Indonesia Forklift Rental Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

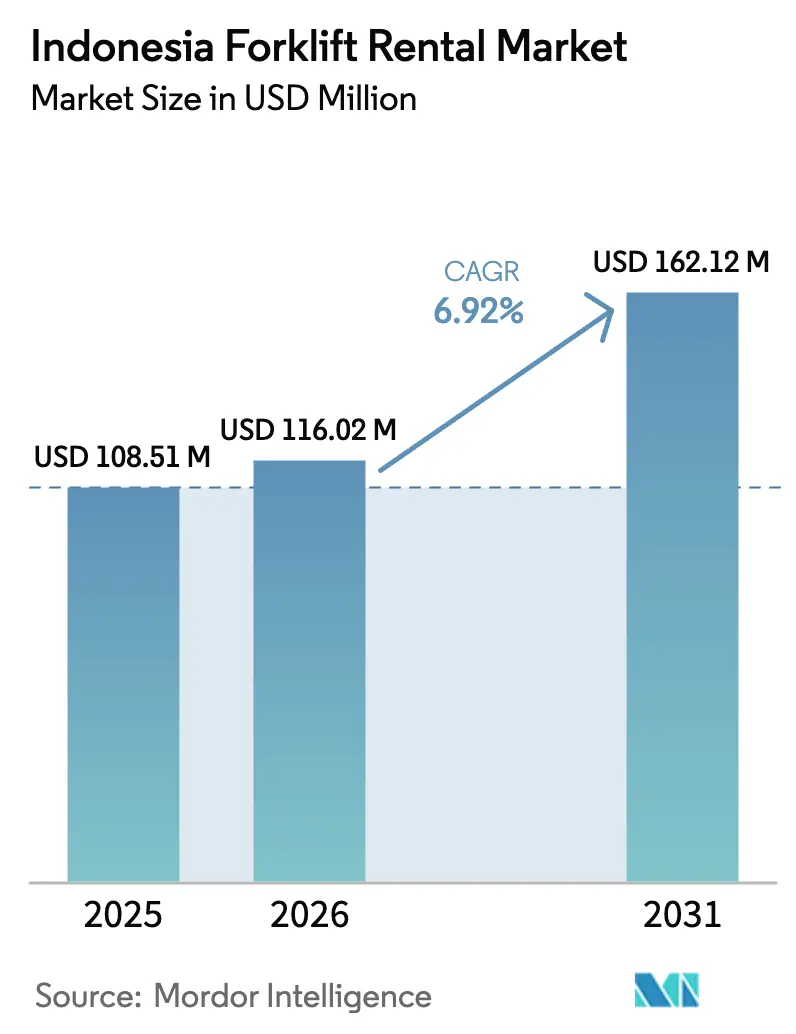

| Base Year Market Size (2025) | USD 108.51 Million |

| Market Size (2026) | USD 116.02 Million |

| Market Size (2031) | USD 162.12 Million |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

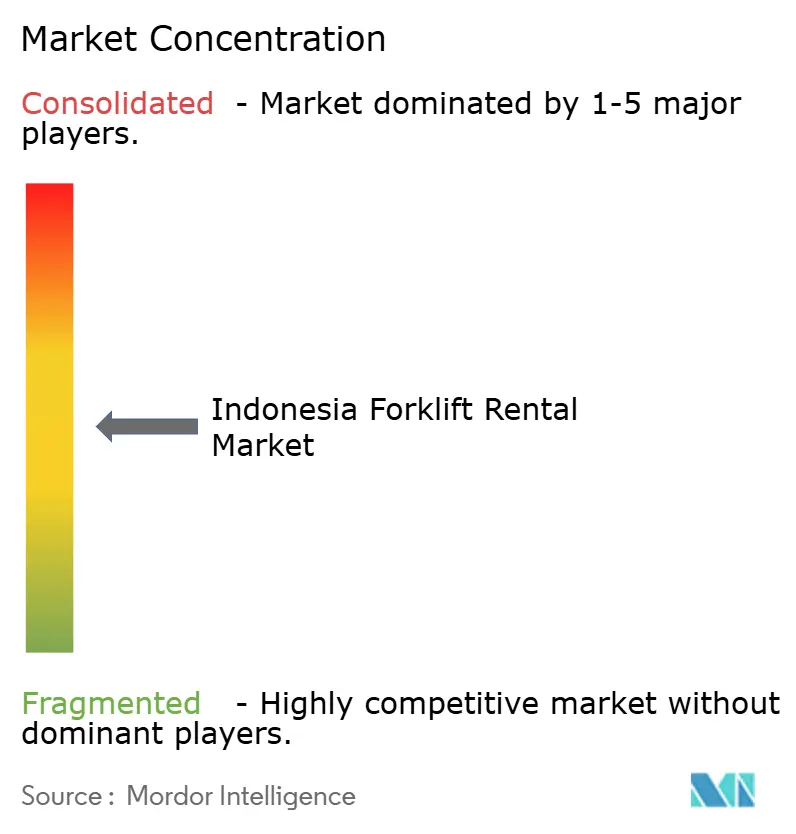

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia Forklift Rental Market Analysis by Mordor Intelligence

The Indonesia forklift rental market size is expected to grow from USD 108.51 million in 2025 to USD 116.02 million in 2026 and is forecast to reach USD 162.12 million by 2031 at 6.92% CAGR over 2026-2031. The surge aligns with national infrastructure spending under the Proyek Strategis Nasional, the logistics sector’s shift toward outsourced warehousing, and accelerating adoption of electric and telematics-enabled fleets. Government expenditure on roads, ports, and the new capital city directly enlarges the customer base for short-cycle equipment leasing while the services sector’s growing 60% share of value added lifts structural demand. Technology diffusion, notably IoT and lithium-ion battery systems, is altering competitive dynamics in favor of professionally managed rental fleets able to integrate safety compliance and performance analytics into customer contracts. At the same time, currency volatility and patchy after-sales coverage in outer islands add cost pressure that only operators with scale or regional partnerships can absorb.

Key Report Takeaways

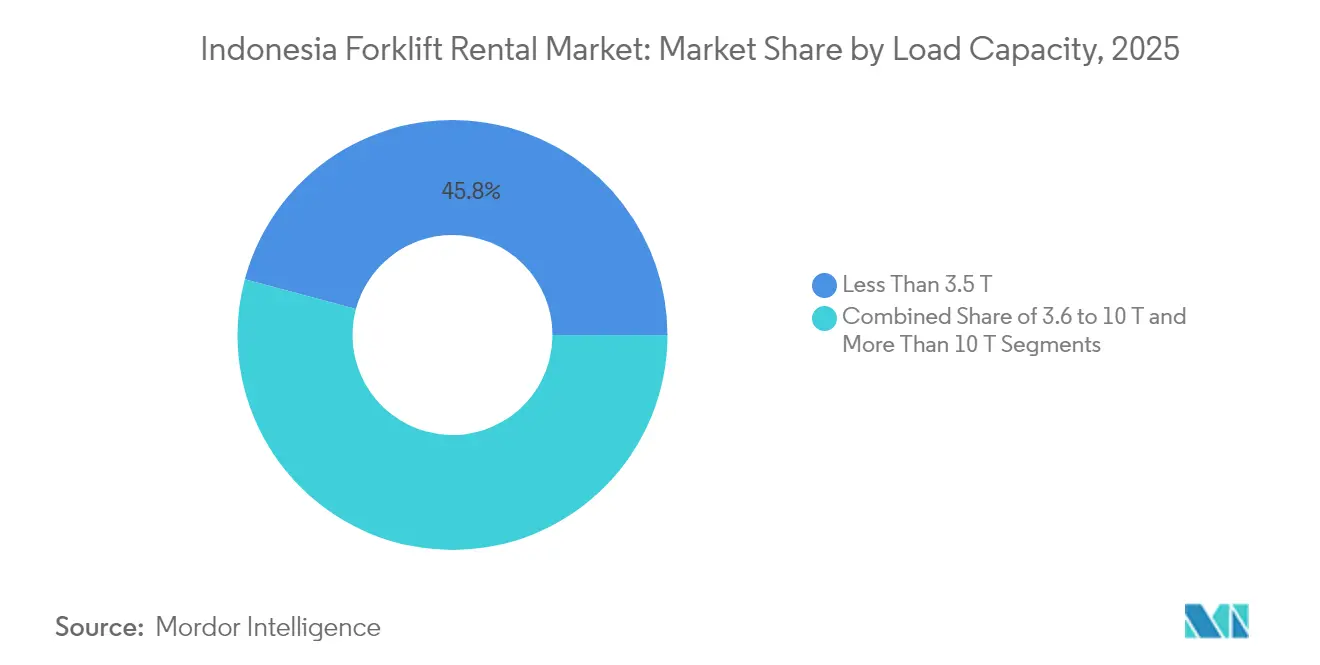

- By load capacity, units below 3.5 tons held 45.83% of the Indonesia forklift rental market share in 2025 and are expanding at a 9.31% CAGR to 2031.

- By rental duration, short-term contracts led with a 53.62% share in 2025, while mid-term deals are growing fastest at an 10.56% CAGR through 2031.

- By power source, internal combustion engines commanded a 61.35% share in 2025, whereas electric models are advancing at a 15.08% CAGR.

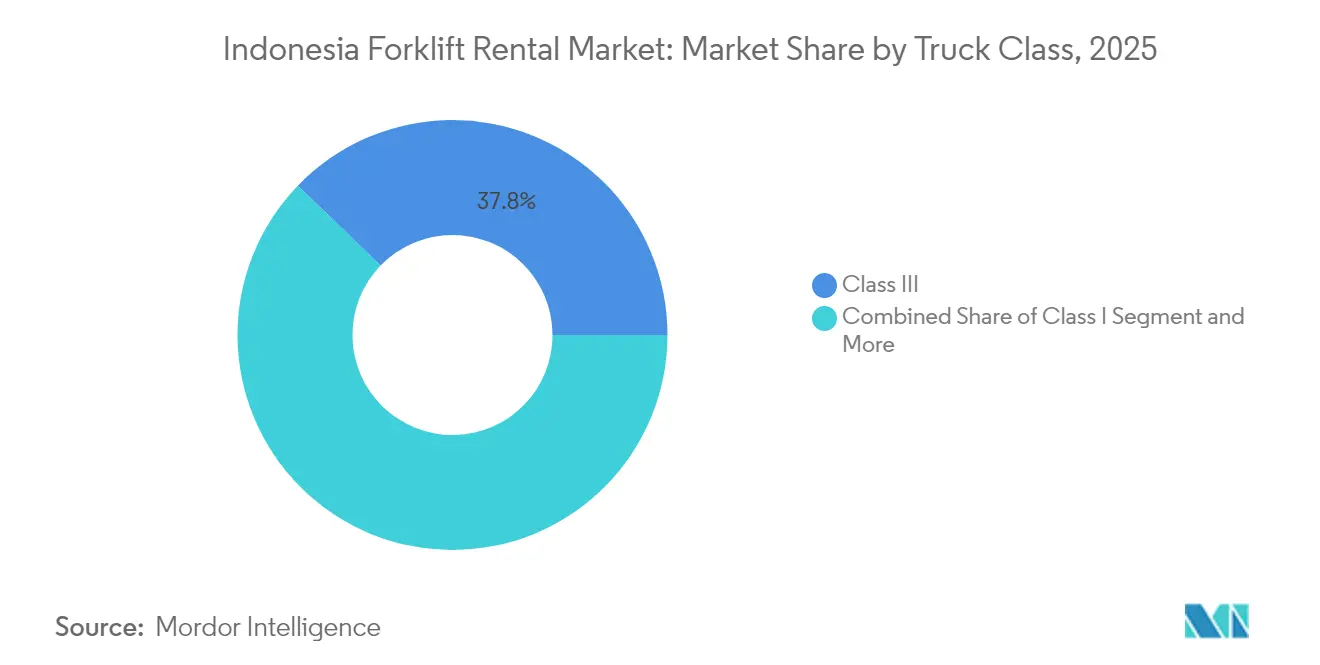

- By truck class, Class III equipment accounted for 37.78% of the Indonesia forklift rental market size in 2025, yet Class I units are projected to grow at a 12.74% CAGR.

- By end-use industry, warehousing and logistics captured a 50.37% share in 2025 and showed the strongest trajectory, with a 12.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia contributes to a system defined not by any single country or region but by the interaction of many. The global forklift rental market data by Mordor Intelligence represents that combined structure.

Indonesia Forklift Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 3PL Outsourcing & E-Commerce Warehousing Expand | +2.1% | Java core, expanding to Sumatra and Kalimantan | Medium term (2–4 years) |

| Govt. Infrastructure Push Fuels Construction Equipment Leasing | +1.8% | National, concentrated in PSN project locations | Long term (≥ 4 years) |

| Electric Forklifts Surge to Align with PLN Green-Power Incentives | +1.4% | Java and Bali, pilot programs in major cities | Medium term (2–4 years) |

| Pelindo's Port Automation Boosts Container-Handling Rentals | +0.9% | Major ports: Jakarta, Surabaya, Medan, Makassar | Short term (≤ 2 years) |

| ISO 45001 Compliance Elevates Demand for Professional Rental Fleets | +0.7% | Industrial zones in Java, expanding to mining regions | Medium term (2–4 years) |

| "Pay-Per-Use" Telematics-Enabled Rental Contracts on the Rise | +0.5% | Urban centers with strong digital infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in 3PL Outsourcing and E-Commerce Warehousing Expansion

Indonesia's logistics sector contributes over 50% of total forklift demand, with transportation and distribution services becoming increasingly critical for supply chain efficiency[1]Noverius Laoli, "Logistics Sector Grows Rapidly, Indonesia's Forklift Industry Ready to Transform," industri.kontan.co.id.. The services sector's dominance at nearly 60% of total value added creates a multiplier effect where each percentage point of logistics growth generates disproportionate equipment rental demand. E-commerce warehousing expansion particularly favors short-term and mid-term rental models, as operators require flexible capacity scaling without capital commitment. The shift toward outsourced logistics operations reduces direct equipment ownership among manufacturers and retailers, channeling demand toward professional rental fleets that offer maintenance, compliance, and operational expertise. This trend accelerates in outer islands where establishing in-house material handling capabilities proves economically unviable for smaller operators.

Government Infrastructure Push Driving Construction Equipment Leasing

The PSN program's completion of 153 projects worth IDR 1,040 trillion generated IDR 1,993 trillion in economic output, creating sustained demand for construction equipment rentals across multiple project phases[2]Titik Anas, "Massive Infrastructure Development and Its Impact on Indonesia’s Economy," eria.org.. Infrastructure investment's contribution to GDP enhancement establishes a feedback loop where improved connectivity reduces logistics costs, making rental services more economically attractive than ownership for project-based operations. The government's USD 430 billion infrastructure commitment through 2024 includes toll road expansion and airport development, requiring intensive material handling during construction and operational phases. The construction sector grows at 4.83% annually, with the industry contributing 9.86% to GDP in 2023, establishing a stable foundation for equipment rental demand[3]"Indonesia’s construction sector remains sturdy," Business Indonesia, business-indonesia.org.. The IKN Nusantara project's USD 35 billion scale represents a singular demand catalyst requiring coordinated equipment deployment across multiple construction phases spanning several years.

Rapid Shift Toward Electric Forklifts to Meet PLN Green-Power Incentives

Electric forklift demand surged over 30% in 2024, driven by lithium-ion battery technology adoption projected to dominate the market by 2030. PLN's green energy initiatives create cost advantages for electric equipment operations, particularly in industrial zones with access to renewable energy infrastructure. Japanese companies' contributions to Indonesia's decarbonization efforts include onsite solar power generation equipment rental services, reducing operational costs for electric forklift fleets. The transition favors rental models over ownership because electric forklifts require specialized charging infrastructure and maintenance expertise that rental companies can provide more efficiently than individual operators. Battery technology evolution creates obsolescence risks that rental agreements can mitigate through regular fleet updates and technology refresh cycles.

Port Automation Programs (Pelindo) Boosting Container-Handling Rentals

Tanjung Priok Port's handling of approximately 50% of Indonesia's cargo volume positions PELINDO's automation initiatives as a critical demand driver for specialized container-handling equipment. Port digitalization and efficiency improvements require coordinated equipment deployment that favors rental arrangements over individual ownership due to operational complexity and maintenance requirements. PELINDO's formation through merging four state-owned companies creates standardization opportunities that benefit large-scale rental providers capable of meeting unified specifications across multiple port locations. Container volume growth at major ports including Jakarta, Surabaya, Medan, and Makassar generates sustained demand for Class IV and Class V forklifts specifically designed for container handling operations. The automation programs' focus on reducing operational costs aligns with rental models that eliminate capital expenditure while providing access to latest-generation equipment with integrated telematics and performance monitoring capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Rupiah Raising Import Cost of Replacement Parts and Units | -1.2% | National, particularly affecting imported equipment | Short term (≤ 2 years) |

| Fragmented After-Sales Network Outside Java Prolongs Downtime | -0.8% | Outer islands: Sumatra, Kalimantan, Sulawesi, Papua | Long term (≥ 4 years) |

| Rising Popularity of AGVs Reducing Class III Forklift Demand | -0.6% | Advanced manufacturing hubs in Java and Batam | Medium term (2-4 years) |

| Unregulated Informal Rental Operators Depressing Prices | -0.4% | Regional markets outside major industrial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Rupiah Hikes Import Costs for Replacement Parts and Units.

Indonesian customers' perception of imported equipment as expensive but durable creates price sensitivity that intensifies during currency volatility periods. The rupiah's fluctuations against major currencies directly impact replacement parts costs, with many customers checking prices online before purchasing, creating transparency that pressures rental rates downward during unfavorable exchange periods. Import-dependent equipment faces additional challenges from the 10% VAT and luxury goods taxes that compound currency impact on total cost of ownership. Rental companies must balance currency hedging costs against competitive pricing, often absorbing exchange rate volatility to maintain market share. The shift toward local assembly and parts sourcing becomes economically attractive during extended periods of currency weakness, though this transition requires significant capital investment and technology transfer agreements.

Fragmented after-sales network outside Java prolongs downtime

Service network fragmentation beyond Java's industrial corridors creates operational risks that favor equipment ownership over rental in remote locations where downtime costs exceed rental savings. The concentration of technical expertise and parts inventory in Java-based service centers results in extended equipment unavailability during repairs, particularly affecting mining and plantation operations in outer islands. Rental companies face higher operational costs in non-Java markets due to logistics complexity and lower equipment utilization rates, often leading to premium pricing that reduces rental attractiveness. The challenge intensifies for specialized equipment requiring manufacturer-certified technicians, creating market opportunities for companies that invest in distributed service capabilities. Regional economic development initiatives may eventually address this constraint, but the timeline extends beyond typical investment planning horizons for most rental operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Load Capacity: Compact Units Drive Market Evolution

Less than 3.5-ton forklifts captured 45.83% market share in 2025 while leading growth at 9.31% CAGR through 2031, reflecting Indonesia's shift toward smaller-scale, flexible operations in e-commerce fulfillment and urban logistics. This segment's dominance stems from warehouse space constraints in Java's industrial areas and the growing preference for multi-shift operations that favor lighter, more maneuverable equipment. The 3.6 to 10-ton segment serves traditional manufacturing and construction applications, maintaining steady demand aligned with Indonesia's industrial production growth. Units exceeding 10 tons concentrate in heavy industry applications, including steel, cement, and mining operations, with demand patterns closely tied to commodity cycles and infrastructure project timing.

E-commerce warehousing expansion particularly drives compact unit demand, as fulfillment centers prioritize throughput over heavy lifting capacity, creating rental preferences for fleets that can scale rapidly during peak seasons. Over 40% of forklift transactions now involve advanced technologies like IoT integration, with compact units leading this adoption due to their deployment in digitally-advanced logistics operations. The segment's growth trajectory aligns with Indonesia's economic transition toward services and light manufacturing, where operational flexibility outweighs raw lifting capacity in equipment selection criteria.

By Rental Duration: Mid-Term Contracts Reshape Industry Dynamics

The rental duration landscape reveals strategic shifts in customer preferences, with short-term arrangements holding 53.62% market share in 2025 despite mid-term contracts accelerating at 10.56% CAGR through 2031. This divergence reflects Indonesia's economic maturation, where businesses increasingly seek operational predictability through medium-duration commitments while maintaining flexibility for capacity adjustments. Short-term rentals remain dominant in construction and event-driven applications where project timelines dictate equipment needs. Long-term leases serve established operations requiring consistent material handling capacity without capital commitment, particularly in manufacturing and distribution facilities.

Mid-term rental growth acceleration indicates sophisticated demand planning among Indonesian businesses, driven by improved economic forecasting capabilities and supply chain optimization initiatives. The services sector's 60% contribution to value added creates stable demand patterns that support longer rental commitments while avoiding the capital intensity of ownership. Banking sector challenges projected for 2025, including tight liquidity and elevated interest rates, make rental arrangements more attractive than equipment financing for businesses seeking to preserve cash flow flexibility.

By Power Source: Electric Transition Accelerates Despite ICE Dominance

Internal combustion engines maintained 61.35% market share in 2025, yet electric variants surge ahead with 15.08% projected CAGR, creating a fundamental shift in rental fleet composition and operational strategies. This transition reflects Indonesia's decarbonization commitments and PLN's green energy initiatives that reduce operational costs for electric equipment in facilities with renewable energy access. Hybrid systems occupy a transitional role, offering operational flexibility while customers adapt to electric infrastructure requirements. The electric surge benefits from Japanese companies' contributions to Indonesia's decarbonization efforts, including solar power generation equipment rental that complements electric forklift operations.

Lithium-ion battery technology adoption, projected to dominate by 2030, creates rental advantages through reduced maintenance requirements and operational cost predictability compared to internal combustion alternatives. Electric forklift rental demand increased over 30% in 2024, driven by warehouse operators seeking to reduce emissions and operational costs while avoiding the capital investment required for charging infrastructure. The transition favors professional rental fleets that can provide integrated charging solutions and maintenance expertise, creating competitive advantages for companies investing in electric fleet capabilities.

By Truck Class: Class I Growth Challenges Traditional Hierarchies

Class III forklifts held 37.78% market share in 2025, reflecting their versatility in warehouse and light industrial applications, while Class I units accelerate at 12.74% CAGR, driven by electric adoption and automation integration in modern facilities. This growth pattern indicates Indonesia's logistics sector evolution toward higher-precision, technology-enabled operations that favor electric counterbalance and reach trucks over traditional internal combustion models. Class II equipment serves specialized narrow-aisle applications in space-constrained facilities, while Class IV and V units concentrate in heavy-duty applications including container handling at ports and steel processing facilities.

The Class I acceleration aligns with warehouse automation trends and electric vehicle adoption, as these units integrate more readily with facility management systems and offer superior operational data collection capabilities. PELINDO's port automation programs create specific demand for Class IV and V equipment designed for container handling, with rental arrangements preferred due to operational complexity and maintenance requirements. Class III dominance reflects Indonesia's industrial structure, where general-purpose material handling remains the primary requirement, though automation and electrification trends gradually shift preferences toward more specialized equipment categories.

By End-Use Industry: Warehousing Dominance Reinforces Logistics Transformation

Warehousing and logistics captured 50.37% market share in 2025 while leading growth at 12.14% CAGR, reinforcing the sector's role as the primary driver of forklift rental demand in Indonesia. This dominance reflects the services sector's 60% contribution to total value added and employment, creating multiplier effects where logistics growth generates disproportionate equipment demand. Construction applications benefit from the PSN program's IDR 1,040 trillion investment, though demand patterns remain project-dependent and cyclical. Automotive sector demand aligns with Indonesia's position as a regional manufacturing hub, while food and beverage applications grow with domestic consumption and export expansion.

The aerospace and defense segment, though smaller in absolute terms, represents high-value applications requiring specialized equipment and maintenance capabilities that favor professional rental arrangements. Other industries, including retail and pharmaceutical, contribute a steady demand driven by distribution center expansion and regulatory compliance requirements. The logistics sector's over 50% contribution to total forklift demand creates rental market stability, as warehousing operations require consistent material handling capacity with predictable utilization patterns. E-commerce growth particularly drives short-term and mid-term rental preferences, as operators require flexible capacity scaling without capital commitment during demand fluctuations.

Geography Analysis

Indonesia's forklift rental market exhibits pronounced regional concentration, with Java commanding the dominant position due to its industrial density and infrastructure development, while outer islands present emerging opportunities constrained by service network limitations and logistics complexity. The archipelago's geography creates distinct demand patterns, where Java's established industrial corridors generate consistent rental demand across manufacturing, logistics, and construction sectors, supported by comprehensive after-sales networks and technical expertise. Sumatra's plantation and mining operations require specialized heavy-duty equipment with extended service intervals due to remote locations and challenging operating conditions. Kalimantan's coal mining and palm oil industries create cyclical demand patterns tied to commodity prices and seasonal production cycles.

The services sector's 60% contribution to national value added concentrates primarily in Java's urban centers, creating stable demand for material handling equipment in warehousing and distribution applications. Tanjung Priok Port's handling of approximately 50% of Indonesia's cargo volume positions Jakarta as a critical demand node, with PELINDO's automation initiatives driving specialized container-handling equipment requirements. Regional economic disparities create varying rental preferences, with Java-based operations favoring advanced technology integration and electric equipment, while outer island applications prioritize durability and extended service intervals over technological sophistication.

The forklift rental market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America. This is complemented by country-specific insights for South Korea, United States, Saudi Arabia, Brazil, and United Arab Emirates, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Indonesia forklift rental market exhibits moderate fragmentation with established players leveraging brand recognition and service network density to maintain competitive positions, while emerging operators focus on niche applications and regional specialization. Market concentration reflects the capital-intensive nature of fleet operations and the importance of after-sales service capabilities, particularly in Indonesia's challenging geographic and infrastructure environment. Strategic patterns emphasize vertical integration, with leading companies combining equipment sales, rental, and maintenance services to capture value across the customer lifecycle and reduce competitive vulnerability.

Technology adoption creates differentiation opportunities, with over 40% of forklift transactions now involving advanced technologies like IoT integration and telematics capabilities. White-space opportunities exist in outer island markets where service network limitations create barriers to entry but also reduce competitive intensity for companies willing to invest in distributed capabilities. The shift toward electric equipment and pay-per-use rental models favors operators with technical expertise and capital resources to support charging infrastructure and advanced fleet management systems. Regulatory barriers in strategic logistics sectors create market access challenges for foreign companies while protecting domestic players' competitive positions, though public-private partnership opportunities may reshape these dynamics as infrastructure development accelerates.

Indonesia Forklift Rental Industry Leaders

-

Toyota Material Handling Indonesia (Traktor Nusantara)

-

PT United Tractors

-

PT UMW Equipment and Engineering

-

PT Berca Mandiri Perkasa (Kalmar)

-

SML Rental

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Indonesia's infrastructure budget reached IDR 422.7 trillion for 2024, representing continued growth from IDR 381.2 trillion in 2017 under the PSN program. This investment level supports sustained construction equipment rental demand across multiple project phases and geographic regions.

- January 2024: In January 2024, MNC Leasing, a subsidiary of MNC Group, inked a IDR 50 billion joint financing deal with Bank SBI Indonesia. This partnership is set to enhance financial backing for Indonesia's strategic sectors. The focus is on amplifying credit distribution and bolstering financial aid, particularly in commercial and industrial equipment sectors like logistics and construction. MNC Leasing, under the MNC Group umbrella, is a key player in multifinance services, providing leasing and financing solutions for vehicles, heavy machinery, and other productive assets.

Indonesia Forklift Rental Market Report Scope

| Less Than 3.5 T |

| 3.6 to 10 T |

| More Than 10 T |

| Short-term/Spot (Less than 1 month) |

| Mid-term (1 to 12 months) |

| Long-term Lease (3 to 5 years) |

| Electric |

| Internal Combustion (Diesel/LPG) |

| Hybrid |

| Class I |

| Class II |

| Class III |

| Class IV |

| Class V |

| Warehousing and Logistics |

| Construction |

| Automotive |

| Food and Beverage |

| Aerospace and Defense |

| Others (Retail, Pharma, etc.) |

| By Load Capacity | Less Than 3.5 T |

| 3.6 to 10 T | |

| More Than 10 T | |

| By Rental Duration | Short-term/Spot (Less than 1 month) |

| Mid-term (1 to 12 months) | |

| Long-term Lease (3 to 5 years) | |

| By Power Source | Electric |

| Internal Combustion (Diesel/LPG) | |

| Hybrid | |

| By Truck Class | Class I |

| Class II | |

| Class III | |

| Class IV | |

| Class V | |

| By End-use Industry | Warehousing and Logistics |

| Construction | |

| Automotive | |

| Food and Beverage | |

| Aerospace and Defense | |

| Others (Retail, Pharma, etc.) |

Key Questions Answered in the Report

What is the current size of the Indonesia forklift rental market?

The Indonesia forklift rental market size reached USD 116.02 million in 2026 and is projected to climb to USD 162.12 million by 2031 at a 6.92% CAGR over 2026-2031.

Which segment leads by load capacity?

Forklifts under 3.5 tons lead with 45.83% share in 2025 and are forecast to grow at 9.31% CAGR through 2031.

How fast is the electric forklift segment growing?

Electric models are the fastest-growing power source segment, advancing at a 15.08% CAGR over 2026-2031 owing to PLN green-power incentives and lower lifecycle costs.

Why are mid-term rental contracts gaining popularity?

Businesses have better demand visibility and prefer three- to twelve-month contracts to balance operational predictability with flexibility, fueling an 10.56% CAGR in mid-term rentals through 2031.

Page last updated on: