Europe Forklift Rental Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.51 Billion |

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 4.74 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

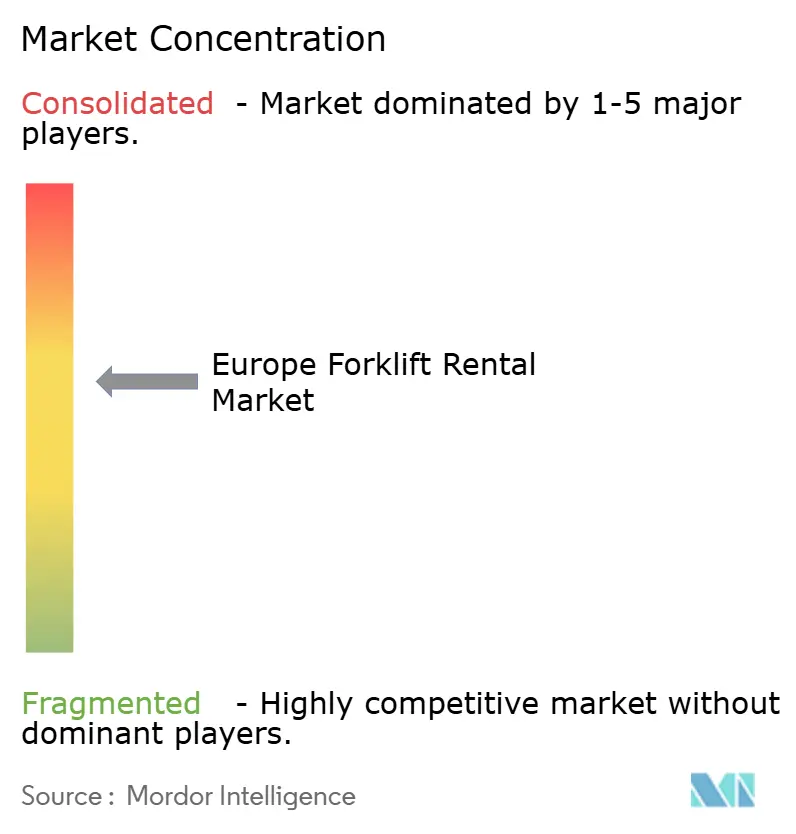

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Forklift Rental Market Analysis by Mordor Intelligence

The Europe forklift rental market size in 2026 is estimated at USD 3.69 billion, growing from 2025 value of USD 3.51 billion with 2031 projections showing USD 4.74 billion, growing at 5.14% CAGR over 2026-2031. As enterprises pivot from owning assets to embracing usage-based models, they align equipment costs with revenue fluctuations. The surge in e-commerce demands a peak handling capacity that can significantly exceed baseline needs during seasonal spikes. This drives warehouse operators to opt for forklifts on a pay-per-use basis. While ongoing electrification and nascent hydrogen pilots introduce technological risks, many firms sidestep these by outsourcing fleet investments to rental specialists. The competition intensifies as pure-play rental firms consolidate and OEM-backed programs emerge, resulting in scale efficiencies for fleet modernization. With manufacturing nearshoring and the rise of pop-up logistics hubs in Central and Eastern Europe, the demand for flexible equipment access sees a notable uptick.

Key Report Takeaways

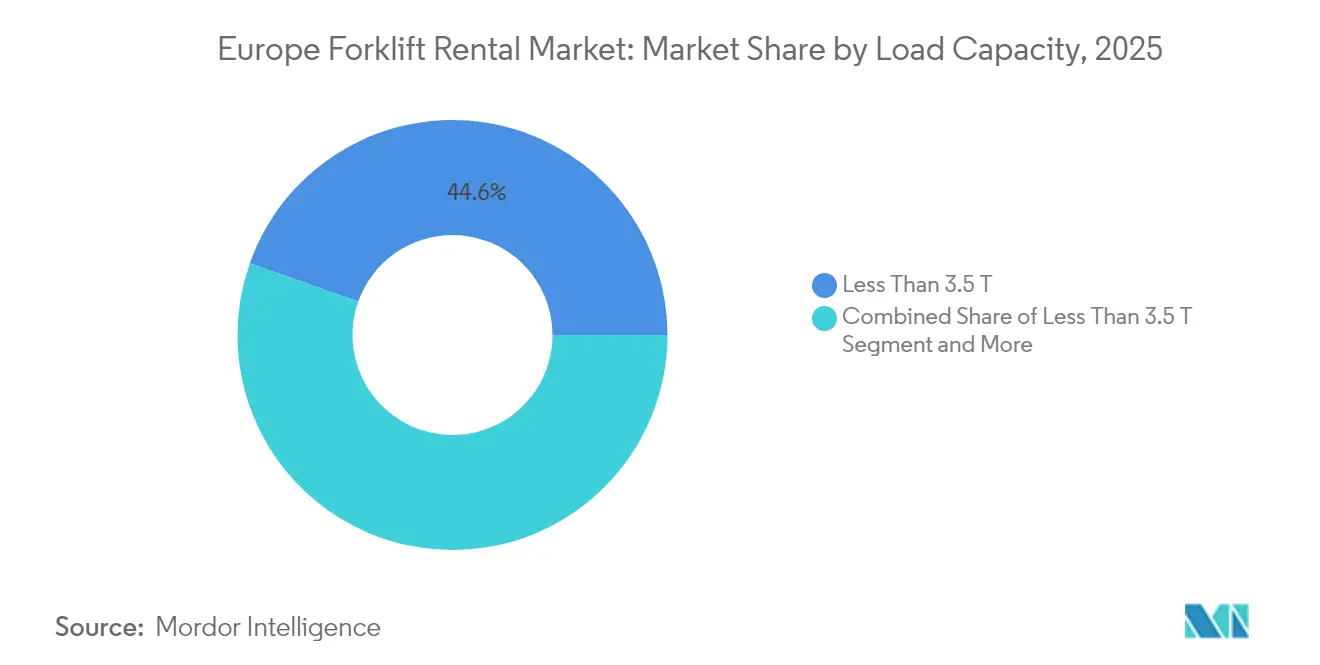

- By load capacity, forklifts under 3.5 tons led with 44.58% of the European forklift rental market share in 2025, while the same segment posts the highest 5.25% CAGR through 2031.

- By rental duration, short-term contracts held 57.08% of the European forklift rental market size in 2025 and grew at a 5.27% CAGR over the forecast horizon.

- By power source, electric models captured a 62.74% European forklift rental market share in 2025; hydrogen fuel cell units are expected to expand at a 5.33% CAGR through 2031.

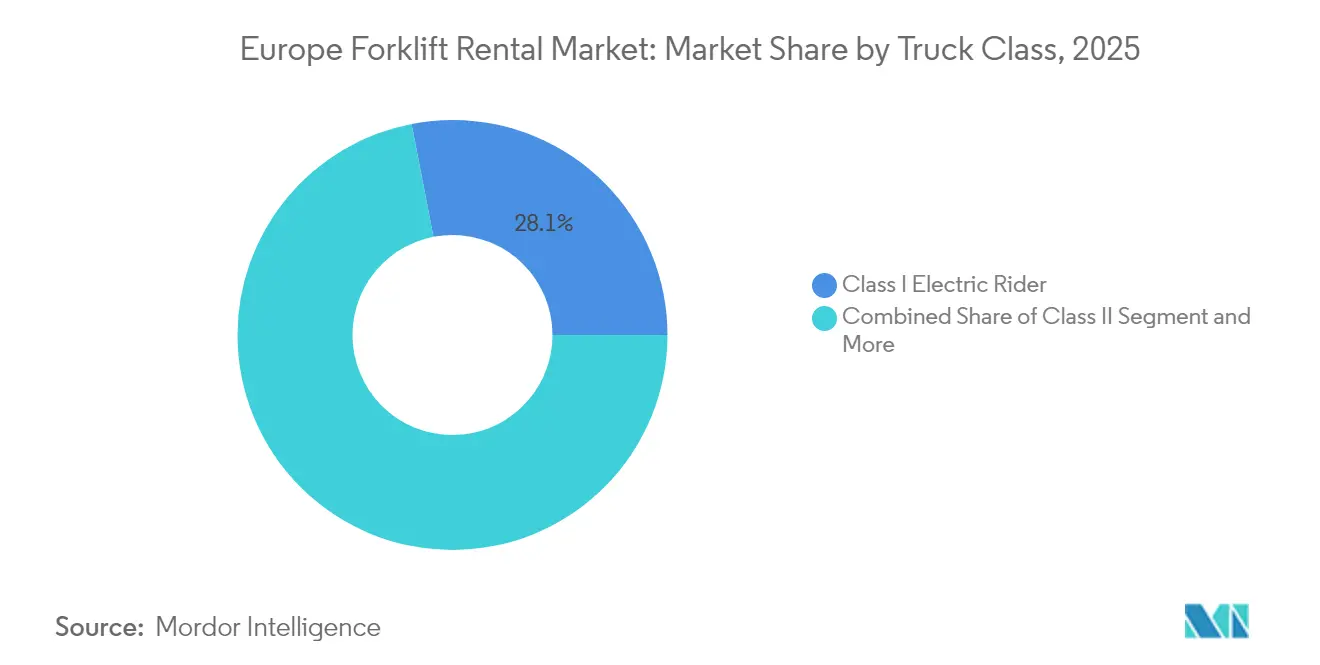

- By truck class, Class I electric riders accounted for 28.05% of the European forklift rental market size in 2025 and registered a 5.24% CAGR through 2031.

- By end-use industry, warehousing and logistics commanded a 36.41% of the European forklift rental market in 2025, while e-commerce fulfillment centers achieved the fastest growth rate of 5.31% CAGR.

- By country, Germany led with a 26.12% of the European forklift rental market in 2025, while Poland delivered the highest 5.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Forklift Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Boom | +1.2% | Germany, Netherlands, UK, France core markets | Medium term (2-4 years) |

| Shift Toward OPEX Models | +0.9% | Global Europe, strongest in SME segments | Short term (≤ 2 years) |

| Tight EU Emissions Rules | +0.8% | EU-wide, early adoption in Nordic countries | Long term (≥ 4 years) |

| Pop-Up Logistics Hubs | +0.6% | Germany, Netherlands, Poland construction corridors | Medium term (2-4 years) |

| Automation-Ready Forklifts | +0.4% | Germany, Netherlands, Nordic countries early adopters | Medium term (2-4 years) |

| Need for Operational Flexibility Management | +0.3% | Europe-wide, strongest in retail and e-commerce | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Boom Raises Warehousing Forklift Rental Demand

Record investment in European fulfillment infrastructure fuels sustained demand for flexible forklift capacity. Otto Group’s automated center in Poland illustrates how operators require specialized trucks during ramp-up without committing to permanent fleets [1]“New Fulfillment Center in Poland,” Otto Group, otto.de . In 2024, developers set a record by delivering a substantial amount of logistics space, with a significant portion earmarked for e-commerce. This surge in e-commerce logistics not only heightened demand but also established equipment needs that are expected to endure well beyond the stabilization of occupancy. Rental providers, in response, rapidly expanded their fleets, taking on technological risks for clients who prioritize core fulfillment metrics. As e-commerce businesses expand their footprint into regional cities, local depots are increasingly turning to short-term rentals to manage their variable throughput patterns. Meanwhile, same-day and next-day delivery targets have intensified volume fluctuations, leading to considerable rental spikes during peak seasons.

Shift Toward OPEX Models to Avoid High CAPEX

European finance teams are increasingly adopting off-balance-sheet equipment strategies to safeguard liquidity and crucial leverage ratios. KION Group revealed that in recent years, a significant portion of industrial truck transactions involved rentals or leases, marking a notable increase compared to earlier periods. CFOs, grappling with rising borrowing costs and macroeconomic uncertainties, are drawn to the predictability of monthly fees. For SMEs, bundled maintenance services are particularly enticing, given their limited internal fleet management resources. Meanwhile, multinationals venturing into new EU markets favor rental contracts that can be swiftly scaled or exited, aligning with crystallizing local demand. This strategy is in line with IFRS 16 lease accounting rules, which allow many short-term rentals to be treated as operating leases, thus preserving flexibility in capital allocation.

Tight EU Emissions Rules Spur Electric Forklift Rental

The Alternative Fuels Infrastructure Regulation requires the widespread installation of charging facilities by 2025, while the Non-Road Mobile Machinery Regulation phases out legacy diesel engines. Manufacturers such as BMW pilot hydrogen fuel cell forklifts through rental programs to validate performance before complete conversion. Rental firms shoulder upfront costs for batteries or fuel cells, allowing end users to remain compliant without fearing rapid technology shifts. Nordic markets move earliest, driven by the abundance of renewable energy and stringent workplace air-quality laws. ISO 3691-4:2023 safety protocols for autonomous trucks add complexity that rental specialists manage at scale, enhancing their value proposition.

Pop-up Logistics Hubs for Modular Construction Projects

European contractors deploy temporary assembly yards that demand intensive material handling for 6-18 months. A typical modular housing site in Germany may rent 20 forklifts to load prefabricated panels before units are trucked to final locations. Rental economics outperform ownership because utilization typically declines sharply once on-site construction concludes. Fleet providers offer rough-terrain options and specialized clamps designed explicitly for prefab modules, thereby mitigating idle inventory risk for builders. Rising labor shortages in Western Europe push contractors toward controlled factory environments, reinforcing the cycle of short-duration, high-intensity equipment demand. Construction spending on modular methods increased by one-fifth in 2024, creating a predictable pipeline for short-term rentals [2]“European Construction Market Forecasts,” Euroconstruct, euroconstruct.org .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant Supply of Inexpensive Used Forklifts | -0.7% | Germany, UK markets with mature fleets | Short term (≤ 2 years) |

| High Lifecycle Maintenance Cost | -0.5% | Europe-wide, acute in cost-sensitive segments | Medium term (2-4 years) |

| Battery-Recycling Bottlenecks Limit Electric Fleet Growth | -0.4% | EU-wide, acute in Germany and Netherlands | Long term (≥ 4 years) |

| Rising Insurance Premiums | -0.3% | Germany, Netherlands, Nordic early automation markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

An Abundant Supply of Inexpensive Used Forklifts

Fleet upgrades to new electric units released large volumes of older trucks into the secondary market in 2024, expanding used inventory by one-fifth across major economies [3]“Used Equipment Market Trends 2024,” Jungheinrich, jungheinrich.com . Operators with stable demand opt to buy three-year-old units outright, achieving lower lifetime cost than short-term rentals. Ready financing from regional banks supports these purchases, particularly for family-owned warehouses that focus on cost containment and efficiency. Rental companies respond by emphasizing service uptime, safety certification, and telematics, rather than engaging in a race to the bottom on daily rates. Yet the price gap between used ownership and premium rentals narrows margin headroom, forcing greater efficiency in fleet utilization.

High Lifecycle Maintenance Cost of Aging Rental Fleets

Intensive duty cycles have pushed rental utilization to high levels, leading to accelerated component wear, especially when compared to privately owned fleets. Over time, replacing lithium-ion batteries can represent a significant portion of a vehicle's original cost. Under EU recycling mandates, additional fees are levied for the safe transport and disposal of batteries, in accordance with ADR rules. Rising spare-parts inflation is squeezing operating margins, causing fleet owners to either shorten replacement cycles or increase rental rates. Customers, who are sensitive to overall costs, might revert to ownership if rental premiums surpass financing charges. This shift poses a threat to growth momentum, especially if maintenance inflation remains unchecked.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Load Capacity: Compact Units Dominate Indoor Workflows

Less-than-3.5-ton models accounted for 44.58% of the European forklift rental market share in 2025 and recorded the highest 5.25% CAGR through 2031. The segment suits narrow-aisle warehouses where maneuverability outweighs brute lift force. E-commerce operators store thousands of SKUs in high-density racks, requiring agile trucks that pivot within tight clearances. Small chassis sizes also integrate easily with emerging navigation software, lowering barriers for autonomous retrofits. The mid-capacity 3.6-10 ton band serves lumber yards, metal depots, and outdoor assembly sites, but its growth is slower as heavy industry remains relatively flat. Units above 10 tons cater to ports and steel mills, maintaining a niche yet stable demand due to specialized attachment needs.

Rental providers prioritize compact electric models because rapid technological change shortens their economic life, making pay-per-use more rational for customers who want the latest energy efficiency and safety features. Toyota Material Handling Europe’s collaboration with Gideon on autonomous kits exemplifies the vendor's focus on these smaller units, where sensor integration is more straightforward and weight balances align with battery architecture. Compact forklifts also benefit from declining lithium-ion battery costs, enabling multi-shift operation without the need for battery swaps. As warehouses add mezzanine floors and micro-fulfillment layouts, demand for low-capacity riders continues to climb, reinforcing the leadership of this class within the European forklift rental market.

By Rental Duration: Short-term Flexibility Underpins Strategy

Short-term contracts captured 57.08% of the European forklift rental market share in 2025 and posted a 5.27% CAGR through 2031. Companies facing demand volatility often lock in equipment for weeks or months, rather than for multi-year blocks. This pattern intensified after pandemic disruptions demonstrated the value of variable cost structures that can shrink during downturns. Long-term agreements remain relevant for predictable manufacturing flows that benefit from bundled maintenance and guaranteed uptime; however, they grow more slowly as macroeconomic uncertainty lingers.

Rental firms expand geographic footprints to supply last-minute requests. Kiloutou’s acquisitions of ToolQuick, Liftisa, and Gloobal in Spain expanded branch density, allowing customers to source equipment within 24 hours across Iberia. Digital portals now quote rates in real time, allowing logistics managers to align forklift counts with weekly parcel forecasts. The trend dovetails with shift-based labor scheduling and dynamic slotting algorithms, which maximize productivity when material-handling assets are scaled in parallel. As automation pilots proliferate, companies test equipment under short contracts before committing to permanent system redesign, reinforcing the dominance of short-term rentals in the European forklift rental market.

By Power Source: Electric Leads as Hydrogen Gains Ground

Electric forklifts secured 62.74% market share in 2025, reflecting strict indoor emissions norms and the maturity of battery technology. Advancements in lithium-ion chemistry provide full-shift runtime with opportunity charging, eliminating mid-day battery swaps and freeing warehouse floor space once reserved for spare packs. Integrated telematics enables rental firms to monitor charge cycles remotely, optimizing fleet rotation and prolonging battery life.

Hydrogen fuel cell models rank as the fastest-growing power class, with a 5.33% CAGR to 2031, addressing applications that require 24/7 operation without long recharge windows. Toyota Material Handling’s trials with cold-chain specialist STEF demonstrate how hydrogen suits environments below freezing, where battery performance degrades. Linde and Plug Power collaborate on modular refueling stations that rental providers can relocate as customer needs evolve. Internal-combustion trucks powered by diesel or LPG remain popular on rough terrain, although their share is expected to decline as the EU tightens CO₂ limits. Hybrid systems provide a bridge for users awaiting the development of a complete hydrogen infrastructure. Yet, most growth capital funnels toward battery and fuel-cell technologies, reshaping fleet mix within the European forklift rental market.

By Truck Class: Class I – Electric Rider Anchor Warehouse Automation

Class I electric rider trucks generated 28.05% of the European forklift rental market size in 2025 and achieved a 5.24% CAGR through 2031. Their standing stems from optimal load balance, ergonomic cabins, and compatibility with both manual and driverless operation. Class II narrow-aisle trucks complement automation strategies by serving high-bay storage, while Class III pallet movers handle last-meter tasks. Class IV and V internal-combustion units retain roles in yards and fabrication plants but face substitution as battery tech extends lifting capacity.

OEMs embed dual-use hardware, allowing the same chassis to run in either manual or autonomous mode, which appeals to renters who expect equipment reuse across multiple assignments. KION’s KANIS navigation suite targets rider platforms to accelerate the deployment of automated pilots in brownfield warehouses. Rental specialists preload safety laser scanners and ISO 3691-4 compliant logic, enabling customers to activate autonomy through a software license rather than incurring new capital expenditures. This plug-and-play approach enhances utilization by allowing trucks to rotate between conventional and high-tech contracts, thereby reinforcing the centrality of Class I riders to the European forklift rental market.

By End-Use Industry: E-commerce Reshapes Material-handling Norms

Warehousing and logistics accounted for 36.41% of the 2025 market revenue, underpinned by the addition of more than 30 million square meters of new distribution centers since 2022. E-commerce fulfillment is projected to post the highest 5.31% CAGR to 2031 as online penetration increases in southern and eastern Europe. Fulfillment sites require rapid acceleration, tight turning radius, and advanced operator-assist systems to manage high volumes of orders per hour.

Construction maintains a solid rental base through modular building projects, where rough-terrain telehandlers and mid-capacity trucks load prefabricated walls. Automotive plants demand mixed fleets that handle inbound components and finished engines, while food and beverage companies prioritize hygienic coatings and condensation-resistant electronics. Pharmaceuticals adopt cold-chain compliant lithium-ion packs to protect product integrity. Each vertical imposes unique attachment and safety standards, encouraging customers to outsource fleet configuration within the European forklift rental market rather than maintain diverse internal inventories.

Geography Analysis

Germany held 26.12% of 2025 revenue, leveraging a dense network of tier-one suppliers and consumer goods hubs. Warehouse construction around Berlin, Hamburg, and Munich continued despite soft macro data, driven by omnichannel retail and build-to-suit projects for third-party logistics firms. Local renters emphasize uptime and advanced safety features, paying premiums for telematics and predictive maintenance. Environmental regulations promote the replacement of diesel yard trucks with electric alternatives, creating recurring upgrade cycles that stabilize demand even in slow economic years.

Poland registers the fastest 5.28% CAGR through 2031, benefiting from nearshoring and record logistics real estate pipelines in Łódź, Poznań, and the Upper Silesian industrial region. International manufacturers relocating production from Asia to Central Europe often turn to rental providers for scalable fleets before their volume forecasts are finalized. Domestic 3PLs prefer rental to circumvent capital outlays while chasing rapid e-commerce growth. EU subsidies for alternative fuel infrastructure accelerate the adoption of battery and hydrogen equipment, enhancing the technology mix available to Polish renters.

The Netherlands, France, Italy, Spain, Belgium, and the Nordic countries collectively contribute a significant portion of the European forklift rental market revenue. Dutch ports anchor specialized heavy-lift rentals, while France mixes legacy industrial clients with rising online grocery fulfillment. Italy’s fashion and automotive sectors drive seasonal surges that suit short-term contracts. Spain’s infrastructure revival boosts telehandler demand, while the Nordic countries secure sustainability-minded contracts for zero-emission fleets. Each geography requires customized service levels and fleet composition, yet unified digital platforms allow major players to pool assets across borders and maximize utilization.

Competitive Landscape

Competition balances global OEM finance arms against agile, pure-play rental specialists, yielding a moderately concentrated field. KION, Toyota Material Handling, and Jungheinrich bundle manufacturing, financing, and after-sales into turnkey rental propositions that appeal to enterprise clients. Independent firms, such as Boels, Kiloutou, and TVH, differentiate themselves through their rapid response and multi-brand fleets. The Boels-Riwal transaction in June 2024 expanded Boels’ portfolio beyond construction equipment into material-handling niches, reinforcing cross-selling potential for joint customers across 13 countries.

Scale matters as electrification raises capital intensity. Top players invest in lithium-ion packs, telemetry gateways, and hydrogen refueling to deliver compliant fleets before smaller rivals can fund upgrades. Telematics portals track utilization and state of charge in real-time, supporting predictive maintenance that curtails downtime penalties in service-level agreements. Technology competencies form new competitive moats because ISO 3691-4 certification, cybersecurity protocols, and integration with warehouse management systems exceed the capabilities of fragmented local outfits.

Consolidation is set to continue as low interest rates on green financing, albeit higher than pre-2023 levels, still favor asset-heavy strategies. Cross-border acquisitions offer immediate scale in underserved Central European markets, where organic branch expansion can take years. Simultaneously, OEMs weigh whether direct rentals cannibalize dealer sales, leading some to pursue minority investments in specialist lessors rather than complete internalization. The race to supply hydrogen units and autonomous riders by 2027 will further separate innovators from laggards within the European forklift rental market.

Europe Forklift Rental Industry Leaders

STILL GmbH

Linde Material Handling

Jungheinrich AG

Riwal

Crown Equipment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Boels closed its EUR 314 million (USD 343 million) acquisition of Riwal, creating Europe’s largest aerial work platform and material-handling rental fleet of more than 20,000 units across 65 branches in 13 countries.

- February 2024: Toyota Material Handling Europe partnered with Gideon to embed autonomous navigation software into Toyota forklifts, targeting retail distribution centers across the region.

Europe Forklift Rental Market Report Scope

The Forklift rental market is segmented by load type (3. 5 tons, 10 tons, and above 10 tons), power source type (Internal combustion engine(ICE), electric), end-use type (construction, automotive, aerospace and defense, warehouse and logistics, and other end-use types), and by country (Germany, United Kingdom, France, Italy, Spain, Rest of Europe).

The report offers market size and forecast for the forklift rental market in value (USD billion) for all the above segments.

| Less Than 3.5 T |

| 3.6 – 10 T |

| More Than 10 T |

| Short-term |

| Long-term |

| Electric |

| Internal Combustion (Diesel/LPG) |

| Hybrid / Hydrogen |

| Class I – Electric Rider |

| Class II – Narrow-Aisle |

| Class III – Electric Hand |

| Class IV – ICE Cushion |

| Class V – ICE Pneumatic |

| Warehousing & Logistics |

| Construction |

| Automotive |

| Food & Beverage |

| Aerospace & Defense |

| Retail |

| Pharmaceuticals |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Belgium |

| Sweden |

| Denmark |

| Rest of Europe |

| By Load Capacity | Less Than 3.5 T |

| 3.6 – 10 T | |

| More Than 10 T | |

| By Rental Duration | Short-term |

| Long-term | |

| By Power Source | Electric |

| Internal Combustion (Diesel/LPG) | |

| Hybrid / Hydrogen | |

| By Truck Class | Class I – Electric Rider |

| Class II – Narrow-Aisle | |

| Class III – Electric Hand | |

| Class IV – ICE Cushion | |

| Class V – ICE Pneumatic | |

| By End-use Industry | Warehousing & Logistics |

| Construction | |

| Automotive | |

| Food & Beverage | |

| Aerospace & Defense | |

| Retail | |

| Pharmaceuticals | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Denmark | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size of the European forklift rental market in 2026?

The European forklift rental market size stands at USD 3.69 billion in 2026 and is projected to reach USD 4.74 billion by 2031.

Which load capacity segment grows the fastest in European rentals?

Forklifts weighing under 3.5 tons are expected to grow at a 5.25% CAGR by 2031, primarily due to their suitability for narrow-aisle warehouses.

Why are short-term rental contracts popular?

Short-term rentals enable companies to match forklift supply with volatile demand, avoiding fixed depreciation during slow periods and allowing for rapid scale-up during seasonal peaks.

Which power technology is gaining the most momentum?

Hydrogen fuel cells are projected to post the highest 5.33% CAGR to 2031, especially in cold-storage and multi-shift applications that require quick refueling.

What drives forklift rental growth in Poland?

Nearshoring of manufacturing, rapid warehouse construction, and EU funding for green logistics are expected to create a 5.28% CAGR for the Polish market through 2031.

How is consolidation shaping the competitive landscape?

Acquisitions such as Boels’ purchase of Riwal demonstrate a trend toward scale economics, allowing large fleets to fund electrification and hydrogen pilots while offering pan-European coverage.

Page last updated on: