Electric Forklift Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

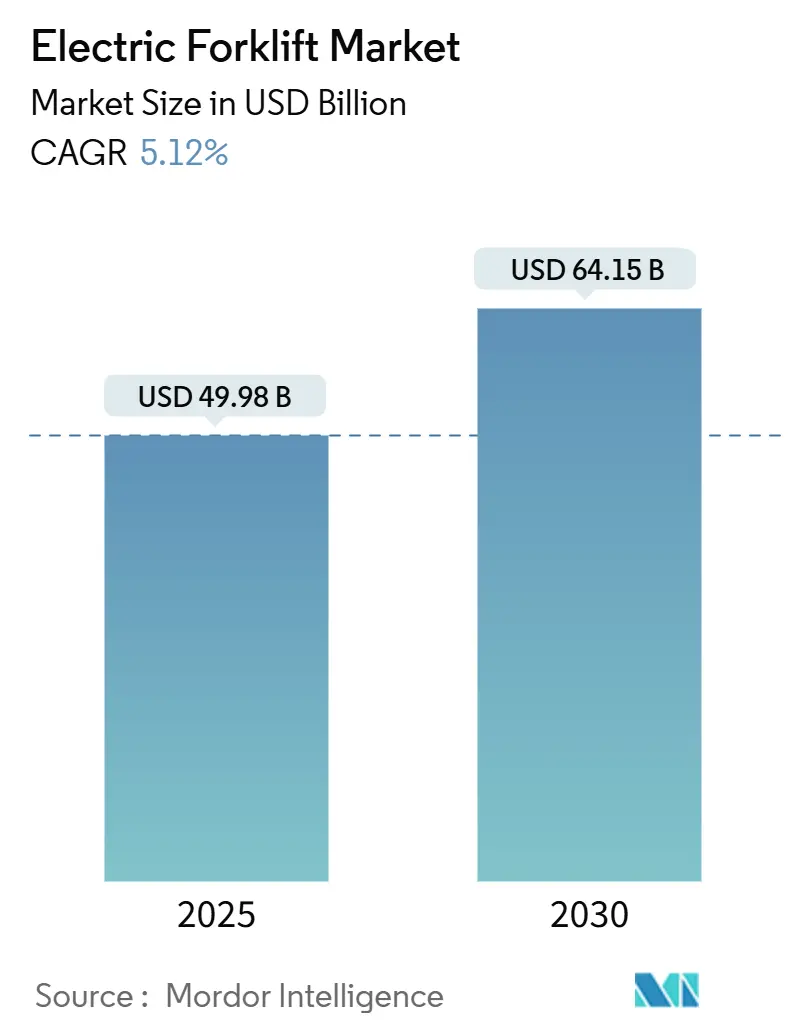

| Market Size (2025) | USD 49.98 Billion |

| Market Size (2030) | USD 64.15 Billion |

| Growth Rate (2025 - 2030) | 5.12% CAGR |

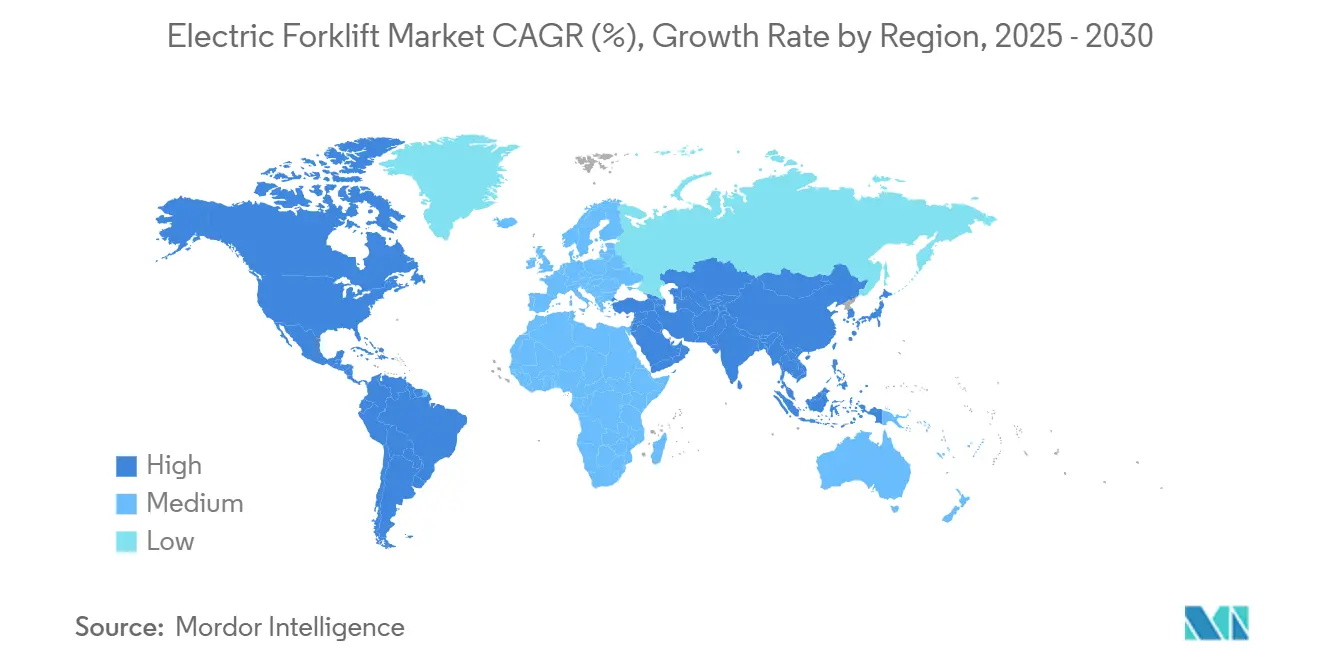

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

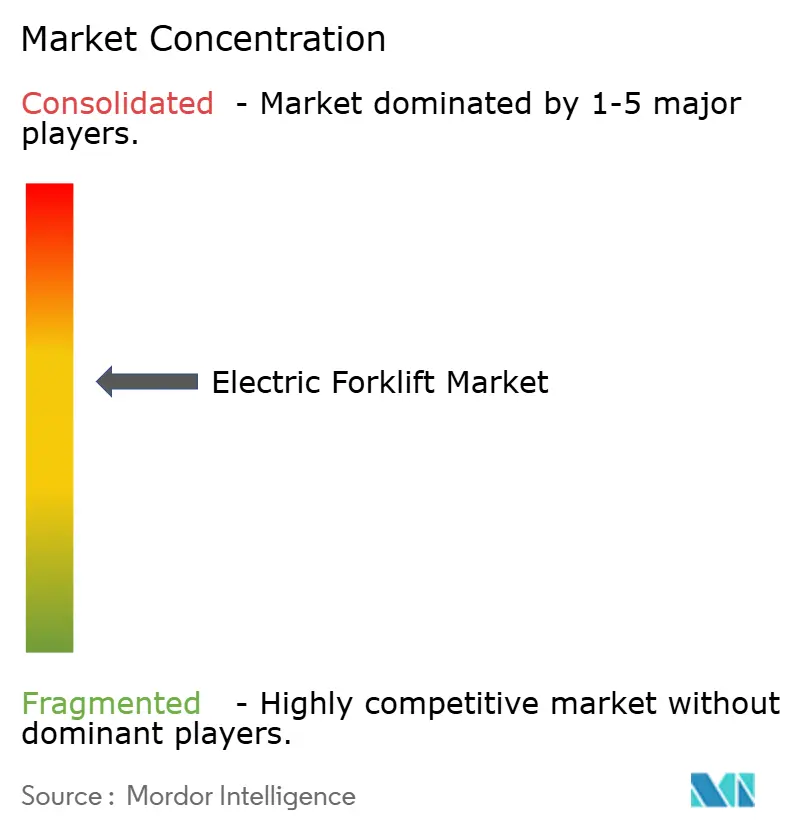

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Forklift Market Analysis by Mordor Intelligence

The electric forklift market stood at USD 49.98 billion in 2025 and is forecast to reach USD 64.15 billion by 2030, reflecting a 5.12% CAGR during the forecast period. Growth is propelled by zero-emission mandates, especially California’s Advanced Clean Fleets Rule, and sustained e-commerce expansion that demands 24/7, ventilation-free material-handling solutions. Fleet operators also respond to lithium-ion battery cost reductions, the rise of battery-as-a-service (BaaS) contracts, and AI-enabled maintenance platforms that sharpen total cost of ownership (TCO) advantages. Warehouse densification trends favor Class II narrow-aisle trucks, while solid-state battery road maps promise further performance gains after 2027. Moderate competitive intensity prevails as leading OEMs invest in dedicated electric manufacturing capacity and integrated charging ecosystems to lock in aftermarket service revenues.

Key Report Takeaways

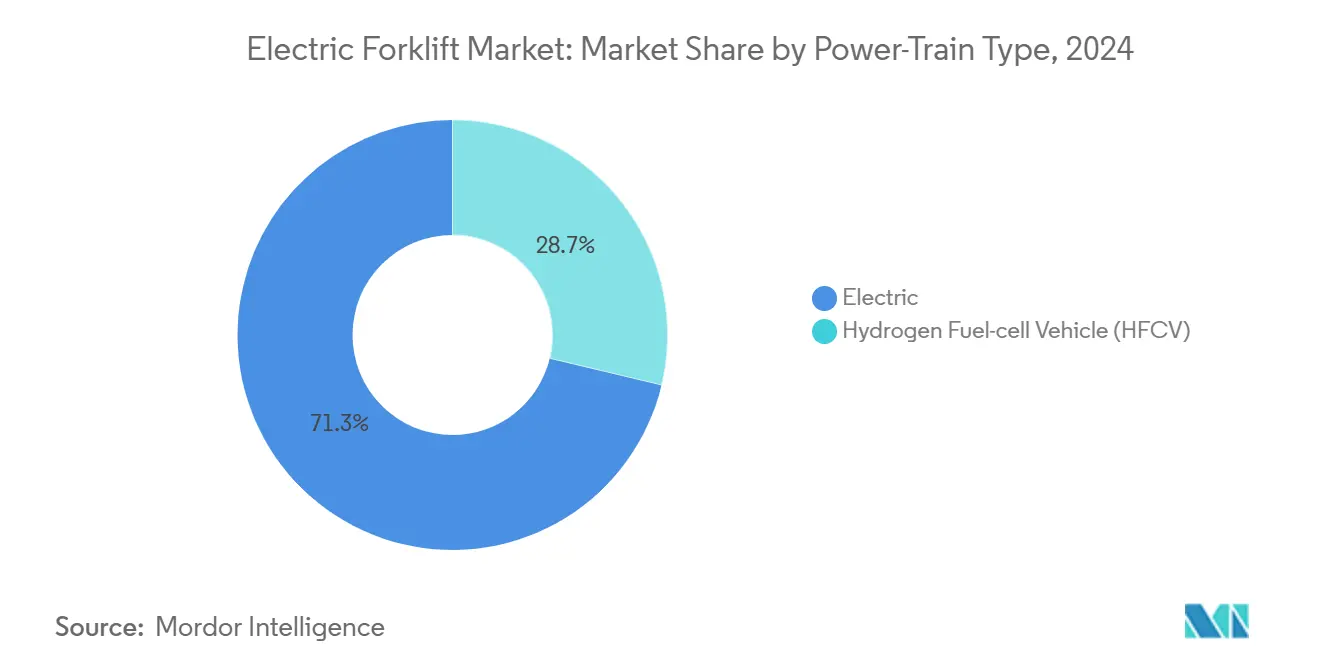

- By power-train, electric forklifts led with a 71.27% share of the electric forklift market in 2024 and are expanding at an 11.79% CAGR through 2030.

- By vehicle class, Class III pallet trucks held 40.31% share of the electric forklift market in 2024; Class II narrow-aisle trucks are projected to grow at a 9.28% CAGR to 2030.

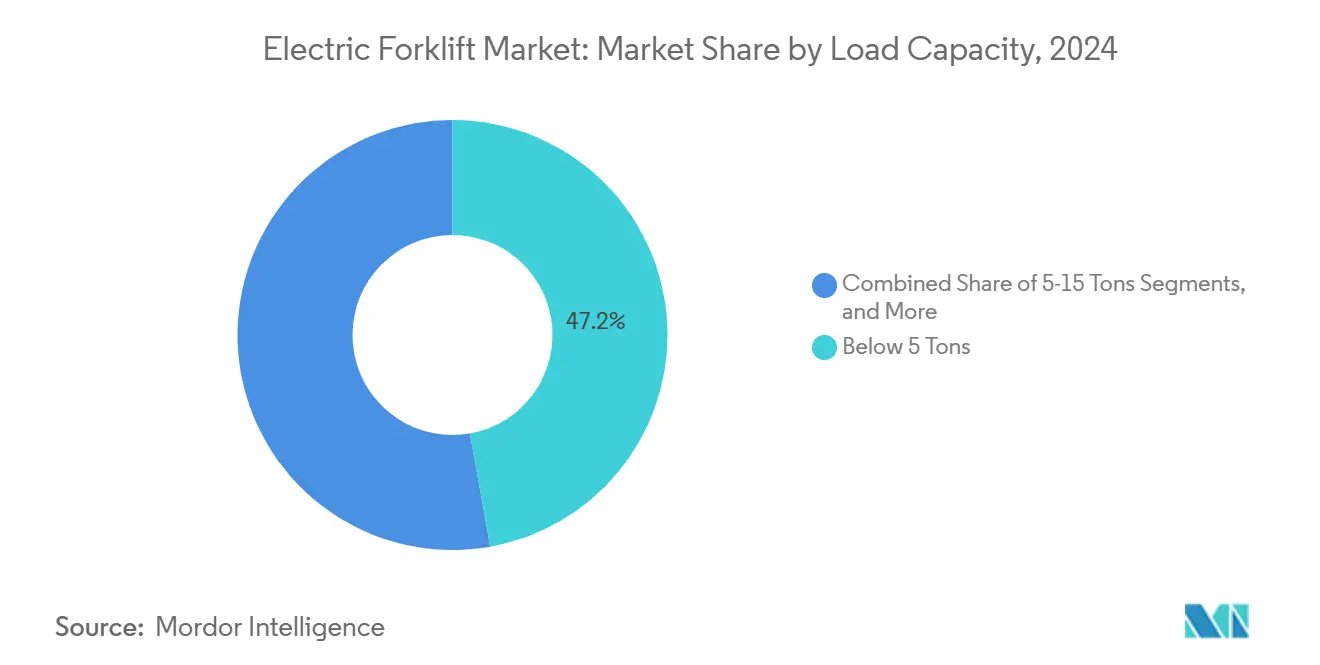

- By load capacity, units below 5 tons accounted for 47.19% share of the electric forklift market in 2024, while the 5-15 ton segment is advancing at a 10.21% CAGR through 2030.

- By end-user, logistics and warehousing commanded a 37.71% share of the electric forklift market in 2024, whereas food and beverage operations are rising at an 11.61% CAGR through 2030.

- By geography, Asia-Pacific dominated the electric forklift market, with a 43.29% share in 2024; South America is poised for the fastest regional CAGR of 10.72% up to 2030.

Global Electric Forklift Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Com Warehouse Boom | +1.8% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Zero-Emission MHE Mandates | +1.5% | North America and EU core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Falling Li-Ion Battery Costs | +1.2% | Global | Medium term (2-4 years) |

| OEM Battery-as-a-Service (BaaS) | +0.9% | North America and EU, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Solid-State Battery Roadmap (2027+) | +0.6% | Global, led by Japan & South Korea | Long term (≥ 4 years) |

| AI Predictive Maintenance for TCO | +0.4% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid E-commerce-Driven Warehouse Expansion

Narrow-aisle fulfillment centers now require 8-10 ft aisles rather than 12 ft, spurring demand for Class II trucks that boost storage density[1]“Narrow Aisle Forklifts and Warehouse Density,”, Leavitt Machinery, leavittmachinery.com. Electric drivetrains excel in enclosed spaces where ventilation is limited and precision control is critical. Automation readiness further tips the balance toward electric platforms because AGV systems rely on instantaneous torque and repeatable maneuverability. Operators confirm lithium-ion trucks sustain performance during peak holiday surges, avoiding the shift-change delays common with lead-acid battery swaps. E-commerce growth accelerates replacement cycles and expands total fleet counts, reinforcing the electric forklift market’s upward trajectory.

Mandates on Zero-Emission Material-Handling Equipment

California requires warehouses to deploy zero-emission forklifts in 2024, with permit restrictions and fines for non-compliance. Similar rules cascade into other United States regions and EU member nations under broader decarbonization policies. Euro 7 extends battery durability requirements to industrial vehicles, pushing fleets to adopt long-life lithium-ion platforms[2]“Euro 7 Proposal,”, European Commission, europa.eu. Occupational health agencies underscore diesel particulate risks, making electric adoption a workforce safety imperative[3]“Diesel Exhaust in Warehouses,”, U.S. Occupational Safety and Health Administration, osha.gov. As a result, many operators pull forward equipment turnover by 2-3 years, prioritizing compliance even when TCO parity is still emerging.

OEM Battery-as-a-Service (BaaS) Models

Battery ownership is shifting from fleet operators to OEMs through subscription-based contracts. These models integrate battery supply, charging infrastructure, maintenance, and end-of-life recycling into a monthly service. By eliminating the upfront cost barrier, they make advanced lithium-ion technology more accessible to smaller fleets. Providers leverage cloud-based analytics to proactively manage battery health and schedule replacements, ensuring high uptime and reducing operational disruptions. This approach enhances fleet reliability and streamlines cost management compared to traditional self-managed systems[4]"Battery-as-a-Service in Material Handling,", ABB Ltd., new.abb.com. The BaaS trend stabilizes residual values, encouraging secondary-market confidence in electric units.

AI-Enabled Predictive Maintenance Driving TCO Optimization

Advanced edge sensors continuously monitor motor, hydraulic, and battery systems, feeding real-time data into cloud platforms that forecast potential component failures well in advance. Early adopters of this technology are seeing significant improvements in operational efficiency, with reduced downtime and extended maintenance cycles. These benefits compound across high-utilization fleets, making electric equipment more cost-effective and strengthening fleet managers’ confidence in long-term electrification strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High EV Upfront Cost vs. ICE | -1.1% | Global, particularly acute in price-sensitive markets | Short term (≤ 2 years) |

| Lead-Acid Recycling Bottlenecks | -0.8% | Global, with concentration in developing markets | Medium term (2-4 years) |

| Hydrogen Refueling Infra Gaps (above1MW) | -0.6% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Grid Limits at Brownfield Sites | -0.5% | North America and EU, expanding to Asia-Pacific industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lead-Acid Battery Recycling Bottlenecks

Legacy lead-acid packs must be responsibly disposed of as fleets electrify, yet recycling capacity in several emerging markets lags behind replacement rates. Informal recycling channels pose environmental and safety hazards that increase regulatory scrutiny. Until collection networks scale, some operators delay lithium-ion adoption to avoid managing dual chemistries. Joint ventures between OEMs and metals refiners aim to close regional gaps, but permitting timelines and capital costs keep the constraint active through at least 2028.

Grid-Capacity Constraints at Brownfield Sites

Retrofitting existing warehouses for rapid charging often entails six-figure utility upgrades and 12-18-month interconnection delays[5]“Commercial Depot Electrification Barriers,”, California Energy Commission, energy.ca.gov. Peak-demand charges can erode electric TCO advantages unless smart chargers and behind-the-meter storage systems smooth load profiles. Department of Energy studies suggest flexible demand response could trim upgrade costs significantly, but require utility-operator collaboration and advanced microgrid control.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power-Train Type: Electric Dominance Accelerates

Electric configurations accounted for a 71.27% share of the electric forklift market in 2024 and are pacing an 11.79% CAGR through 2030, nearly double the overall electric forklift market growth. The electric forklift market share surge correlates with lithium-ion’s superior energy density, fast-charge capability, and reduced maintenance burden. Hydrogen fuel-cell units occupy a nascent niche in heavy-duty roles exceeding 15,000 lb, but infrastructure scarcity hinders immediate scale.

Continuous battery cost declines reinforce the electric forklift industry's shift away from lead-acid, while sodium-ion proof-of-concept trials indicate future diversification of chemistries. OEM platform commonality lets fleet operators switch chemistries without major chassis redesigns, protecting residual values and lowering transition risk. Collectively, these factors make electric power-trains the centerpiece of next-decade procurement strategies.

By Vehicle Class: Narrow-Aisle Solutions Drive Growth

Class III pallet trucks hold a 40.31% share of the electric forklift market in 2024, benefiting from high-turnover dock operations. Class II narrow-aisle trucks, however, exhibit a 9.28% CAGR through 2030, the fastest within the electric forklift market, as fulfillment centers pursue storage density gains. Class I rider units continue to serve general-purpose indoor-outdoor needs, adding pneumatic-tire options to tackle yard duties.

Rising real-estate costs are driving a shift toward space-optimized warehouse designs, where high-bay racking systems are paired with narrow-aisle trucks to maximize vertical storage. Warehouse architects embed advanced navigation technologies into building plans, such as guidance rails, laser positioning, and AGV compatibility. This approach positions Class II equipment as operational tools and core components of long-term infrastructure strategy, aligning facility design with future-ready automation.

By Load Capacity: Mid-Range Segment Accelerates

Units below 5 tons held a 47.19% slice of the electric forklift market size in 2024, addressing ubiquitous palletized freight moves. Demand for 5-15 ton models is expanding at a 10.21% CAGR as advances in AC motor torque and high-capacity lithium-ion packs close the performance gap versus diesel. BaaS contracts neutralize the higher battery cost in this segment, enabling multi-shift operation without capex spikes.

Manufacturers such as Crown Equipment now offer 7,000 lb electric pneumatics, proving viability for mixed indoor-outdoor sites. As the segment matures, residual-value data indicates parity with diesel after five years, further motivating the switch.

By End-User Industry: Food & Beverage Leads Growth

Logistics and warehousing dominated with a 37.71% share of the electric forklift market in 2024, mirroring global e-commerce proliferation. Food and beverage operations post the fastest 11.61% CAGR because lithium-ion retains more capacity even in −20 °C cold stores, cutting swap-room downtime. Automotive and electronics manufacturing maintain steady electric adoption for precision handling and emissions control.

Retail chains embrace whisper-quiet electric forklifts to extend restocking hours without disturbing shoppers, while construction firms trial mid-capacity models on indoor fit-outs where diesel exhaust is prohibited. Broadening use cases reinforces the technology’s versatility.

Geography Analysis

Asia-Pacific captured 43.29% share of the electric forklift market in 2024 and remains the anchor of the electric forklift market, supported by China’s integrated battery supply chain and India’s target of 100 million sq ft new warehousing by 2026. South America grows at a 10.72% CAGR during the forecast period, spurred by Brazilian manufacturing and Argentine agricultural export logistics.

North America ranks second, anchored by California’s zero-emission deadline and e-commerce fulfillment clusters requiring Class II fleets. Canadian cold-store deployments validate lithium-ion’s sub-zero resilience, and Mexico’s export-oriented plants specify electric forklifts to satisfy multinationals’ Scope 3 targets. Utility upgrade delays remain a hurdle, but federal incentives for commercial charging equipment are narrowing payback periods.

Europe’s decarbonization agenda ensures steady growth. Germany orders heavy-duty electric models for automotive logistics, France invests in cold-chain-optimized units, and the United Kingdom accelerates narrow-aisle adoption to meet net-zero corporate pledges. Scandinavian case studies display seamless electric integration even in −30 °C facilities, exemplifying best practices for the broader region.

Competitive Landscape

The electric forklift market remains moderately concentrated. Toyota Industries, KION Group, and Jungheinrich hold a sizable share by leveraging global manufacturing scale, BaaS platforms, and dealer service footprints. KION’s cloud telemetry suite delivers predictive analytics that lock in aftermarket parts revenue.

Mid-tier challengers such as BYD and EP Equipment deploy aggressive pricing backed by vertically integrated battery supply, widening access in price-sensitive Asia-Pacific markets. Crown and Raymond concentrate on segment niches—outdoor-capable pneumatics and high-reach warehouse trucks, respectively—to defend margins. Hydrogen specialists Plug Power and Hyster-Yale cultivate alliances with retailers running multi-shift fleets that justify onsite fueling investments.

Automotive cell manufacturers eye forklift packs as incremental volume, threatening to compress battery costs further and erode incumbent OEMs’ proprietary chemistry advantages. Consequently, the next strategic frontier revolves around software ecosystems that optimize fleet uptime, energy costs, and operator safety.

Electric Forklift Industry Leaders

-

Toyota Industries Corporation

-

KION Group AG

-

Jungheinrich AG

-

Crown Equipment Corporation

-

Hyster-Yale Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: STEF Group, a European leader in transport and logistics for temperature-controlled food products, launched two hydrogen projects in partnership with Toyota Material Handling Europe, a supplier of hydrogen fuel cell equipment, and Plug Power, a provider of comprehensive green hydrogen solutions.

- March 2025: Hangcha Group launched its newest electric forklifts and warehouse equipment, introducing a cutting-edge intelligent logistics ecosystem. This move directly addresses Europe's pressing need for sustainable heavy-duty operations and the push for scalable automation.

Global Electric Forklift Market Report Scope

| Electric | Lead-acid |

| Li-ion | |

| Hydrogen Fuel-cell Vehicle (HFCV) |

| Class I (Electric Rider Trucks) |

| Class II (Electric Narrow-Aisle) |

| Class III (Electric Pallet) |

| Below 5 Tons |

| 5 - 15 Tons |

| Above 15 Tons |

| Manufacturing |

| Logistics and Warehousing |

| Construction and Infrastructure |

| Retail and Wholesale |

| Food and Beverage Cold-Chain |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Power-train Type | Electric | Lead-acid |

| Li-ion | ||

| Hydrogen Fuel-cell Vehicle (HFCV) | ||

| By Vehicle Class | Class I (Electric Rider Trucks) | |

| Class II (Electric Narrow-Aisle) | ||

| Class III (Electric Pallet) | ||

| By Load Capacity | Below 5 Tons | |

| 5 - 15 Tons | ||

| Above 15 Tons | ||

| By End-user Industry | Manufacturing | |

| Logistics and Warehousing | ||

| Construction and Infrastructure | ||

| Retail and Wholesale | ||

| Food and Beverage Cold-Chain | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the electric forklift market and its projected growth?

The market stands at USD 49.98 billion in 2025 and is forecast to reach USD 64.15 billion by 2030, translating to a 5.12% CAGR.

Which power-train type is expanding fastest within electric forklifts?

Pure electric platforms, especially lithium-ion configurations, are advancing at an 11.79% CAGR, outpacing hydrogen fuel-cell alternatives.

Why are Class II narrow-aisle trucks gaining popularity?

Fulfillment centers favor narrow 8-10 ft aisles that boost storage density, making Class II trucks the optimal choice for space-constrained, high-throughput operations.

How does battery-as-a-service improve fleet economics?

BaaS shifts battery costs from capital to operating budgets, guarantees uptime, and can cut total fleet operating expenses by 15-20%.

What key constraint could slow electric forklift adoption in brown-field sites?

Limited grid capacity often necessitates costly utility upgrades and long interconnection timelines, delaying fast-charging infrastructure deployment.

Page last updated on: