Indonesia Cloud Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

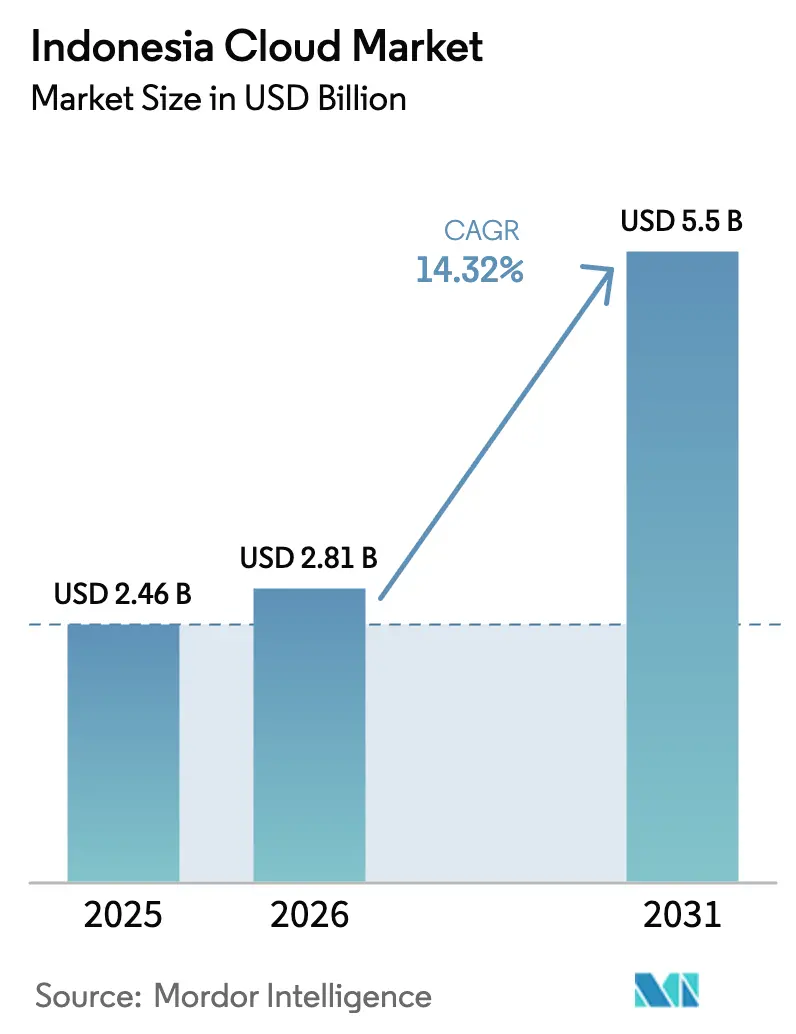

| Base Year Market Size (2025) | USD 2.46 Billion |

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 5.5 Billion |

| Growth Rate (2026 - 2031) | 14.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Cloud Market Analysis by Mordor Intelligence

The Indonesia cloud market size is expected to grow from USD 2.46 billion in 2025 to USD 2.81 billion in 2026 and is forecast to reach USD 5.5 billion by 2031 at 14.32% CAGR over 2026-2031. This expansion is propelled by sustained enterprise digital-transformation spending, large-scale hyperscaler capital expenditure, and government mandates under the Digital Indonesia 2025 framework. Public cloud retains leadership on the back of Java-centric infrastructure density, while hybrid architectures gain momentum as regulators tighten data-sovereignty rules. Sector-specific cloud platforms that combine AI and compliance functionality differentiate providers, and rising ESG targets push demand for renewable-powered data centers. Talent scarcity and escalating cyber-attack losses temper adoption velocity, but overall growth prospects remain intact as providers embed security-by-design and training initiatives into service portfolios.

Key Report Takeaways

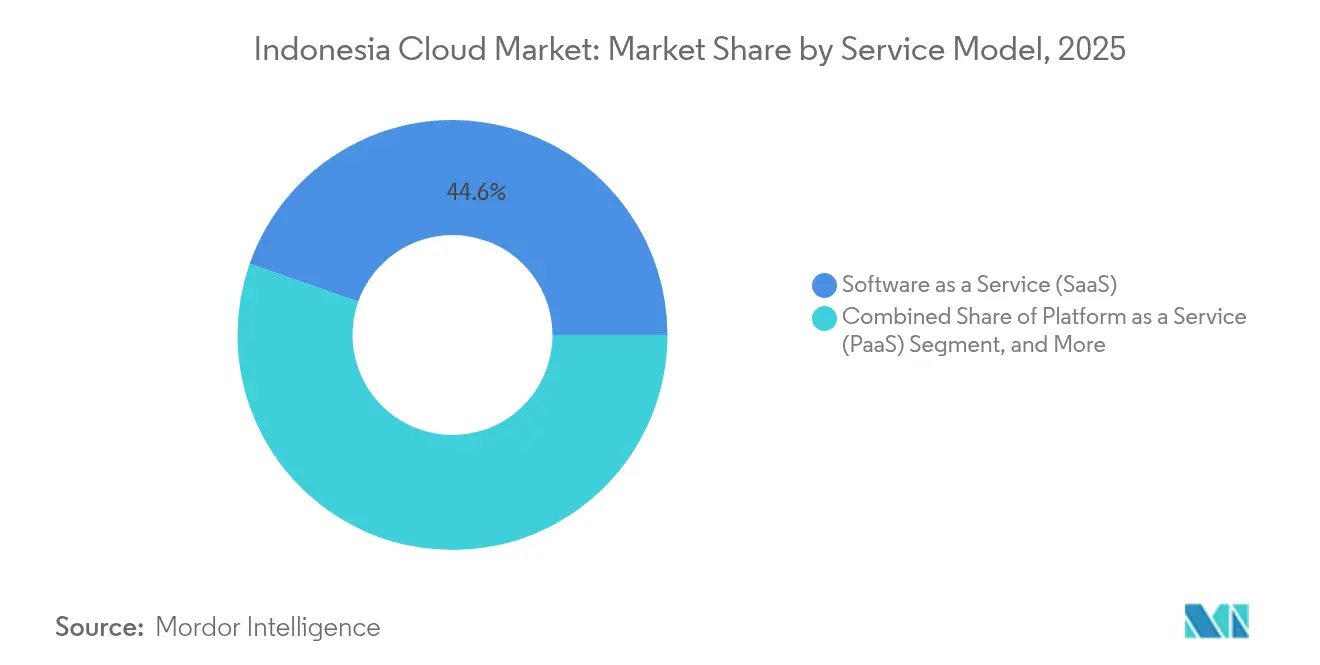

- By service model, Software as a Service led with 44.62% revenue share of the Indonesian cloud market in 2025, Platform as a Service is projected to expand at a 15.42% CAGR to 2031.

- By deployment model, public cloud accounted for 66.05% of the Indonesian cloud market share in 2025, while hybrid cloud recorded the highest projected CAGR at 15.21% through 2031.

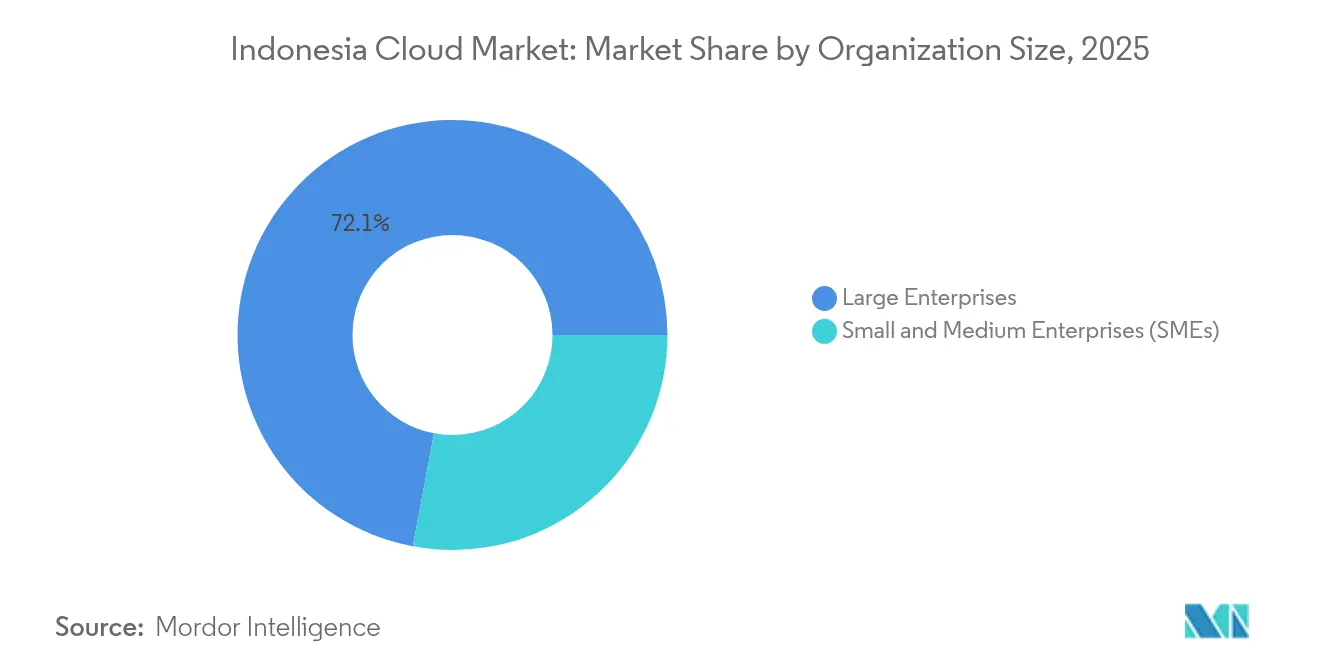

- By organization size, large enterprises commanded a 72.05% share of the Indonesian cloud market size in 2025, yet the SME segment is advancing at a 15.18% CAGR through 2031.

- By end-use industry, BFSI captured 27.32% of Indonesia's cloud market revenue in 2025, whereas healthcare and life sciences posted the fastest 15.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digital-transformation spend by enterprises | +3.2% | Java-centric with spillover to Sumatra, Kalimantan | Medium term (2-4 years) |

| Hyperscaler CAPEX on Indonesian data-centre regions | +2.8% | Java, Batam, with expansion to outer islands | Long term (≥ 4 years) |

| Government "Digital Indonesia 2025" and e-Gov push | +2.1% | National, with priority focus on underserved regions | Short term (≤ 2 years) |

| Surge in e-commerce/fintech cloud workloads | +1.9% | Java dominance, expanding to tier-2 cities | Medium term (2-4 years) |

| National Data Centre (PDN) enabling sovereign cloud | +1.5% | National infrastructure with regional data centers | Long term (≥ 4 years) |

| Renewable-powered 'green-cloud' demand from ESG-focused firms | +1.1% | Java, Sumatra with geothermal/solar integration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid digital-transformation spend by enterprises

Large corporations modernize core systems to defend market share against digital-native rivals. Microsoft’s USD 1.7 billion regional cloud plan and Oracle’s USD 6.5 billion Batam campus validate long-term demand. Multi-cloud adoption accelerates as GoTo partners concurrently with Alibaba Cloud and Tencent Cloud to balance pricing and resilience. [1]GoTo Group, “Alibaba and GoTo Group Announce Strategic Partnership,” gotocompany.com Telkom Indonesia’s alliance with Reka AI shows traditional firms embedding language-aware AI through Platform as a Service to improve customer interactions. Continuous innovation cycles elevate spend beyond one-off migrations, sustaining uptake of higher-margin cloud offerings. This dynamic cements SaaS leadership while igniting demand for DevOps-ready PaaS stacks.

Hyperscaler CAPEX on Indonesian data-center regions

Amazon’s USD 5 billion AI-cloud pledge, alongside Digital Realty’s USD 499 million Jakarta JV, reinforces confidence in multiyear workload growth. Investment clusters around low-latency corridors in Greater Jakarta and Batam, with renewable power procurement aligning ESG goals. Google Cloud’s BerdAIa program illustrates how regional capacity underpins ecosystem building for industry-specific AI. [2]Google Cloud, “Google Cloud Unveils Indonesia BerdAIa,” googlecloudpresscorner.com Hyperscalers accept decade-long payback profiles, signaling belief in Indonesia’s macro stability and regulatory clarity. Local colocation providers benefit via anchor-tenant demand, catalyzing secondary market development in second-tier cities.

Government Digital Indonesia 2025 and e-Gov push

Mandatory cloud-first rules for ministries plus the National Data Centre initiative spur immediate public-sector migrations. The UMKM Go Digital program, bringing 27 million SMEs online, expands downstream infrastructure consumption. Parallel grid expansions of 37 electricity projects totaling 3,222 MW improve power reliability for new data halls. Coordinated policy plus physical infrastructure raises the Indonesia cloud market growth ceiling, especially for hybrid offerings that match sovereignty needs.

Surge in e-commerce/fintech cloud workloads

Digital-economy value hit USD 90 billion in 2024 and could quadruple by 2030, multiplying compute and storage requirements. GoTo and Indosat’s generative-AI rollout underscores domain-specific model demand that favors local language processing. Crypto-tax reforms that waive VAT propel transaction volumes, further stressing fintech back-ends. E-commerce logistics firms like JNE adopt Alibaba Cloud DRaaS to assure uptime during sales peaks. Consequently, the Indonesian cloud market witnesses elevated Infrastructure as a Service usage, complemented by low-code PaaS for rapid fintech product launches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cybersecurity-breach costs | -1.8% | National, with highest impact on Java financial centers | Short term (≤ 2 years) |

| Complex data-localisation and sectoral compliance | -1.4% | National regulatory framework with sector-specific variations | Medium term (2-4 years) |

| Shortage of cloud-skilled talent and high wage inflation | -1.2% | Java concentration with spillover effects nationally | Medium term (2-4 years) |

| Inter-island power and fibre reliability gaps | -0.9% | Outer islands, particularly Papua, Maluku, eastern regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating cybersecurity-breach costs

A USD 8 million ransomware demand on the National Data Center shook enterprise confidence, pushing risk-averse sectors to delay migrations. [3]Kementerian Komunikasi dan Digital, “Komdigi Bekukan Izin Worldcoin dan WorldID,” komdigi.go.id New child online protection rules add additional security layers, increasing provider overhead. Financial institutions face punitive fines and reputational harm, tilting the market toward vendors with proven zero-trust frameworks. Heightened scrutiny may short-term curb Indonesia's cloud market uptake among late-adopting firms until providers showcase certified resilience programs.

Complex data-localization and sectoral compliance

While a 2025 trade accord softened some cross-border data rules, sector-specific regimes remain onerous. The 15% global minimum tax introduces new reporting duties for multinationals. Imminent AI regulation adds further uncertainty. Compliance cost burdens weigh heavier on niche PaaS and SaaS vendors, potentially slowing innovation and fragmenting the Indonesian cloud industry landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Model: SaaS entrenches while PaaS accelerates

Software as a Service accounted for 44.62% of the Indonesian cloud market in 2025 as firms opted for ready-to-run business applications with predictable OPEX. PaaS follows with the fastest 15.42% CAGR, reflecting developer demand for micro-services and container orchestration. Infrastructure as a Service underpins both, supplying elastic compute that smaller SaaS players lease rather than own. Disaster Recovery as a Service uptake spikes after high-profile outages, embedding resiliency into board-level risk agendas.

The Indonesian cloud market size for SaaS will widen as compliance-ready solutions gain traction in BFSI and healthcare. PaaS vendors differentiate on domain-specific APIs, such as Telkom DWS’s multimedia CPaaS suite. Local provider Lintasarta bundles OpenShift-based PaaS with backup vaults, meeting stringent localization rules. These integrated stacks protect margins against hyperscale price cuts, stabilizing competitive equilibrium.

By Deployment Model: Hybrid strategies rise

Public deployments captured 66.05% Indonesia cloud market share in 2025 due to immediate scalability and cost visibility. Hybrid architectures, however, post a 15.21% CAGR as firms blend on-premise or colocation nodes for latency-sensitive or regulated workloads. Private clouds remain niche, reserved for ultra-regulated setups in defense or critical infrastructure.

Hybrid growth stems from GoTo’s dual-provider play and Singtel-GMI’s pooled GPU project that share capacity across borders. Rollout of Wi-Fi 6E/7 enables site-to-cloud throughput up to 46 Gbps, supporting distributed architectures. The Indonesian cloud market size for hybrid solutions is forecast to compound as regulators mandate in-country data copies while boards demand multicloud resilience.

By Organisation Size: SME momentum builds

Large enterprises delivered 72.05% Indonesia cloud market revenue in 2025, leveraging scale to negotiate enterprise-grade SLAs. Yet the SME cohort charts 15.18% CAGR on the back of the UMKM Go Digital program and low-code SaaS billing models. Start-up resilience, with 65% of investors planning larger tickets through 2031, adds to SME demand trajectories.

Affordable bundles from IDCloudHost and Dewaweb target payroll, accounting, and storefront apps, removing upfront CAPEX. For providers, the long-tail SME pool diversifies revenue and dilutes concentration risk tied to a handful of conglomerates. Consequently, Indonesia's cloud market penetration deepens into rural and tier-2 cities as connectivity improves.

By End-Use Industry: Healthcare surges

BFSI preserved 27.32% share in 2025, anchored by open-banking obligations and real-time settlement rules. Yet healthcare and life sciences record a 15.66% CAGR as tele-consult platforms and electronic medical record mandates take hold. Manufacturing, retail, and transport harness supply-chain visibility apps, expanding horizontal cloud uptake.

Indonesia's cloud market size for healthcare will scale further once AI-driven diagnostics integrate with government insurance schemes. Energy utilities deploy IoT telemetry in line with the 69.5 GW renewable roadmap, feeding analytics workloads to regional data hubs. Sector diversification cushions providers against cyclicality in any single vertical, ensuring broad-based revenue streams.

Geography Analysis

Java anchors 58.7% of GDP and houses most hyperscale zones, giving it an outsized Indonesia cloud market share. Proximity to banking headquarters and fiber backbones trims latency, driving public-cloud offloads from legacy data rooms. Government electrification raised village coverage to 99.92%, extending cloud-readiness to peri-urban districts. Java’s dominance persists, but growth rates in outer islands now outpace as new zones come online.

Sumatra, Kalimantan, and Sulawesi inherit spill-over demand from mining and agribusiness digitization. Renewable build-out 76% of the 2025-34 capacity plan pitches these islands as green data-hub alternatives. Improved sea-cable redundancy narrows bandwidth gaps, allowing regional firms to adopt hybrid architectures without relocating compute to Jakarta.

Bali-Nusa Tenggara plus Papua-Maluku show niche uptake driven by tourism analytics and e-government portals. Oracle’s Batam investment illustrates how strategic free-trade zones can attract hyperscaler nodes outside Java. Continued subsidies for fiber and power back-haul remain critical to unlock full cloud potential across the archipelago, equalizing Indonesia's cloud market access.

Competitive Landscape

Indonesia cloud market competition blends hyperscale capital with local compliance agility. AWS, Microsoft, and Google extend regional zones and AI accelerators to capture enterprise modernization budgets. Alibaba Cloud and Tencent Cloud ride alliances with GoTo and other digital natives for traffic scale. Telkom Indonesia, Biznet Gio, DCI, and newcomer Lintasarta differentiate by local support, rupiah billing, and audited data residency.

Joint-venture models proliferate: Digital Realty pairs with Bersama Digital Infrastructure for a USD 499 million Jakarta campus, delivering neutral interconnectivity to all carriers. [4]Stock Titan, “Digital Realty Enters Indonesia…,” stocktitan.net XL Axiata-Smartfren’s USD 6.5 billion merger pools spectrum to propel 5G edge services nationwide. Indosat’s AI-RAN deployment with Nokia and NVIDIA showcases telco-cloud convergence that can offload radio workloads to regional clouds. Local specialists focus on DRaaS, GPU-as-a-Service, and sovereign PaaS niches, sustaining healthy fragmentation despite hyperscale weight.

Emerging battlegrounds center on sector-tuned SaaS, green-energy procurement, and managed security. Providers that bundle carbon reporting, threat intelligence, and compliance templates win share as tighter regulations loom. Still, the top five vendors combined control less than 60% of total revenue, leaving room for challenger entry in managed Kubernetes, edge caching, and AI model-hosting.

Indonesia Cloud Industry Leaders

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Alibaba Cloud (Alibaba Group Holding Limited)

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: GoTo Group and Indosat Ooredoo Hutchison launched Indonesia’s first home-grown generative AI service supporting local languages.

- June 2025: The Energy Ministry issued Regulation No. 10/2025 outlining a net-zero electricity roadmap.

- May 2025: Google Cloud introduced the BerdAIa co-creation program for enterprise AI solutions.

- May 2025: Digital Realty formed a 50-50 JV with Bersama Digital Infrastructure Asia for data-center development in Jakarta.

- February 2025: Indonesia launched Wi-Fi 6E and Wi-Fi 7, enabling 46 Gbps throughput.

- January 2025: President Prabowo inaugurated 37 electricity projects totaling 3,222 MW to support 8% growth target.

Indonesia Cloud Market Report Scope

Cloud technology refers to servers used over the Internet and the software and databases that operate on those servers. Cloud servers are placed in data centers all over the globe. Using cloud computing, users and businesses cannot handle physical servers or run software applications on their machines.

The Indonesia cloud market is segmented by type (public cloud (Saas, Paas, Iaas) and private cloud), by organization size (SMEs and large enterprises), by end user industry (IT and telecom, BFSI, retail and consumer goods, manufacturing, healthcare and life sciences, government, and other end user verticals), by region (Java, Sumatra, Kalimantan, and Other Regions). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Software as a Service (SaaS) |

| Platform as a Service (PaaS) |

| Infrastructure as a Service (IaaS) |

| Disaster-Recovery as a Service (DRaaS) |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Retail and Consumer Goods |

| Manufacturing |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Transportation and Logistics |

| Energy and Utilities |

| Other End-Use Industries |

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Bali and Nusa Tenggara |

| Papua and Maluku |

| By Service Model | Software as a Service (SaaS) |

| Platform as a Service (PaaS) | |

| Infrastructure as a Service (IaaS) | |

| Disaster-Recovery as a Service (DRaaS) | |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Organisation Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-Use Industry | IT and Telecom |

| BFSI | |

| Retail and Consumer Goods | |

| Manufacturing | |

| Healthcare and Life Sciences | |

| Government and Public Sector | |

| Transportation and Logistics | |

| Energy and Utilities | |

| Other End-Use Industries | |

| By Region | Java |

| Sumatra | |

| Kalimantan | |

| Sulawesi | |

| Bali and Nusa Tenggara | |

| Papua and Maluku |

Key Questions Answered in the Report

What is the forecast value of the Indonesia cloud market by 2031?

The market is projected to reach USD 5.5 billion by 2031, growing at a 14.32% CAGR.

Which cloud service model currently leads adoption in Indonesia?

Software as a Service leads with 44.62% revenue share in 2025.

Why are hybrid cloud architectures gaining momentum?

Enterprises seek to comply with data-sovereignty rules while preserving flexibility, driving hybrid deployments at a 15.21% CAGR.

Which vertical shows the fastest cloud spending growth?

Healthcare and life sciences posts the highest 15.66% CAGR through 2031 as telemedicine and digital health investments rise.

How is government policy influencing demand?

Digital Indonesia 2025 mandates cloud-first approaches and, coupled with nationwide power and connectivity upgrades, expands addressable demand.

What security challenges affect adoption?

A high-profile ransomware attack and stricter child-safety rules increase compliance costs, pushing firms toward providers with robust zero-trust frameworks.

Page last updated on: