Brazil Forklift Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.73 Billion |

| Market Size (2030) | USD 3.07 Billion |

| Growth Rate (2025 - 2030) | 12.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Forklift Rental Market Analysis by Mordor Intelligence

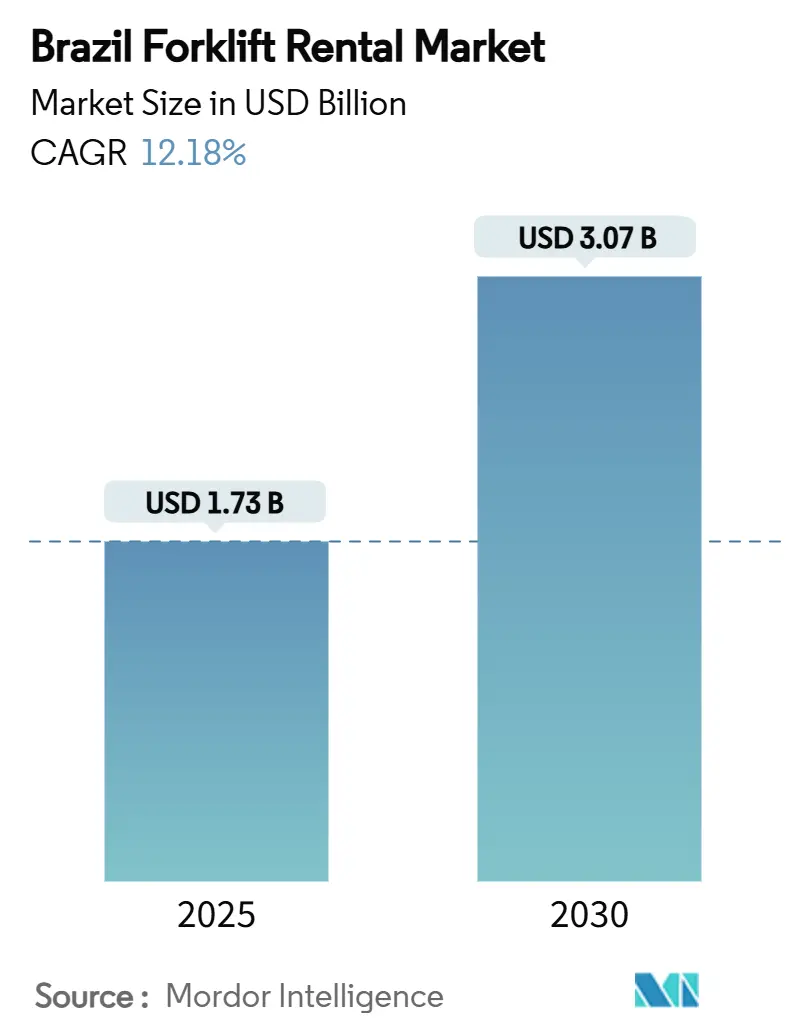

The Brazil forklift rental market size reached USD 1.73 billion in 2025 and is forecast to climb to USD 3.07 billion by 2030, reflecting a 12.18% CAGR that places the segment among the fastest-growing logistics support services in Latin America. Robust e-commerce expansion, an acute shortage of modern warehouse space, and project-based infrastructure spending combine to push rental penetration higher, especially in metropolitan freight corridors such as São Paulo–Santos. As ownership costs rise sharply, this tilts customer preference toward pay-as-you-go fleets that protect cash flow while ensuring regulatory compliance under NR-11 and NR-12 standards. Intense competition among global OEMs and agile local specialists further accelerates service innovation, deepens after-sales coverage, and compresses downtime, making the Brazilian forklift rental market increasingly attractive to capital-constrained warehouse operators. On the demand side, agribusiness exports, 24/7 port operations, and multiphase railway projects under PAC-3 lock in rental demand beyond the short run, underpinning the current growth trajectory

Key Report Takeaways

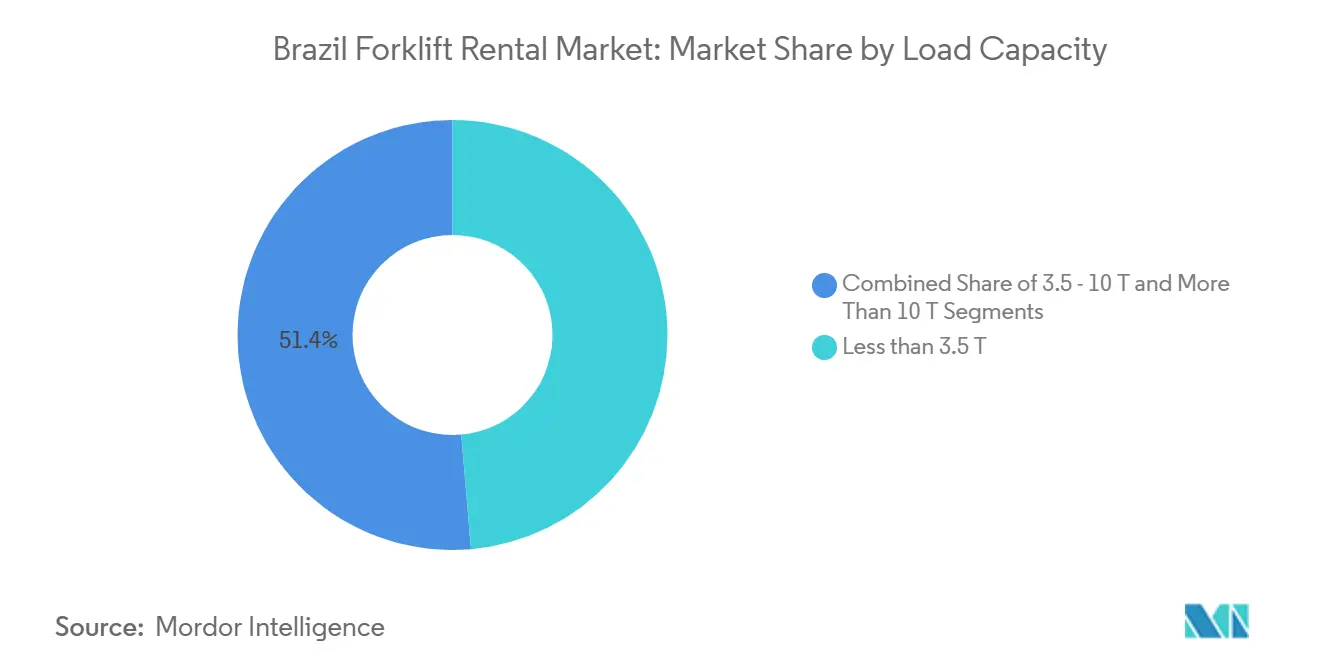

- By load capacity, sub-3.5 ton units captured 48.62% of Brazil's forklift rental market share in 2024, and the same segment is expanding at a 13.21% CAGR through 2030.

- Mid-term contracts spanning 1–12 months controlled 51.29% of the Brazil forklift rental market size in 2024; short-term rentals under one month are advancing at a 12.28% CAGR to 2030.

- Internal combustion models retained 63.87% of the Brazil forklift rental market size in 2024, but electric variants are pacing the market with a 13.78% CAGR.

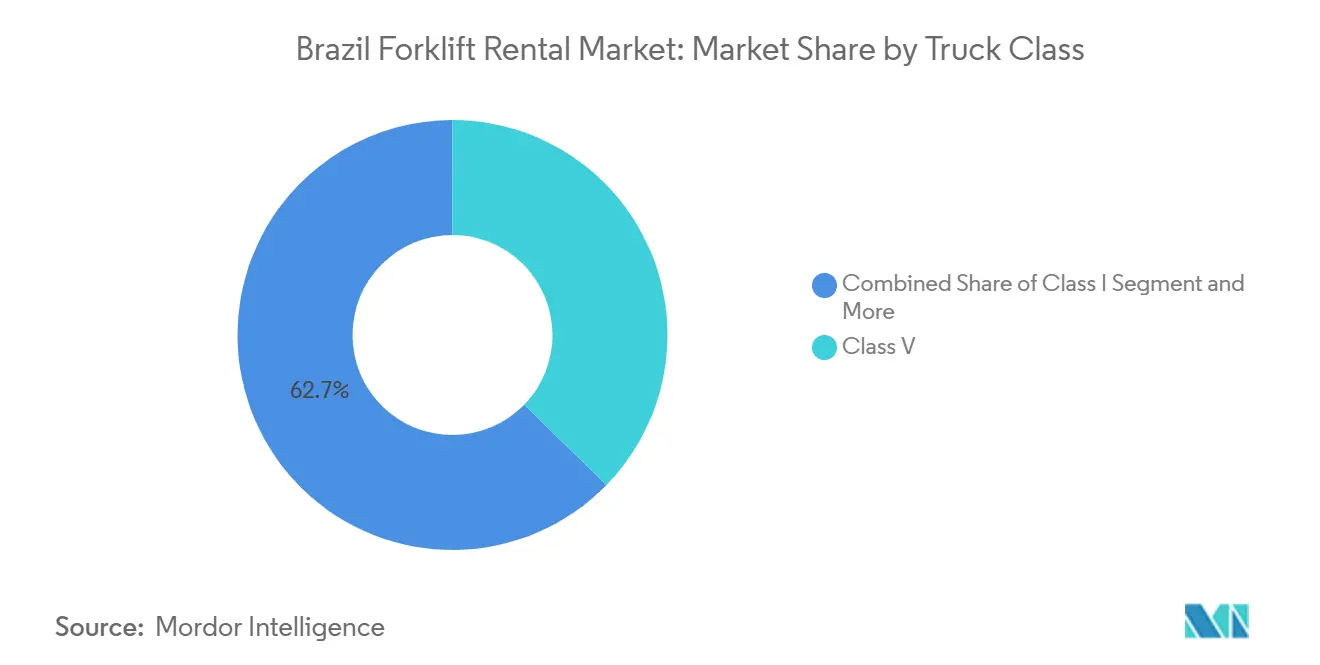

- Class V trucks led revenue with 37.28% share, whereas Class I units are on track for the highest CAGR at 12.33% through 2030.

- The warehouse and logistics sector commanded 65.75% of Brazil's forklift rental market size in 2024 and is forecast to grow 12.32% annually, outpacing all other end-use segments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Future direction is shaped by developments occurring across multiple countries and regions, with Brazil contributing to the overall trajectory. The outlook on worldwide forklift rental market reflects how these are expected to evolve collectively.

Brazil Forklift Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Warehousing | +2.8% | São Paulo, Rio de Janeiro, Belo Horizonte | Medium term (2-4 years) |

| Agribusiness Logistics | +2.1% | Mato Grosso, Goiás, Paraná, Santos corridor | Long term (≥ 4 years) |

| PAC-3 Rail Spend | +1.9% | National, concentrated in Northeast, North regions | Long term (≥ 4 years) |

| OEM Service Rentals | +1.4% | Global, early adoption in São Paulo industrial belt | Short term (≤ 2 years) |

| Lei do Bem Incentives | +1.2% | National, concentrated in technology hubs | Medium term (2-4 years) |

| Santos Port 24/7 | +0.8% | Santos port region, São Paulo logistics corridor | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

E-Commerce-Fueled Warehousing Expansion

The rents grew more than 500 basis points faster than the global average, reinforcing demand for flexible material-handling capacity[1]“Brazil Logistics Real Estate Outlook 2024,”, Prologis Research, prologis.com. Rental fleets of compact forklifts thrive because they solve short-cycle throughput spikes without tying up capital at a time when new construction pipelines account for less than 1% of modern stock. These trends cluster around São Paulo’s industrial arc, where only some existing space meets modern logistics criteria, granting rental providers strong geographic pricing power. OEMs and local lessors are scaling telemetry-enabled units to capture utilisation data, cut downtime, and align rates with the life-cycle value proposition that warehouse operators now expect.

Agribusiness Export Boom Boosting Logistics Nodes

Brazilian food processing revenue reinforces grain-export supremacy and stokes freight flows through intermodal terminals[2]“Boletim Logístico – December 2024,”, Companhia Nacional de Abastecimento (Conab), conab.gov.b. Harvest cycles produce concentrated handling peaks at rail-to-port corridors, particularly Santos, requiring short-duration rental infusions rather than permanent fleet expansion. As the government aims to lift rail cargo share from 17% to 40% by 2035, new trans-shipment hubs depend on quick-deploy forklifts that can bridge construction delays and seasonal throughput volatility. Rental firms exploit this window by pooling fleets across Mato Grosso, Goiás, and Paraná, leveraging asset mobility to maximise utilisation. Ancillary demand comes from cold-chain modernisation in the meat export value stream, where temperature-controlled warehouses mandate high-uptime electric units, further supporting growth.

Federal PAC-3 Infrastructure Spending Uptick

The BRL 94.2 billion earmarked for rail development through 2026 funnels equipment demand to project sites and future terminals, amplifying rental volume in regions historically underserved by logistics networks[3]“PAC-3 Projetos Prioritários,”, Ministério dos Transportes, transportes.gov.br. Flagship projects such as the Transnordestina line depend on forklifts for permanent cargo handling and interim construction needs. These projects, bankrolled by regional development funds exempt from Brazil’s fiscal cap, sustain contracting momentum even under macro-prudential tightening. For rental providers, the phased nature of worksites aligns perfectly with shorter amortisation horizons, making fleet rotation of construction machinery between construction and operations commercially attractive. Resulting asset churn feeds the secondary market, enabling providers to cascade older units into price-sensitive segments without compromising profitability.

24/7 Port of Santos Modernization Spikes Short-Term Demand

Santos port moved to 24/7 operations in 2024, pressuring terminal operators to add night-shift capacity instantly rather than through gradual fleet build-outs. Short-term rentals of specialised container forklifts surged as operators sought to maintain berth productivity during dredging and berthing upgrades. The Santos-São Paulo corridor now acts as a demand bellwether; every construction milestone triggers a proportional uptick in rental call-offs. Lessons learned at Santos serve as a template for other ports such as Suape and Itaqui, making round-the-clock scheduling a systemic driver of forklift rental utilisation nationwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High SELIC Costs | -1.8% | National, acute in capital-intensive sectors | Short term (≤ 2 years) |

| Used Imports Influx | -1.2% | Port cities, industrial centres | Medium term (2–4 years) |

| Electricity-tariff Volatility | -0.9% | Urban centres, industrial zones | Medium term (2–4 years) |

| Certification Bottlenecks | -0.7% | National, unionised sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Influx of Low-Priced Used Imports

A depreciated real encourages opportunistic inflows of used forklifts that undercut domestic rental tariffs, especially in secondary ports such as Itajaí and Vitória. While NR-11 and NR-12 impose uniform safety standards on all units, compliance audits often lag import cycles, letting subpar equipment slip into short-term hire pools. Established lessors counter by highlighting maintenance transparency, uptime guarantees, and certified operator training, thus reframing the offering around total cost of risk rather than daily rental rates. Over time, regulatory tightening and customer aversion to liability concerns are expected to curb the grey-market threat.

Union-Mandated Operator Certification Bottlenecks

National labour federations negotiated stricter skill verification for forklift drivers in 2024, aligning with updated NR-11 language that requires periodic proficiency tests conducted by accredited schools[4]“NR-11 Atualização 2024,”, Ministério do Trabalho e Emprego, trabalho.gov.br. The limited capacity of approved trainers produces scheduling bottlenecks, delaying new-hire onboarding and, by extension, suppressing rental utilisation. Larger logistics firms hedge the bottleneck by contracting rental packages that include operator staffing, transferring compliance obligations to the lessor. Smaller warehouses, however, face downtime penalties that blunt productivity gains otherwise delivered by rental flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Load Capacity: Sub-3.5 T Units Drive Market Leadership

Sub-3.5 ton forklifts held 48.62% of Brazil forklift rental market share in 2024 while leading growth at a 13.21% CAGR through 2030. Demand intensifies in e-commerce fulfilment centres where narrow aisles and mezzanine pick-lines dominate floor layouts. Rising land prices spur vertical storage strategies, increasing lifts-per-hour metrics that favour nimble electric or LPG models capable of sustained duty cycles. Rental providers standardise parts inventories around this capacity band, keeping maintenance costs low and turnaround times fast. Larger 3.6–10 ton units maintain relevance in port and automotive lineside logistics, yet their lower utilisation and higher fuel consumption restrain growth. Heavy-duty equipment above 10 tons remains a niche rental product tied to mining and steel-plant outages, where custom mast heights and carriage widths discourage broad fleet pooling.

The persistent warehouse imbalance around São Paulo – only 28% classified as modern – deepens reliance on compact trucks that can manoeuvre inside older sheds with column grids unsuited to high-bay racking. Rental companies exploit this topology by bundling fleet-management software, guiding allocation of sub-3.5 ton units across multiple sites, raising asset productivity. Secondary cities such as Campinas and Ribeirão Preto replicate the pattern as suburban fulfilment nodes proliferate, creating a cascading uplift for the segment.

By Rental Duration: Mid-Term Contracts Dominate Despite Short-Term Acceleration

Mid-term rentals covering 1–12 months accounted for 51.29% of Brazil forklift rental market size in 2024, offering the sweet spot between project flexibility and cost predictability. Construction contractors under PAC-3 favour six-month rollovers that match civil-works phases, while 3PLs lock in quarterly contracts to balance seasonal peaks. Short-term agreements under one month register the fastest 12.28% CAGR because of harvest-season surges in agrarian states and emergency call-outs at ports when berth schedules slip. Long-term contracts of 3–5 years shrink as corporate treasurers shun multi-year liabilities amid monetary uncertainty.

Providers optimise fleet mix by redeploying short-term units into mid-term pools once initial depreciation tails off, smoothing revenue seasonality. Digital portals now allow customers to up-size or off-hire at 24-hour notice, reinforcing the variable-cost value proposition. That elasticity is most visible in the Brazil forklift rental market where e-commerce flash sales or climate-driven crop cycles introduce demand spikes too volatile for owned fleets.

By Power Source: ICE Dominance Persists Despite Electric Growth Momentum

Internal combustion forklifts retained 63.87% of Brazil forklift rental market size in 2024 on the back of abundant diesel and LPG distribution channels and lower upfront prices. Nevertheless, electric models post the highest 13.78% CAGR as indoor air-quality mandates spread from food logistics into general merchandise warehouses. Telematics reveal that electric units deliver up to 18% lower per-shift energy cost in constant indoor duty cycles, narrowing the payback gap even with volatile grid tariffs. Hybrid prototypes remain proofs-of-concept, yet rental providers pilot them at multimodal hubs demanding seamless indoor-outdoor rosters.

Operational hurdles include limited charger availability and high peak-load tariffs. Some rental companies offer energy-as-a-service bundles, installing temporary chargers funded through rental premiums, thus inoculating clients against capex. The approach aligns with Lei Do Bem tax perks, further propelling electrification within the Brazil forklift rental market.

By Truck Class: Class V Leadership Contrasts With Class I Growth

Class V counterbalanced forklifts secured 37.28% revenue share in 2024 because they straddle indoor staging and outdoor yard work, indispensable at ports, metallic-parts yards, and big-box DCs. Their pneumatic tyres and higher ground clearance fit Brazil’s often uneven dock aprons. Yet Class I sit-down electrics chart the swiftest 12.33% CAGR, servicing high-throughput pallet moves inside new high-cube warehouses sprung up on São Paulo’s western ring road.

The performance gap underscores evolving building typologies: while legacy facilities still require ruggedised units, new builds incorporate laser-flat floors welcoming battery-powered trucks. Rental providers hedge by maintaining mixed fleets and upselling telemetry add-ons that benchmark energy efficiency across classes, nudging customers gradually toward electrics.

By End-Use Industry: Warehouse and Logistics Sector Concentration

Warehouse and logistics operations dominated at 65.75% of Brazil forklift rental market size in 2024, expanding 12.32% annually as fulfilment nodes multiply near urban consumption centres. PAC-3 construction sites generate stable cross-rentals but represent cyclical income streams tied to federal budget rhythms. Automotive OEMs and tier-ones sustain baseline demand through line-feeding contracts, though real-growth prospects hinge on Brazil’s re-industrialisation incentives. Food and beverage processing maintains a steady rental volume anchored in export-driven cold chains, whereas aerospace and defence require bespoke attachments that restrict fleet fungibility.

The logistics sector’s long runway stems from systematic under-supply: modern speculative warehouse commencements cover only a sliver of new demand, keeping vacancy low and throughput pressure high. Rental fleets plug the gap by rotating units across multi-tenant parks, reducing idle time and widening provider margins even as headline daily rates compress under competitive pressure.

Geography Analysis

São Paulo’s industrial corridor commanded the largest slice of Brazil's forklift rental market in 2024 owing to its dense highway grid, proximity to the Port of Santos, and the country’s deepest inventory of third-party logistics facilities. Vacancy below 5% in prime sub-markets pushes users to maximise cubic throughput, translating into elevated pick rates and corresponding rental uptake of sub-3.5 ton electrics. The region’s exposure to e-commerce giants further accelerates fleet modernisation and telemetry adoption.

Rio de Janeiro and Minas Gerais follow, the former anchored by port-centric energy projects and the latter by mining and steel verticals that demand heavier Class V models. Infrastructure upgrades along the Vitória-Minas railway broaden demand for mid-term rentals as maintenance shutdowns necessitate temporary lifts to avoid production bottlenecks. Meanwhile, Paraná’s agribusiness corridor posts consistent high-season spikes, with rental providers staging satellite yards near soybean storage silos to ensure 24-hour response times.

The Northeast and North benefit disproportionately from PAC-3 allocations—R$816 million via the Northeast Investment Fund and R$350 million from the Amazon Fund—unlocking latent demand for forklifts during rail bed construction and later for intermodal cargo handling. Emerging free-trade zones along the Manaus industrial pole lure electronics assemblers who prefer bundled rental packages that embed operator training, easing entry into Brazil’s complex regulatory fabric. Across all regions, market participants report that the Brazil forklift rental market adapts fleet geography dynamically, redeploying units to chase infrastructure milestones and harvest cycles, underscoring the segment’s operational elasticity.

Analysis of the forklift rental market by Mordor Intelligence spans multiple other regional evaluations across North America, supported by country-level insights for United States, Indonesia, Saudi Arabia, South Korea, and United Arab Emirates, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Competition in the Brazil forklift rental market is moderate, conveying significant yet not monopolistic concentration. Players like Toyota Material Handling Mercosul leverage global manufacturing scale to localise parts supply, lowering Mean Time To Repair and securing multi-year contracts with top 3PLs. KION Group’s Linde and Still brands differentiate through lithium-ion models and data services; their Brazil unit promotes subscription-based “Power by the Hour” plans that mute capex shock for customers. Hyster-Yale Brasil exploits its heavy-duty lineage, securing port contracts in Santos and Paranaguá where high-capacity mast strength is essential.

Local specialists Movicarga, Baloc, and Stemp Empilhadeiras capitalise on regional agility, offering 24-hour field service via motorcycle technicians who navigate congested urban arteries faster than truck-based teams. These firms often bundle certified operators into daily rates, sidestepping union onboarding lags for clients. Competitive vectors increasingly revolve around digital fleet-management portals, predictive analytics, and compliance outsourcing rather than headline rental price.

Recent currency swings compress import margins, incentivising OEMs to expand remanufacturing hubs that refurbish returned lease units for secondary hire. The strategic embrace of circular-economy practices lowers total lifecycle cost and aligns with corporate sustainability scorecards demanded by multinational shippers. As service quality, not machine novelty, becomes the purchase trigger, the Brazil forklift rental market witnesses a recalibration in value narratives centred on uptime, regulatory peace-of-mind, and data-enabled productivity metrics.

Brazil Forklift Rental Industry Leaders

Toyota Material Handling

KION Group

Hyster-Yale

Caterpillar, Inc.

Movicarga

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CSI Remarketing Locação de Equipamentos LTDA. , a wholly-owned subsidiary of CSI Leasing, Inc. (“CSI”), has acquired Somov Rental LTDA. Somov Rental, headquartered in São Paulo, specializes in renting and maintaining forklifts manufactured by Hyster-Yale.

- April 2025: BRL 1.166 billion in regional funds—BRL 816 million from the Northeast Investment Fund and BRL 350 million from the Amazon Investment Fund—were released to accelerate rail and port projects.

- January 2025: The Brazilian government confirmed BRL 94.2 billion for railway infrastructure under PAC-3, aiming to lift rail cargo share to 40% by 2035.

Brazil Forklift Rental Market Report Scope

| Less Than 3.5 T |

| 3.6 - 10 T |

| More Than 10 T |

| Short-term / Spot (less than 1 month) |

| Mid-term (1 - 12 months) |

| Long-term Lease (3 - 5 years) |

| Electric |

| Internal Combustion (Diesel/LPG) |

| Hybrid |

| Class I |

| Class II |

| Class III |

| Class IV |

| Class V |

| Warehousing & Logistics |

| Construction |

| Automotive |

| Food & Beverage |

| Aerospace & Defense |

| Others (Retail, Pharma, etc.) |

| By Load Capacity | Less Than 3.5 T |

| 3.6 - 10 T | |

| More Than 10 T | |

| By Rental Duration | Short-term / Spot (less than 1 month) |

| Mid-term (1 - 12 months) | |

| Long-term Lease (3 - 5 years) | |

| By Power Source | Electric |

| Internal Combustion (Diesel/LPG) | |

| Hybrid | |

| By Truck Class | Class I |

| Class II | |

| Class III | |

| Class IV | |

| Class V | |

| By End-use Industry | Warehousing & Logistics |

| Construction | |

| Automotive | |

| Food & Beverage | |

| Aerospace & Defense | |

| Others (Retail, Pharma, etc.) |

Key Questions Answered in the Report

What is the projected CAGR for the Brazil forklift rental market through 2030?

The segment is forecast to grow at 12.18% annually, taking revenue from USD 1.73 billion in 2025 to USD 3.07 billion by 2030.

Which load-capacity segment leads in both share and growth?

Forklifts under 3.5 tons command 48.62% of 2024 revenue and register the fastest 13.21% CAGR through 2030.

How do high SELIC rates influence rental demand?

Elevated financing costs make ownership expensive, prompting operators to adopt rentals that convert capex into manageable opex.

Why is São Paulo the largest regional market?

Dense warehouse stock, proximity to the Port of Santos, and high e-commerce penetration generate concentrated demand for rental fleets.

How are OEMs differentiating their rental offerings?

Industry leaders now bundle maintenance, operator training, and IoT telemetry into rental contracts, delivering predictable uptime and regulatory compliance.

Page last updated on: