Forklift Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 5.39 Billion |

| Market Size (2031) | USD 7.35 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

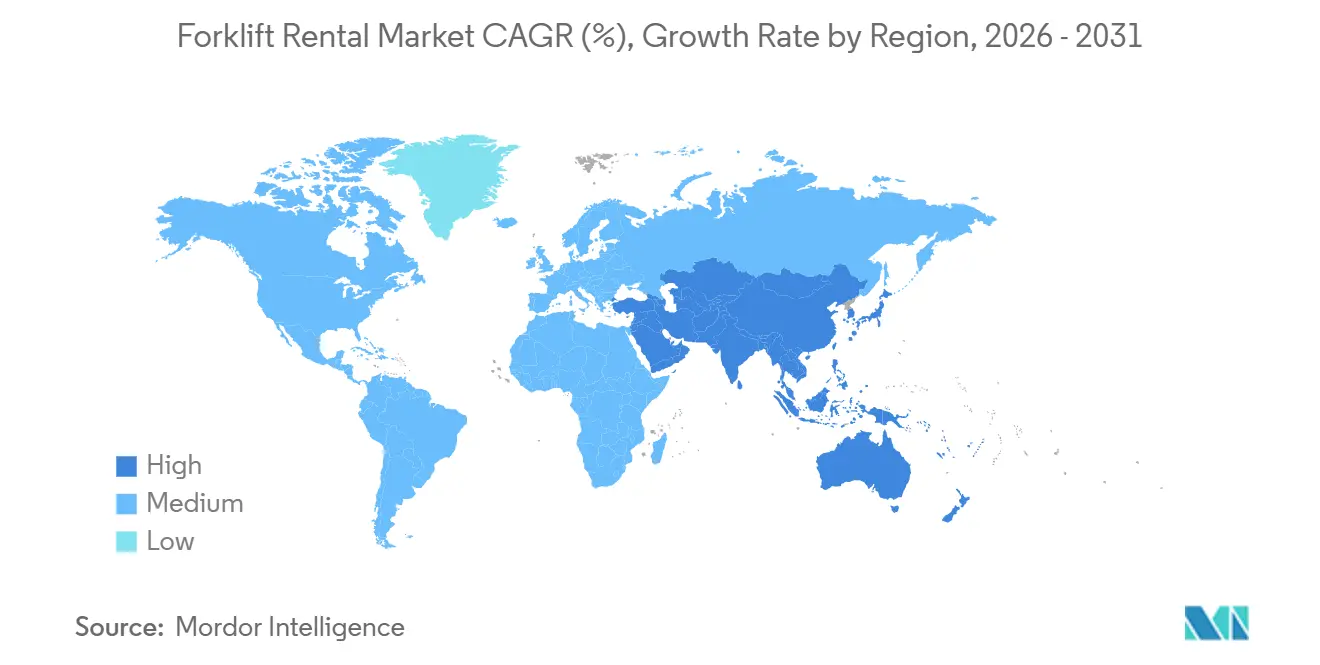

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Forklift Rental Market Analysis by Mordor Intelligence

The forklift rental market size was valued at USD 5.10 billion in 2025 and estimated to grow from USD 5.39 billion in 2026 to reach USD 7.35 billion by 2031, at a CAGR of 6.39% during the forecast period (2026-2031). Growth is accelerating because companies are favoring short-cycle operating expenses over balance-sheet-heavy equipment ownership, while electric models are rapidly displacing diesel and LPG fleets that face costly compliance under tightening emission rules. Heightened peak-season volatility in e-commerce, the proliferation of narrow-aisle warehouses, and the need for telematics-enabled units that support automation keep utilization rates high and reduce downtime. Original equipment manufacturer subscription offerings that bundle hardware, software, and maintenance deepen competition, yet they also expand demand by lowering entry barriers for midsize operators. Overall, the forklift rental market benefits from a structural pivot toward flexible capacity in supply chains that value uptime and environmental compliance over outright ownership.

Key Report Takeaways

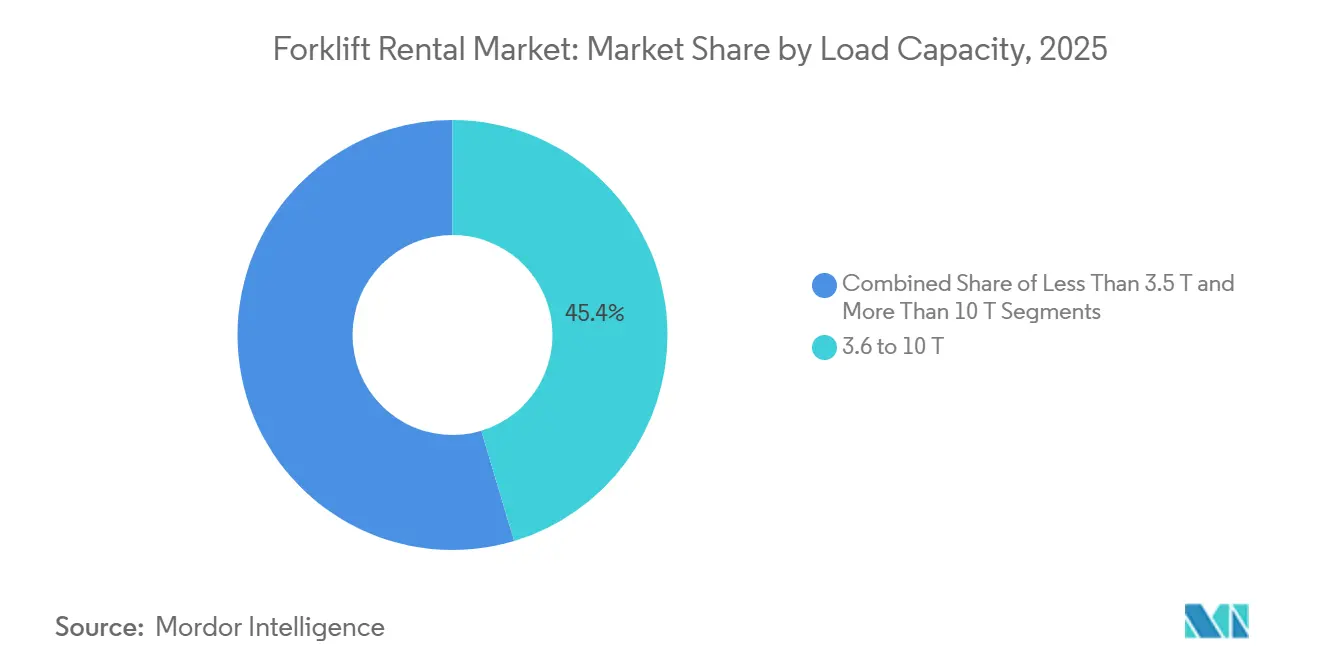

- By load capacity segment, the 3.6-10 ton category held 45.37% of the forklift rental market share in 2025; the sub-3.5 ton class is projected to expand at a 10.67% CAGR through 2031.

- By power source, electric forklifts commanded 54.39% of the forklift rental market share in 2025 and are expected to grow at an 11.89% CAGR.

- By rental duration, short-term contracts accounted for 64.73% of revenue in 2025, whereas long-term agreements are forecast to post the fastest growth at an 8.50% CAGR.

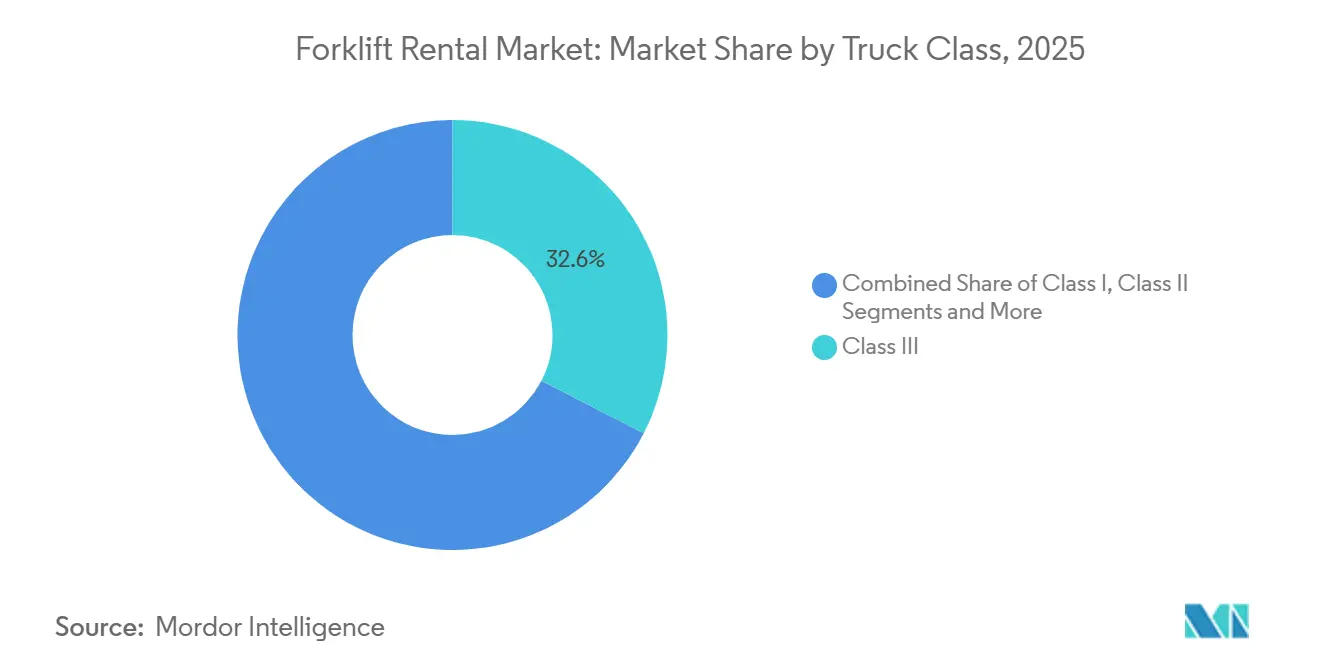

- By truck class, Class III electric hand trucks led with 32.56% revenue share in 2025; Class II narrow-aisle equipment is advancing at a 9.10% CAGR.

- By end-use industry, warehousing and logistics accounted for 38.67% of the forklift rental market size in 2025, while e-commerce warehousing is projected to grow at an 11.70% CAGR.

- By geography, the Asia-Pacific region dominated with a 37.65% revenue share in 2025, growing at a 10.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Forklift Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Fulfillment Boom | +1.8% | Global, Asia-Pacific core, North America leading | Medium term (2-4 years) |

| Shift to Opex Budgets | +1.5% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Accelerated Warehouse Automation | +1.2% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Emission Rules Phasing Out ICE Trucks | +1.0% | North America (California) and EU Stage V regions | Long term (≥ 4 years) |

| AI-Driven Fleet Optimization | +0.6% | North America and Europe, early Asia-Pacific adoption | Short term (≤ 2 years) |

| OEM Subscription Models | +0.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfillment Boom

Amazon's extensive global fulfillment network and DHL's significant investment in automation are driving rental fleets to expand during peak periods, making variable-cost agreements more favorable compared to ownership [1]“Global Operations Footprint,”, Amazon, aboutamazon.com. The Asia-Pacific region is expected to witness substantial growth in warehouse space, with notable contributions from emerging markets. Fluctuations in parcel volumes at last-mile hubs are increasing the demand for flexible capacity solutions. Rental operators are addressing this by offering compact electric models that can operate efficiently in narrow aisles while maintaining high lifting capabilities. The rapid growth of e-commerce continues to shape the development of the forklift rental market over the planning horizon.

Shift from Capex to Opex in Material-Handling Budgets

The Equipment Leasing and Finance Association noted a notable rise in the financing and leasing of material-handling equipment in the United States, reflecting a shift from traditional patterns[2]“2024 Survey of Equipment Finance Activity,”, Equipment Leasing and Finance Association, elfaonline.org. Finance leaders are increasingly turning to rentals to mitigate risks associated with depreciation and residual value. This strategy ensures access to the latest technology as advancements like electric and hydrogen drives replace older diesel models. In industries such as automotive and consumer electronics, where order cycles are unpredictable and production schedules frequently change, ownership is often not a cost-effective solution. Moreover, rental agreements transfer maintenance responsibilities to lessors, aligning with regulatory recertification requirements and helping operators reduce expenses. The forklift rental market is further bolstered by multi-site 3PLs adopting master agreements that ensure consistent rates and service quality.

Emission Regulations Phasing-Out Class IV/V ICE Trucks

California plans to ban the sale of new Class IV and V internal-combustion forklifts and gradually phase them out in large warehouses [3]“Zero-Emission Forklift Regulation,”, California Air Resources Board, ww2.arb.ca.gov. In the European Union, stricter standards are increasing compliance costs for diesel models. Lithium-ion batteries are becoming the dominant power source for new electric forklifts in North America and Europe. Rental companies are accelerating the replacement of their internal-combustion engine fleets to align with upcoming regulations and mitigate financial risks. The combination of decreasing battery costs and regulatory clarity is driving the growing preference for electric forklifts in the rental market.

AI-driven Fleet-Optimization Software Adoption

Rental firms now utilize real-time data from cloud dashboards to monitor utilization, battery health, and collision alerts. This capability enables them to quickly re-route idle units, leading to significant reductions in logistics costs. The deployment of telematics solutions has enhanced asset productivity across rental fleets. Additionally, analytics support a pay-per-use billing model, appealing to customers who prefer flexible pricing during periods of lower demand. Early adopters in industries such as grocery distribution and automotive manufacturing have reported significant cost savings, which has encouraged broader adoption. AI integration further strengthens the forklift rental market's position as a flexible and insight-driven resource.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical Construction Spend | -1.1% | Global, with pronounced impact in North America and Europe | Short term (≤ 2 years) |

| Tight Labor Pool for Forklift Operators | -0.8% | North America and Europe primarily | Medium term (2-4 years) |

| Rising Lithium-Ion Raw Material Costs | -0.6% | Global, with supply chain concentration in Asia-Pacific | Medium term (2-4 years) |

| OEM Direct Leasing Cannibalizes Rental Fleets | -0.4% | Global, with stronger impact in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyclical Construction Spending

Fluctuations in the construction industry directly influence the demand for forklift rentals, leading to unpredictable revenue streams for rental companies. Recently, the construction equipment market experienced mixed results, with a major player reporting a decline in revenue due to reduced sales volumes and a drop in equipment sales to end users. However, the outlook for the near future indicates a potential rebound in construction equipment sales, supported by improving economic conditions and easing interest rates. Additionally, significant federal investments in infrastructure projects are expected to provide stability, with a notable portion of contractors already engaged in these initiatives. Despite this support, rental companies continue to face challenges such as project delays and rising material costs, which remain a significant concern for many firms. The cyclical nature of construction spending often results in periods of surplus rental inventory, as reflected in the recent slowdown in rental revenue growth, marking one of the weakest performances in recent times.

OEM Direct-Leasing Cannibalizing Independent Rental Fleets

As manufacturers implement captive programs, independent dealers lose access to new equipment at factory pricing and must purchase at higher costs, reducing their profit margins. Larger independents secure favorable agreements through higher purchase volumes, but smaller regional players face challenges such as potential market exit or consolidation. While this approach increases rental adoption among end-users, it also shifts revenue distribution, adding strategic challenges within the forklift rental market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Load Capacity: Compact Units Gain in Dense Urban Warehouses

The 3.6 to 10 ton bracket captured 45.37% of 2025 revenue, affirming its versatility across production, logistics, and construction operations. In contrast, sub-3.5-ton forklifts are on track for a 10.67% CAGR to 2031, supported by land-scarce cities where narrow aisles and high racks dominate facility design. In major urban centers, as vertical storage increases, warehouses are increasingly adopting compact electric forklifts. These forklifts are designed to achieve significant lift heights while efficiently navigating through narrow corridors. Additionally, advanced battery technologies enhance the economic viability for rental fleets, leading to lower overall lifecycle costs.

As urban areas become increasingly densely populated, the demand for compact forklift rentals is expected to grow at a faster pace compared to other categories. Telematics technology enables lessors to optimize forklift rotation, ensuring efficient servicing of quieter locations while maintaining readiness in high-demand areas. Secondary markets, including industrial facilities, still show a preference for larger machines, with rental adoption remaining limited due to the need for specialized equipment ownership. This trend highlights the forklift rental market's shift towards more agile and environmentally friendly assets, with compact electric models driving this transformation.

By Rental Duration: Short-Term Flexibility Drives Current Demand

Short-term rentals with durations of less than 12 months accounted for 64.73% of revenue in 2025, primarily driven by construction and seasonal logistics. However, deals longer than 12 months now post an 8.50% CAGR as large 3PLs execute multi-site agreements that standardize fleet specs and service levels. A significant portion of material-handling leases now spans longer durations. Extended tenures enable lessors to amortize acquisition costs over a longer period, thereby reducing monthly rates without compromising returns.

Flexible rental options enable customers to exit with short notice after the initial period, striking a balance between predictability and agility. Contractors likewise stretch average rental periods as bundled deals simplify billing and unlock volume discounts. As a result, the forklift rental market size attributable to long-term contracts continues to expand, though short-term demand remains vital for project-specific peaks.

By Power Source: Electric Dominance Accelerates Under Emission Mandates

Electric forklifts secured 54.39% forklift rental market share in 2025 and exhibit an 11.89% CAGR through 2031, bolstered by battery costs falling below USD 150/kWh and zero-emission rules in California and the EU. Major players in the forklift rental market are focusing on increasing the penetration of electric fleets, reflecting a significant shift in the dynamics of their fleets. Meanwhile, traditional power units are experiencing a steady decline in their residual values.

Although hybrid and hydrogen forklifts currently contribute minimally to revenue, pilot projects in industrial applications demonstrate their potential, particularly in operations requiring continuous uptime and rapid refueling. High infrastructure costs remain a challenge, but collaborations with industrial gas suppliers for localized hydrogen production could help address adoption barriers. Consequently, electric technology continues to dominate the forklift rental market outlook, while alternative powertrains gradually gain traction.

By Truck Class: Narrow-Aisle Units Surge as Warehouses Maximize Density

In 2025, Class III electric hand trucks and pallet jacks accounted for 32.56% of the rental revenue, catering to light loads and meeting the ever-present demands of retail. With urban warehouse rents on the rise, operators are shifting from wide-aisle setups to very-narrow configurations. This transition, boasting a CAGR of 9.10%, has spurred significant growth in Class II narrow-aisle models and markedly enhanced storage capacity. A prominent manufacturer introduced telematics-enabled Class II units, resulting in reduced downtime and extended lifespan.

Class I electric forklifts maintain their position in mid-range applications, while Class IV and V internal-combustion trucks face stagnation due to emission regulations. With tightening regulations, the forklift rental market for narrow-aisle electric forklifts is expected to surpass all other classes in the future.

By End-Use Industry: E-Commerce Warehousing Outpaces Broader Logistics

Warehousing and logistics generated 38.67% of 2025 demand, with the e-commerce subset climbing at 11.70% CAGR on the back of Amazon’s 750,000-robot network and DHL’s automation push. While construction remains a significant contributor to revenue, its growth has slowed due to a decline in project flows. Meanwhile, the automotive, food, and aerospace sectors collectively drive demand, with electric vehicle plants notably increasing the need for specialty forklifts designed for battery production lines.

Retail chains expand their forklift fleets during peak months, only to scale back significantly afterward. This trend underscores the growing preference for rentals over outright ownership. Additionally, while the pharmaceutical industry's cold-chain requirements are niche, they are experiencing notable growth. In summary, the forklift rental industry is closely tied to sectors that experience demand fluctuations or have stringent uptime requirements, underscoring the diverse range of end-use applications within the market.

Geography Analysis

The Asia-Pacific region commanded 37.65% of global revenue in 2025 and is expected to post a 10.28% CAGR through 2031. China's extensive warehouse pipeline and India's logistics completions are driving this surge. With high e-commerce penetration in China, rental fleets experience significant growth during major shopping events. Japan's introduction of new automated space highlights the integration of narrow-aisle electrics and telematics, addressing labor shortages and rising wages.

North America, led by the United States, contributes significantly to the revenue. The region's push for zero-emission deadlines is accelerating the shift to electric, supporting the growth of the forklift rental market. Meanwhile, Canada maintains a steady demand, particularly along key corridors.

Europe accounts for a substantial portion of the revenue, with leading countries driving the market. Regulatory changes are encouraging rental fleets to adopt electric options, despite the higher costs associated with them compared to traditional units. Dominant players in the region leverage extensive branch networks to serve pan-regional customers. South America and the combined areas of the Middle East and Africa, while contributing a smaller share, are experiencing notable growth. This is driven by expanding port logistics and ambitious infrastructure projects, which are boosting demand for specialty rentals.

Mordor Intelligence provides coverage of the forklift rental market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States, Indonesia, Saudi Arabia, South Korea, Brazil, and United Arab Emirates incorporating local coverage and market participation, as required.

Competitive Landscape

United Rentals, Sunbelt Rentals, Toyota Industries, Caterpillar, and Herc Rentals, the top five operators, command a significant share of the global revenue, indicating a moderate concentration in the forklift rental market. United Rentals operates a large fleet of forklifts, using its scale to secure factory-direct terms and promote aerial platforms. Sunbelt Rentals showcases a similar expansive reach. Meanwhile, OEM-captives like Jungheinrich's Full Flex and Caterpillar's Pay for Use are tightening their grip on the market, offering uptime guarantees bundled with telematics, thereby diminishing the share of independent players.

First movers, such as Plug Power, are eyeing the hybrid and hydrogen niches, collaborating with automotive plants to roll out pilot units. Digital platforms like BigRentz and Sunstate cater to price-sensitive clients, but their reliance on brokered fleets results in slimmer profit margins. Leaders in the industry are setting themselves apart through technology investments; for instance, Crown and Raymond's telematics have achieved notable reductions in downtimes and have facilitated dynamic pricing strategies. Additionally, to compete for procurement contracts with Fortune 500 companies, firms must meet baseline standards, such as ISO 9001 certification, and adhere to stringent OSHA compliance requirements.

Forklift Rental Industry Leaders

Caterpillar Inc

Crown Equipment Corporation

Sunbelt Rentals, Inc.

Toyota Industries Corporation

Combillift Depot

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Herc Rentals completed its USD 5.3 billion acquisition of H&E Equipment Services, outbidding United Rentals' previous USD 4.8 billion offer and combining Herc's USD 3.5 billion annual revenue with H&E's USD 1.5 billion to strengthen its position as the third-largest rental company in North America.

- January 2025: Crown Equipment announced the opening of a new company-owned sales and service location in Chesapeake, Virginia, United States. The Crown Lift Trucks facility, situated at 551 Woodlake Circle, aims to support regional customers seeking enhanced productivity and uptime.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the forklift rental market as the annual revenue earned from short- and long-term operating leases of self-propelled industrial trucks, counterbalance, warehouse, very narrow aisle, and rough-terrain, supplied by rental specialists or OEM-affiliated dealers to end users in warehousing, manufacturing, construction, retail, and allied sectors. Turnkey options that bundle maintenance and telematics support are included because lessees treat those fees as part of the rental charge.

Scope exclusion: Purchase finance, outright equipment sales, and used-unit refurbishment revenues are outside the study.

Segmentation Overview

- By Load Capacity

- Less Than 3.5 T

- 3.6 to 10 T

- More Than 10 T

- By Rental Duration

- Short-term (Less Than 12 months)

- Long-term/Contract (More Than 12 months)

- By Power Source

- Electric

- Internal Combustion (Diesel/LPG)

- Hybrid/Hydrogen

- By Truck Class

- Class I – Electric Rider

- Class II – Narrow-Aisle

- Class III – Electric Hand

- Class IV – ICE Cushion

- Class V – ICE Pneumatic

- By End-use Industry

- Warehousing and Logistics

- Construction

- Automotive

- Food and Beverage

- Aerospace and Defense

- Others (Retail, Pharma, etc.)

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Egypt

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with rental fleet managers, OEM leasing directors, e-commerce fulfillment engineers, and logistics association advisors across North America, Europe, and Asia Pacific helped validate average utilization hours, residual value trends, and emerging contract preferences. These discussions closed data gaps left by desk work and guided assumption ranges used in the model.

Desk Research

Mordor analysts first gathered macro and sector inputs from publicly available authorities such as the American Rental Association, Eurostat industrial output series, United Nations Comtrade forklift HS codes, and warehouse construction permits logged by the U.S. Census. Company 10-Ks, investor decks, and trade-press price lists supplemented fleet size and average daily rate indicators. Paid databases, notably D&B Hoovers for renter balance sheets and Volza for shipment flows, offered deeper calibration. The sources cited here are illustrative; many additional references were mined to cross-check figures and narrative cues.

Market-Sizing & Forecasting

A top-down construct converts national forklift stock, replacement cycles, and rental penetration rates into demand pools, which are then reconciled with sampled average daily price multiplied by utilization roll-ups from bottom-up checks. Key variables include e-commerce parcel volume, warehouse floor space additions, industrial production growth, lithium-ion battery cost index, typical rental duration, and fleet utilization hours. Multivariate regression with an ARIMA overlay projects each driver to 2030; scenario bands adjust for regulatory zero-emission mandates and construction spending shifts. Where sampled ASP data were sparse, median regional rates were imputed using price dispersion observed in primary calls.

Data Validation & Update Cycle

Outputs pass three-step variance scans, peer review, and senior analyst sign-off. Models refresh annually, with interim tweaks triggered by material events, large stimulus bills, emission rule changes, or sizable M&A, so clients receive the latest vetted view.

Why Our Forklift Rental Baseline Commands Reliability

Published figures often diverge because firms vary scope, base year, currency conversion, and refresh cadence.

Key gap drivers include whether refurbished equipment is counted, the mix of contract services folded into revenue, and the rigor of primary validation against fleet utilization signals. Mordor's disciplined segmentation, annual refresh, and dual-approach modeling keep our baseline balanced and transparent.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.39 B (2025) | Mordor Intelligence | - |

| USD 6.39 B (2025) | Global Consultancy A | Includes truck-leasing and ancillary service fees; limited interview backing |

| USD 10.3 B (2023) | Industry Intelligence B | Counts refurbishment revenue and uses earlier base year without inflation rebasing |

| USD 15.6 B (2033) | Market Analytics C | Long-range projection assumes constant fleet utilization and broader equipment classes |

These contrasts show that Mordor's tighter scope, fresher base year, and verified assumptions furnish decision-makers with a dependable, reproducible market starting point.

Key Questions Answered in the Report

How big is the forklift rental market in 2026?

The forklift rental market size is USD 5.39 billion in 2026 and is projected to reach USD 7.35 billion by 2031.

What is the expected growth rate through 2031?

The market is forecast to advance at a 6.39% CAGR over the 2026–2031 period.

What segment is growing quickest by load capacity?

Units below 3.5 tons are advancing at a 10.67% CAGR due to narrow-aisle warehouse designs in urban areas.

How are rental companies using technology to stay competitive?

How are rental companies using technology to stay competitive?

Page last updated on: