Manga Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.12 Billion |

| Market Size (2031) | USD 56.38 Billion |

| Growth Rate (2026 - 2031) | 19.52% CAGR |

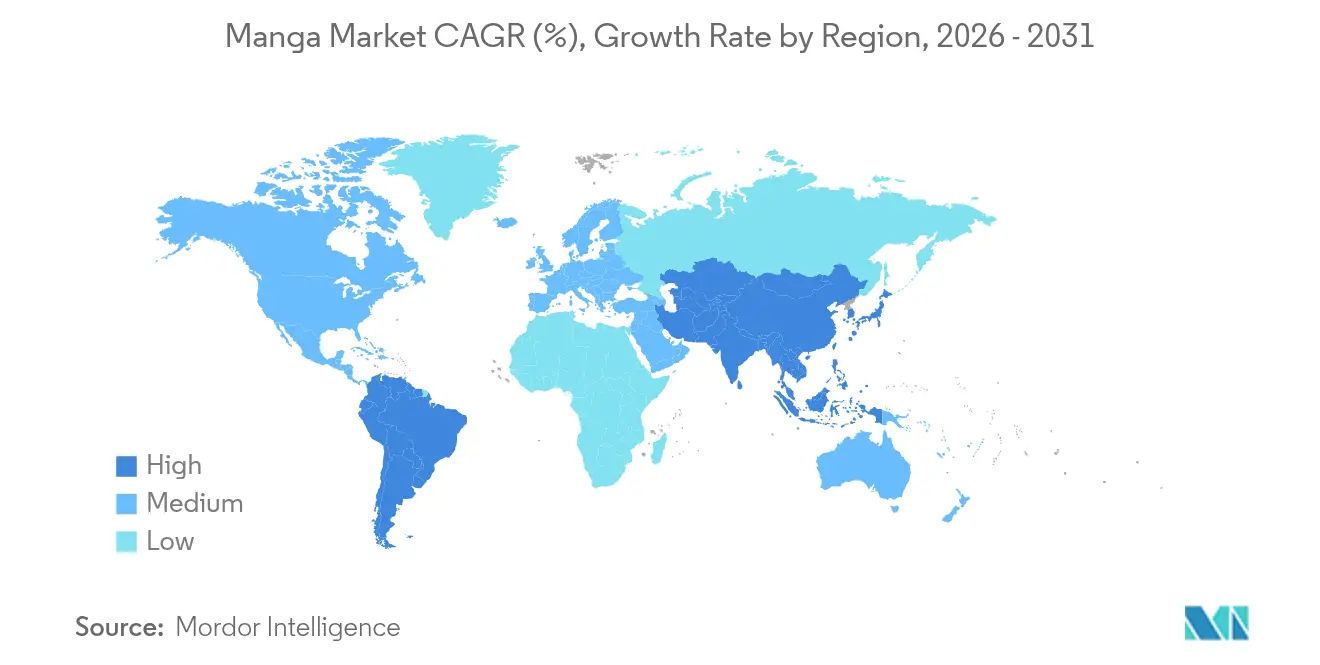

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

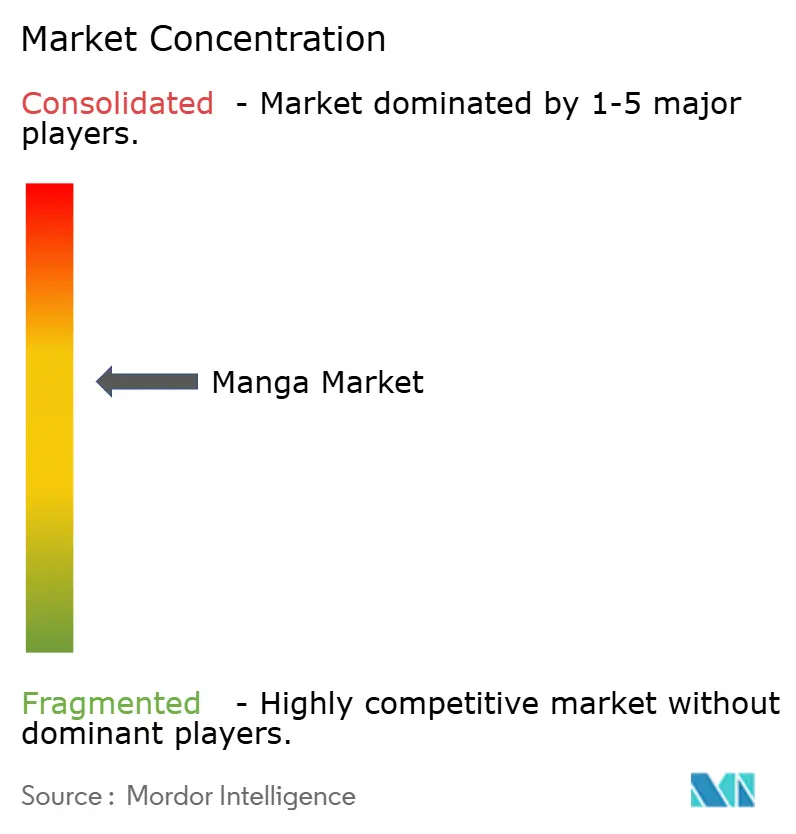

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Manga Market Analysis by Mordor Intelligence

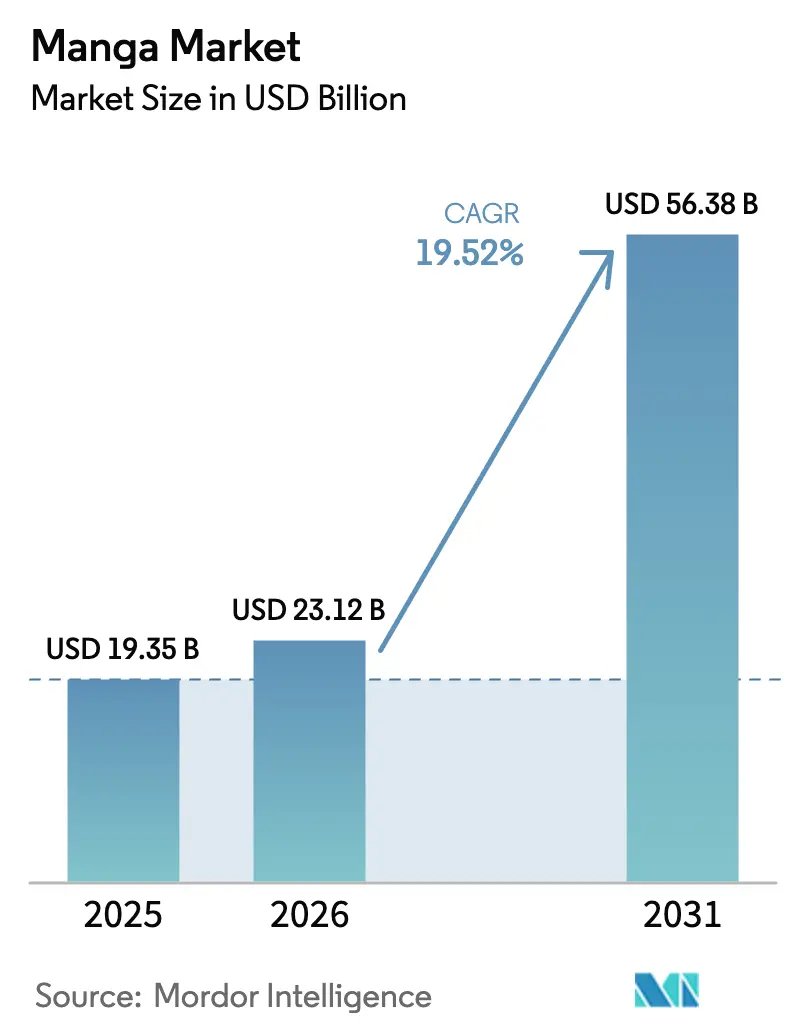

The Manga Market size market is expected to grow from USD 19.35 billion in 2025 to USD 23.12 billion in 2026 and is forecast to reach USD 56.38 billion by 2031 at 19.52% CAGR over 2026-2031.

High-speed growth reflects the medium’s shift from a niche Japanese export to a global entertainment mainstay, powered by digital platforms, cross-media franchising and a mobile-first audience that reads on the go. Digital formats already account for 72.70% of consumption, while online channels command 68.55% of sales, a structural pivot that compresses distribution costs and opens new revenue models such as subscriptions and microtransactions. Intellectual-property (IP) leverage is deepening: publishers now earn 27% of income from licensing, streaming and merchandising, reinforcing franchise economics over single-volume sales Piracy, however, wiped an estimated USD 12.5 billion from industry coffers in 2024, and rising trade frictions threaten print margins. AI-enabled translation startups are countering these headwinds by cutting localization time and cost, accelerating overseas growth.

Key Report Takeaways

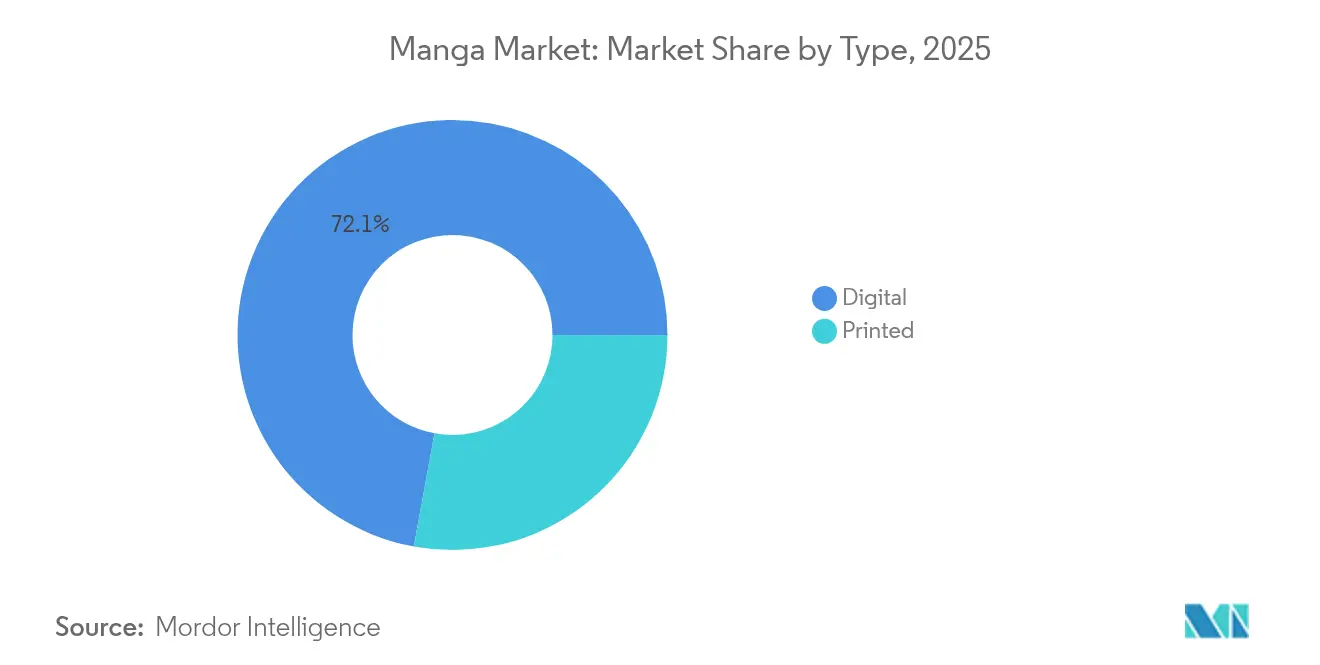

- By type, digital formats captured 72.12% of manga market share in 2025; print retains relevance but digital is set to grow at a 16.21% CAGR through 2031.

- By distribution channel, online platforms held 67.90% revenue share in 2025, while app-based services are forecast to expand at a 21.05% CAGR to 2031.

- By genre, shonen titles led with 39.10% of manga market share in 2025; webtoons are projected to expand at a 35.62% CAGR through 2031.

- By geography, the Asia-Pacific region contributed 62.20% of the manga market revenue in 2025; South America is expected to record a 20.85% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Manga Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Japanese pop-culture mainstream reach | +4.2% | Global (strongest in North America and Europe) | Medium term (2-4 years) |

| Accelerated digital consumption and monetization | +5.8% | Global (led by Asia-Pacific and North America) | Short term (≤ 2 years) |

| Cross-media IP synergies | +3.7% | Global premium markets | Medium term (2-4 years) |

| Expanding female and mature readership | +2.9% | North America and Europe; growing in Asia-Pacific | Long term (≥ 4 years) |

| Generative-AI multilingual localization | +2.1% | Early-adopting developed markets | Long term (≥ 4 years) |

| Fractional IP and fan-investment platforms | +1.1% | North America and Europe; pilots in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Japanese Pop-Culture Mainstream Reach

Anime adaptations regularly double manga volume sales, as seen when “Frieren: Beyond Journey’s End” surged after its 2024 broadcast.[1]Deb Aoki, “Kidults Propel USD 1.5 Billion Anime Toy Spend,” news.animenomics.com Mature “kidult” buyers in the United States spent USD 1.5 billion on anime-themed toys in Q1 2024, eclipsing preschool demand. Two in five U.S. Gen Z viewers stream anime weekly, cementing future demand. Because these viewers age into higher disposable income brackets, the manga market gains a durable, multi-decade revenue base. Crucially, Japanese publishers have scaled without diluting cultural authenticity, preserving brand equity as titles cross borders.

Accelerated Digital Consumption and Monetization

Japan reached 72.7% digital penetration in 2024, generating JPY 512.2 billion (USD 3.3 billion) from e-volumes. Freemium platforms such as WEBTOON earned USD 1.35 billion in 2024, with 80.2% from paid content, 11.3% advertising, and 8.4% IP adaptations.[2]SEC Staff, “WEBTOON Entertainment Inc. Form 424B4,” sec.gov Revenue-share schemes return 50% of ad earnings to creators once monthly payouts exceed USD 100, seeding a self-reinforcing creator economy. Digital-native titles now represent 37% of new releases, doubling in 10 years, a sign that mobile feedback loops are supplanting print gatekeeping.

Cross-Media IP Synergies (Anime, Games, Films)

IP monetization accounts for 27% of Shueisha income and 16% at Kodansha. Episode-based adaptation fees average JPY 200,000– JPY400,000, while merchandise royalties can reach 35% of net sales. Kadokawa earned USD 130 million from franchises like “Oshi no Ko” in 2024, illustrating the upside of multi-format exploitation. Overseas anime revenue climbed to JPY 1.72 trillion (USD 11.2 billion) in 2024, overtaking domestic sales and confirming that well-managed IP scales globally.

Expanding Female and Mature Readership Segments

U.S. bookstore data show girls and young women now account for a majority of manga buyers. The female fan economy is valued at JPY 1.8 trillion (USD 12 billion); IDOLiSH7’s 2024 movie grossed JPY 2.8 billion (USD 19 million), validating purchasing power. Platforms have responded by adding comment threads, creator QandA and social sharing—features that map to community-oriented consumption habits and support premium pricing for collector editions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Piracy and scanlation communities | -6.3% | Global (highest in emerging markets) | Short term (≤ 2 years) |

| Censorship / political content limits | -2.8% | China, Middle East, selective in North America | Medium term (2-4 years) |

| Rising print and logistics costs | -1.9% | Global (physical distribution) | Short term (≤ 2 years) |

| Trade tariffs on printed imports | -1.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Piracy and Scanlation Communities

Industry losses hit USD 12.5 billion in 2024 as 1,332 illegal sites distributed free scans.[3]David Taylor, “Japan’s Publishers Target 1,300 Pirate Sites,” lexology.com English-language platforms alone cost publishers USD 800 million that May. Japan’s AI-enabled anti-piracy tools shut hundreds of URLs, yet 100 new pirate domains appeared within a month. The result is a vicious cycle: revenue siphoned by piracy reduces funds for official localization, which in turn leaves unmet demand that pirates exploit.

Censorship / Political Content Restrictions

Graphic novels faced 378 challenges in U.S. libraries during 2024, with series such as “Assassination Classroom” temporarily removed. China’s clampdown on Boys’ Love content forces redundant editing passes and separate domestic versions, inflating cost. Across the Middle East, import checks delay shipment of volumes depicting LGBTQ+ themes. Maintaining multiple SKUs erodes the scale advantages of digital distribution and drags on the manga market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Digital Dominance Accelerates Adoption

Digital volumes represented 72.12% of 2025 revenue and are projected to expand at a 16.21% CAGR to 2031. Within this category, web-optimized vertical scrolls outpace classic page layouts, reflecting how smartphones shape reading sessions. E-comics subscriptions drive higher lifetime value than one-off tankōbon purchases. Print continues to serve collectors, yet shrinking circulation of weekly magazines underscores irreversible migration to screens. The digital segment’s share of manga market size for premium e-book bundles reached 38.45% in 2025 and is forecast to top 51.6% by 2031, illustrating the widening monetization gap over physical media.

Publishers now design titles specifically for scrolling flow, unlocking rapid feedback loops and data-driven story pivots. Webtoon portals employ machine-learning recommendation engines that lift completion rates, supporting repeat micro-transactions. Advertising is another lever: CPM yields rose 14% in 2024 as brand marketers chase Gen Z attention in content-safe environments.

By Distribution Channel: Online Platforms Reshape Value Chains

Online platforms controlled 67.90% of 2025 revenue, a clear lead that continues as apps integrate payments, forums and merchandise storefronts. Between 2026-2031, app-centric sales are expected to climb at a 21.05% CAGR. The ascendancy of direct-to-reader storefronts shrinks middle-man margins and returns data ownership to rights holders. Offline retail still matters for gift-giving and limited editions, but footfall is migrating online, driving hybrid strategies where customers browse digitally and redeem collectors’ editions via mail or pop-up events.

Large platforms exploit network effects: Crunchyroll’s 2025 manga app cross-sells to its 15 million anime subscribers, reducing acquisition cost per reader. Smaller publishers list on open marketplaces to bypass stocking fees. Data insights from click-through and dwell time analytics help editorial teams green-light new arcs, shortening concept-to-launch cycles and reinforcing the flywheel that propels the manga market.

By Genre: Shonen Leadership Faces Webtoon Disruption

Shonen titles held 39.10% of 2025 revenue, reflecting broad demographic reach and strong synergy with action-oriented anime and video games. Nevertheless, webtoon-exclusive IP is forecast to expand at a 35.62% CAGR, driven by snackable story arcs and social-sharing hooks that attract new readers. Shojo romance benefits from the rising female readership, while Seinen and Josei capture the spending power of mature fans.

Isekai narratives monetize via cross-platform gaming tie-ins, and horror franchises sell premium omnibuses to niche collectors. Sports serials remain stable, anchored by evergreen fandom. BL and Yuri's manga tap underserved audiences seeking inclusive representation, a trend amplified by the algorithmic discovery that surfaces long-tail content. This diversity underpins resilience, enabling the manga market to weather saturation in legacy genres.

Geography Analysis

Asia-Pacific manga market generated 62.20% of global revenue in 2025, buoyed by Japan’s ¥704.3 billion (USD 4.67 billion) sales and South Korea’s thriving webtoon ecosystem Nippon.com. Digital formats account for 72.7% of Japanese turnover, freeing capital for aggressive overseas localization. China offers vast potential but tight censorship; Southeast Asian economies gain ground as mobile broadband costs fall, supporting double-digit volume growth.

North America is the largest overseas revenue pool despite a 26% volume decline in 2024 to 21.8 million units as pandemic-era spikes normalize. VIZ Media holds a 57% share, and bundle discounts with streaming services sustain premium pricing. Piracy remains a drag, yet the rising adoption of simulpub releases on the same day as Japan is narrowing the lag that fueled illegal scans.

South America is projected to grow by 20.85% CAGR through 2031. Brazil, now the third-largest anime market outside East Asia, drives spill-over demand for print omnibuses and Portuguese digital editions. Argentina and Chile see new Spanish-language portals that circumvent import tariffs accelerating uptake. Europe remains mature: France sells 66 million manga volumes annually, but growth moderates below 5% amid competition from domestic BD titles. The Middle East and Africa offer long-term upside tied to smartphone adoption, though content vetting lengthens market-entry timelines. Overall, diversification across continents reduces reliance on any single region, insulating the manga market from localized shocks.

Competitive Landscape

The Manga market is highly competitive and fragmented, primarily driven by the presence of major players. These key players employ strategies such as mergers, acquisitions, and product innovations to maintain a competitive edge and broaden their global footprint. Key player include Akita Publishing Co., Ltd., Bilibili Comics Pte. Ltd., Bungeishunju Ltd., and others.

The manga market is poised for robust growth driven by cultural trends, digital accessibility, and a diverse range of genres appealing to a global audience. Further, collaborations between manga creators and other media formats (such as video games and films) are becoming more common, creating additional avenues for growth and audience engagement. Overall, as the industry continues to evolve, it presents abundant opportunities for both traditional publishers and new digital platforms.

Manga Industry Leaders

Shueisha Inc.

Kodansha Ltd.

Shogakukan Inc.

Kadokawa Corporation

VIZ Media LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Media Do, NTT Docomo and Akatsuki debuted Manga Mirai in the United States with 11,000+ volumes across 780 titles; MyAnimeList handles cross-promotion.

- October 2024: Sony invested JPY 50 billion (USD 320 million) to lift its Kadokawa stake to about 10%, funding new IP production and overseas distribution.

- June 2024: WEBTOON Entertainment raised USD 315 million in a Nasdaq IPO at USD 21 per share, valuing the platform at USD 2.67 billion.

- May 2024: AI localization start-up Orange secured USD 20 million to scale multilingual translation from 100 to over 1,000 volumes per month while retaining human quality control.

Global Manga Market Report Scope

Manga are comics or graphic novels originating from Japan. The term manga is used in Japan to refer to both comics and cartooning. Outside of Japan, the word is typically used to refer to comics originally published in Japan.

The manga market is segmented by type (printed, digital), by distribution channel (offline, online), by genre (action & audience, sci-fi & fantasy, sports, romance & drama, other genres), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Printed | Tankōbon / Graphic Albums |

| Serialized Magazines | |

| Light Novels | |

| Digital | E-comics / E-books |

| Webtoons and Vertical Scroll | |

| Subscription Streaming Apps |

| Offline | Bookstores and Comic Shops |

| Mass-Merchandisers / Convenience Stores | |

| Online | E-commerce (Physical Delivery) |

| Digital Platforms and Apps |

| Shonen (Action / Adventure) |

| Shojo (Romance / Drama) |

| Seinen (Adult Men) |

| Josei (Adult Women) |

| Isekai and Fantasy |

| Sports |

| Horror / Thriller |

| Other Niches (BL, Yuri, Educational) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Spain | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | Japan | |

| China | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of APAC | ||

| Middle East and Africa | Middle East | Turkey |

| Saudi Arabia | ||

| UAE | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Type | Printed | Tankōbon / Graphic Albums | |

| Serialized Magazines | |||

| Light Novels | |||

| Digital | E-comics / E-books | ||

| Webtoons and Vertical Scroll | |||

| Subscription Streaming Apps | |||

| By Distribution Channel | Offline | Bookstores and Comic Shops | |

| Mass-Merchandisers / Convenience Stores | |||

| Online | E-commerce (Physical Delivery) | ||

| Digital Platforms and Apps | |||

| By Genre | Shonen (Action / Adventure) | ||

| Shojo (Romance / Drama) | |||

| Seinen (Adult Men) | |||

| Josei (Adult Women) | |||

| Isekai and Fantasy | |||

| Sports | |||

| Horror / Thriller | |||

| Other Niches (BL, Yuri, Educational) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| Italy | |||

| Spain | |||

| United Kingdom | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | Japan | ||

| China | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of APAC | |||

| Middle East and Africa | Middle East | Turkey | |

| Saudi Arabia | |||

| UAE | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the manga market?

The manga market is worth USD 23.12 billion in 2026 and is projected to reach USD 56.38 billion by 2031.

How fast is digital manga growing compared with print?

Digital formats already hold 72.12% share and are expanding at a 16.21% CAGR, while print circulation continues to contract.

Which region offers the highest growth potential?

South America is forecast to deliver a 20.85% CAGR through 2031, driven by Brazil’s booming anime fan base and improved broadband.

What are the biggest threats to revenue growth?

Online piracy, causing USD 12.5 billion in losses during 2024, and censorship policies that limit content diversity in key markets.

Page last updated on: