Brazil Cloud Computing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

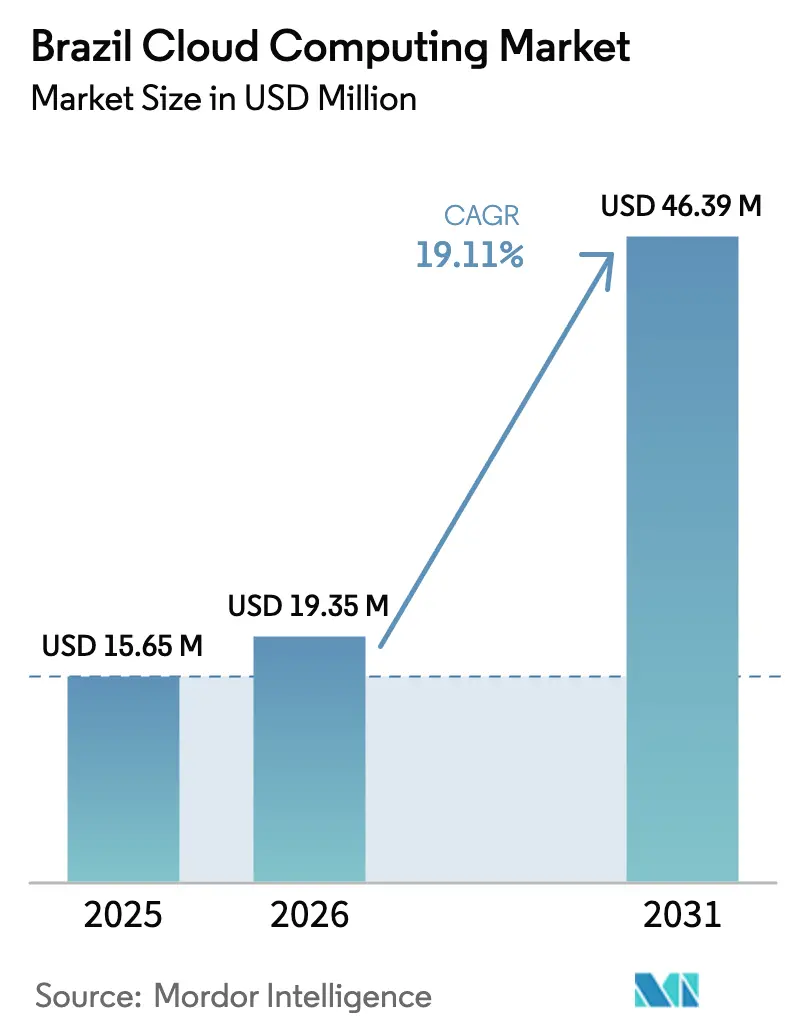

| Base Year Market Size (2025) | USD 15.65 Million |

| Market Size (2026) | USD 19.35 Million |

| Market Size (2031) | USD 46.39 Million |

| Growth Rate (2026 - 2031) | 19.11% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Cloud Computing Market Analysis by Mordor Intelligence

The Brazil cloud computing market size is expected to grow from USD 15.65 million in 2025 to USD 19.35 million in 2026 and is forecast to reach USD 46.39 million by 2031 at a 19.11% CAGR over 2026-2031. Public procurement reforms under the federal E-Digital strategy are steering ministry and agency workloads toward hyperscale regions, while FinTech unicorns and neobanks scale their transaction engines on elastic infrastructure to handle Pix payment spikes. Multinational manufacturers, retailers and energy majors headquartered in São Paulo and Rio de Janeiro are modernizing resource-planning and customer platforms to shorten product cycles and personalize commerce. Hyperscale operators continue to lower network latency through fresh availability zones and edge nodes in Brasília, Belo Horizonte and Fortaleza, and this dispersion is widening regional access to advanced analytics and AI services. Currency depreciation of the Brazilian Real against the U.S. Dollar remains a structural headwind, compressing reseller margins and prompting cost-optimization projects that favour hybrid deployment models.

Key Report Takeaways

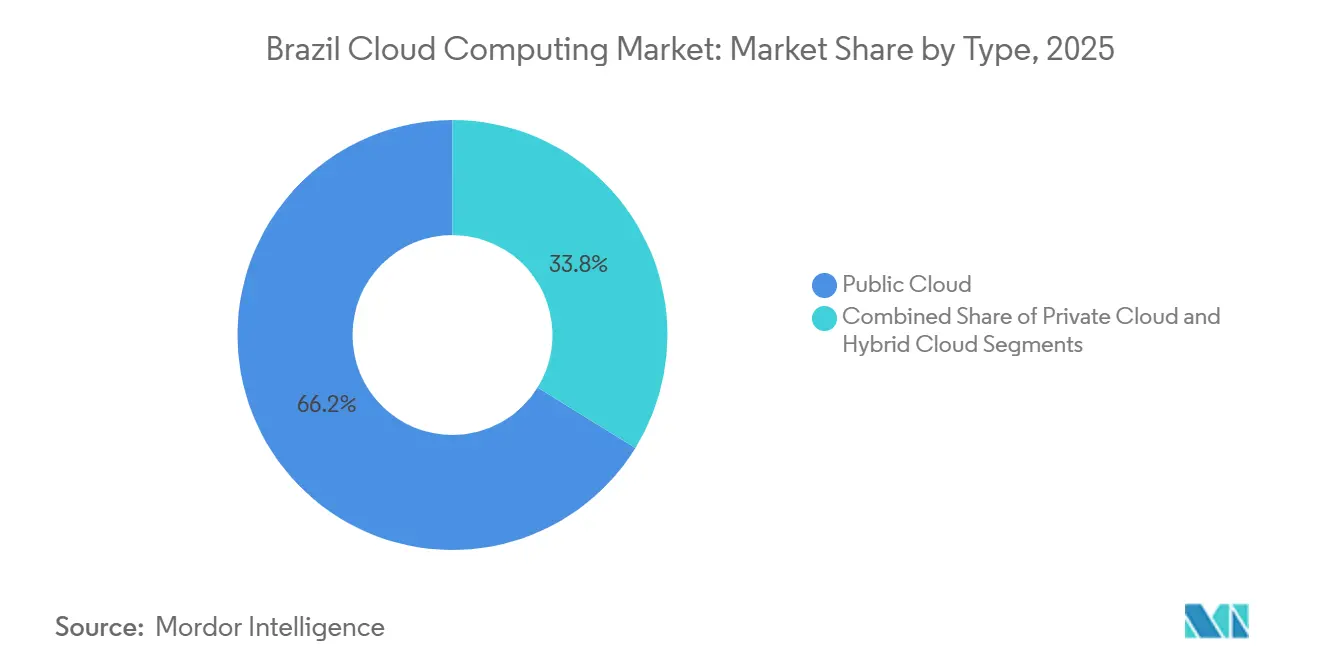

- By type, public cloud led with 66.19% revenue share in 2025, while hybrid cloud is advancing at a 19.78% CAGR through 2031.

- By organization size, large enterprises captured 72.41% of the Brazil cloud computing market share in 2025, whereas small and medium-sized enterprises are expanding at a 19.91% CAGR to 2031.

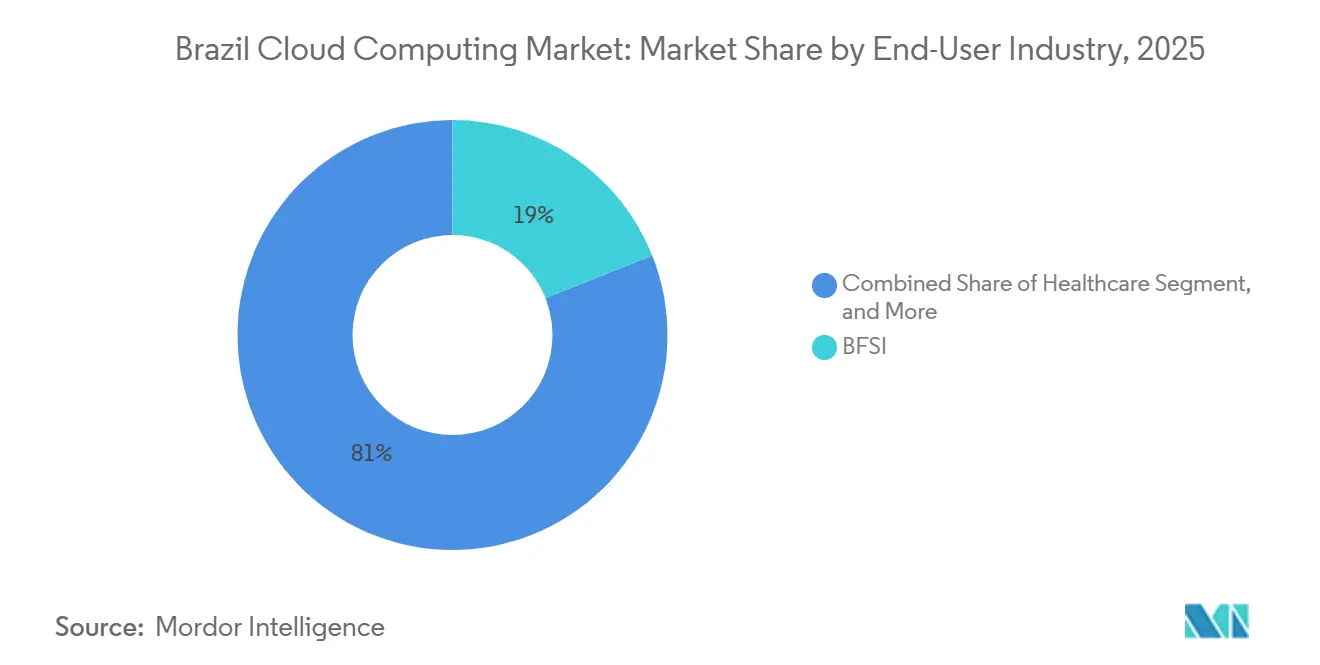

- By end-user industry, banking, financial services and insurance accounted for 18.98% of spending in 2025, and healthcare is forecast to grow at a 20.06% CAGR to 2031.

- By workload, business and productivity applications commanded 34.59% of usage in 2025, but analytics and artificial intelligence workloads are rising at a 22.48% CAGR.

- By geography, the Southeast held a 55.63% share of value in 2025, while the Northeast is projected to climb at a 22.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide industry scale is not derived from any single country or region but from the combination of national and regional inputs. The cloud computing market size of Mordor Intelligence integrates these into one global valuation.

Brazil Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Digitalization of Brazilian Enterprises | +5.20% | National, with concentration in Southeast and South | Medium term (2-4 years) |

| Surge in Hyperscale Data Center Investments | +4.80% | Southeast, expanding to Northeast | Short term (≤ 2 years) |

| Federal E-Digital Cloud-First Mandate | +3.90% | National, led by federal agencies in Brasília | Medium term (2-4 years) |

| FinTech Boom Demanding Scalable Infrastructure | +3.10% | Southeast urban centers, spillover to Center-West | Short term (≤ 2 years) |

| AI and Generative AI Workload Acceleration on Cloud | +2.70% | Southeast and South, early adoption in tech hubs | Long term (≥ 4 years) |

| Regional Edge-Cloud Roll-outs for Latency-Sensitive Applications | +2.20% | Northeast coastal cities, North logistics corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Digitalization of Brazilian Enterprises

Enterprises in manufacturing, retail and utilities are moving resource-planning, CRM and supply-chain applications to the Brazil cloud computing market in order to reduce capital outlays and shrink product launch cycles.[1]Deloitte, “2025 Digital Transformation Survey - Brazil,” DELOITTE.COM A 2025 transformation survey recorded that 72% of firms boosted cloud budgets to support remote work and omnichannel commerce after pandemic disruptions. Automotive assemblers now run cloud-based logistics dashboards that reroute components when port congestion threatens just-in-time inventories, slashing idle time across Mercosur corridors. National retailers synchronize point-of-sale feeds with cloud analytics engines, generating real-time price recommendations that lifted conversion by 15-20% in Grupo Pão de Açúcar pilot stores.[2]Grupo Pão de Açúcar, “Annual Report 2025,” GPABR.COM Because legacy mainframes cannot expose modern APIs, refresh cycles have tightened from seven to three years, and CIOs cite integration agility as the prime catalyst for cloud migration.

Surge In Hyperscale Data Center Investments

More than USD 2 billion in new hyperscale capacity is flowing into the Brazil cloud computing market between 2024 and 2026. Google committed USD 1.2 billion to its three-zone São Paulo region, targeting media streaming and capital-markets clients that need sub-10 millisecond roundtrips.[3]Google Cloud, “Google Cloud Announces USD 1.2 Billion Investment in Brazil,” CLOUD.GOOGLE Microsoft added GPU clusters to Azure São Paulo in March 2025 to serve generative AI training for imaging start-ups and agritech vision models.[4]Microsoft Azure, “Azure Expands São Paulo Region with GPU Clusters,” AZURE.MICROSOFT.COM Domestic operator Scala raised USD 450 million to build facilities in Fortaleza and Salvador, positioning itself near subsea cable landings that cut latency to North America and Europe. New capacity trims data-egress fees and catalyses adoption of bandwidth-hungry workloads such as video conferencing, IoT telemetry and 8K streaming.

Federal E-Digital Cloud-First Mandate

The updated 2024 E-Digital strategy obliges every new federal project to consider cloud architecture before on-premises alternatives, reinforcing demand for compliant hyperscale and sovereign platforms. Economy-ministry guidelines issued in January 2025 instruct agencies to adopt ISO 27017 controls and present total-cost comparisons. SERPRO had migrated 40% of its portfolio to hybrid cloud by December 2025, including Brazil’s tax-filing engines now hosted on Oracle Cloud, which processes 180 million submissions each year. State portals in São Paulo and Minas Gerais leverage serverless functions that auto-scale during annual vehicle-registration peaks, highlighting how policy has become a demand engine for the Brazil cloud computing market.

FinTech Boom Demanding Scalable Infrastructure

More than 1,200 FinTechs surfaced by 2025, and each hinges on elastic infrastructure to withstand transaction bursts during promotional events and Pix adoption waves. Nubank processes 1.2 billion daily API calls on AWS and trebles capacity during Black Friday without idle hardware costs. Stone Co reduced false-positive fraud flags by 35% after shifting models to Google Vertex AI in 2024. Open-banking rules announced by the Central Bank in 2024 mandate interoperable APIs across 700 banks, stimulating uptake of integration platforms that reside in the Brazil cloud computing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Sovereign-Cloud and Data-Residency Costs | -3.40% | National, acute in regulated sectors | Short term (≤ 2 years) |

| Acute Shortage of Cloud-Certified Talent | -2.90% | National, severe in secondary cities | Medium term (2-4 years) |

| Persistent Macroeconomic Currency Volatility | -2.10% | National, export-dependent sectors | Short term (≤ 2 years) |

| Legacy On-Premises Lock-ins within State-Owned Firms | -1.80% | Federal and state enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Sovereign-Cloud and Data-Residency Costs

Lei Geral de Proteção de Dados Pessoais obliges banks and insurers to host customer information in-country, raising infrastructure bills by 20-30% relative to multi-region deployments. A 2025 PwC assessment found compliance overhead tacked 12-18 months onto migration timelines for highly regulated enterprises. The data-protection authority issued 14 penalties in 2025 for unauthorized cross-border transfers, prompting risk-averse firms to split storage across on-premises and sovereign-cloud zones. Local providers including Locaweb market “never leaves Brazil” guarantees, yet the fragmentation prevents hyperscalers from exploiting global scale efficiencies, dampening price competition in the Brazil cloud computing market.

Acute Shortage of Cloud-Certified Talent

Brazil operated with a 70,000-person deficit in cloud architects in 2025, inflating senior salaries by 18% year-over-year. University syllabi trail practice in Kubernetes, infrastructure-as-code and FinOps. AWS added Portuguese training modules across 15 campuses in 2024, but the graduate pipeline needs several years to mature. SMEs in Recife and Goiânia rely on external consultants who command premium day rates, extending project timelines. The talent gap pushes enterprises toward managed services, yet it also caps consumption of advanced serverless and machine-learning features inside the Brazil cloud computing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hybrid Architectures Balance Sovereignty and Flexibility

Hybrid deployments accounted for a growing slice of the Brazil cloud computing market size as institutions combine on-premises cores with multi-cloud edges. In value terms, public cloud still held 66.19% during 2025, but hybrid is charted to increase faster because Central Bank auditors require retention of certain transactional datasets on local metal. Banks such as Itaú Unibanco maintain proprietary São Paulo data centers while bursting customer-facing mobile workloads onto AWS, a pattern repeating across insurance, telecom and utilities. Private cloud persists inside state-owned oil and power majors where procurement law favours dedicated stacks, yet those same firms piggyback Azure Arc to extend Kubernetes controls beyond their fences, underscoring the maturing sophistication of Brazil cloud computing market participants.

Microsoft’s Azure Arc lets manufacturers export container management to field plants while keeping sensor data resident for latency reasons, an enabler for Industry 4.0 cells on automotive floors. Telecom operators bundle private 5G with managed edge nodes to furnish mining and farming conglomerates with sub-5 millisecond compute, and government agencies run confidential citizen modules on sovereign zones while adopting cloud-native analytics for open-data dashboards. Platform-as-a-Service traction grows among software vendors who prize consistent CI/CD chains over virtual-machine lift-and-shift, signalling an evolution beyond raw IaaS toward higher-order abstractions throughout the Brazil cloud computing market.

By Organization Size: SMEs Close the Digital Gap

Large enterprises generated 72.41% of revenue in 2025 thanks to complex multi-cloud programs and GPU-heavy AI research, yet small and medium-sized enterprises are closing the gulf. SEBRAE incentives and subscription pricing let family-run manufacturers spin up ERP or e-commerce stacks without capex hurdles. Brazilian SaaS champions TOTVS and Linx now deliver retail management suites from multi-tenant clusters, quadrupling user onboarding velocity and lowering maintenance overhead. The Brazil cloud computing market size for SMEs is widening as Shopify and Nuvemshop add thousands of merchants each month, bundling inventory, payment and shipping APIs behind turnkey dashboards.

Meanwhile, conglomerates continue to dictate absolute dollars, running distributed machine-learning labs and high-fidelity digital twins. Banco Bradesco orchestrates cost governance across AWS, Azure and Google to prevent shadow IT, exemplifying the FinOps maturity possible at scale. Large miners simulate ore flows with GPU clusters, and media titans leverage multi-CDN routing for live streaming. Nevertheless, tooling vendors are surfacing simplified cost and compliance modules so that SMEs can exploit the same advanced levers, signalling longer-term democratization across the Brazil cloud computing market.

By End-User Industry: Healthcare Leads Growth Curve

Telehealth surges and electronic health record updates push healthcare to a 20.06% CAGR, the fastest within the Brazil cloud computing market. Platforms like Dr. Consulta leverage resilient video consult infrastructure and secure prescription workflows that scale nationally. Hospitals adopt cloud Picture Archiving and Communication Systems, enabling AI-assisted diagnostics that cut interpretation time by up to 40%. Pharma firms upload clinical-trial data to interoperable repositories connected to the food and drug regulator’s portals, shortening drug-approval lags. The Ministry of Health’s Conecte SUS immunization ledger uses multi-zone replication to guarantee uptime during mass campaigns.

BFSI still captured 18.98% of the Brazil cloud computing market share in 2025 because digital wallets and instant payments force continuous scaling. Retail and e-commerce chains run omnichannel order systems in the cloud to orchestrate click-and-collect and last-mile logistics. Manufacturing adopts predictive quality analytics, while telecom operators simultaneously consume and resell cloud. Public-sector portals migrate under the E-Digital decree, and universities retain cloud learning suites beyond pandemic remote phases, all combining to broaden vertical diversification inside the Brazil cloud computing market.

By Workload: Analytics and AI Accelerate Value Creation

Analytics and AI comprised the swiftest workload cohort, advancing at 22.48% CAGR as firms pivot from descriptive dashboards to prescriptive forecasting. Retailers link sales, weather and social chatter in lake houses to recalibrate prices hourly. Banks deploy GPU-accelerated fraud models that inspect billions of signals per minute, and agribusiness monitors satellite imagery for yield predictions. Generative AI is emerging for contact-center scripts and marketing copy, a testament to cloud-delivered foundation-model APIs.

Conversely, business and productivity software still ruled 34.59% of 2025 workloads because email, collaboration and file sharing underpin distributed labour. Storage, backup and disaster recovery services replace tape libraries with eleven-nines durability promises. Dev/test and CI/CD pipelines accelerate agile releases, letting software teams ship features daily instead of quarterly. High-performance computing for energy reservoir simulation and media rendering adds further depth, cementing the Brazil cloud computing market as a multipurpose platform rather than a single-use utility.

Geography Analysis

The Southeast accounted for 55.63% of the Brazil cloud computing market size in 2025, with São Paulo alone representing roughly 40% thanks to the clustering of Fortune 500 lenders, manufacturers and technology start-ups. Dense fiber backbones, reliable power and proximity to subsea landings in Santos and Rio sustain hyperscaler build-outs, and a mature ecosystem of integrators accelerates adoption. Google’s third zone launch in São Paulo during November 2025 boosted regional GPU availability by 40%, giving financial, healthcare and media customers new capacity for AI experimentation.

Growth momentum is migrating northward, and the Northeast is on track for a 22.52% CAGR through 2031. Fortaleza and Recife market land and energy 20-30% cheaper than São Paulo while tapping trans-Atlantic cables, a combination that enticed Scala Data Centers to commit USD 200 million for a hyperscale campus. State incentives slash property and energy taxes for data-center investors, and hospitality, retail and smart-city pilots are early adopters of local edge nodes. Universities in Salvador stream HD lectures to rural municipalities via low-latency connections, reflecting inclusive digitalization of the Brazil cloud computing market.

The South region enjoys solid uptake within agribusiness and automotive clusters stretching from Curitiba to Porto Alegre, where suppliers sync factory sensors with regional edge clouds. Center-West cloud spend is buoyed by Brasília departments implementing the E-Digital doctrine along with soy and cattle exporters in Mato Grosso running precision-agriculture analytics. The North lags due to limited fiber, but edge deployments in Manaus are shrinking that gap for e-commerce order routing and streaming media, foreshadowing a broader diffusion of the Brazil cloud computing market across every Brazilian biome.

Mordor Intelligence tracks the cloud computing market across other major regions such as Asia, South America, and North America, with additional country-level coverage spanning Canada, United States, China, United Kingdom, Germany, and Italy, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Competitive intensity remains moderate as the top five hyperscale’s hold an estimated 60-65% of 2025 Infrastructure-as-a-Service and Platform-as-a-Service spend. Amazon Web Services retains first position through an early São Paulo foothold and the widest menu of compute, database and AI services. Microsoft Azure is leveraging Office 365 enterprise entrenchment by bundling credits and sovereign-cloud blueprints compliant with data-protection mandates, a tactic central ministries regard favourably. Google Cloud differentiates via industry-specific accelerators, such as its 2025 tie-up with media giant Globo to offload transcoding and CDN processing onto GCP infrastructure.

Domestic contenders Locaweb and TIVIT accentuate Portuguese support, local billing and hard residency guarantees, niches still valuable where legislation curbs cross-border transfers. Locaweb’s 2025 purchase of a managed Kubernetes platform extends its Platform-as-a-Service reach into mid-market independent software vendors. Systems integrators, consultancies and telecommunications operators are carving out value-added services that wrap migration, compliance and FinOps tooling around hyperscaler cores, absorbing as much as 30% of customer outlays. Patent filings by IBM and Oracle covering confidential computing and homomorphic encryption could recast security table stakes over the next cycle, potentially resetting buying criteria inside the Brazil cloud computing market.

Edge computing, multi-cloud observability and spend-optimization software stand out as viable white spaces. Emerging challenger Semantix positions a managed data-lakehouse stack for enterprises lacking data-engineering muscle, whereas telecom operators Vivo and Claro exploit 5G rollouts to furnish edge containers for streaming and industrial IoT. Competitive dynamics are thus shifting from raw capacity to differentiated managed experiences that tame complexity for both multinational majors and regionally anchored SMEs participating in the Brazil cloud computing market.

Brazil Cloud Computing Industry Leaders

Alibaba Group Holding Limited

Amazon Web Services (AWS)

Google LLC (Alphabet Inc.)

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Brazil’s federal government approved USD 433 million in financing for Serpro to modernize public-sector networks and reinforce the sovereign-cloud strategy.

- March 2025: Serpro reported BRL 3.93 billion net revenue and launched Government Cloud, signalling domestic viability in sovereign computing.

- February 2025: IBM closed its USD 6.4 billion HashiCorp acquisition, delivering advanced automation portfolios through Brazilian partners.

- February 2025: Utility Copel reached 1 million smart meters in Paraná, heightening demand for cloud analytics.

Brazil Cloud Computing Market Report Scope

The Brazil Cloud Computing Market Report is Segmented by Type (Public Cloud with IaaS, PaaS, and SaaS; Private Cloud; Hybrid Cloud), Organization Size (SMEs and Large Enterprises), End-User Industry (Manufacturing, Education, Retail and E-commerce, Transportation and Logistics, Healthcare, BFSI, Telecom and IT, Government and Public Sector, Utilities, Media and Entertainment), Workload (Business and Productivity Applications, Storage and Backup, Analytics and AI, Dev/Test and CI/CD, Disaster Recovery, Other Workloads), and Geography (Southeast, South, Northeast, Center-West, North). The Market Forecasts are Provided in Terms of Value (USD).

| Public Cloud | IaaS |

| PaaS | |

| SaaS | |

| Private Cloud | |

| Hybrid Cloud |

| SMEs |

| Large Enterprises |

| Manufacturing |

| Education |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Utilities, Media and Entertainment |

| Business and Productivity Applications |

| Storage and Backup |

| Analytics and AI |

| Dev/Test and CI/CD |

| Disaster Recovery |

| Other Workloads |

| By Type | Public Cloud | IaaS |

| PaaS | ||

| SaaS | ||

| Private Cloud | ||

| Hybrid Cloud | ||

| By Organization Size | SMEs | |

| Large Enterprises | ||

| By End-User Industry | Manufacturing | |

| Education | ||

| Retail and E-commerce | ||

| Transportation and Logistics | ||

| Healthcare | ||

| BFSI | ||

| Telecom and IT | ||

| Government and Public Sector | ||

| Utilities, Media and Entertainment | ||

| By Workload | Business and Productivity Applications | |

| Storage and Backup | ||

| Analytics and AI | ||

| Dev/Test and CI/CD | ||

| Disaster Recovery | ||

| Other Workloads |

Key Questions Answered in the Report

How fast is cloud spending growing in Brazil?

The Brazil cloud computing market is projected to expand from USD 19.35 million in 2026 to USD 46.39 million by 2031 at a 19.11% CAGR.

Which deployment model is adding users most rapidly?

Hybrid cloud is the fastest, advancing at a 19.78% CAGR as firms balance data-sovereignty mandates with multi-cloud flexibility.

Which sector will contribute the next wave of demand?

Healthcare leads with a forecast 20.06% CAGR through 2031, driven by telemedicine scaling and electronic health record modernization.

What is the biggest operational hurdle companies face?

A shortage of cloud-certified professionals inflates salaries and lengthens deployment timelines, especially outside São Paulo and Rio de Janeiro.

How are currency swings affecting adoption?

Real depreciation raises subscription bills denominated in USD, pressing resellers and prompting enterprises to optimize workloads for cost efficiency.

Page last updated on: