Bone Metastasis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

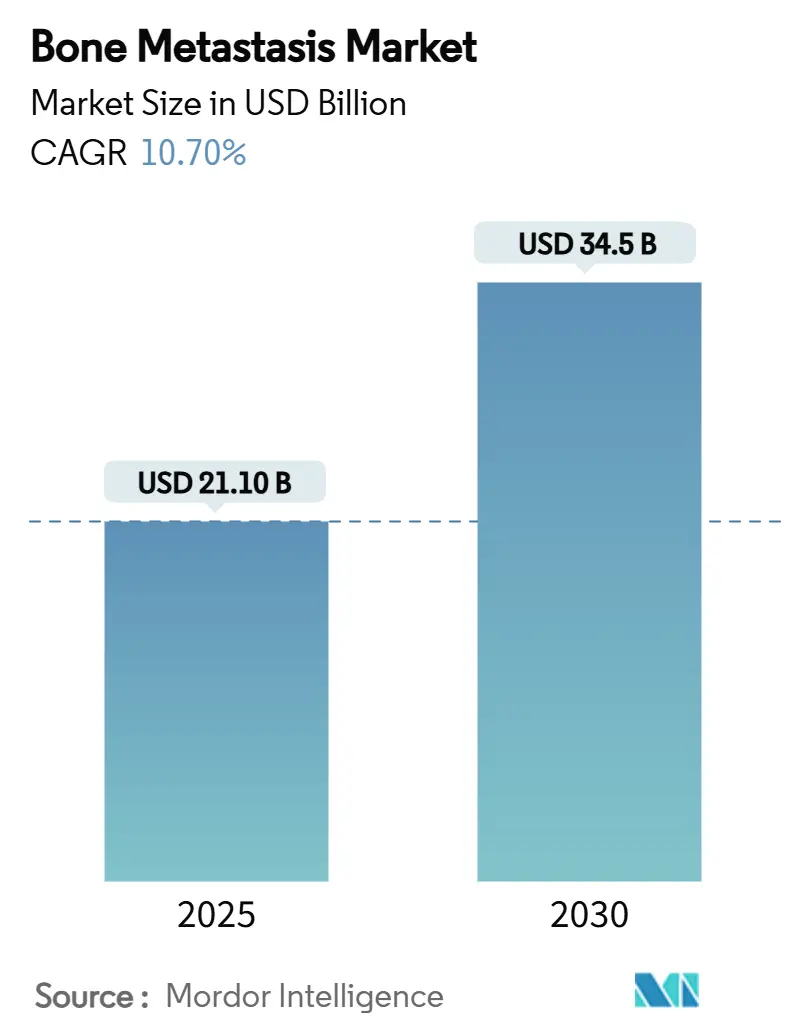

| Market Size (2025) | USD 21.10 Billion |

| Market Size (2030) | USD 34.5 Billion |

| Growth Rate (2025 - 2030) | 10.70% CAGR |

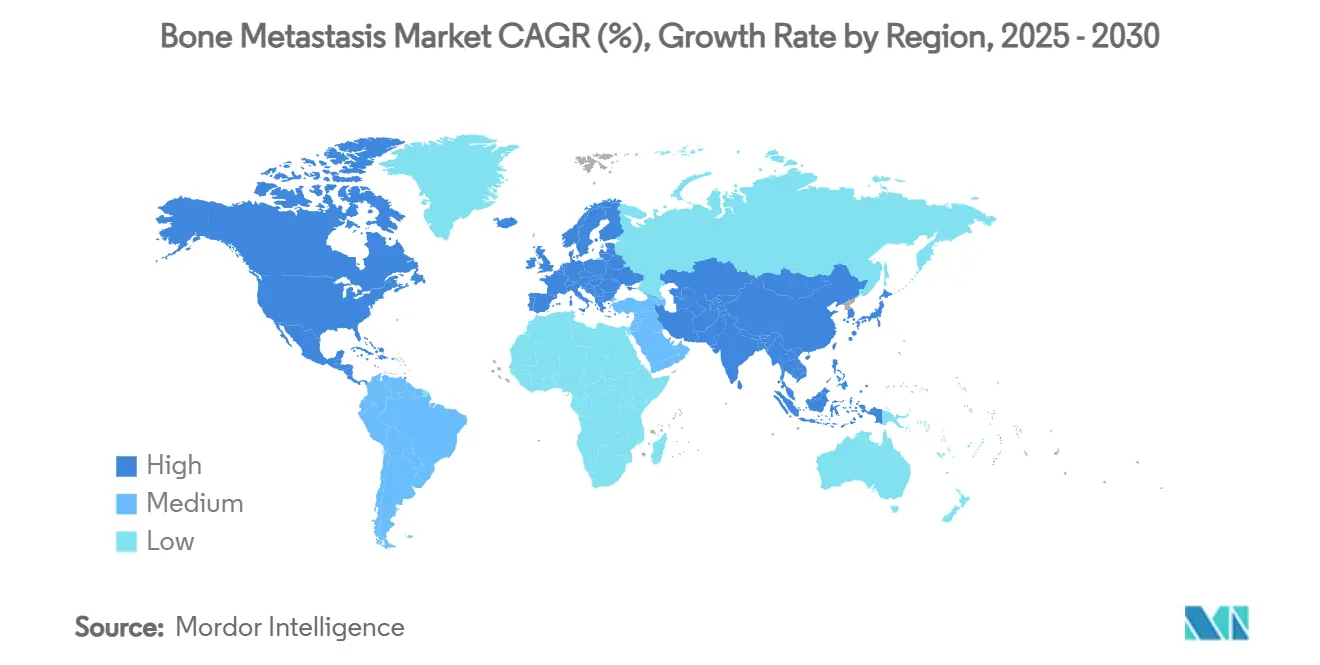

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bone Metastasis Market Analysis by Mordor Intelligence

The bone metastasis market size reached USD 21.1 billion in 2025 and is projected to rise to USD 34.5 billion by 2030, translating into a 10.7% CAGR. Growth is anchored in increasing cancer incidence, broader radiopharmaceutical approvals, and payer moves toward value-based oncology care that rewards skeletal-related-event prevention. Roughly 70% of advanced breast and prostate cancer patients develop skeletal lesions, creating a large addressable pool. Preventive bone-modifying agents gain traction because European data show that treating a single skeletal-related event can cost USD 65,000 per patient. Meanwhile, manufacturers are expanding alpha-emitting radiopharmaceutical capacity in response to robust demand. AI-enabled imaging is pushing detection earlier in the course of disease, widening the funnel for timely intervention.

Key Report Takeaways

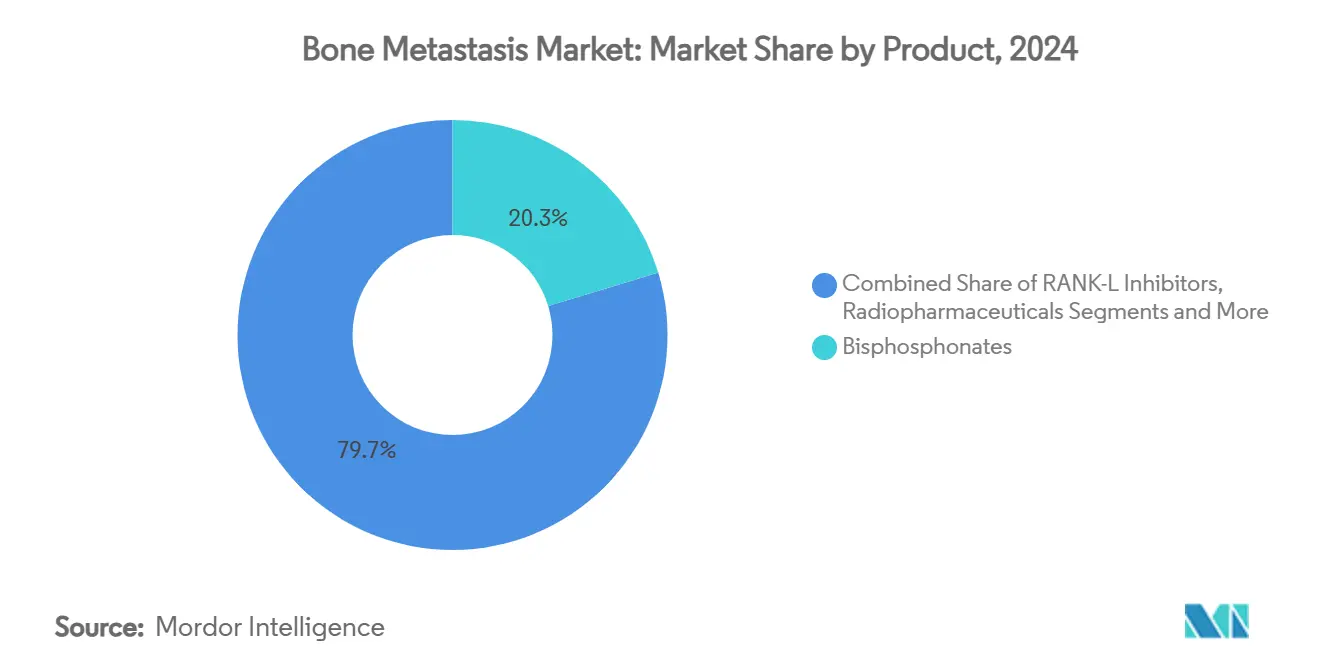

- By therapy type, bisphosphonates led with 20.3% Bone metastasis market share in 2024, while radiopharmaceuticals are forecast to advance at a 13.6% CAGR to 2030.

- By cancer type, breast cancer accounted for 17.7% of the Bone metastasis market size in 2024; lung cancer is projected to grow fastest at 11.4% CAGR through 2030.

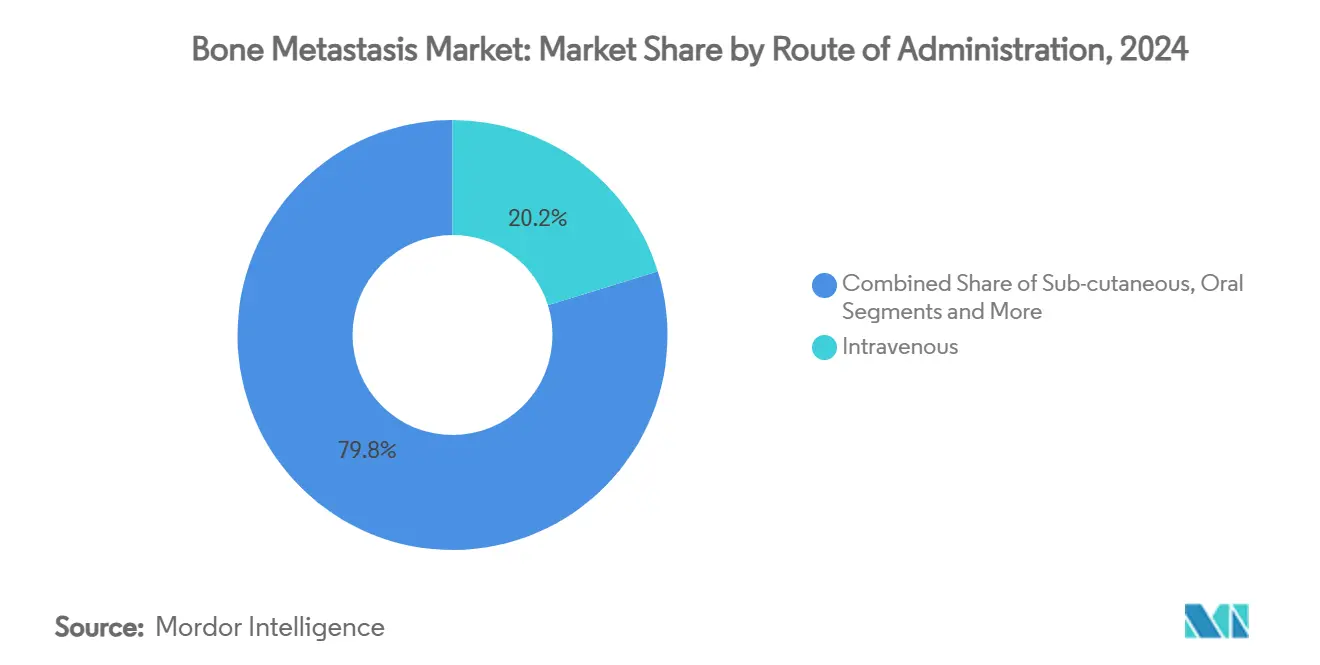

- By route of administration, intravenous delivery captured 20.2% revenue share in 2024; subcutaneous formulations are expanding at 9.3% CAGR to 2030.

- By end user, hospitals held 20.8% of the Bone metastasis market size in 2024, while ambulatory surgical centers are set to post an 8.6% CAGR through 2030.

- By geography, North America maintained 19.9% share of the Bone metastasis market in 2024; Asia Pacific is positioned to grow at 9.9% CAGR to 2030.

Global Bone Metastasis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of primary cancers | +2.80% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Rising adoption of targeted bone-modifying agents | +2.10% | North America & EU; expanding to Asia Pacific | Medium term (2-4 years) |

| Shift toward value-based oncology care | +1.90% | Primarily North America; EU to follow | Medium term (2-4 years) |

| Expansion of radiopharmaceutical approvals | +2.40% | Global; regulatory leadership in US & EU | Short term (≤ 2 years) |

| AI-driven image analytics | +1.20% | North America & EU initially; Asia Pacific rapidly scaling | Long term (≥ 4 years) |

| Emergence of theranostic alpha-emitters | +1.80% | Global; manufacturing centered in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Primary Cancers

Bone metastases arise in up to 70% of metastatic breast and prostate cancers and 17% of advanced melanoma cases, underpinning durable demand for the Bone metastasis market. Aging demographics in North America and Europe amplify this burden, while Beijing surveillance showed prostate-bone spread climbing 57% between 2011 and 2014. Higher de-novo metastatic rates in parts of the Middle East spotlight unmet needs, spurring interest in early-detection imaging that shifts care upstream.[1]BMJ Open Research Team, “Prostate cancer bone metastasis trends in Beijing,” bmjopen.bmj.com

Rising Adoption of Targeted Bone-Modifying Agents

Denosumab biosimilars secured simultaneous US and EU approvals in 2024, intensifying competition inside a USD 5 billion sub-segment. Health-economic studies in Central Europe confirm favorable quality-adjusted life-year profiles despite higher pharmacy spend. Multiple myeloma protocols now favor agents with lower osteonecrosis risk, bolstering uptake of next-generation biologics and reinforcing growth for the Bone metastasis market.

Shift Toward Value-Based Oncology Care & Bundled Payments

Medicare’s Radiation Oncology Model bundles episode-level payments, encouraging providers to prevent costly skeletal events. Multicenter EU findings report that the average number of inpatient stays topped 8 days after such events, underlining the fiscal imperative for prophylaxis. The 2025 inclusion of bone disease-arthritis as a core chronic condition within Medicare’s medication therapy programs is expected to raise adherence, supporting long-run expansion of the Bone metastasis market.[2]Centers for Medicare & Medicaid Services, “Radiation Oncology Model Fact Sheet,” cms.gov

Expansion of Radiopharmaceutical Approvals

Alpha-emitting candidates such as 212Pb and ZetaMet progressed through early-stage trials in 2024-2025, while China’s approval of SKB107 signaled widening geographic uptake. Actinium-225 PSMA therapy achieved 65% PSA50 responses in resistant prostate cancer, demonstrating disease-modifying potential that accelerates the Bone metastasis market trajectory. Investments exceeding USD 200 million by industry leaders are targeting isotope production scale-up to alleviate supply constraints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of biologics and radiopharmaceuticals | -2.30% | Global; pronounced in emerging markets | Short term (≤ 2 years) |

| Delayed diagnosis in low-resource settings | -1.80% | Sub-Saharan Africa, parts of Asia Pacific, Latin America | Long term (≥ 4 years) |

| Reimbursement caps on skeletal events | -1.40% | North America & EU; influence private insurers | Medium term (2-4 years) |

| Radioisotope supply-chain bottlenecks | -1.10% | Global; acute where central production dominates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologics and Radiopharmaceutical Therapies

Pricing around USD 3,400 per Xgeva injection restricts uptake in self-pay markets, and Chinese datasets show medicines consuming half of annual metastatic prostate budgets. Radiopharmaceuticals add logistics overhead from radiation safety compliance, lifting overall therapeutic costs. Biosimilars may soften list prices by as much as 30% once litigation hurdles clear, but near-term affordability remains an obstacle to the diffusion of the Bone metastasis market.

Delayed Diagnosis in Low-Resource Settings

Median time to specialist care surpasses 8 months in several African series, so patients present with extensive skeletal compromise that diminishes therapy effectiveness. Thailand’s rise in spinal-metastasis surgeries underscores how late presentation tilts practice toward invasive interventions over pharmacologic prevention. Tele-oncology and point-of-care imaging are emerging to bridge access gaps and open underserved populations to the Bone metastasis market.[3]Journal of Korean Neurosurgical Society, “Trends in spinal metastasis surgery,” jkns.or.kr

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Radiopharmaceutical Acceleration

Radiopharmaceuticals are forecast to post a 13.6% CAGR through 2030, the quickest within the Bone metastasis market, because they deliver tumoricidal activity and palliation concurrently. Bisphosphonates preserved the largest 20.3% slice of the 2024 Bone metastasis market size owing to entrenched guidelines and cost familiarity, yet RANK-L inhibitors face share erosion following February 2025 patent expiry. Chinese trials with 68Ga/177Lu-DOTA-ibandronate delivered 82% pain-relief rates, evidencing regional innovation primed to reshape competitive dynamics.

Established bisphosphonate users remain sizeable, but payers increasingly fund agents that cut hospitalization risk. Radiopharmaceutical developers are responding with vertically integrated supply chains that guard isotope availability and support the growth of the Bone metastasis market. Combination regimens pairing radiopharmaceuticals with immune checkpoint inhibitors are entering mid-phase studies, signaling further pipeline momentum.

By Cancer Type: Breast Cancer Dominance with Lung Cancer Upswing

Breast cancer accounted for 17.7% of the bone metastasis market share in 2024, owing to its high skeletal tropism and survivorship that prolongs therapy duration. Lung cancer, propelled by improving systemic survival, is on track for the fastest 11.4% CAGR to 2030. Prostate cancer remains a foundational volume driver because more than two-thirds of men with metastatic disease exhibit skeletal lesions.

Segment demand is nuanced by biology: osteolytic breast lesions require anti-resorptive emphasis, while osteoblastic prostate lesions favor radiopharmaceutical approaches. Peru’s registry showed 26% five-year survival when metastasis was bone-only, encouraging clinicians to intensify bone-focused control strategies. These patterns reinforce the heterogeneity that companies must address to deepen penetration of the Bone metastasis market.

By Route of Administration: Subcutaneous Preference

Intravenous formulations maintained 20.2% of the Bone metastasis market size in 2024, upheld by clinician familiarity and hospital workflows. Subcutaneous options are scaling at 9.3% CAGR because they shift care to outpatient settings, shrink chair time, and align with patient convenience. Oral bisphosphonates confront adherence barriers, limiting share growth.

Focused ultrasound and other image-guided ablation modalities broaden the treatment toolbox without systemic exposure, complementing pharmacologic options and expanding addressable spend in the Bone metastasis market. Manufacturers are reformulating legacy IV molecules into high-concentration pre-filled syringes to ride the subcutaneous wave.

By End User: Ambulatory Expansion

Hospitals held 20.8% of Bone metastasis market size in 2024 thanks to complex infusion setups and acute management needs. Ambulatory surgical centers, however, are on an 8.6% CAGR runway to 2030. Tailwinds include payer push to lower-cost sites and the arrival of subcutaneous biologics that require minimal infrastructure.

Dedicated cancer centers leverage multidisciplinary teams to coordinate imaging, surgery, systemic therapy, and palliative care under one roof, sustaining meaningful volume. Academic institutions continue to seed innovation, feeding clinical-trial participants into the wider Bone metastasis market ecosystem.

Geography Analysis

North America retained the largest 19.9% slice of the Bone metastasis market in 2024. Reimbursement frameworks cover most bone-modifying drugs, and Medicare’s 2025 policy update broadens medication therapy management for skeletal disease, likely improving adherence. Research collaboration networks accelerate protocol refinement, ensuring rapid assimilation of radiopharmaceutical innovations.

Asia Pacific delivers the fastest 9.9% CAGR outlook, powered by demographic aging, industrialized healthcare buildouts, and domestic radiopharmaceutical production that trims import costs. China’s scale-up in nuclear medicine capacity positions regional manufacturers as export suppliers, further reinforcing the expansion of the Bone metastasis market. Japan’s super-aged society fuels steady demand, while India’s tiered oncology rollout is adding linear accelerators and PET-CT units that expand diagnostic throughput.

Europe posts balanced growth backed by universal coverage and early biosimilar adoption, illustrated by the May 2024 denosumab biosimilar approval. Germany and the United Kingdom pioneer value-based reimbursement pilots that reward skeletal-event avoidance. In parallel, the Middle East, Africa, and South America remain nascent but strategically important, as increasing private-sector oncology investment catalyzes penetration of the Bone metastasis market.

Competitive Landscape

Competition is moderate: the top five players control near-60% of global revenue, yet biosimilar pressure and specialist entrants are flattening share curves. Amgen’s Prolia and Xgeva delivered combined Q1 2025 sales of USD 1.666 billion but face January 2025 biosimilar launches that could erode volumes. Novartis committed more than USD 200 million to U.S. isotope capacity to secure upstream supply advantages in radiopharmaceuticals.

Acquisition activity centers on nuclear medicine assets. Bristol Myers Squibb’s USD 4.1 billion RayzeBio purchase and Lantheus’s USD 1 billion Evergreen buyout illustrate the premium on alpha-emitting expertise. Start-ups pursue theranostic pairings that combine diagnostic scans with matched therapy, aiming for precision dosing that further differentiates offerings within the Bone metastasis market.

Barriers persist in isotope half-life intricacies demand tight logistics, and global radioisotope shortages occasionally suspend dosing schedules, highlighting the value of vertically integrated models. AI-enabled imaging partnerships are emerging as non-traditional differentiators, giving suppliers data footprints that help clinicians track skeletal tumor burden in real time and buttress the Bone metastasis industry’s push toward outcome-based contracts.

Bone Metastasis Industry Leaders

Novartis AG

Bayer AG

Amgen Inc.

Johnson & Johnson

AstraZeneca PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Lilly closed its acquisition of Point Biopharma, securing targeted alpha therapy platforms for late-stage skeletal disease.

- March 2025: China’s NMPA approved SKB107, the nation’s first domestically developed radiopharmaceutical for bone metastases.

- February 2025: The FDA cleared trastuzumab deruxtecan for HER2-low metastatic breast cancer, extending targeted therapy to patients with dominant bone lesions.

- September 2024: Novartis announced USD 200 million to expand U.S. radioligand production in Carlsbad and Indianapolis.

Global Bone Metastasis Market Report Scope

| Bisphosphonates |

| RANK-L Inhibitors (Denosumab etc.) |

| Radiopharmaceuticals |

| Hormonal Therapies |

| Chemotherapy |

| Immunotherapy |

| Analgesics & Supportive Care |

| Breast Cancer |

| Prostate Cancer |

| Lung Cancer |

| Renal Cell Carcinoma |

| Thyroid Cancer |

| Intravenous |

| Sub-cutaneous |

| Oral |

| Hospitals |

| Cancer Centers & Specialty Clinics |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Bisphosphonates | |

| RANK-L Inhibitors (Denosumab etc.) | ||

| Radiopharmaceuticals | ||

| Hormonal Therapies | ||

| Chemotherapy | ||

| Immunotherapy | ||

| Analgesics & Supportive Care | ||

| By Cancer Type | Breast Cancer | |

| Prostate Cancer | ||

| Lung Cancer | ||

| Renal Cell Carcinoma | ||

| Thyroid Cancer | ||

| By Route of Administration | Intravenous | |

| Sub-cutaneous | ||

| Oral | ||

| By End User | Hospitals | |

| Cancer Centers & Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Bone metastasis market?

The Bone metastasis market size was USD 21.1 billion in 2025 and is forecast to climb to USD 34.5 billion by 2030.

Which therapy segment is growing fastest?

Radiopharmaceuticals are expanding at a 13.6% CAGR through 2030 due to their disease-modifying potential and widening regulatory approvals.

Why is Asia Pacific the fastest-growing region?

Demographic aging, rapid oncology infrastructure build-outs, and domestic isotope production support a 9.9% CAGR outlook for Asia Pacific.

How will biosimilars affect pricing?

Denosumab biosimilars launching from 2025 could trim treatment costs by as much as 30%, increasing affordability in price-sensitive markets.

What are the main cost drivers in bone metastasis care?

High biologic prices, radioisotope supply logistics, and hospital stays for skeletal events together shape total spending, averaging USD 65,000 per event in Europe.

Which policy shifts favor market growth?

Medicare’s bundled radiation payments and expanded medication therapy management for bone disease incentivize preventive treatment and improve reimbursement access.

Page last updated on: