traction as precision planting relies on constant speed under variable load. However, after-sales logistics and spare-parts tariffs remain barriers to widespread conversion, reinforcing mechanical dominance across volume segments of the Brazil tractor market.

Geography Analysis

The South captured 33.84% of the Brazil tractor market in 2025, drawing on entrenched mechanisation and a dense dealer network in Rio Grande do Sul, Paraná, and Santa Catarina. Replacement demand for under-100 HP models predominates, yet farms increasingly experiment with telematics retrofits as mobile coverage improves. The Southeast sustains diversified equipment needs ranging from sugarcane row-crop tractors to orchard units for coffee and citrus. Availability of turnkey finance via regional banks supports the Brazil tractor market size in this zone, even under tighter national credit conditions.

The Central-West leads growth at 5.93% CAGR to 2031 as Mato Grosso and Goiás extend double-crop rotations. Large estates incorporate above-140 HP 4WD tractors to handle expansive grain fields, pushing the region’s share of Brazil tractor market size higher each year. Frontier states in the North, including Pará and Rondônia, show rising uptake tied to pasture conversion programs, though logistical hurdles keep absolute volumes modest. Dealer-network rollouts and satellite service facilities aim to close service gaps that currently suppress sales.

The Northeast remains under-mechanised, relying heavily on manual labor and small animal traction despite irrigation projects that improve farm viability. Climate variability and fragmented landholding patterns limit purchase scale. However, targeted PRONAF loans help family farms acquire compact 4WD units, creating an entry market for budget-oriented brands. Nationwide, geographic disparities in tractor density mirror broader socio-economic divides, ensuring that region-specific product-service bundles stay central to Brazil tractor market strategy.

Competitive Landscape

The Brazilian tractor market exhibits moderate concentration. John Deere surged ahead after investing R$700 million to localize high-tech models and secure supply resilience. CNH Industrial follows, leveraging its Sorocaba expansion and dual brand (Case IH and New Holland) strategy to deepen reach. AGCO slipped to third due to gaps in mid-hp 4WD offerings, prompting its FarmerCore satellite store initiative to regain share.

High fixed capacity and soft short-term demand heighten price competition, especially in the 75–125 HP ranges. Precision technology ecosystems emerge as the new battleground. CNH’s stake in Bem Agro bolsters AI imagery for sugarcane and grain management. Deere’s Operations Center integrates field data into financing decisions, creating a service moat. Smaller local assemblers concentrate on under-40 HP niches, often courting family farms with aggressive pricing, but struggle with safety compliance, exposing them to regulatory fines.

Embedded finance partnerships give large OEMs an edge while dealers test subscription models, bundling telematics, maintenance, and upgrade pathways. Start-ups like Solinftec position autonomous field robots as complementary tools rather than outright tractor replacements, adding pressure on incumbents to differentiate. Overall competitive dynamics indicate that technology depth, financing reach, and rural service density will dictate share shifts within the Brazil tractor market through 2030.

Brazil Tractors Industry Leaders

Deere & Company

CNH Industrial

AGCO

Kubota Corporation

Mahindra & Mahindra Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Bradesco bought 50% of Banco John Deere to expand agribusiness credit access and cut funding costs.

- April 2024: CNH Industrial and Intelsat partnered on satellite internet to boost telematics coverage across Brazilian farms.

Brazil Tractors Market Report Scope

A tractor is a vehicle usually available with one or two small wheels in front and two large wheels at the back. It is used in agriculture, construction, and logistics applications to move attached implements such as rotavators, plowing, tilling, sowing, cultivation, and harvesting.

Brazil's tractors market is segmented by horsepower, drive type, and application. By horsepower, the market is segmented into below 40 HP, 40 HP - 100 HP, and above 100 HP. By drive type, the market is segmented into two-wheel drive and four-wheel drive/all-wheel drive. By application, the market is segmented into row crop tractors, orchard tractors, and other applications.

For each segment, the market sizing and forecast have been done based on the value (USD).

| Below 40 HP |

| 40 - 100 HP |

| 101 - 140 HP |

| Above 140 HP |

| Two-Wheel Drive |

| Four-/All-Wheel Drive |

| Row-Crop |

| Orchard / Specialty |

| Industrial and Other |

| Diesel |

| Hybrid / Biomethane |

| Fully-Electric |

| Mechanical (Sync/Unsync) |

| Semi-/Full Powershift |

| CVT / Hydrostatic |

| South |

| Southeast |

| Central-West |

| Northeast |

| North |

| By Horsepower | Below 40 HP |

| 40 - 100 HP | |

| 101 - 140 HP | |

| Above 140 HP | |

| By Drive Type | Two-Wheel Drive |

| Four-/All-Wheel Drive | |

| By Application | Row-Crop |

| Orchard / Specialty | |

| Industrial and Other | |

| By Fuel / Power Source | Diesel |

| Hybrid / Biomethane | |

| Fully-Electric | |

| By Transmission Type | Mechanical (Sync/Unsync) |

| Semi-/Full Powershift | |

| CVT / Hydrostatic | |

| By Region | South |

| Southeast | |

| Central-West | |

| Northeast | |

| North |

Key Questions Answered in the Report

What is the current size of the Brazil tractor market and how fast is it growing?

The Brazil tractor market reached USD 1.88 billion in 2026 and is set to climb to USD 2.12 billion by 2031, registering a 2.48% CAGR.

Which horsepower segment is expanding most rapidly?

Tractors above 140 HP lead growth, advancing at 6.93% CAGR because large Cerrado grain farms need high-capacity machines.

How are financing conditions affecting tractor demand?

The 2024 suspension of subsidized loans and a Selic rate of 13.25% raised borrowing costs, prompting many farmers to delay purchases until credit terms stabilize.

Which region offers the strongest growth prospects?

The Central-West is forecast to log a 5.93% CAGR through 2031 as large-scale farms in Mato Grosso and Goiás continue expanding cropped area.

What technologies are most influencing new tractor purchases?

Precision-ag features, embedded telematics, and remote diagnostics are key differentiators, encouraging upgrades to connected models despite higher upfront prices.

Page last updated on: