Brazil Construction Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

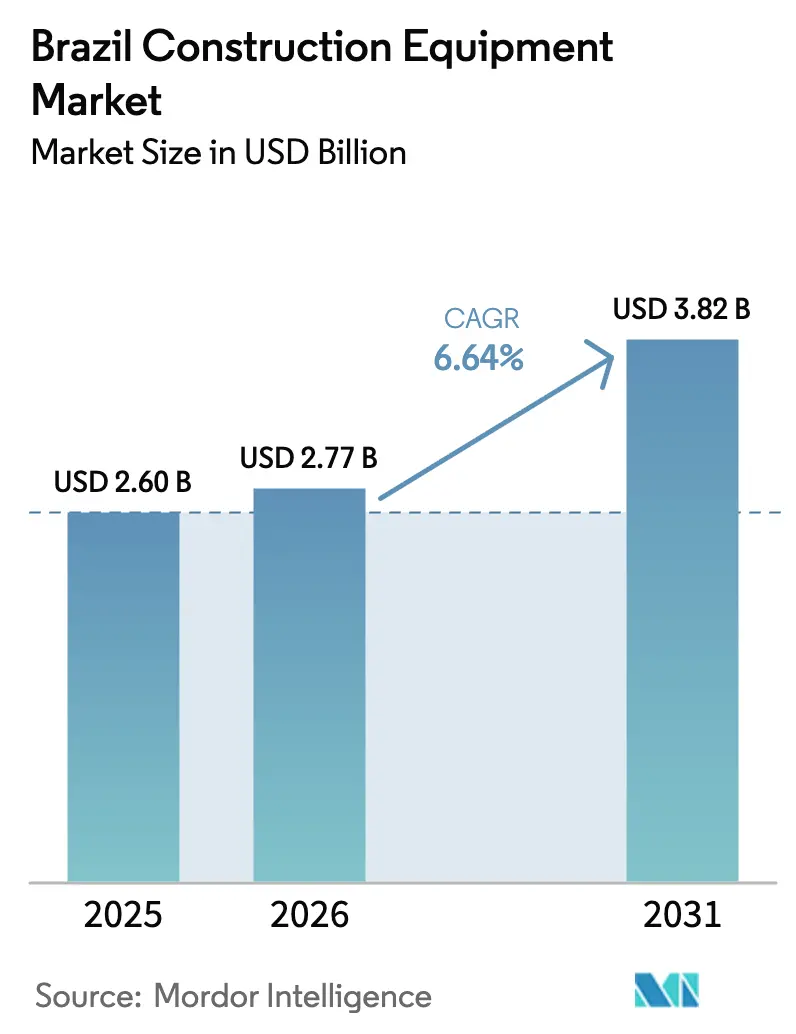

| Base Year Market Size (2025) | USD 2.60 Billion |

| Market Size (2026) | USD 2.77 Billion |

| Market Size (2031) | USD 3.82 Billion |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Construction Equipment Market Analysis by Mordor Intelligence

The Brazil construction equipment market size is projected to expand from USD 2.60 billion in 2025 and USD 2.77 billion in 2026 to USD 3.82 billion by 2031, registering a CAGR of 6.64% between 2026 and 2031. Fleet evolution in the Brazilian construction equipment market is shifting toward infrastructure-grade earthmoving and material-handling assets as the federal PAC-3 program revives stalled highway and sanitation projects, while green-hydrogen mega-sites anchor long-cycle demand in the Northeast. While excavators continue to be the primary revenue drivers, telescopic handlers are gaining momentum, fueled by modular social housing projects and large-scale renewable energy hubs. Battery-electric platforms, still niche, are gaining visibility after mining majors began field trials of zero-emission haul trucks in Pará and Minas Gerais, signaling an eventual powertrain transition that OEMs cannot ignore. Competitive stakes are rising as Chinese assemblers deepen completely-knocked-down (CKD) footprints in Minas Gerais, eroding price points that global incumbents defend through autonomy, telematics, and hybrid-electric differentiation.

Key Report Takeaways

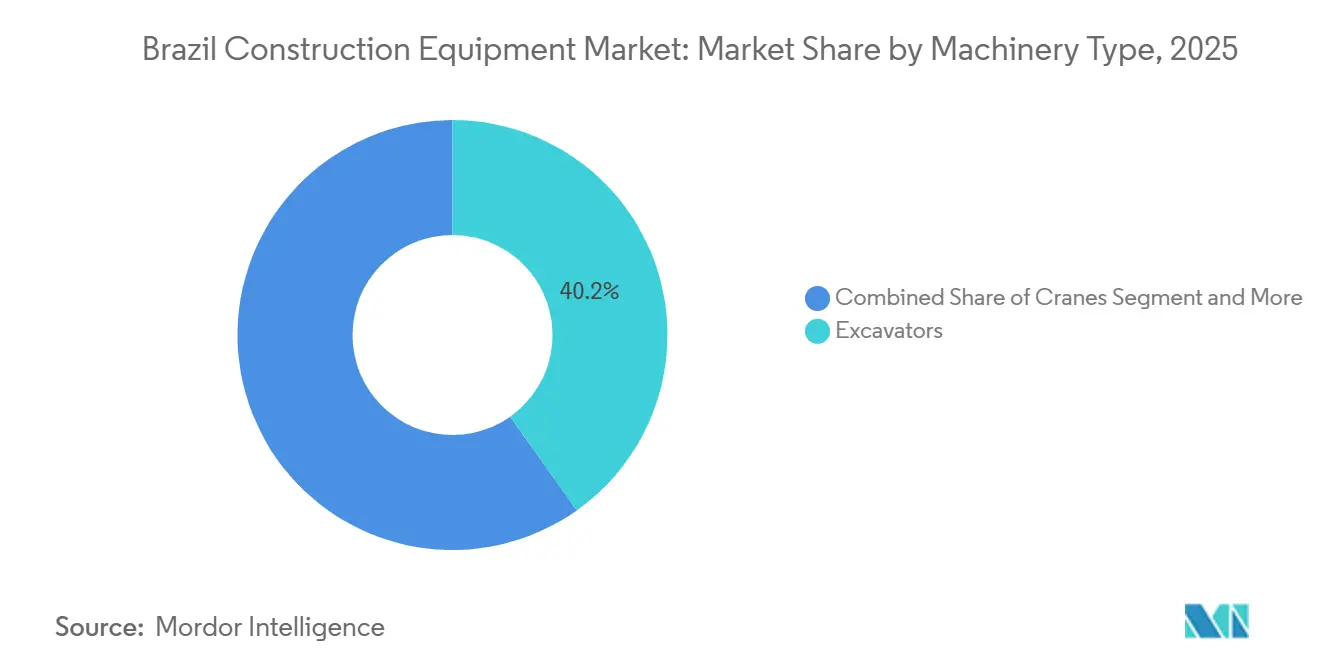

- By machinery type, excavators led with 40.15% of Brazil's construction equipment market share in 2025, while telescopic handlers are forecast to post the fastest 7.45% CAGR through 2031.

- By propulsion, internal-combustion platforms accounted for 92.33% of the Brazilian construction equipment market size in 2025, and battery-electric units are advancing at a 14.05% CAGR to 2031.

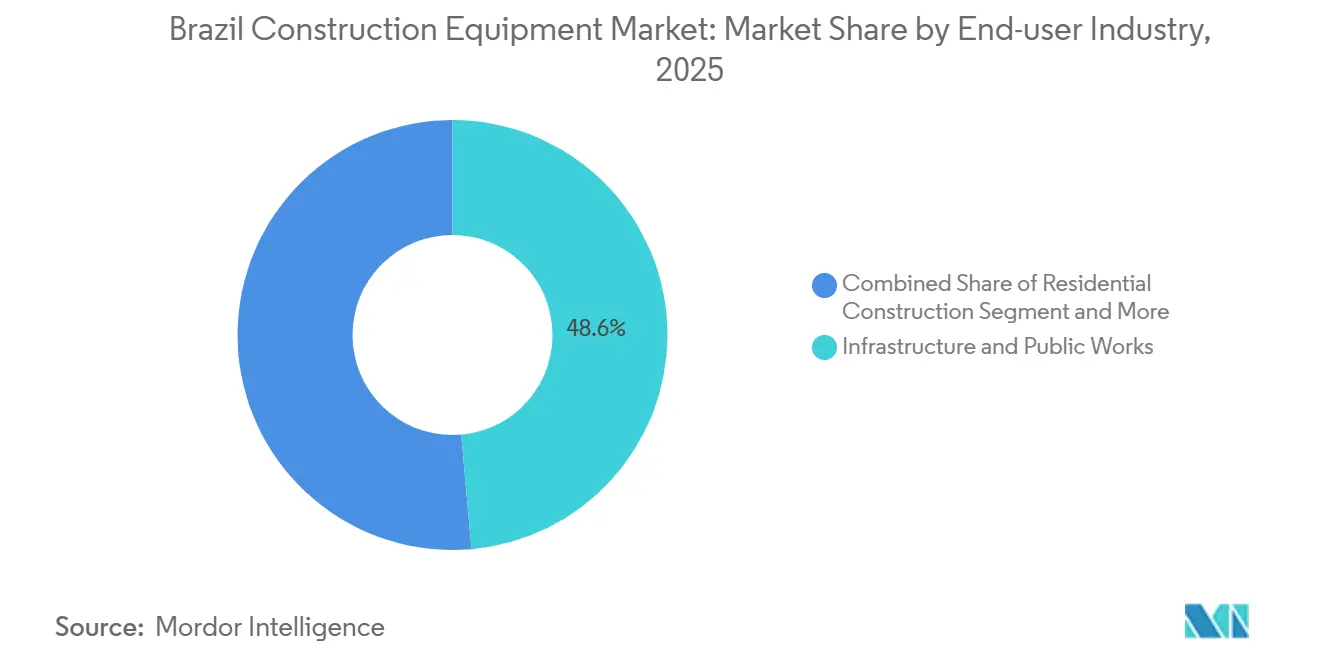

- By end-user, infrastructure and public works held 48.56% revenue in 2025; energy projects are projected to expand at a 9.01% CAGR to 2031.

- By application, road building and paving is growing at a 9.63% CAGR between 2026 and 2031, outpacing earthmoving’s established base of 59.13% in 2025 revenue.

- By region, the North region is the fastest-growing cluster at a 7.94% CAGR to 2031, while the Southeast retains 54.28% of 2025 demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PAC-3 Infrastructure Revival | +1.2% | National (Southeast/South focus) | Medium term (2-4 years) |

| Minha Casa Minha Vida Housing | +1.0% | National (São Paulo, Rio, Brasília) | Short term (≤ 2 years) |

| Mining Royalty Earmarks | +0.9% | North/Central-West (spill-over to SE) | Medium term (2-4 years) |

| Utility-Scale Green-Hydrogen Hubs | +0.8% | Northeast and Southeast | Long term (≥ 4 years) |

| Chinese OEM CKD Expansion | +0.7% | Northeast and Southeast | Medium term (2-4 years) |

| 5G-Enabled Remote-Operation | +0.3% | North (Pará/Amazonas pilots) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal PAC-3 Infrastructure Pipeline Revival

Under the Growth Acceleration Program's third cycle, Brazil has allocated significant funding for civil-works spending by 2026. However, by late 2025, only a small portion of the initial projects were completed, primarily due to budget freezes that delayed contract awards. As a result, contractors find themselves in a constant state of flux: they rent excavators and graders during funding delays but swiftly transition to purchasing fleets once financing is confirmed. In response, equipment vendors have started bundling services like telematics and rental buy-back clauses. They've also introduced flexible payment schedules aligned with the PAC-3 tranche releases, ensuring revenue protection even amidst shifting tender calendars. The most significant potential lies in highway and railway projects, which are expected to receive substantial allocations for 2025–2026 [1]“Infrastructure 2025,” National Confederation of Industry, cni.com.br. However, whether this momentum translates to sustained growth hinges on the federal government's ability to shorten permitting lead times, a process that has historically extended project timelines by several years.

Minha Casa Minha Vida" Phase-IV Social-Housing Push"

In 2024, government guarantees spurred significant housing contracts, with ambitions for further growth by 2027, dominating the nation's housing launches. The program's focus on repetitive, low-rise footprints has shifted site logistics, prioritizing backhoe loaders, mini excavators, and skid steers over traditional tower cranes. Mills Estruturas, with control over a substantial number of rental units across the country, has emerged as the primary beneficiary of these orders, underscoring the growing trend of a rental-first procurement model at urban job sites. While short-term demand appears strong, any tightening of subsidy tranches could lead to a swift reduction in unit shipments, highlighting the critical need for OEMs to maintain working-capital agility.

New Mining Royalty Earmarks for Roadworks (2025-2029)

Brazil's miners are set to make significant investments into capital programs by 2029, with a notable portion allocated specifically for haul roads and logistics spurs. These investments aim to circumvent the congested export corridors. Notably, Vale has earmarked a substantial amount for its 2025 capital expenditures, directing much of this towards remote routes tailored for autonomous truck platoons [2]“Investment Plan 2025,” Vale SA, vale.com. As a result, there's been a noticeable uptick in demand for heavy-duty graders, high-tonnage dump trucks, and continuous-duty compactors. Given that private miners are self-financing these corridors, they enjoy shorter lead times compared to public-sector projects. This efficiency not only accelerates the development process but also establishes a reliable revenue stream in the North and Central-West regions. Furthermore, suppliers are capitalizing on this environment, using it as a testing ground for dual-fuel haul trucks. These innovative trucks, which combine diesel with ethanol, manage to reduce haulage costs.

Rapid Expansion of Utility-Scale Green-Hydrogen Hubs

Fortescue, Solatio, and a World Bank-backed consortium have mega-projects in Pecém, requiring extensive earthworks before the arrival of electrolyzers. In a bid to meet their Scope 1 and 2 reduction commitments, developers are increasingly turning to hybrid or battery-electric excavators. This shift has prompted OEMs to prioritize positioning their premium, low-volume green fleets in Ceará and Piauí. Given that environmental permitting can take years, the anticipated growth will only be realized once these projects move from the feasibility stage to obtaining necessary clearances.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SELIC Rates Dampening CAPEX | -0.9% | National, acute in Central-West and Northeast | Short term (≤ 2 years) |

| Shift Toward Equipment Rental | -0.6% | National, strongest in Southeast and South | Short term (≤ 2 years) |

| Logistics Bottlenecks at Ports | -0.5% | Southeast and South, affecting national supply | Medium term (2-4 years) |

| Import Duties on Tier-4 Engines | -0.4% | National, higher on imported premium brands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High SELIC Rates Dampening SME Capex

In January 2025, the benchmark rate was high, with expectations of further increases by March. As a result, small builders are hesitant to engage in long-term debt structures, which now come at significantly higher financing costs compared to 2023. This tightening in the macro environment is steering SME contractors in Mato Grosso and Pernambuco towards opting for secondhand or rental fleets. This shift is expected to negatively impact forecasted growth. Meanwhile, OEM captive-finance arms are attempting to navigate this landscape by cross-subsidizing interest or deferring principal payments until project milestones are met. However, despite these efforts, the uptake has been tepid, primarily due to ongoing rate volatility.

Accelerating Shift Toward Equipment Rental

Mills Estruturas, having acquired Armac, now boasts the largest multi-brand fleet in the country. They provide backhoes and boom lifts on flexible contracts, ensuring contractors maintain cash flow during project lotteries. In São Paulo's high-rise sites, rental penetration has grown significantly and is now extending to regional roadworks. This trend is reducing OEM unit sales, despite a surge in utilization. To counteract thinner margins on new machines, manufacturers are increasingly wooing rental consolidators. They're offering volume rebates and integrating telematics that highlight preventive maintenance, thus creating a steady annuity from parts and services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Excavators Anchor Demand, Telescopic Handlers Surge

Excavators captured 40.15% of Brazil's construction equipment market share in 2025 on the back of multi-year highway and mining dig programs that need 20-ton to 50-ton hydraulic units at scale. Komatsu’s plan to nationalize the PC500LC-10M0 large excavator at Suzano underlines OEM faith in earthmoving’s staying power. Telescopic handlers are forecast to grow at a 7.45% CAGR, well above the overall Brazil construction equipment market size trajectory, as modular housing and large solar fields require rapid vertical reach in space-constrained footprints.

Wheel-loader demand dipped in 2024 as contractors favored mini excavators for tight urban plots, yet graders and compactors rallied in the Amazon-bound BR-163 upgrade. Niche lines such as heavy-lift lattice cranes remain tied to delayed high-rise pipelines in São Paulo and Rio de Janeiro, limiting volumes until financing costs recede. Across categories, price pressure intensifies where Chinese CKD imports overlap, while premium lift and reach segments retain double-digit margins because fewer domestic production lines compete.

By Propulsion: Internal Combustion Dominates, Battery-Electric Gains Momentum

Internal-combustion platforms held 92.33% of 2025 demand in the Brazilian construction equipment market, leveraging a dense diesel network and ethanol blending flexibility. Battery-electric units, now seeded in Vale’s zero-emission haul-truck pilots, will post a 14.05% CAGR through 2031, raising the Brazil construction equipment market size for high-voltage components and fast-charge depots. Hybrid-electric loaders bridge range anxiety while Stage V norms remain voluntary, drawing in city contractors facing local air-quality mandates in São Paulo.

XCMG’s delivery of several pure-electric dump trucks validates the Chinese OEM's ambition to leapfrog combustion incumbents, while Volvo CE’s Brazilian upgrade fund earmarks assembly space for hybrid excavators. Uptake, however, still hinges on lithium-ion cost curves and grid upgrades beyond coastal metros, especially in the Amazon corridor, where diesel logistics outcompete scarce charging.

By End-User Industry: Infrastructure Leads, Energy Projects Accelerate

Accelerated tender pipelines for highways and rail spurs under the PAC-3 initiative led infrastructure and public works to account for 48.56% of the 2025 revenue. Energy developments will grow at a 9.01% CAGR, outpacing the broader Brazil construction equipment market, spurred by Petrobras offshore upgrades and a 15-GW onshore wind queue that needs cranes, dozers, and all-terrain transporters. Residential starts surged under Minha Casa Minha Vida, yet now decelerate alongside fiscal scrutiny and elevated mortgage rates, steering OEM attention toward civil and energy megaprojects with deeper pockets and predictable drawdowns.

Mining steadies baseline demand for ultra-class excavators and 150-ton haulers as Vale, CSN, and Anglo American maintain significant capital envelopes focused on low-strip, high-grade deposits. Commercial real estate lags, with occupancy rates yet to reclaim pre-pandemic benchmarks, curtailing tower-crane bookings beyond a few marquee CBD sites.

By Application: Earthmoving Dominates, Road Building Surges

Earthmoving claimed 59.13% of 2025 equipment volume, mirroring Brazil’s vast cut-and-fill obligations across plateau and rainforest terrains. Road-building and paving applications will grow at 9.63% through 2031, eclipsing earthmoving’s base growth as BR-163 and mineral-royalty corridors mobilize graders, pavers, and soil compactors at scale. Material-handling orders follow e-commerce warehouse booms and modular housing logistics, while demolition stays a São Paulo and Rio niche anchored to brownfield redevelopment.

Tunnel-boring and underground works pick up marginally alongside metro extensions but remain CAPEX-heavy slots suited to a handful of specialized OEMs. Attachment suppliers ride each wave by bundling breakers, augers, and grapple kits that elevate per-unit invoice values without large capital outlays.

Geography Analysis

In the Brazilian construction equipment market, the Southeast captured 54.28% of the 2025 demand, driven by its proximity to Santos port, a dense dealer network, and ongoing metro extension projects. This region's strategic advantages have positioned it as a dominant player in the market. Meanwhile, the North region is set to experience significant growth, with a projected CAGR of 7.94%. This growth is fueled by infrastructure upgrades to BR-163 and mining-led logistics activities, which are increasing the demand for graders and 50-ton excavators, particularly in Pará and Amazonas. These developments highlight the region's growing importance in the construction equipment market.

The Northeast is emerging as a key area of focus, leveraging the hydrogen boom to drive demand for construction equipment. Multi-billion-dollar hydrogen hubs in Pecém and Parnaíba are expected to attract cranes and heavy dozers between 2026 and 2031. This surge in activity underscores the region's potential as a hub for renewable energy infrastructure. In contrast, the Central-West region's spending is concentrated on widening grain corridors rather than large-scale civil construction projects. This focus has moderated growth in the region, with order books reflecting nominal growth rates. Despite this, the region remains an essential contributor to the overall market dynamics.

The South faces challenges stemming from a slowdown in the real estate sector, which is tied to persistently high SELIC rates. This has created a drag on the region's construction equipment demand. However, OEMs that proactively establish parts depots in strategic locations such as Belém, Manaus, and Fortaleza are well-positioned to outperform competitors. By addressing logistical challenges, these OEMs can maintain a competitive edge in the market.

Competitive Landscape

Global majors Caterpillar, Komatsu, Volvo CE, CNH Industrial, and Deere together command a notable share of the Brazilian construction equipment market, yet Chinese entrants are eroding boundaries via CKD economics. XCMG’s Pouso Alegre plant already ships several units annually and now adds an electric-truck wing, while SANY and LiuGong layer USD-scale tranches that neutralize import levies and amplify payment flexibility [3]“Pouso Alegre Plant Milestone Report,” XCMG Brasil, xcmg.com.

Incumbents strike back with autonomy and hybrid portfolios: Komatsu investing to localize the WA380-6 loader, will double engineering headcount to tailor fuel-tolerant hydraulics; Caterpillar inks a yearly Vale pact for dual-fuel, autonomy-ready fleets, locking in parts annuities and software subscriptions.

Specialists like Dynapac and Astec defend compaction and asphalt niches through rapid service SLAs where scale is less decisive. Technology adoption cleaves the field: Tier-1 miners and energy EPCs demand 5G-ready, analytics-driven fleets, while SME builders still chase the lowest acquisition cost. Regulatory drift toward municipal emission caps will likely hasten a split, with premium OEMs dominating high-utilization, high-spec segments and CKD assemblers sweeping budget urban and rural jobs.

Brazil Construction Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Volvo Construction Equipment (Volvo CE)

Deere and Company

CNH Industrial N.V. (Case CE and New Holland)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Hiab agreed to acquire local crane maker ING Cranes, strengthening its Brazilian load-handling portfolio and expanding market access.

- October 2025: Cunzolo Máquinas e Equipamentos added a 230-ton Liebherr LTM 1230-5.1 all-terrain crane to serve tower crane assembly, industrial maintenance, and construction lifts around São José dos Campos.

- September 2025: Vertical Equipamentos purchased a Liebherr LTC 1050-3.1 compact crane, the first of its type in Brazil, targeting refinery and petrochemical plant turnarounds.

- March 2025: ZAMine Service Brasil, a Hitachi–Marubeni joint venture, opened to supply and service Hitachi mining excavators, reinforcing aftermarket parts opportunities as the installed base grows.

Brazil Construction Equipment Market Report Scope

The scope includes segmentation by machinery type (excavators, wheel loaders and backhoes, cranes, motor graders, telescopic handlers, and others), propulsion (internal-combustion engine, hybrid-electric, and battery-electric), end-user industry (infrastructure and public works, residential construction, commercial real-estate, mining and quarrying, and energy projects), and application (earthmoving, material handling, road building and paving, demolition and recycling, and tunnelling and underground works). The analysis also covers regional-level segmentation, including North, Northeast, Central-West, Southeast, and South. Market size and growth forecasts are presented by value in USD and by volume in units.

| Excavators |

| Wheel Loaders and Backhoes |

| Cranes |

| Motor Graders |

| Telescopic Handlers |

| Others (Compactors, Pavers, etc.) |

| Internal-Combustion Engine |

| Hybrid-Electric |

| Battery-Electric |

| Infrastructure and Public Works |

| Residential Construction |

| Commercial Real-Estate |

| Mining and Quarrying |

| Energy Projects (Oil, Gas and Renewables) |

| Earthmoving |

| Material Handling |

| Road Building and Paving |

| Demolition and Recycling |

| Tunnelling and Underground Works |

| North Region |

| Northeast Region |

| Central-West Region |

| Southeast Region |

| South Region |

| By Machinery Type | Excavators |

| Wheel Loaders and Backhoes | |

| Cranes | |

| Motor Graders | |

| Telescopic Handlers | |

| Others (Compactors, Pavers, etc.) | |

| By Propulsion | Internal-Combustion Engine |

| Hybrid-Electric | |

| Battery-Electric | |

| By End-user Industry | Infrastructure and Public Works |

| Residential Construction | |

| Commercial Real-Estate | |

| Mining and Quarrying | |

| Energy Projects (Oil, Gas and Renewables) | |

| By Application | Earthmoving |

| Material Handling | |

| Road Building and Paving | |

| Demolition and Recycling | |

| Tunnelling and Underground Works | |

| By Region | North Region |

| Northeast Region | |

| Central-West Region | |

| Southeast Region | |

| South Region |

Key Questions Answered in the Report

How large will the Brazil construction equipment market be in 2031?

The market is forecast to reach USD 3.82 billion by 2031, up from USD 2.77 billion in 2026.

Which machinery category holds the biggest share of demand?

Excavators lead with 40.15% of 2025 revenue because they serve diverse earthmoving tasks across infrastructure and mining sites.

What is the fastest-growing equipment category?

Telescopic handlers are projected to grow at a 7.45% CAGR through 2031 as modular housing and renewable-energy projects expand.

Which region will grow fastest by 2031?

The North is set to advance at a 7.94% CAGR, supported by BR-163 upgrades and mining-driven roadworks that need graders and compactors.

Are battery-electric machines gaining traction?

Yes, pilots with pure-electric haul trucks and hybrid excavators are accelerating, driving a 14.05% CAGR for battery-electric units through 2031.

Page last updated on: