United States Forklift Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

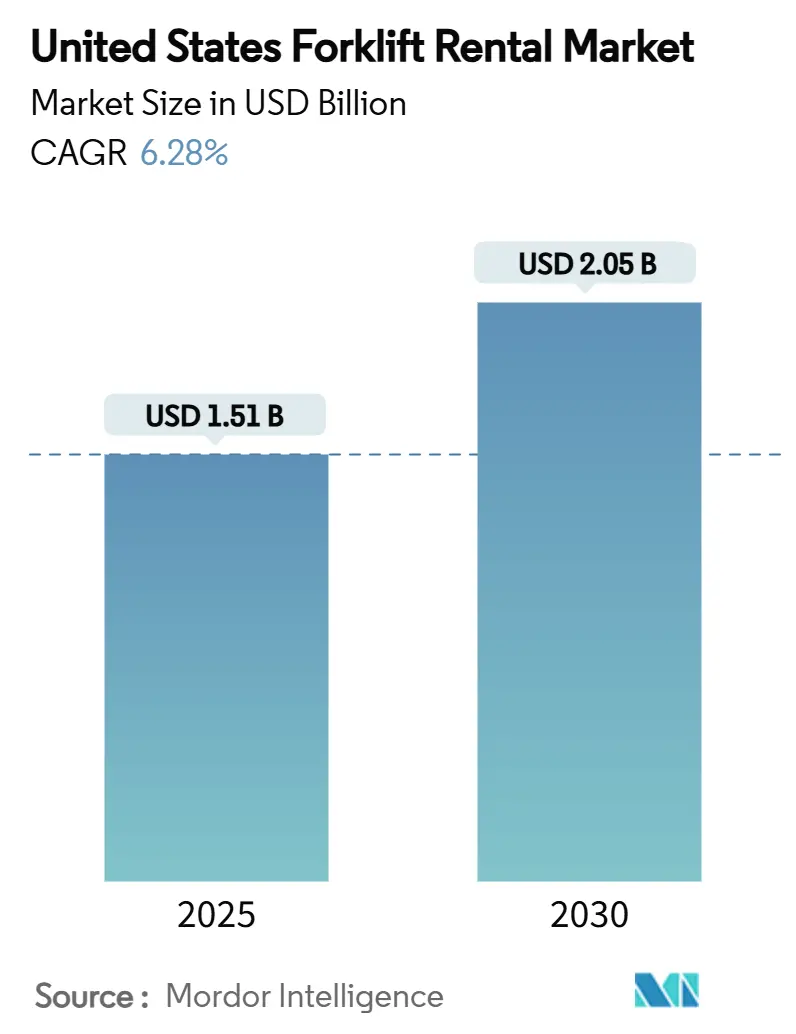

| Market Size (2025) | USD 1.51 Billion |

| Market Size (2030) | USD 2.05 Billion |

| Growth Rate (2025 - 2030) | 6.28% CAGR |

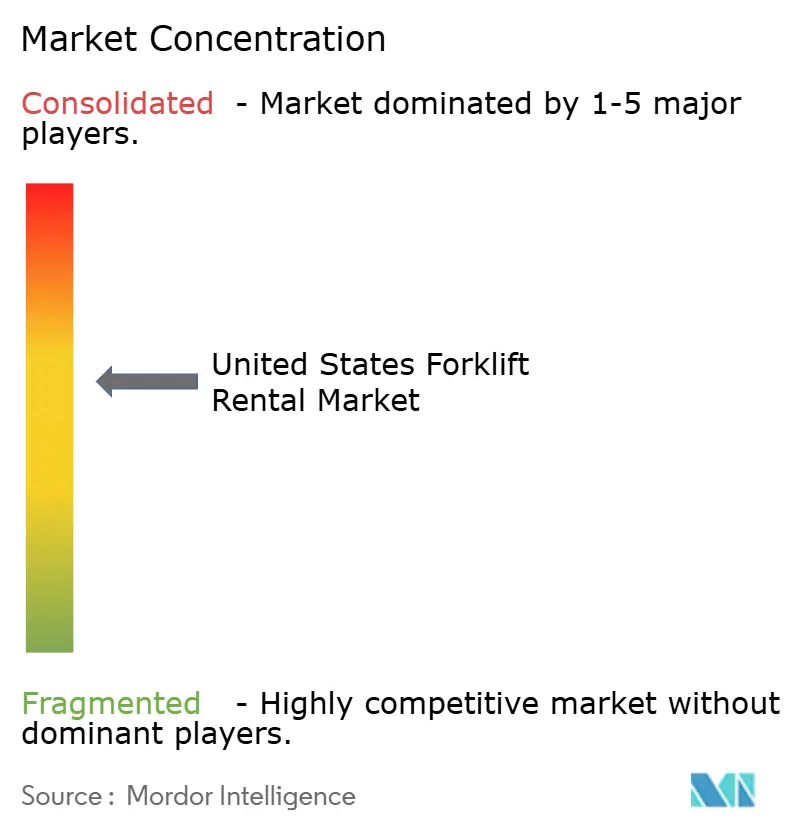

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Forklift Rental Market Analysis by Mordor Intelligence

The United States forklift rental market size is estimated at USD 1.51 billion in 2025 and is forecast to reach USD 2.05 billion by 2030, registering a 6.28% CAGR over the period. Rental penetration is advancing as warehouse operators and construction contractors favor operating flexibility, rapid fleet scaling, and off-balance-sheet treatment of material-handling assets. E-commerce fulfillment, California’s zero-emission mandate for large spark-ignition (LSI) forklifts, and elevated interest rates are the chief forces sustaining demand, while consolidation among large rental houses intensifies competition. In parallel, fleet electrification and telematics adoption help rental providers manage utilization and reduce total cost of ownership, supporting long-term margins.

Key Report Takeaways

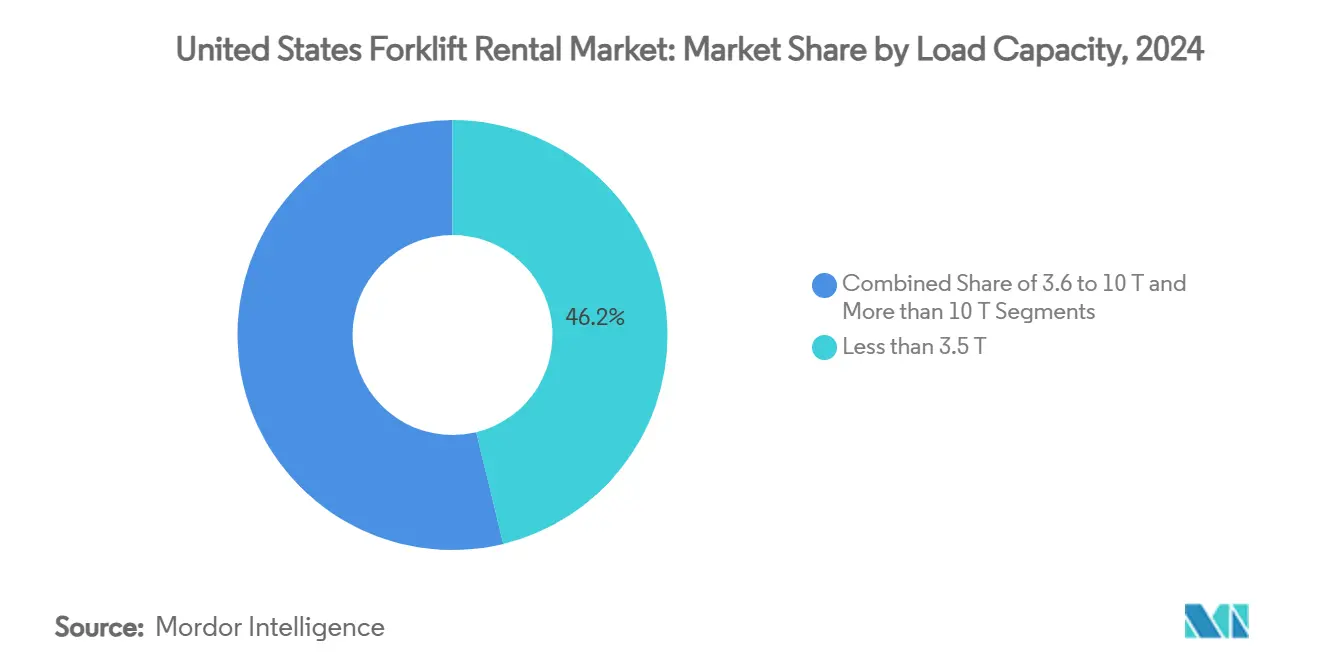

- By load capacity, forklifts under 3.5 tons accounted for 46.18% of the United States forklift rental market in 2024 and are projected to grow at an 8.52% CAGR to 2030.

- By power source, electric forklifts held 58.12% of the United States forklift rental market share in 2024 while registering the fastest forecast growth at 10.73% CAGR through 2030.

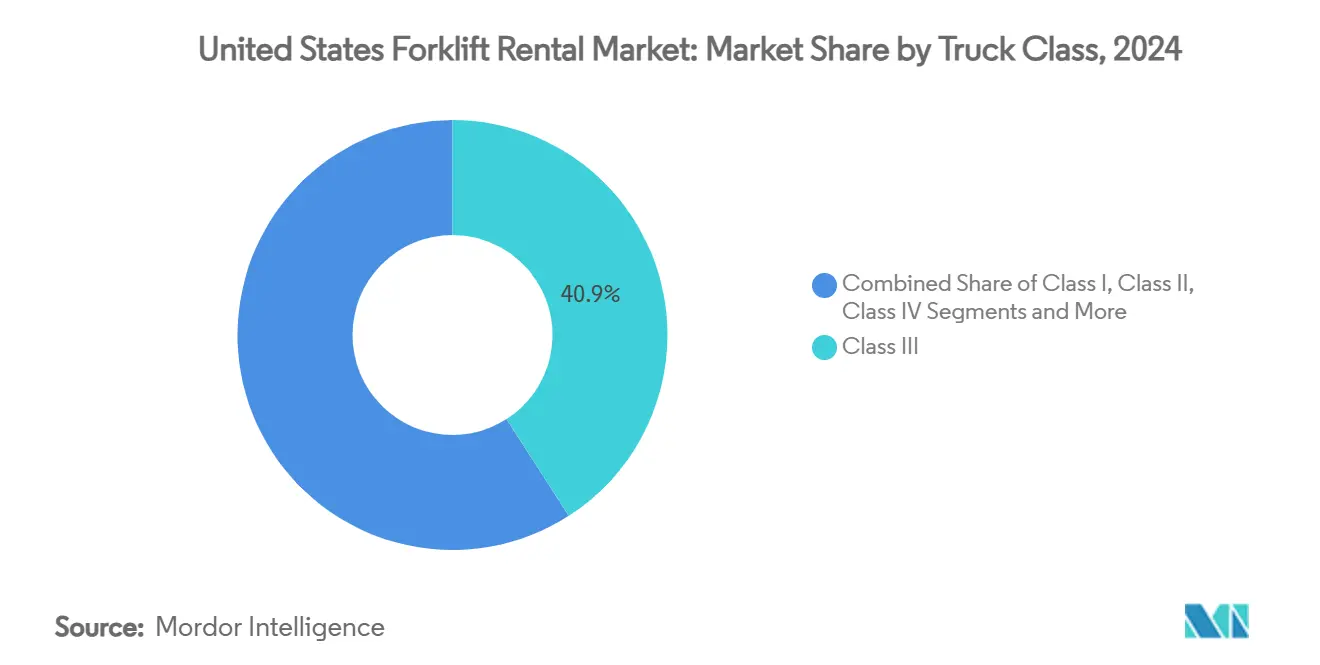

- By truck class, the class III segment accounted for 40.96% of the market share, while the Class I segment registered the highest CAGR of 9.42%.

- By rental duration, short-term contracts captured 51.87% revenue share in 2024; mid-term rentals are projected to expand at 9.04% CAGR over the same period.

- By end-use industry, warehousing and logistics generated 49.14% of 2024 revenue; e-commerce fulfillment is the fastest-rising sub-segment at 11.26% CAGR.

- By region, the South commanded a 30.08% share in 2024, while the West is forecast to grow at an 8.85% CAGR, propelled by California’s zero-emission rules and port-centric logistics.

Global valuation is built by aggregating outputs from multiple countries and regions, with United states being one of the contributors. Our global forklift rental market size represents that cumulative total.

United States Forklift Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Warehousing Surge | +2.1% | National, concentrated in West and South regions | Medium term (2–4 years) |

| CAPEX-Lite Preference in High-Rate Era | +1.8% | National, particularly affecting small-to-medium enterprises | Short term (≤ 2 years) |

| EPA/CARB Rules Driving Electric Rentals | +1.4% | California-led, expanding to Northeast states | Long term (≥ 4 years) |

| OEM Fleet-as-a-Service Uptake | +0.9% | National, with early adoption in industrial corridors | Medium term (2–4 years) |

| Telematics-Based Pay-Per-Use Rentals | +0.6% | National, concentrated in tech-forward metropolitan areas | Long term (≥ 4 years) |

| Micro-Fulfillment Centers Fueling Demand | +0.8% | Urban centers, particularly West Coast and Northeast | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive E-commerce Warehousing Demand

E-commerce fulfillment infrastructure expansion drives forklift rental demand through operational models prioritizing flexibility over fixed asset ownership. The South Coast Air Quality Management District reported over 662 million square feet of warehouse space in its jurisdiction alone, significantly exceeding neighboring regions' capacity[1]"Assessment of Warehouse Relocations Associated with the South Coast Air Quality Management District Warehouse Indirect Source Rule," aqmd.gov.. This concentration creates dense rental demand clusters where operators require rapid fleet scaling capabilities to accommodate seasonal volume fluctuations. Micro-fulfillment centers, designed for last-mile delivery optimization, typically operate with 10,000-50,000 square feet compared to traditional distribution centers' 200,000+ square feet, necessitating smaller, more maneuverable equipment that rental models can efficiently provide. The shift toward urban fulfillment nodes intensifies demand for electric forklifts due to indoor operation requirements and noise restrictions, aligning with rental companies' fleet electrification strategies.

CAPEX-lite Preference Amid Higher Interest Rates

Rising borrowing costs have fundamentally altered equipment acquisition economics, with the Equipment Leasing & Finance Association reporting that 54% of equipment acquisitions utilize financing despite historically high interest rates. Construction equipment costs have increased 27% since the pandemic, while rental rates provide immediate operational access without capital commitment[2]"Managing Equipment Costs with Inflation: When to Rent vs Buy," conexpoconagg.com.. This economic pressure particularly affects small-to-medium enterprises that lack the balance sheet capacity to absorb equipment purchases during inflationary periods. Mitsubishi HC Capital America projects that high inventory levels will make equipment rentals more attractive in 2025, as organizations leverage short-term leases to access new technology without substantial upfront costs. The convergence of elevated interest rates and technological advancement creates a financing landscape where rental models offer superior risk-adjusted returns for operators seeking operational flexibility.

Stricter U.S. EPA/CARB Emission Rules Accelerating Electric Rentals

California's Zero-Emission Forklift Regulation represents the most aggressive emission standard in North America, prohibiting Class IV and V large spark-ignition forklift sales starting January 2026 and requiring fleet phase-outs by 2029. The regulation targets over 89,000 LSI forklifts statewide, with projected nitrogen oxide emission reductions exceeding 2 tons daily by 2031[3]"California’s forklifts to become cleaner and less polluting," California Air Resources Board (CARB), arb.ca.gov.. Rental agencies benefit from regulatory compliance uncertainty as fleet operators prefer rental arrangements over purchasing decisions during transition periods. The regulation includes rental agency requirements mandating compliance with phase-out schedules, creating market opportunities for companies with electric fleet capabilities. Federal emission standards are expected to follow California's lead, with similar regulations anticipated in Northeast states where environmental compliance drives industrial policy.

OEM Fleet-as-a-Service Programs Boosting Rental Penetration

Original equipment manufacturers increasingly offer fleet-as-a-service models that blur traditional rental boundaries, with Toyota Material Handling's Energy Solutions program providing comprehensive electric fleet transitions including consulting services and UL-certified battery combinations. These programs address operator concerns about electric forklift adoption by bundling equipment, maintenance, and energy management into single contracts. Caterpillar's continued strategic relationship with Mitsubishi Logisnext ensures Cat lift truck support through over 600 dealer locations worldwide, demonstrating OEM commitment to service-based revenue models. The integration of telematics data with fleet management systems enables predictive maintenance and usage optimization, creating value propositions that extend beyond traditional rental arrangements. This evolution positions OEMs as fleet partners rather than equipment suppliers, fundamentally altering competitive dynamics in the rental sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Maintenance Liability Concerns | -0.8% | National, particularly affecting first-time rental users | Short term (≤ 2 years) |

| Construction Project Delays | -1.2% | National, with regional variations based on infrastructure spending | Medium term (2–4 years) |

| Lithium-Ion Battery Supply Crunch | -0.6% | National, with supply chain concentration risks | Short term (≤ 2 years) |

| AMR/AGV Cannibalizing Light Forklifts | -0.4% | Industrial corridors, particularly in automated facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Perceived Maintenance Liability and Damage Charges

Rental hesitancy persists among operators concerned about maintenance responsibilities and damage assessments that can exceed predictable operating costs. The Baird/RER Rental Equipment Industry Survey reported Q3 2024 rental revenue growth slowing to 1.9%, the lowest since the pandemic, partly attributed to competitive pressures affecting rental terms and conditions. Damage charge disputes create operational friction that can deter repeat business, particularly among smaller operators lacking dedicated fleet management expertise. Rental companies increasingly offer damage waiver programs and transparent maintenance policies to address these concerns, though implementation varies significantly across regional markets. The perception of hidden costs remains a barrier to rental adoption, especially in price-sensitive segments where ownership economics appear more predictable despite higher capital requirements.

Cyclical Construction Project Delays

Construction industry volatility directly impacts forklift rental demand through project postponements and reduced activity levels during economic uncertainty periods. The American Rental Association's forecast revision from 9.7% to 8.9% growth in 2024 reflects softening construction demand and economic headwinds affecting project initiation. Off-highway equipment manufacturers anticipate a 5% to 10% revenue decline in 2025 due to slowing U.S. economic growth and excess inventories. Construction project delays create demand volatility that complicates fleet planning and utilization optimization for rental companies. However, infrastructure spending from the Infrastructure Investment and Jobs Act provides some demand stability, with USD 1.2 trillion allocated for projects that require material handling equipment support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Load Capacity: Compact Units Drive Market Penetration

Less than 3.5-ton capacity forklifts dominate the market with 46.18% share in 2024 and lead growth projections at 8.52% CAGR through 2030, reflecting the operational requirements of modern fulfillment facilities that prioritize maneuverability over heavy-lifting capacity. E-commerce warehouses typically handle packages weighing under 50 pounds, making compact forklifts optimal for aisle navigation and inventory management tasks. The 3.6 to 10-ton segment serves traditional manufacturing and construction applications where moderate lifting capacity meets most operational needs without the operational complexity of larger units. More than 10-ton capacity forklifts address specialized industrial applications, including steel processing, heavy manufacturing, and port operations, where lifting requirements exceed standard warehouse parameters.

Compact forklift demand acceleration stems from warehouse design evolution toward higher storage density and narrower aisles that maximize cubic utilization. The California Air Resources Board's regulation disproportionately affects larger capacity units, as Class IV and V forklifts targeted for phase-out typically operate in the 3.6-ton and above categories. This regulatory pressure creates rental opportunities as operators transition to compliant equipment without capital investment. Lithium-ion battery technology adoption favors compact units due to energy density advantages and reduced infrastructure requirements compared to larger capacity forklifts that demand substantial charging capabilities.

By Rental Duration: Short-term Flexibility Meets Mid-term Growth

Short-term rentals (less than 1 month) command 51.87% of the market in 2024, driven by seasonal demand fluctuations and project-based requirements that favor operational flexibility over long-term commitments. Mid-term rentals (1 to 12 months) demonstrate the fastest growth at 9.04% CAGR through 2030 as operators balance cost optimization with operational stability during extended projects or capacity expansion phases. Long-term leases (3 to 5 years) serve operators seeking ownership-like benefits while maintaining off-balance-sheet treatment and avoiding technology obsolescence risks.

The shift toward mid-term rental preferences reflects changing customer behavior as operators recognize the cost efficiency of extended contracts while retaining flexibility for fleet adjustments. Southeast Handling Systems emphasizes the importance of rental equipment for managing seasonal demands without ownership costs, which is particularly relevant for businesses experiencing variable operational requirements. Construction project timelines increasingly favor mid-term arrangements as infrastructure spending creates predictable demand periods extending beyond traditional short-term rental windows. The emergence of telematics-enabled usage tracking allows rental companies to offer more sophisticated pricing models that align rental duration with actual equipment utilization patterns.

By Power Source: Electric Dominance Accelerates

Electric forklifts maintain a 58.12% market share in 2024 and exhibit the fastest growth at 10.73% CAGR through 2030, driven by regulatory compliance requirements and operational efficiency advantages in indoor applications. Internal combustion forklifts (diesel/LPG) serve outdoor and heavy-duty applications where electric alternatives face range or power limitations, though market share continues declining as battery technology improves. Hybrid systems represent a transitional technology addressing specific operational requirements where neither pure electric nor internal combustion solutions provide optimal performance characteristics.

California's Zero-Emission Forklift Regulation accelerates electric adoption by eliminating internal combustion alternatives in most applications, creating rental demand as operators avoid purchasing decisions during regulatory transition periods. Lithium-ion battery technology enables over 3,500 cycles with 10,000-12,000 operational hours, significantly exceeding lead-acid battery performance while reducing maintenance requirements. The U.S. battery market for materials handling is projected to reach USD 3 billion annually, with lithium-ion adoption accelerating despite higher initial costs due to total cost of ownership advantages.

By Truck Class: Class III Warehouse Applications Lead

Class III forklifts command 40.96% market share in 2024, reflecting their suitability for warehouse applications where electric power and compact design optimize indoor operations. Class I forklifts demonstrate the fastest growth at 9.42% CAGR through 2030 as automated facilities require precise positioning capabilities and integration with warehouse management systems. Class II units serve specialized applications, including narrow aisle operations and order picking tasks that demand specific performance characteristics. Class IV and V forklifts face regulatory pressure from emission standards while serving heavy-duty applications with limited electric alternatives.

The dominance of Class III units aligns with e-commerce fulfillment requirements where indoor operations, noise restrictions, and emission concerns favor electric counterbalance forklifts. Fox Robotics' partnership with KION North America to assemble autonomous lift trucks demonstrates the integration of automation technology with traditional forklift classifications. Class I growth acceleration reflects warehouse automation trends where reach trucks and order pickers integrate with automated storage and retrieval systems. The California regulation specifically targets Class IV and V units for phase-out, creating rental opportunities as operators transition to compliant alternatives without capital investment.

By End-use Industry: Warehousing Dominance with E-commerce Acceleration

Warehousing and logistics applications account for 49.14% of the market share in 2024, with e-commerce warehousing specifically growing at 11.26% CAGR through 2030 as fulfillment networks expand to meet consumer delivery expectations. Construction applications serve project-based demand where rental models align with variable activity levels and equipment requirements. Automotive industry applications reflect manufacturing process requirements and supply chain logistics that demand reliable material handling capabilities. Food and beverage operations require specialized equipment meeting sanitary standards and temperature-controlled environments.

E-commerce warehousing growth acceleration stems from last-mile delivery optimization, requiring distributed fulfillment networks with flexible equipment requirements. The warehouse automation market is projected to reach USD 27 billion by 2025, driven by e-commerce growth and labor shortages exacerbated by COVID-19. Aerospace and defense applications demand specialized equipment that meets security and performance requirements and that rental models can efficiently provide without long-term capital commitments. Other industries, including retail and pharmaceutical operations, are increasingly adopting rental strategies to manage seasonal demand variations and operational flexibility requirements.

Geography Analysis

The South’s leadership hinges on diversified industrial demand, robust port throughput, and a favorable tax environment that attracts corporate relocations. The region captures 30.08% of the market share, while the western region is the fastest growing with 8.85% CAGR.Texas and Florida posted double-digit warehouse construction growth in 2024, underpinning stable lift-truck utilization. A consistent base of automotive, petrochemical, and aerospace plants ensures year-round rental activity despite cyclical swings in any single sector.

The West enjoys the highest growth trajectory given California’s forklift emission mandate and a concentration of import gateways at Los Angeles and Long Beach. Warehouse vacancy in the Inland Empire fell below 4% in 2025, spurring speculative builds that rapidly convert to rental contracts. Technology firms in Silicon Valley pilot autonomous forklifts, requiring rental partners capable of servicing advanced navigation and safety systems.

Northeast and Midwest markets post steady, modest gains. Dense population supports continuous retail fulfillment needs in New Jersey and Pennsylvania, while Ohio and Michigan automotive hubs generate predictable demand for Class IV and specialized heavy electrics. Infrastructure Investment and Jobs Act funding for bridge rehabilitation across the Ohio River and rail hub upgrades near Chicago ensures sustained rentals for rough-terrain units.

Coverage of the forklift rental market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, alongside detailed country-level intelligence for Brazil, Indonesia, Saudi Arabia, South Korea, and United Arab Emirates, each shaped by local operating conditions.

Competitive Landscape

Market structure is moderately fragmented. United Rentals, Sunbelt Rentals, and Herc Rentals hold a significant share, leveraging national depots, purchasing power, and technology platforms. The fragmented nature of the remaining market creates opportunities for regional players and specialty providers to serve niche applications and local markets where scale advantages are less pronounced.

Regional independents remain agile by focusing on service responsiveness and niche equipment—such as freezer-rated electrics or explosion-proof models—where scale offers limited advantage. OEM-linked lessors, including Toyota, Raymond, and Crown branches, reinforce customer loyalty by bundling parts availability, maintenance, and operator training. Digital entrants like BigRentz aggregate surplus fleet inventory through online marketplaces, though their share remains below 2%.

Technological differentiation centers on telematics, predictive maintenance, and customer-facing apps that streamline rental cycles and billing. Electrification readiness is a critical battleground: fleets with high proportions of lithium-ion units secure priority contracts in California and the Northeast, where emission compliance is non-negotiable. Integration with warehouse management systems and AMR/AGV platforms is emerging as the next competitive frontier.

United States Forklift Rental Industry Leaders

-

United Rentals

-

Sunbelt Rentals (Ashtead Group)

-

Herc Rentals

-

Toyota Material Handling USA

-

Crown Equipment Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Herc Holdings completed its USD 5.3 billion acquisition of H&E Equipment Services, including USD 1.5 billion in debt, creating the third-largest rental company in North America with combined annual revenue of approximately USD 5.2 billion. The transaction enhances Herc's geographic footprint and operational scale while generating expected annual EBITDA synergies of USD 300 million.

- June 2024: California Air Resources Board adopted the Zero-Emission Forklift Regulation, mandating the phase-out of large spark-ignition forklifts starting January 2026. The regulation affects over 89,000 LSI forklifts statewide and creates significant rental market opportunities as operators transition to compliant equipment.

- May 2024: WMH Solutions partnered with KION North America to distribute Linde Material Handling equipment, enhancing product offerings and market position in the southeastern U.S. The collaboration emphasizes environmental sustainability and hydrogen fuel cell technology.

United States Forklift Rental Market Report Scope

| Less than 3.5 T |

| 3.6 to 10 T |

| More than 10 T |

| Short-term/Spot (Less than 1 month) |

| Mid-term (1 to 12 months) |

| Long-term Lease (3 to 5 years) |

| Electric |

| Internal Combustion (Diesel/LPG) |

| Hybrid |

| Class I |

| Class II |

| Class III |

| Class IV |

| Class V |

| Warehousing and Logistics |

| Construction |

| Automotive |

| Food and Beverage |

| Aerospace and Defense |

| Others (Retail, Pharma, etc.) |

| Northeast |

| Midwest |

| South |

| West |

| By Load Capacity | Less than 3.5 T |

| 3.6 to 10 T | |

| More than 10 T | |

| By Rental Duration | Short-term/Spot (Less than 1 month) |

| Mid-term (1 to 12 months) | |

| Long-term Lease (3 to 5 years) | |

| By Power Source | Electric |

| Internal Combustion (Diesel/LPG) | |

| Hybrid | |

| By Truck Class | Class I |

| Class II | |

| Class III | |

| Class IV | |

| Class V | |

| By End-use Industry | Warehousing and Logistics |

| Construction | |

| Automotive | |

| Food and Beverage | |

| Aerospace and Defense | |

| Others (Retail, Pharma, etc.) | |

| By Region (U.S.) | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

How big is the United States forklift rental market in 2025?

The market generated USD 1.51 billion in 2025 and is on course to reach USD 2.05 billion by 2030.

Which forklift type dominates U.S. rentals?

Electric models lead with 58.12% 2024 share and are forecast to grow 10.73% CAGR as emission regulations tighten.

Why are mid-term rental contracts gaining traction?

Operators use 1–12 month rentals to lock in availability at better rates while retaining fleet flexibility during multishift projects.

How will California’s zero-emission rule affect demand?

The 2026 ban on new LSI forklifts will accelerate electric rentals, lifting West Coast rental revenue at an 8.85% CAGR.

Which companies hold the largest market positions?

United Rentals, Sunbelt Rentals and Herc Rentals collectively control about one-third of U.S. forklift rental revenue.

What impact do high interest rates have on equipment decisions?

Elevated borrowing costs make ownership less attractive, pushing rental penetration toward 56.4% across material-handling equipment.

Page last updated on: