Autonomous Forklift Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.21 Billion |

| Market Size (2031) | USD 5.72 Billion |

| Growth Rate (2026 - 2031) | 12.23% CAGR |

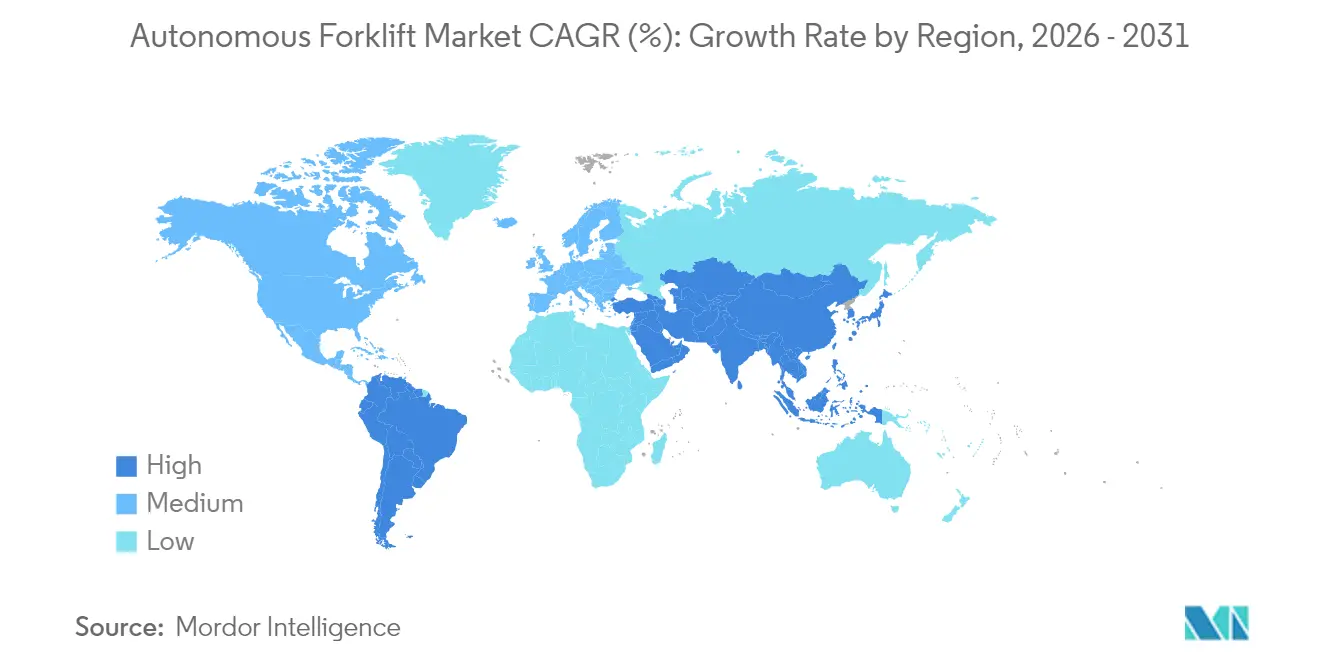

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

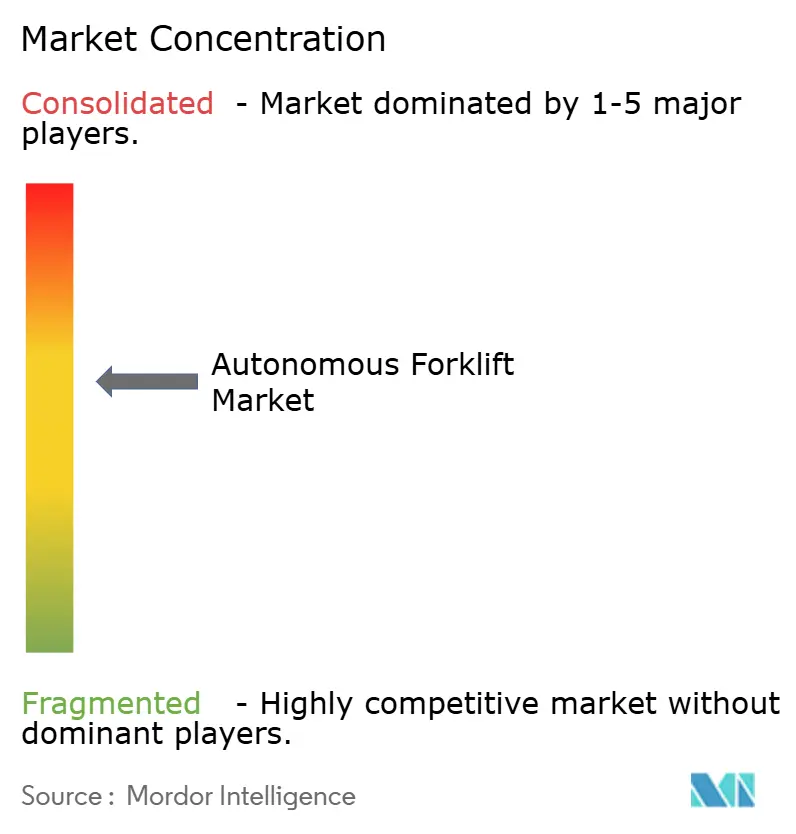

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Forklift Market Analysis by Mordor Intelligence

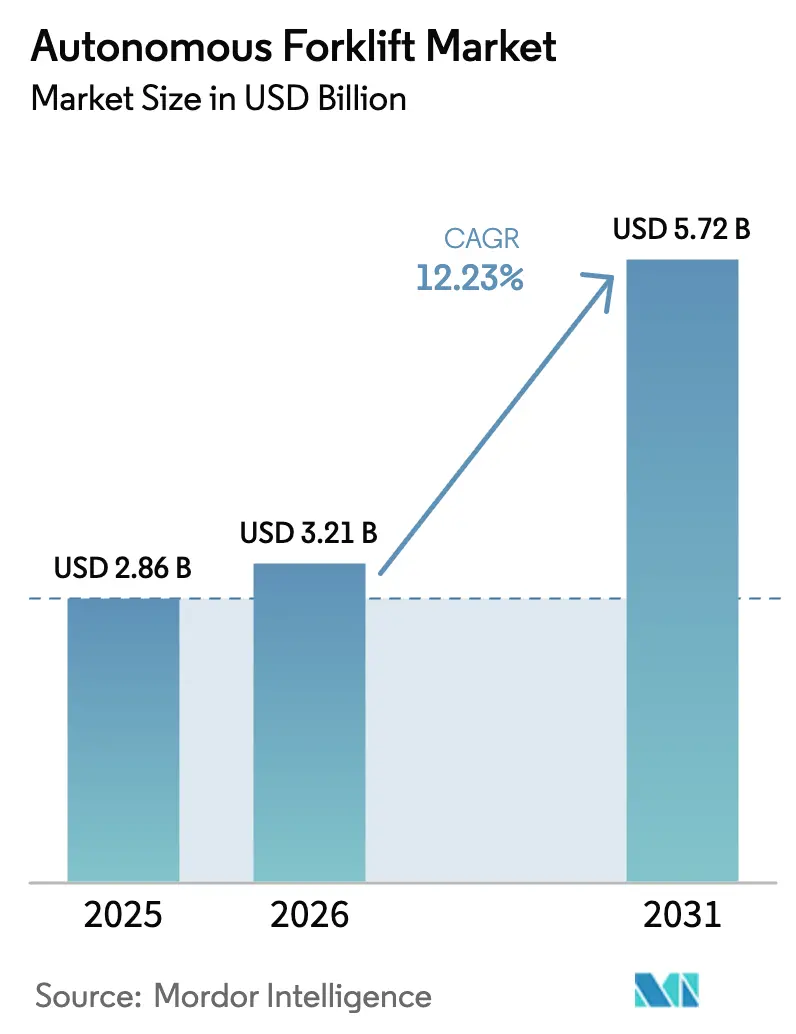

The Autonomous Forklift Market size was valued at USD 2.86 billion in 2025 and estimated to grow from USD 3.21 billion in 2026 to reach USD 5.72 billion by 2031, at a CAGR of 12.23% during the forecast period (2026-2031).

Strong growth reflects tightening labor availability, rapid e-commerce fulfillment needs, and steady improvements in navigation, sensing, and fleet-coordination software. Electric powertrains dominate shipments as corporations pursue decarbonization commitments, while emerging private 5G networks enable real-time fleet optimization across large campuses. Rising capital-expenditure tax incentives in North America and Europe shorten payback periods, and documented productivity gains ranging from 25% to 100% continue to validate the automation business case. Asia-Pacific remains the demand anchor thanks to cold-chain modernization programs and acute driver shortages, whereas South America leads growth on the back of logistics infrastructure upgrades and favourable macroeconomic reforms.

Key Report Takeaways

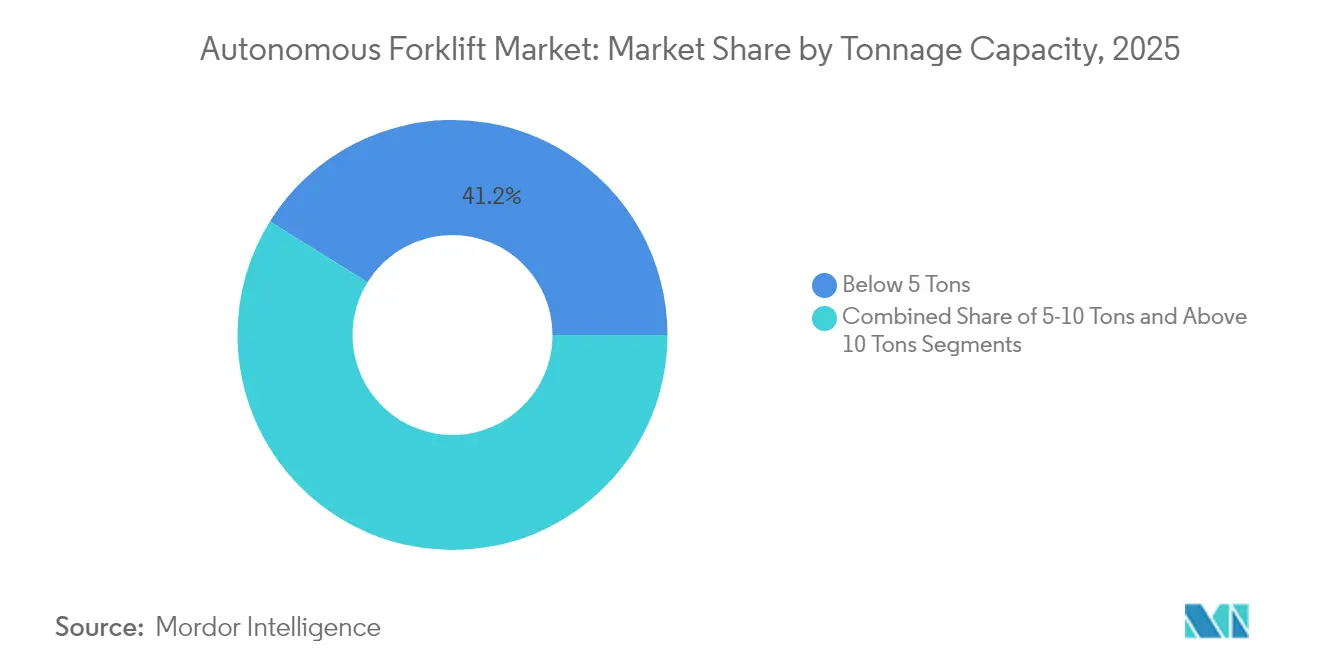

- By tonnage capacity, the 5 tons segment commanded 41.15% market share in 2025, while the above 10 tons segment exhibits the fastest growth at 18.10% CAGR through 2031.

- By navigation technology, laser guidance retained 38.10% share of the autonomous forklift market size in 2025, with SLAM/hybrid systems advancing at a 20.94% CAGR between 2026–2031.

- By application, logistics and warehousing commanded 49.05% of the autonomous forklift market share in 2025; cold-storage handling is forecast to post a 18.92% CAGR through 2031.

- By propulsion type, electric systems held 71.40% of the autonomous forklift market size in 2025, while hydrogen fuel cells are projected to grow at a 23.65% CAGR to 2031.

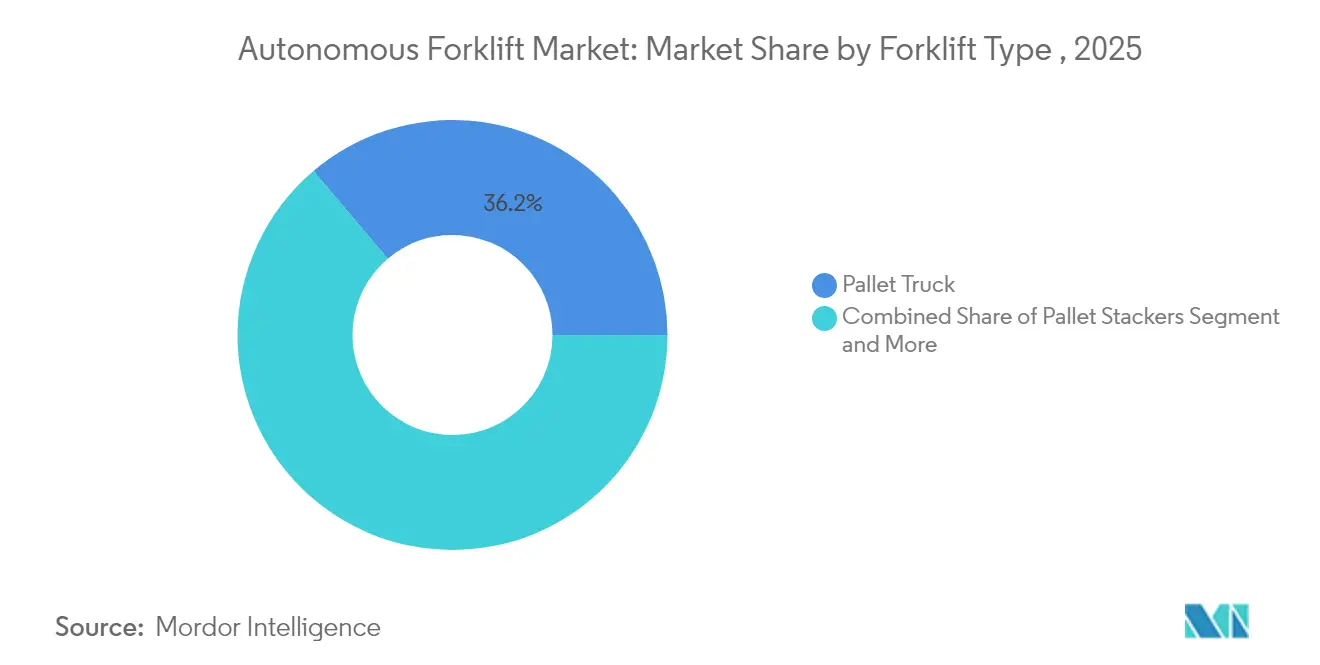

- By forklift type, pallet trucks held 36.20% of the autonomous forklift market share in 2025; very-narrow-aisle trucks are projected to expand at a 21.80% CAGR through 2031.

- By end-user industry, retail and e-commerce led 32.30% of the autonomous forklift market share in 2025, while pharmaceuticals is the fastest-growing segment at a 17.35% CAGR.

- By geography, Asia-Pacific led with 45.40% of the autonomous forklift market share in 2025; South America is expected to register the fastest 15.50% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Autonomous Forklift Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor Shortages and Rising Warehouse Wages | +3.2% | Global, acute in North America and Japan | Short term (≤ 2 years) |

| E-Commerce Fulfillment Boom | +2.8% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Cap-Ex Tax Incentives Accelerating ROI | +2.1% | North America and Europe | Short term (≤ 2 years) |

| Advancements In Lidar / SLAM Sensors | +1.9% | Global | Medium term (2-4 years) |

| Corporate ESG Push Toward Electric Fleets | +1.6% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Private 5G-Enabled Fleet Coordination | +0.9% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor shortages and rising warehouse wages

Warehouse operator turnover reaching 400% in some distribution centers alters material-handling economics, positioning autonomous forklifts as a primary continuity tool. Japan’s truck-driver overtime cap intensifies demand despite premiums exceeding USD 100,000 per unit, and certified operator wages keep escalating. Facilities running multiple shifts realize yearly labor savings of USD 50,000 – 100,000 per vehicle, compressing return-on-investment cycles in regions with aging workforces and restrictive immigration.

E-commerce fulfillment boom

Online order volumes keep outpacing labor capacity, and autonomous forklifts provide scalable throughput without proportional head-count growth. A leading global retailer is investing USD 200 million to roll out autonomous fleets across its distribution network, signaling confidence in the technology’s readiness. Smaller urban fulfillment nodes further lift demand for compact autonomous models that maneuver in space-constrained facilities while sustaining same-day delivery promises.

Cap-ex tax incentives accelerating ROI

Accelerated depreciation schedules and targeted automation credits in the United States and European Union help operators recover as much as 50% of upfront spending, trimming payback periods to under two years. Local development agencies add grants that tie automation to high-skill job creation, and finance providers are rolling out Robot-as-a-Service contracts that shift investments from capital budgets to operating expenses.

Advancements in LiDAR / SLAM sensors

SLAM systems eliminate fixed-infrastructure needs, expanding addressable markets beyond greenfield megasites. Collaborative projects between forklift OEMs and semiconductor leaders are merging AI perception with digital twins, enabling vehicles to self-optimize routes and operate safely beside human crews. Lower sensor prices, driven by automotive volumes, bring advanced navigation to mid-size enterprises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Purchase and Integration Cost | -2.4% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Safety Certification and Liability Concerns | -1.8% | Global, stringent in North America and Europe | Medium term (2-4 years) |

| Fragmented Fleet-Management Software | -1.1% | Global | Medium term (2-4 years) |

| Scarcity Of Outdoor-Yard Simulation Data | -0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High initial purchase and integration cost

Many businesses, especially smaller and medium-sized enterprises (SMEs), face significant hurdles in the forklift industry due to the steep initial purchase and integration costs of advanced technologies. Electric and automated forklifts, while promising long-term savings and environmental perks, come with a hefty price tag that can deter some businesses. For instance, autonomous forklifts can be priced 70%–400% higher than their conventional counterparts. Moreover, integrating these advanced models often necessitates upgrades to wireless infrastructure and the establishment of dedicated charging or hydrogen refueling stations. Even with emerging subscription models aimed at easing entry, the annual maintenance for advanced sensors and software can still hit USD 15,000 per truck, posing a challenge for smaller operators.

Safety certification and liability concerns

Regulatory clarity around ISO 3691-4 and evolving regional rules remains limited. Insurers demand new risk-assessment frameworks, increasing premiums until consistent safety records are demonstrated. California’s zero-emission forklift mandate, effective in 2026, adds another compliance layer but simultaneously accelerates electrification demand[1]California Air Resources Board, “Emission Forklifts,” ww2.arb.ca.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tonnage Capacity: Heavy-duty automation accelerates

Units below 5 tons held 41.15% market share in 2025, primarily serving e-commerce and pharmaceutical jobs that reward maneuverability. Conversely, forklifts above 10 tons exhibit an 18.10% CAGR, addressing heavy manufacturing and construction needs where safety and labor issues are pronounced. The mid-range 5-10 tons class benefits from optimal cost-performance balances that attract mid-market adopters. Komatsu’s work on sodium-ion batteries underscores how energy innovations unlock continuous heavy-duty duty cycles.

Komatsu's development of sodium-ion battery systems for heavy-duty electric forklifts demonstrates how technological advances are enabling autonomous operation in previously challenging applications. The tonnage capacity segmentation reflects broader industry trends toward specialization, with manufacturers developing purpose-built autonomous systems rather than retrofitting existing designs.

By Navigation Technology: SLAM revolution transforms deployment

Laser guidance controlled 38.10% of the autonomous forklift market size in 2025, thanks to high precision on fixed routes, yet SLAM/hybrid navigation is scaling at a 20.94% CAGR as it avoids costly infrastructure changes. Vision-guided systems cater to high-resolution identification tasks, and magnetic or inductive tracks stay relevant for predictable high-volume lanes.

Further, fleet-level coordination through private 5G and declining sensor costs make SLAM viable for brownfield upgrades, solidifying the technology’s leadership outlook.

By Application: Cold-storage drives specialized growth

Logistics and warehousing accounted for 49.05% of the autonomous forklift market share in 2025, reflecting early automation traction. Cold-storage handling, running at a 18.92% CAGR, benefits from a regulatory push for pharmaceutical temperature compliance and the health-safety upside of reduced human exposure.

Dematic's third-generation freezer-rated AGVs operating at temperatures as low as -25°C demonstrate how specialized autonomous systems are enabling automation in previously challenging environments, with 360° scanning systems and emergency safety features addressing the unique risks of cold-storage operations.

By Propulsion Type: Hydrogen fuel cells gain momentum

Electric powertrains dominated 71.40% of the autonomous forklift market size in 2025. Hydrogen fuel cells, however, post a 23.65% CAGR because rapid refueling circumvents battery-charging downtime, particularly attractive for multi-shift operations.

The U.S. Department of Energy’s data shows 700+ fuel-cell forklifts in service and explains how regional zero-emission mandates accelerate the shift from LPG and diesel to battery and hydrogen solutions. In addition, California's zero-emission forklift regulation requiring the phase-out of large spark-ignition engines starting in 2026 exemplifies how regulatory mandates are reshaping propulsion technology adoption.

By Forklift Type: VNA trucks lead specialized automation

Pallet trucks held a 36.20% share in 2025, aligned with high-volume horizontal movement. Very-narrow-aisle trucks, advancing at 21.80% CAGR, suit dense storage strategies that rely on high-reach precision, while counter-balanced and reach models continue to address heavier lift or racking applications.

Toyota Material Handling's launch of 22 new electric models, including 12 reach truck variants designed for modern warehousing challenges, demonstrates how manufacturers are developing autonomous-ready platforms that integrate navigation systems and safety features from initial design rather than retrofit approaches.

By End-User Industry: Pharmaceuticals drive premium adoption

Retail and e-commerce controlled a 32.30% share in 2025 on fulfillment-volume growth. Pharmaceuticals, growing at 17.35% CAGR, draw on strict traceability demands and hygiene rules that favor consistent robotic handling. The Australian healthcare sector's adoption of driverless forklifts demonstrates how hospitals and life-science distributors deploy autonomous fleets for regulatory documentation and 24/7 uptime, with 3PLs investing to ensure compliance across diverse client inventories.

Geography Analysis

Asia-Pacific led the autonomous forklift market with 45.40% share in 2025, powered by Chinese logistics modernization, Japanese driver shortages, and South Korean fuel-cell incentives. Local manufacturers are rolling out freezer-capable forklifts that perform at minus 30 °C, and new overtime limits in Japan further raise automation urgency. India’s expanding manufacturing base gains from recent domestic automation plant openings, ensuring localized supply for growing warehouse networks.

North America grows at a 12.15% CAGR to 2031. A recent USD 200 million investment by a key market player validates large-scale rollouts, and favorable U.S. tax policy improves capital economics. California’s pending 2026 zero-emission forklift deadline intensifies electric-fleet purchases while boosting demand for integrated safety and telematics systems.

Europe advances at an 10.95% CAGR, with Germany pioneering cooperative outdoor fleets over private 5 G. The European Union’s sustainability targets align with electrification, and strict safety standards drive the adoption of perception-rich systems. South America is the fastest-growing region, expanding at 15.50% CAGR. The region benefits from logistics upgrades across Brazil and Argentina, although deployment data remain limited given nascent automation ecosystems.

Competitive Landscape

The market is moderately concentrated. Robotics specialists like Fox Robotics and Third Wave Automation increasingly partner with heavyweights to embed AI autonomy into established dealer networks. Toyota’s growth fund recently injected USD 27 million into Third Wave Automation, highlighting the convergence of legacy OEM scale and global startup software expertise[2]Toyota Motor Corporation, “Toyota Group to Accelerate Collaboration Towards Transforming into a Mobility Company Through Privatization of Toyota Industries Corporation,” global.toyota. Meanwhile, KION is co-developing weather-resistant autonomous trucks for outdoor yards, targeting white-space applications underserved by indoor-only vehicles.

Fleet-management software is emerging as the new battleground, with vendor-agnostic platforms reducing lock-in risks and shifting competitive advantage from mechanical engineering to data analytics. Strategic acquisitions and joint ventures dominate headline activity, signaling recognition that hardware alone no longer assures leadership.

Autonomous Forklift Industry Leaders

Toyota Industries Corporation

Jungheinrich AG

Hyster-Yale Group, Inc.

Mitsubishi Logisnext Co. Ltd

KION Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Toyota Motor Corporation confirmed a plan to privatize Toyota Industries Corporation to strengthen autonomous forklift technology under a unified mobility strategy.

- October 2024: Third Wave Automation closed a USD 27 million Series C round led by Toyota’s Woven Capital to scale autonomous reach-truck production.

- July 2024: Walmart pledged USD 200 million to deploy autonomous forklifts across its U.S. distribution centers, one of the retail sector’s largest single commitments.

Global Autonomous Forklift Market Report Scope

An autonomous forklift is a type of automated guided vehicle (AGV) that can carry loads along the floor of a facility without a driver onboard. The scope of the report considers pallet trucks/movers/jacks, pallet stackers, and forked automated guided vehicles, which are autonomously operated without manual intervention.

The autonomous forklift market is segmented by tonnage capacity, navigation technology, application, propulsion type, type, and geography. By tonnage capacity, the market is segmented into below 5 tons, 5-10 tons, and above 10 tons. By navigation technology, the market is segmented into laser guidance, vision guidance, optical tape guidance, magnetic guidance, inductive guidance, and others (simultaneous localization and mapping, etc.). By application, the market is segmented into logistics and warehousing, manufacturing, material handling, and others (retail, etc.). By propulsion type, the market is segmented into electric, diesel, and others (LPG, CNG, etc.). By type, the market is segmented into pallet trucks/movers/jacks, pallet stackers, and others (forked AGV, etc.). By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

The report offers market size and forecasts for autonomous forklifts in value (USD) for all the above segments.

| Below 5 Tons |

| 5-10 Tons |

| Above 10 Tons |

| Laser Guidance |

| Vision Guidance |

| Optical Tape Guidance |

| Magnetic Guidance |

| Inductive Guidance |

| SLAM / Hybrid |

| Logistics and Warehousing |

| Manufacturing |

| Retail and E-commerce DCs |

| Cold-Storage Handling |

| Construction Materials |

| Others |

| Electric (Li-ion / Lead-acid) |

| Diesel |

| LPG / CNG |

| Hydrogen Fuel Cell |

| Pallet Truck / Mover / Jack |

| Pallet Stackers |

| Counter-balanced Truck |

| Very-Narrow-Aisle (VNA) Truck |

| Reach / Straddle / Forked AGV |

| Others |

| Retail and E-commerce |

| Automotive |

| Food and Beverage |

| Pharmaceuticals |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Tonnage Capacity | Below 5 Tons | |

| 5-10 Tons | ||

| Above 10 Tons | ||

| By Navigation Technology | Laser Guidance | |

| Vision Guidance | ||

| Optical Tape Guidance | ||

| Magnetic Guidance | ||

| Inductive Guidance | ||

| SLAM / Hybrid | ||

| By Application | Logistics and Warehousing | |

| Manufacturing | ||

| Retail and E-commerce DCs | ||

| Cold-Storage Handling | ||

| Construction Materials | ||

| Others | ||

| By Propulsion Type | Electric (Li-ion / Lead-acid) | |

| Diesel | ||

| LPG / CNG | ||

| Hydrogen Fuel Cell | ||

| By Forklift Type | Pallet Truck / Mover / Jack | |

| Pallet Stackers | ||

| Counter-balanced Truck | ||

| Very-Narrow-Aisle (VNA) Truck | ||

| Reach / Straddle / Forked AGV | ||

| Others | ||

| By End-User Industry | Retail and E-commerce | |

| Automotive | ||

| Food and Beverage | ||

| Pharmaceuticals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the autonomous forklift market?

The global autonomous forklift market stands at USD 3.21 billion in 2026 with a forecast to reach USD 5.72 billion by 2031 at a 12.23% CAGR.

Which region holds the largest share of autonomous forklift deployments?

Asia-Pacific leads with 45.40% of global revenue, driven by Chinese logistics build-out and Japanese labor shortages.

Which application segment is growing the fastest?

Cold-storage handling is expanding at a 18.92% CAGR due to rising pharmaceutical and food-safety requirements.

Why are hydrogen fuel cell forklifts gaining attention?

Hydrogen models can refuel in minutes, making them attractive for multi-shift operations and supporting a 23.65% CAGR through 2031.

What are the main barriers to wider adoption?

High upfront costs and evolving safety certification frameworks remain the principal obstacles, particularly for small and medium enterprises.

Page last updated on: