Books Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

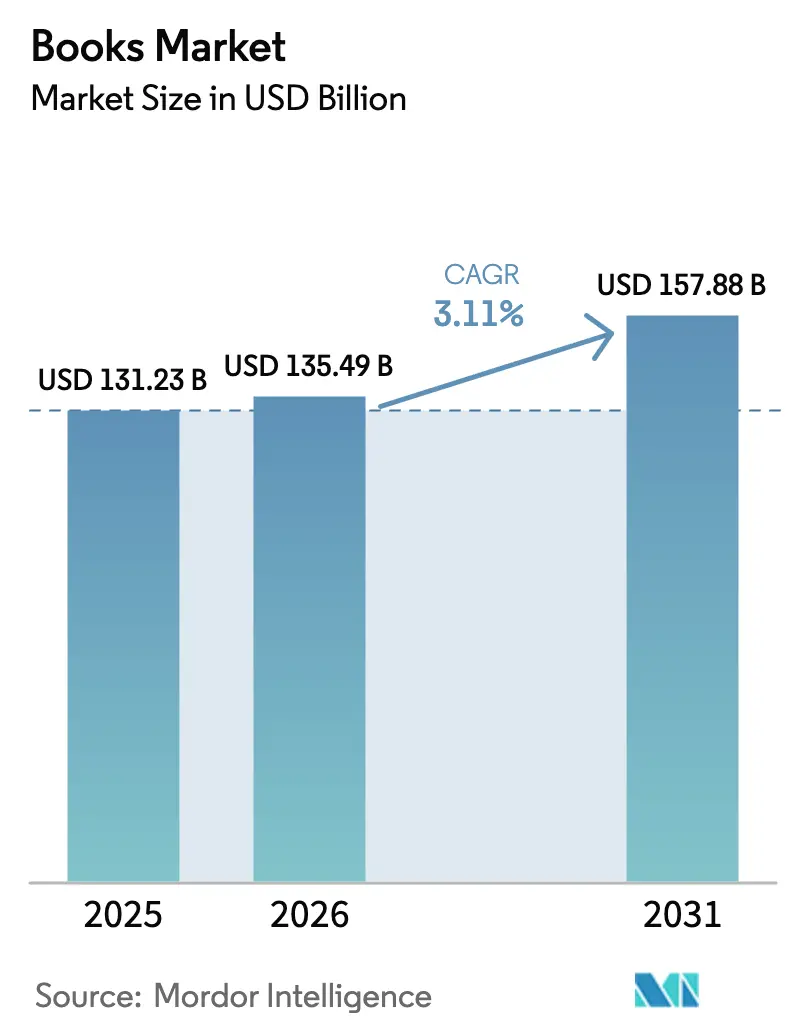

| Market Size (2026) | USD 135.49 Billion |

| Market Size (2031) | USD 157.88 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

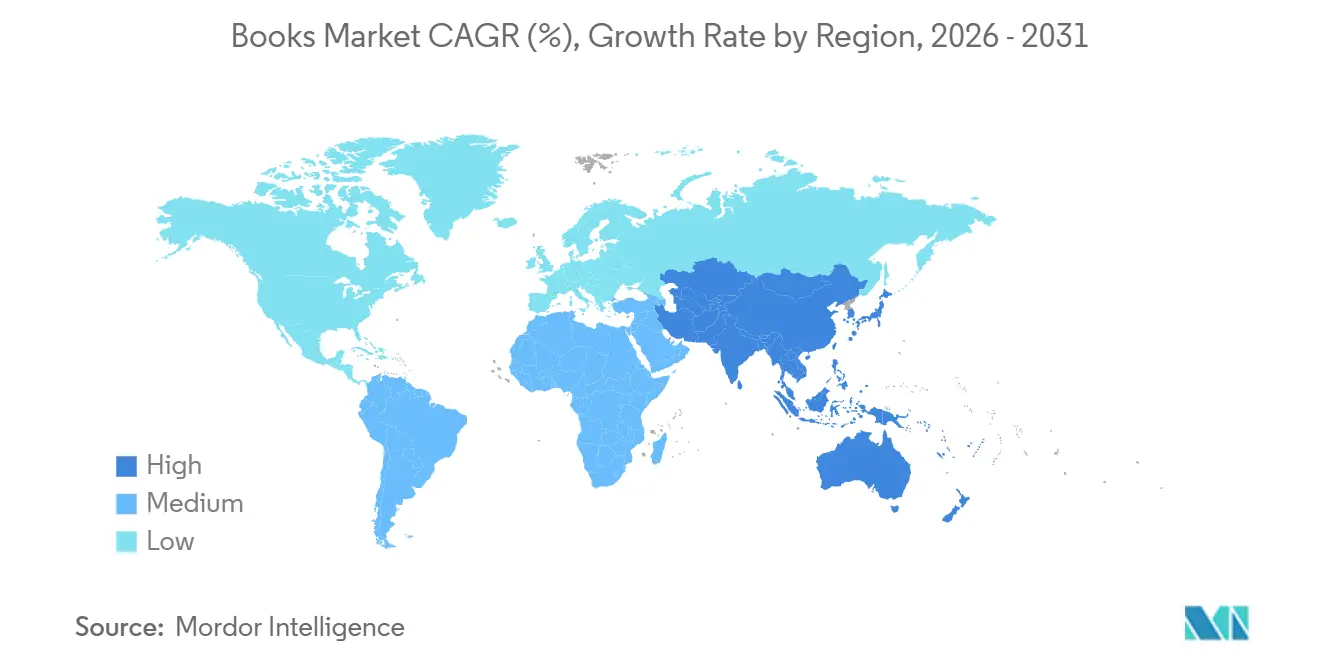

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Books Market Analysis by Mordor Intelligence

The Books Market size is expected to grow from USD 131.23 billion in 2025 to USD 135.49 billion in 2026 and is forecast to reach USD 157.88 billion by 2031, with a 3.11% CAGR over 2026-2031. Continued demand for printed titles, rapid adoption of audiobooks, and the rise of subscription reading platforms are shaping revenue prospects. Format preferences are fragmenting as commuters favor audio, younger readers adopt e-books, and collectors seek premium hardbacks. Publishers are sharpening omnichannel distribution, expanding direct-to-consumer storefronts, and experimenting with AI-enabled production to offset shrinking brick-and-mortar shelf space. Regionally, Asia-Pacific leads sales, the Middle East and Africa post the fastest growth, and Latin America benefits from government literacy drives. Across every region, piracy, paper shortage, and sand VAT inconsistencies temper momentum but also drive operational innovation.

Key Report Takeaways

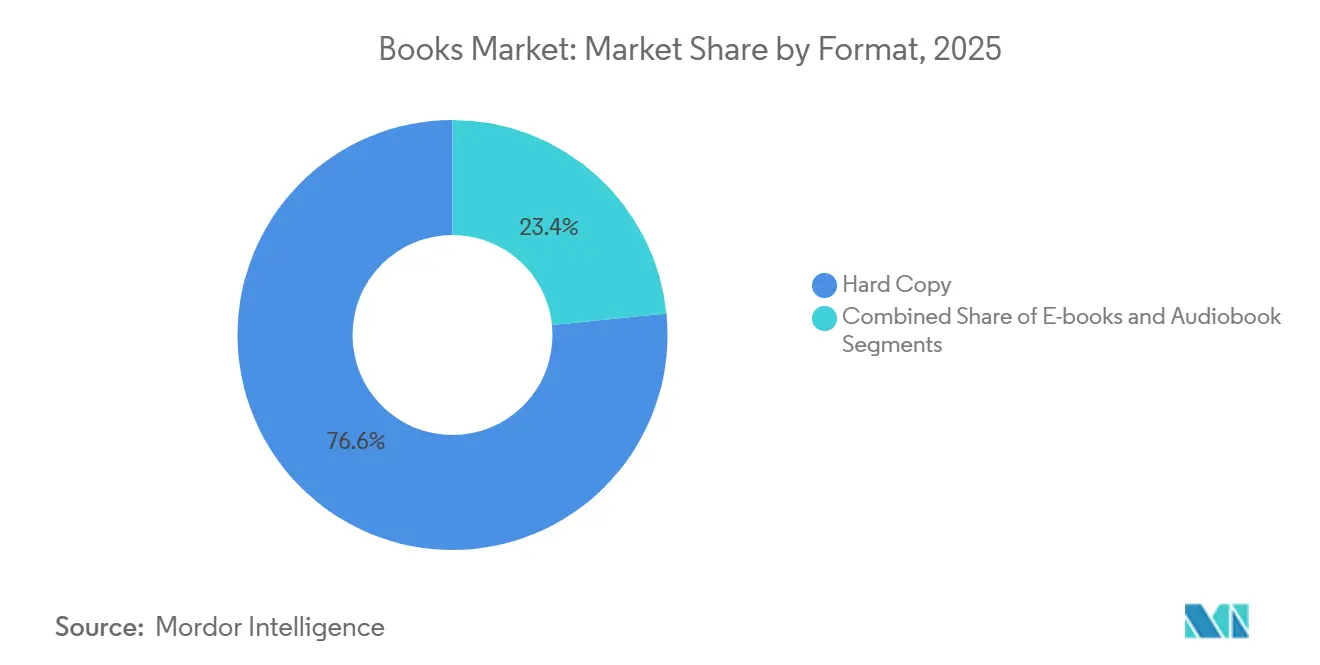

- By format, hard copy retained 76.59% of the book market share in 2025, while audiobooks are forecast to expand at 8.49% CAGR to 2031.

- By genre, fiction commanded a 33.26% share of the books market in 2025, and comics and graphic novels are projected to grow at a 4.81% CAGR through 2031.

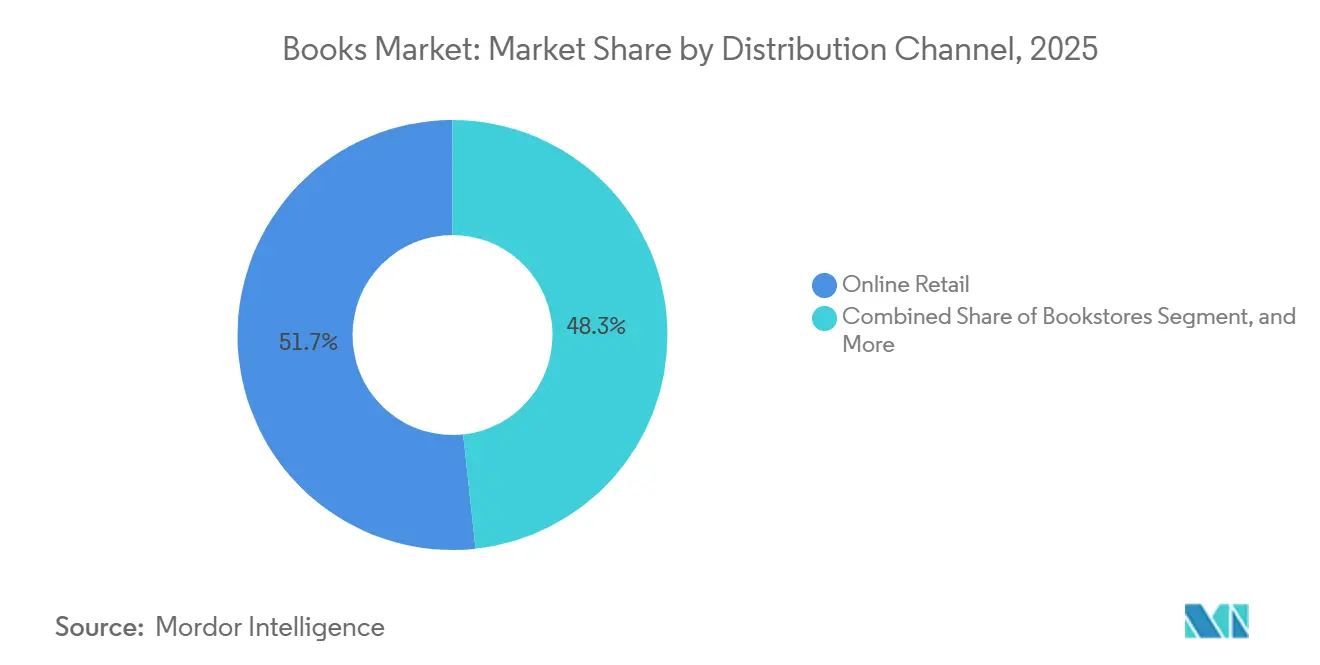

- By distribution channel, online retail accounted for 51.71% of the books market in 2025, and is projected to grow at a 4.05% CAGR between 2026-2031.

- By geography, Asia Pacific accounted for 36.66% of the books market share in 2025 and is expected to deliver a 4.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Books Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Subscription-Based Reading in Asia | +0.6% | Asia-Pacific | Medium term (3-4 yrs) |

| Rapid Audiobook Uptake Among Commuters in Europe | +0.5% | Europe | Medium term (3-4 yrs) |

| Growing K-12 and Higher-Ed Textbook Adoption in Africa | +0.3% | Africa | Long term (≥ 5 yrs) |

| Government-Backed Literacy Missions in South America | +0.3% | South America | Long term (≥ 5 yrs) |

| Copyright Reform Fueling Digital Libraries in Middle East | +0.2% | Middle East | Medium term (3-4 yrs) |

| Premiumization of Special-Interest Print in North America | +0.2% | North America | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Shift Toward Subscription-Based Reading in Asia

Subscription platforms are redefining value perception by swapping one-off purchases for unlimited access. Audible’s monthly app revenue climbed more than 12,000% between early 2020 and February 2025, delivering USD 440 million in 2024 and USD 63 million in January 2025 [1] Appfigures Staff, “Audible Revenue Trends 2020-2025,” appfigures.com . The model lowers entry costs for price-sensitive readers yet lifts lifetime spend by increasing reading hours, prompting Google and regional competitors to launch rival offers. Publishers gain predictable cash flow but must balance cannibalization of single-title sales with the reach of bundled consumption.

Growing K-12 and Higher-Ed Textbook Adoption in Africa

Governments are pairing infrastructure investment with bulk textbook procurement, stimulating hybrid print-digital publishing. South Africa’s entertainment and media sector is forecast to expand from USD 9 billion to USD 13.6 billion by 2028, with education content a primary contributor. Localized curricula and multilingual editions strengthen adoption, yet complex tender cycles reward publishers able to navigate public procurement and deliver region-specific pedagogical resources.

Premiumization of Special-Interest Print in North America

Collectors view high-spec editions as cultural artefacts, driving a renaissance in physical book production. Bloomsbury’s consumer division grew revenue 49% in 2024 on the back of premium fantasy hardbacks [2]Bloomsbury Publishing PLC, “Annual Report 2025,” bloomsbury.com . Demand concentrates on titles with foil stamping, cloth bindings and sustainable paper, allowing publishers to command double-digit price uplifts that cushion rising input costs.

Rapid Audiobook Uptake Among Commuters in Europe

Audio spending hit USD 2 billion in the United States in 2024, up 9% year-on-year, with parallel climbs in the UK and Germany [3]Association of American Publishers, “Monthly StatShot February 2025,” publishers.org . Average annual consumption reached 4.8 titles as commuters convert travel time into listening time. Production is shifting toward audio-first originals featuring full casts and immersive sound design, widening the gap with text-to-speech conversions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking Shelf-Space in Brick-and-Mortar Retailers | –0.4% | Global | Short term (≤ 2 yrs) |

| Piracy Surge on Telegram and Discord Channels | –0.3% | Global | Medium term (3-4 yrs) |

| VAT on E-books in Select EU Countries | –0.2% | European Union | Medium term (3-4 yrs) |

| Supply-Chain Paper Shortages since 2023 | –0.2% | Global | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Shrinking Shelf-Space in Brick-and-Mortar Retailers

Even as Barnes & Noble plans 60 new US stores for 2025, many chains rationalize inventory, allocating fewer linear feet to books in favor of higher-turnover items [4] PBS NewsHour, “Barnes & Noble’s Comeback Strategy,” pbs.org . Mid-list authors lose discovery opportunities, forcing publishers to invest in data-driven online marketing and virtual author events to replace impulse in-store purchases.

VAT on E-books in Select EU Countries

While printed books often benefit from reduced or zero VAT, digital editions attract standard rates in several EU states. The higher final price suppresses e-book uptake and disadvantages born-digital publishers. Industry bodies lobby for parity, but until harmonization arrives, publishers hedge by bundling formats and experimenting with tiered pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Format: Audiobooks Drive New Consumption Moments

Hard copy retained 76.59% of the book market share in 2025, yet audiobooks booked the fastest expansion, tracking an 8.49% CAGR to 2031. The Books market size attributable to audio is forecast to more than double, supported by smartphone penetration, connected cars, and smart-speaker adoption in households. Commuters account for the largest listener cohort and now finish an average of 4.8 titles per year. Publishers that embrace simultaneous release strategies and commission audio-first originals gain share across both digital storefronts and subscription bundles. E-books maintain a complementary role, with February 2025 revenue increasing 7.8% to USD 102.7 million. Evidence that readers cross-shop formats underlines the need for format-agnostic editorial pipelines and unified customer data lakes.

Print remains culturally and commercially significant. Premium hardbacks-featuring cloth spines, sprayed edges and archival paper-command price uplifts that cushion per-unit cost inflation. The segment also benefits from gifting occasions and collector psychology. Meanwhile, agile offset printers and on-demand digital presses mitigate inventory risk, ensuring backlist titles stay in print even as shelf space contracts.

By Genre: Fiction Retains Primacy While Children’s Accelerates

Fiction ended 2025 with 33.26% of total revenue 2025, Limited-edition runs and author-signed copies amplify basket values within fantasy, illustrating how experiential merchandising maximizes the Books market revenue per title. As parents embrace read-aloud audiobooks and educators adopt interactive e-books for remote learning. Middle-grade print sales dipped 5% in early 2024, yet graphic novel hybrids rejuvenate engagement among reluctant readers.

Educational and academic presses face budget constraints and institutional subscription fatigue, leading to double-digit revenue declines in 2024. Open-access models such as MIT Press’s Direct to Open quadruple usage compared to paywalled equivalents. Non-fiction growth is uneven: adult self-help titles rise on mental-wellness trends, while narrative history contracts. Religious presses surprised with an 18.9% gain, reflecting demand for devotional study aids and audio sermons. Comics and graphic novels are predicted to climb at 4.81% CAGR as manga and webtoon crossovers drive mainstream adoption.

By Distribution Channel: Online Retail Redefines Discovery

Online retail accounted for 51.71% of the market in 2025 and is on track for a 4.05% CAGR to 2031, as frictionless checkout and algorithmic recommendations boost conversion rates. Strategic initiatives such as Amazon’s “Your Books” personalized hub increase dwell time and repeat purchase frequency. Though physical chains open new concept stores that emphasize community events and local curation, constrained shelf space forces faster title rotation. The Books market participants, therefore, bolster metadata, cover design, and influencer partnerships to cut through digital noise.

Direct-to-consumer sites and subscription bundles augment margins by capturing shopper data and upselling cross-format collections. Audiobook users display the highest subscription propensity; 63% hold at least one active membership. Libraries remain pivotal for discovery, yet restrictive e-book licensing libraries paying USD 55 for a copy that expires in two years versus USD 15 for consumers spurs legislative. Supermarkets and convenience stores sustain volume on bestsellers, especially during holiday peaks, but their limited assortments shift mid-list promotion firmly online.

Geography Analysis

Asia-Pacific generated 36.66% of global revenue in 2025 and is expected to deliver a 4.13% CAGR to 2031, anchored by China, where digital reader penetration reached 38%. India’s fiction sales surged 30.7%, underscoring how rising disposable incomes unlock discretionary cultural spend. Subscription-based reading apps dominate the regional growth narrative, quickly translating smartphone ubiquity into predictable monthly revenue streams. The Books market size in Asia-Pacific is projected to expand further as publishers localize content in Mandarin, Hindi, and Bahasa Indonesia and partner with telcos to offer bundled offers.

In the Middle East and Africa, Saudi Arabia’s USD 2.5 billion national market benefits from enhanced IP frameworks and a flourishing book-fair circuit that welcomed 1,350 publishers from 90 countries in Abu Dhabi in 2024. South Africa’s media spend outlook, rising from USD 9 billion to USD 13.6 billion by 2028, highlights the textbook demand’s central role in education reforms. Publishers that translate STEM materials into Arabic, Amharic, and Swahili secure an early mover advantage.

Europe maintains solid, if slower, momentum. UK sales stood at GBP 1.82 billion (USD 1.82 billion) in 2024; fiction hit record highs despite a 0.6% dip overall . VAT anomalies on e-books remain a drag. Latin America shows accelerator characteristics: Brazil advanced 16.4% and Mexico 20.7% in 2024 on literacy campaigns and currency stabilization. North America remains the single biggest mature market; US print units edged up to 782.7 million in 2024, even as digital formats capture incremental time slices. Combined, these patterns reinforce how the Books market requires hyper-localized strategies to convert regional structural shifts into sustainable revenue.

Competitive Landscape

The four largest trade houses Penguin Random House, Hachette, HarperCollins and Macmillan captured 48.6% of UK sales in 2024, illustrating a tightening oligopoly. Penguin Random House surpassed USD 5 billion in 2024 revenue after an 8.5% jump, accompanied by workforce rationalization to protect margins. Acquisition pipelines target niche imprints that deliver genre depth and influencer-led nonfiction.

Technology features prominently in competitive positioning. Elsevier and Springer Nature deploy AI-based integrity checks that flag manipulated images and fabricated citations, shortening peer-review cycles and enhancing reputational capital. Trade publishers experiment with generative-AI metadata enrichment to uplift discoverability while instituting guardrails to uphold author copyrights. This capability gap opens space for digital-native challengers that design workflows around continuous analytics.

Self-publishing swells to an estimated 30% of all e-book sales in 2024, drawn by royalty rates topping 70% on some platforms. Aggregators offer editorial, cover-design and marketing packages once reserved for traditional houses, fragmenting author supply. As the Books market evolves, incumbents counter with hybrid contracts granting authors flexible paths between self-service and full-service publishing, preventing high-potential franchises from migrating permanently to rival ecosystems.

Books Industry Leaders

Penguin Random House LLC

Hachette Livre

HarperCollins Publishers LLC

Pearson PLC

Macmillan Publishers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Penguin Random House reported an 8.5% sales rise for 2024, topping USD 5 billion, despite market headwinds.

- March 2025: MIT Press’s Direct to Open model showed open-access humanities titles receive nearly four times more usage than paywalled editions.

- September 2024: HarperCollins, Lagardère Publishing and Penguin Random House each reported earnings rebounds, with HarperCollins sales up 6% and profits up 54%.

- April 2024: The Abu Dhabi International Book Fair welcomed 1,350 publishers and introduced AI-driven payment innovations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global books market as annual publisher-level revenue from new printed volumes, e-books, and professionally produced audiobooks across trade, educational, and religious genres, whatever the sales channel. We convert all regional figures to constant 2024 USD so cross-country trends stay visible.

Scope Exclusions: Used-book resale, self-published titles without ISBN registration, and illicit digital downloads remain outside this scope.

Segmentation Overview

- By Format

- Hard Copy

- E-books

- Audiobooks

- By Genre

- Fiction

- Non-Fiction

- Educational and Academic

- Childrens and Young Adult

- Religious / Spiritual

- Comics and Graphic Novels

- By Distribution Channel

- Online Retail

- Bookstores

- Supermarkets / Convenience Stores

- Direct-to-Consumer and Subscriptions

- Libraries and Institutional Procurement

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts speak with publishing executives, distributors, online platforms, bookstore buyers, and campus procurement officers across North America, Europe, Asia-Pacific, and Latin America, then follow up with reader surveys. Their insight challenges early desk findings and supplies live averages for selling prices, audiobook uptake, and subscription penetration.

Desk Research

We begin by mapping title output and unit flow through public datasets such as UNESCO ISBN registrations, trade audits from the Association of American Publishers and the Federation of European Publishers, customs export ledgers, and national library circulation dashboards. Company filings, investor decks, and reputable press refine segment shares, while D&B Hoovers and Dow Jones Factiva confirm publisher financials. These sources anchor base-year values, yet they are only a starting point; many additional documents guide our checks and clarifications.

Market-Sizing & Forecasting

A top-down construct converts country-level turnover and trade data into a global pool, which is then tested through selective bottom-up roll-ups of sampled ASP x units and printer capacity checks. Key variables like ISBN issuance growth, reading-age population, e-commerce share, average price inflation, and school enrollment feed a multivariate regression with scenario analysis to project format substitution. Gaps in emerging markets are bridged by regional proxies vetted in expert calls before acceptance.

Data Validation & Update Cycle

Outputs pass multi-step variance screens and peer review; anomalies trigger re-contact with sources. We refresh every twelve months and issue interim revisions when material events, such as currency swings, postal rate hikes, or new VAT rules, shift market math. A final analyst pass occurs just before release, so clients receive the most current view.

Why Mordor's Books Baseline Earns Trust

Published estimates often differ because firms select unlike product mixes, freeze exchange rates on varied dates, or refresh at uneven cadences. Our disciplined scope, annual update, and price-normalized currency conversion temper those skews and give decision-makers a balanced point of departure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 140.44 B | Mordor Intelligence | - |

| USD 151.00 B | Global Consultancy A | Includes second-hand sales and treats net receipts as gross, inflating totals |

| USD 144.11 B | Regional Consultancy B | Uses static average prices and skips currency normalization, understating growth |

Taken together, the comparison shows that Mordor's step-wise checks, transparent exclusions, and fresh data deliver a dependable baseline traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

How big is the Books Market?

The Books Market size is expected to reach USD 135.49 billion in 2026 and grow at a CAGR of 3.11% to reach USD 157.88 billion by 2031.

What is the current Books Market size?

In 2026, the Books Market size is expected to reach USD 135.49 billion.

Who are the key players in Books Market?

Pearson PLC, McGraw-Hill Publications, Penguin Random House LLC, Hachette Livre and Elsevier Foundation are the major companies operating in the Books Market.

Which is the fastest growing region in Books Market?

The Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031) at 4.13%.

Which region has the biggest share in Books Market?

In 2025, the Asia-Pacific accounts for the largest market share in Books Market at 36.66%.

Page last updated on: