Metastatic Melanoma Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

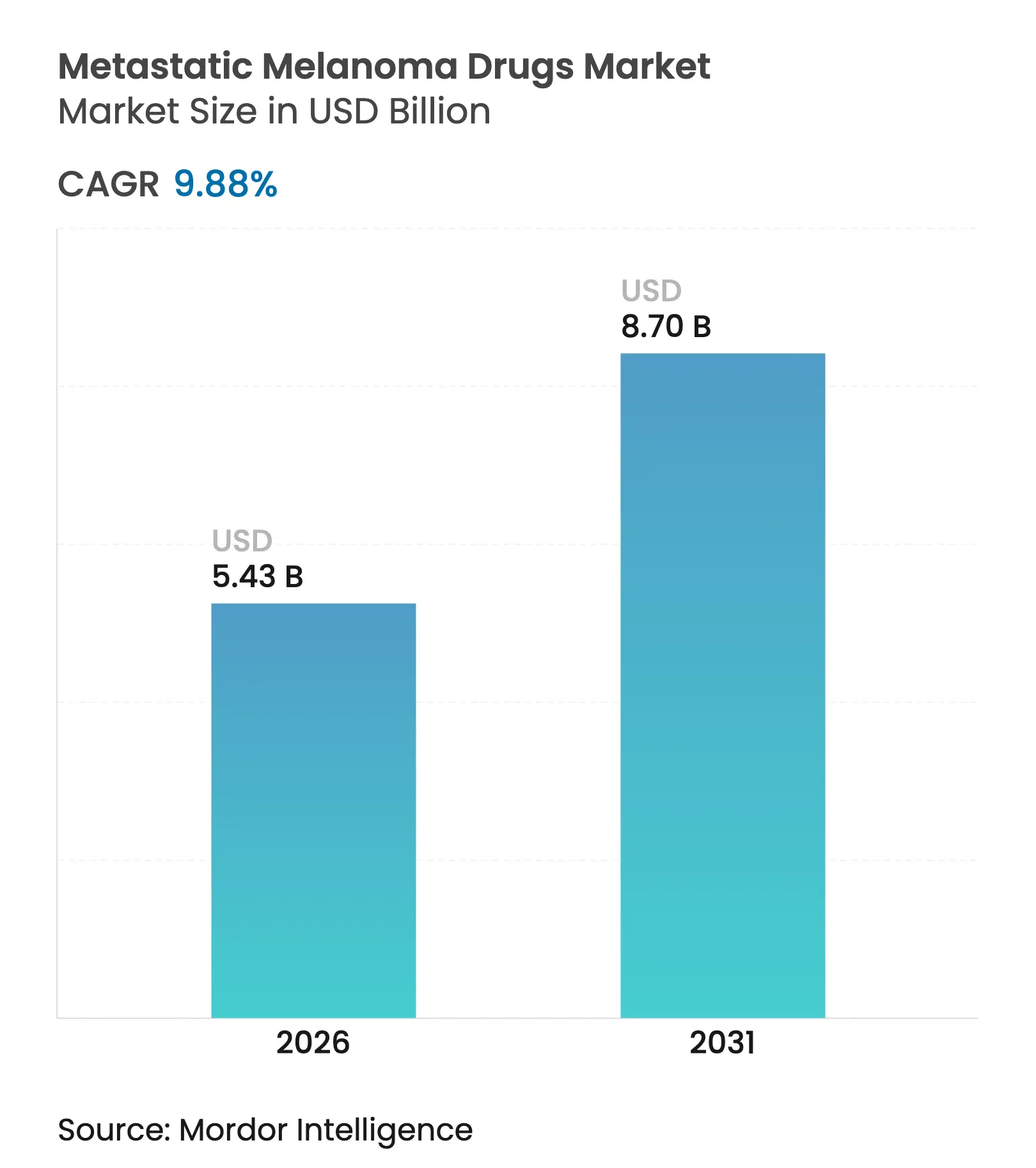

| Market Size (2026) | USD 5.43 Billion |

| Market Size (2031) | USD 8.7 Billion |

| Growth Rate (2026 - 2031) | 9.88 % CAGR |

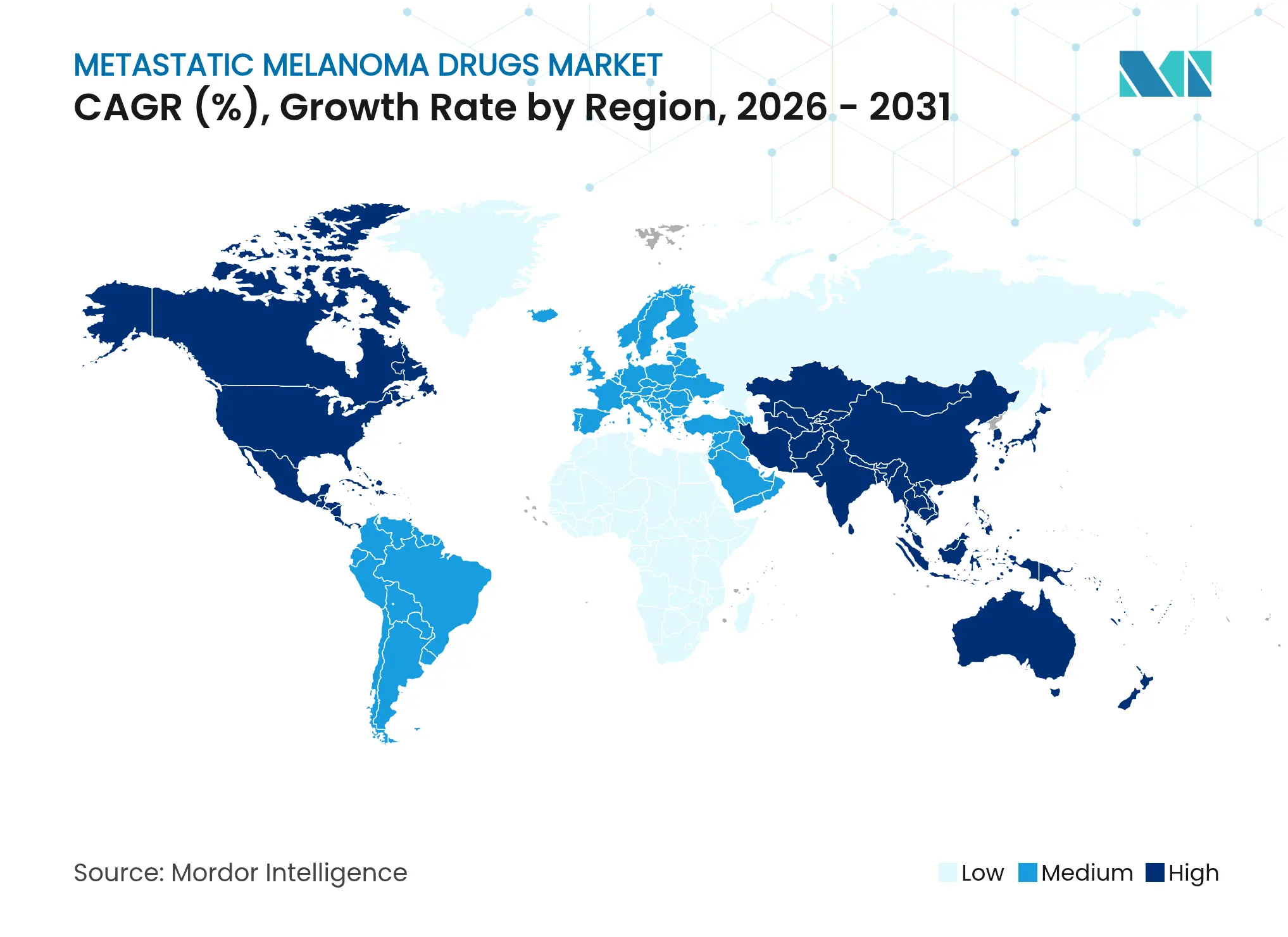

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

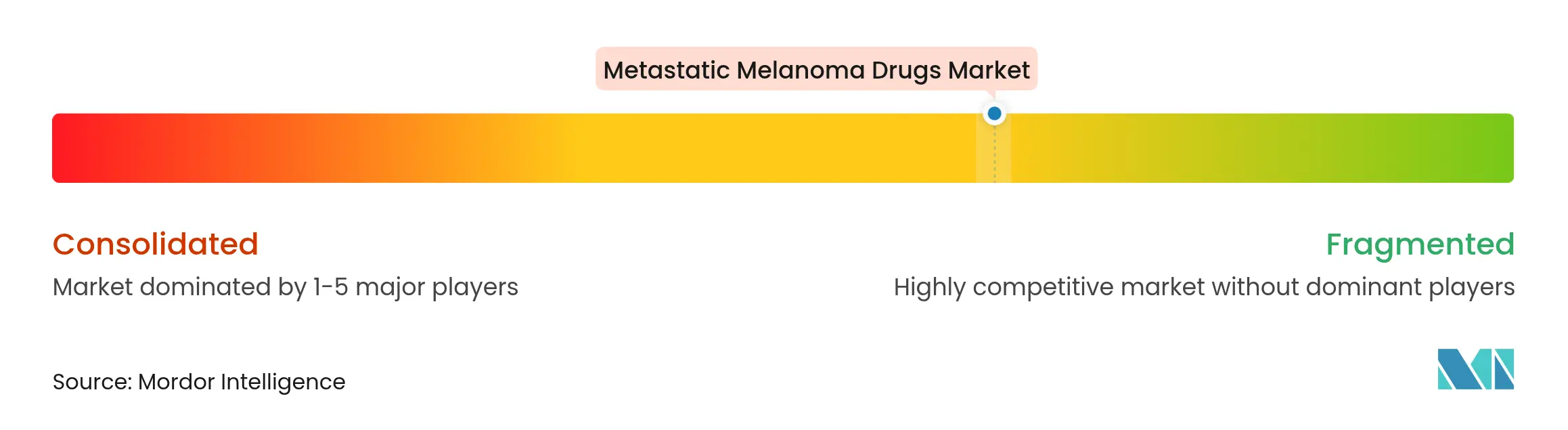

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Metastatic Melanoma Drugs Market Analysis by Mordor Intelligence

The metastatic melanoma drugs market size was valued at USD 4.94 billion in 2025 and estimated to grow from USD 5.43 billion in 2026 to reach USD 8.7 billion by 2031, at a CAGR of 9.88% during the forecast period (2026-2031). Demand rises on the back of durable immunotherapy responses, next-generation targeted options and wider reimbursement adoption that reduce financial toxicity for patients. Consistent clinical evidence showing decade-long survival benefits with dual checkpoint blockade sustains physician confidence, while pipeline breakthroughs such as tumor-infiltrating lymphocyte therapy expand the armamentarium. Delivery innovation through intratumoral regimens cuts systemic toxicity, and AI-guided discovery tools shorten development timelines. Heightened competition emerges as leading players defend first-line dominance against biotech newcomers introducing oncolytic viruses, bispecific antibodies and radiopharmaceuticals.

Key Report Takeaways

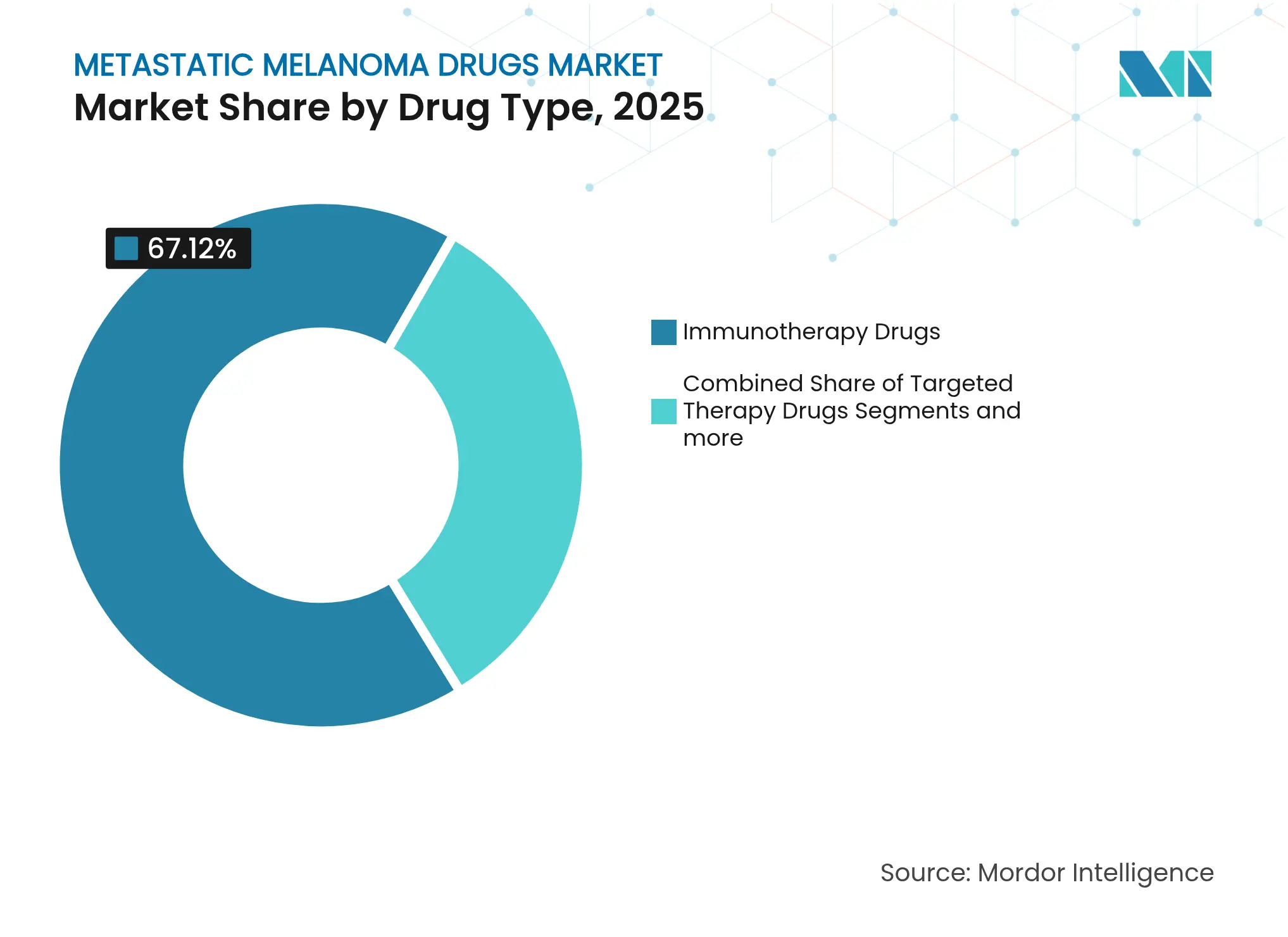

- By drug type, immunotherapy led with 67.12% revenue share in 2025, while targeted therapy is projected to expand at a 10.62% CAGR through 2031.

- By mechanism of action, immune checkpoint inhibition captured 69.85% of metastatic melanoma drugs market share in 2025, whereas oncolytic virus-mediated cytotoxicity advances at a 10.55% CAGR to 2031.

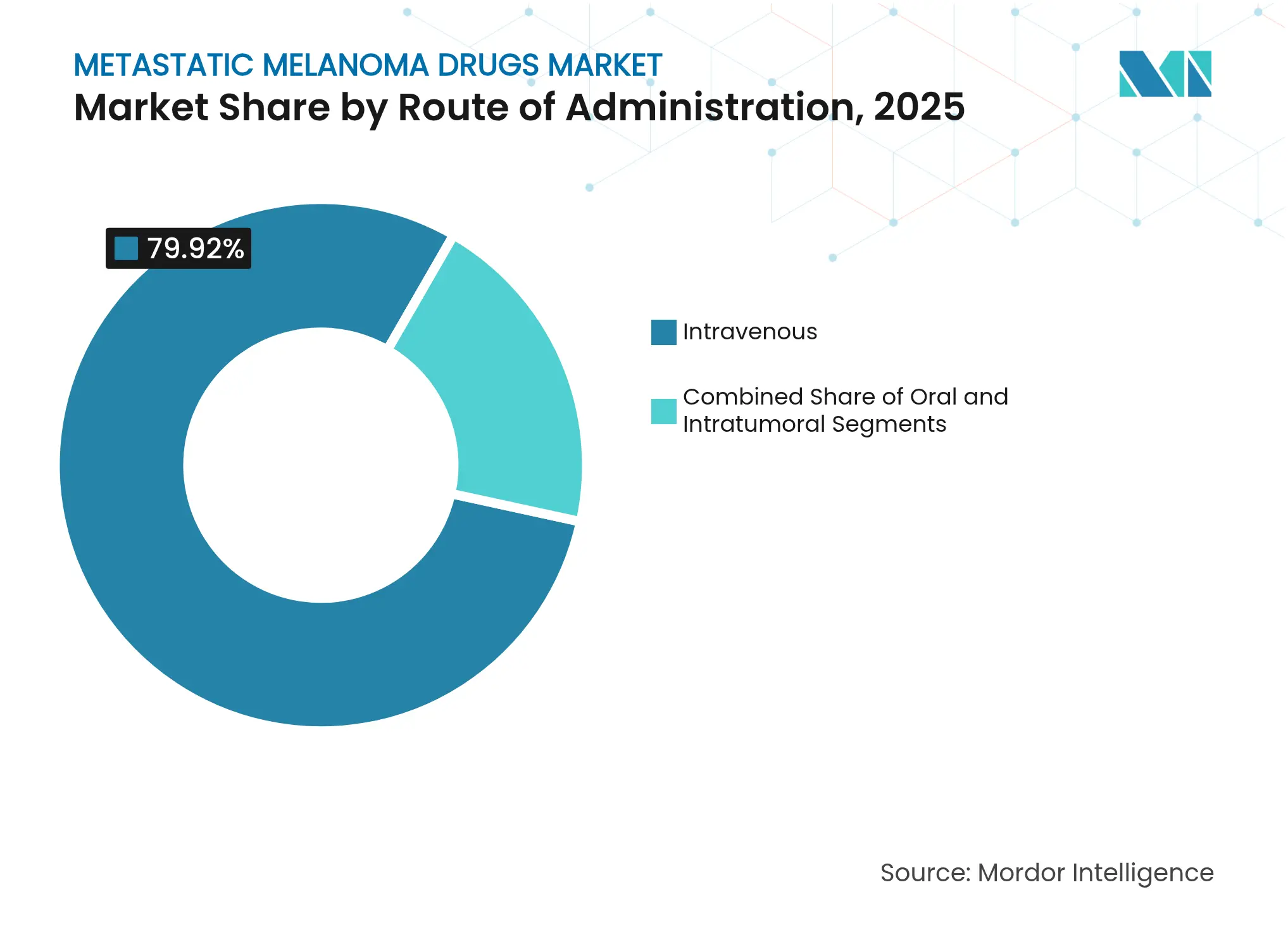

- By route of administration, intravenous therapy accounted for 79.92% of the metastatic melanoma drugs market size in 2025; intratumoral delivery is forecast to rise at a 10.46% CAGR through 2031.

- By distribution channel, hospital pharmacies held 59.22% share of the metastatic melanoma drugs market in 2025, while retail pharmacies show the fastest expansion at a 10.57% CAGR to 2031.

- By geography, North America commanded 39.55% share in 2025 and Asia-Pacific records the highest projected CAGR of 10.72% up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metastatic Melanoma Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing incidence of metastatic melanoma

Increasing incidence of metastatic melanoma

| +2.1% | Global, with highest rates in North America & Australia | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+2.1% |

Geographic Relevance

:

Global, with highest rates in North America &

Australia

|

Impact Timeline

:

Long term (≥ 4 years)

|

Technological advancements in immuno-oncology

Technological advancements in immuno-oncology

| +2.8% | Global, led by US & EU regulatory approvals | Medium term (2-4 years) | |||

Rising development of novel biologics

Rising development of novel biologics

| +1.9% | North America & EU core, expansion to APAC | Medium term (2-4 years) | |||

Favorable reimbursement & access programs

Favorable reimbursement & access programs

| +1.4% | Primarily developed markets (US, EU, Japan) | Short term (≤ 2 years) | |||

AI-driven melanoma drug discovery acceleration

AI-driven melanoma drug discovery acceleration

| +1.2% | North America & EU, with emerging APAC adoption | Medium term (2-4 years) | |||

Tumor-agnostic regulatory approvals expanding label use

Tumor-agnostic regulatory approvals expanding label use

| +0.9% | Global, led by FDA and EMA pathways | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Incidence of Metastatic Melanoma

Rising case numbers underpin long-run demand as the global burden grows, illustrated by China’s 313.5% jump in incidence between 1990 and 2021 [1]Yu-hong Xiao, “Burden of Melanoma in China, 1990-2021,” Frontiers in Public Health, frontiersin.org. Higher ultraviolet exposure, aging demographics and broader diagnostic access sustain a patient pool that requires advanced therapy. Men aged 55-59 register the highest risk, guiding screening initiatives and clinical trial stratification. The concentration of new cases in coastal provinces mirrors epidemiology in Australia and parts of the United States, reinforcing universal preventive campaigns. Strong incidence signals translate into prioritized R&D budgets and encourage payers to widen coverage windows, solidifying volume expansion through 2030.

Technological Advancements in Immuno-Oncology

Checkpoint blockade longevity is now proven, with the CheckMate-067 decade review showing 43% survival for nivolumab plus ipilimumab versus pre-immunotherapy results near 25% [2]Bristol-Myers Squibb, “CheckMate-067 Ten-Year Survival Data,” BMS.com. Molecular engineering extends beyond PD-1 and CTLA-4 to novel targets like LAG-3, revitalizing progress in refractory populations. Algorithms that parse single-cell data predict responders, trimming trial size and accelerating approvals. Such precision curtails unnecessary exposure to severe irAEs and positions combination protocols earlier in treatment sequencing. Consequently, developers emphasize modular design platforms that allow rapid plug-and-play of new epitopes, sustaining the metastatic melanoma drugs market trajectory.

Rising Development of Novel Biologics

February 2024 marked the first tumor-infiltrating lymphocyte approval with lifileucel, achieving a 31.5% objective response in heavily pre-treated patients [3]U.S. Food and Drug Administration, "FDA grants accelerated approval to lifileucel for unresectable or metastatic melanoma," fda.gov. Oncolytic viruses like RP1 combine direct tumor lysis with systemic immune activation, producing 33.6% responses post anti-PD-1 failure and pending a July 2025 FDA decision. Bispecific formats, such as Merck’s LM-299 that targets PD-1 and VEGF, address immune escape plus angiogenesis in one molecule. These modalities diversify revenue streams and shorten clinic infusion times, appealing to providers managing crowded oncology schedules.

Favorable Reimbursement and Access Programs

Medicare’s negotiation framework takes effect in January 2026 and is set to lower out-of-pocket oncology costs by USD 6 billion for ten drugs. The Prescription Payment Plan spreads annual payments, improving adherence and hospital cash flow. European conditional authorizations fast-track innovative agents, evidenced by multiple oncology products receiving positive EMA opinions during 2024-2025. Collectively, these mechanisms reduce financial friction and quicken adoption curves, raising the metastatic melanoma drugs market size across developed economies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High risk of immune-related adverse events

High risk of immune-related adverse events

| -1.6% | Global, particularly affecting combination therapies | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.6%

|

Geographic Relevance

:

Global, particularly affecting combination therapies

|

Impact Timeline

:

Medium term (2-4 years)

|

High cost of treatment

High cost of treatment

| -2.2% | Global, most pronounced in emerging markets | Long term (≥ 4 years) | |||

Biosimilar price pressure on branded therapies

Biosimilar price pressure on branded therapies

| -0.8% | Developed markets with established biosimilar pathways | Medium term (2-4 years) | |||

Limited biomarker validation for combination regimens

Limited biomarker validation for combination regimens

| -1.1% | Global, affecting precision medicine adoption | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Risk of Immune-Related Adverse Events

Around 80% of irAEs manifest within three months of treatment start and vary by regimen. Dual checkpoint blockade elevates gastrointestinal and hepatic toxicities, while emerging LAG-3 combinations heighten cardiovascular concerns. Institutions deploy natural language processing to flag early symptoms, yet corticosteroid use still spans 17.3% to 57.4% across organ systems. These complexities necessitate immunology expertise and may deter smaller centers from offering advanced regimens, restraining metastatic melanoma drugs market penetration in under-resourced geographies.

High Cost of Treatment

Median list prices exceed USD 373,000 for autologous cell therapies, and supply chain intermediaries capture disproportionate margins, squeezing provider economics. Latin America sees only 4% of oncology trials, delaying regional approvals and curbing reimbursement coverage. Denial of larotrectinib in Brazil during 2022 typifies the challenge of integrating novel agents into public systems. Persistent affordability gaps slow uptake despite clinical merit, trimming the overall metastatic melanoma drugs market CAGR.

Segment Analysis

By Drug Type: Immunotherapy Dominance Drives Market Evolution

Immunotherapy retained 67.12% of 2025 revenue, underlining its anchoring role in modern algorithms. Combination regimens that blend PD-1 inhibitors with CTLA-4 or BRAF/MEK blockade deliver durable benefits, and lifileucel now offers a cell-based salvage option. Targeted therapy grows fastest at 10.62% CAGR as resistance-modifying triplets reach 63-75% response levels. Chemotherapy continues to support palliative intent in select settings.

The metastatic melanoma drugs market size for immunotherapy will widen as payers back long progression-free intervals that lower downstream costs. In contrast, targeted agents strengthen first-line positioning in BRAF-mutant disease and function as pre-immunotherapy debulking tools. Competitive tension rises as branded combinations seek niche differentiation through safety profiles rather than efficacy alone.

Note: Segment shares of all individual segments available upon report purchase

By Mechanism of Action: Checkpoint Innovation Expands Beyond PD-1

Immune checkpoint inhibition held 69.85% of metastatic melanoma drugs market share in 2025, justified by survival plateaus unseen with earlier treatments. Oncolytic viruses post a 10.55% CAGR, buoyed by superior intratumoral delivery techniques. Signal pathway inhibition sustains commitment via eight-year survival gains from BRAF/MEK pairs, while adoptive transfer techniques open a bespoke segment despite manufacturing constraints.

Pipeline analysis suggests multi-mechanism cocktails could surpass single-target durability, integrating viral, antibody and cell therapy components within sequential protocols. Regulators encourage such innovation by aligning tumor-agnostic approvals that streamline label expansion, quickening metastatic melanoma drugs market growth.

By Route of Administration: Intratumoral Delivery Gains Momentum

Intravenous methods represented 79.92% of 2025 spending because monoclonal antibodies dominate volumes. Nonetheless, intratumoral injections expand at 10.46% CAGR as real-time ultrasound guidance enables accurate deep organ dosing with minimal systemic exposure.

The metastatic melanoma drugs market size for intratumoral regimens remains small but accelerates as patient preference tilts toward reduced infusion center visits. Oral agents retain utility for outpatient management yet require pharmacist oversight to mitigate drug–drug interactions.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Hospital Integration Transforms Access

Hospital pharmacies manage 59.22% of prescriptions given the need for sterile compounding, step-up monitoring and prompt irAE intervention. Retail channels rise at 10.57% CAGR in line with greater oral therapy share and the proliferation of medically integrated dispensing models.

Online services secure foothold through supportive medications, although biologic cold-chain needs restrict scale. The metastatic melanoma drugs market share of hospital settings may plateau as home infusion technologies mature.

Geography Analysis

North America controlled 39.55% of 2025 revenue thanks to strong payer coverage, dense trial networks and rapid FDA approvals such as lifileucel. Medicare’s negotiation policy supports continued volume growth, while academic centers pioneer combination regimens that then diffuse into the community.

Asia-Pacific logs an 10.72% CAGR driven by China’s steep incidence uptick and rising disposable income. National regulators approve domestic PD-1 agents at price points below imported therapy, broadening access. Yet real-world effectiveness lags Western outcomes due to later stage presentation, spotlighting education efforts and earlier diagnosis.

Europe benefits from EMA conditional approvals that shorten time-to-market for breakthrough agents. Local health technology assessments still cap pricing flexibility, but pan-EU initiatives promote uniform access. Conversely, Latin America’s limited trial footprint, fragmented insurance models and import duties impede state-of-the-art adoption. These disparities underscore untapped metastatic melanoma drugs market expansion potential once logistical and policy barriers ease.

Competitive Landscape

Market Concentration

Industry concentration remains moderate, with Bristol-Myers Squibb leading through Opdualag’s 30% first-line share and a broad immunotherapy franchise valued at USD 2.5 billion in Q4 2024 revenue. Merck leverages pembrolizumab back-bone status while stacking pipeline assets such as LM-299 and mRNA-4157 in multidimensional regimens. Iovance commands first mover advantage in cell therapy, and Replimune primes the viral therapy segment with RP1 nearing approval.

Strategic deals accelerate capability building. Bristol-Myers Squibb absorbed RayzeBio for USD 4.1 billion to diversify into radiopharmaceuticals that may rescue post-checkpoint failures. Joint ventures like Moderna–Merck apply mRNA technology to generate neoantigen vaccines that personalize immunity. AI platforms embedded across discovery workflows slash cycle times and identify resistance pathways, raising competitive hurdles for entrants lacking data infrastructure.

Barriers also stem from manufacturing sophistication. Commercial-scale TIL production demands closed-system bioreactors and cryogenic logistics, assets held by few companies. These high fixed costs raise thresholds for meaningful entry, steering the metastatic melanoma drugs market toward specialized, well-capitalized operators.

Metastatic Melanoma Drugs Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: FDA granted priority review to RP1 plus nivolumab for advanced melanoma after anti-PD-1 failure, with a July 22 2025 decision date based on 33.6% response in the IGNYTE trial.

- July 2024: Iovance Biotherapeutics filed an EMA application for lifileucel, positioning the first TIL therapy for EU approval.

- June 2024: Moderna and Merck reported three-year data showing mRNA-4157 combined with pembrolizumab improved recurrence-free survival versus pembrolizumab alone.

- February 2024: FDA granted accelerated approval to lifileucel for unresectable or metastatic melanoma with a 31.5% objective response in heavily pre-treated patients.

Table of Contents for Metastatic Melanoma Drugs Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing incidence of metastatic melanoma

- 4.2.2Technological advancements in immuno-oncology

- 4.2.3Rising development of novel biologics

- 4.2.4Favorable reimbursement & access programs

- 4.2.5AI-driven melanoma drug discovery acceleration

- 4.2.6Tumor-agnostic regulatory approvals expanding label use

- 4.3Market Restraints

- 4.3.1High risk of immune-related adverse events

- 4.3.2High cost of treatment

- 4.3.3Biosimilar price pressure on branded therapies

- 4.3.4Limited biomarker validation for combination regimens

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1by Drug Type

- 5.1.1Immunotherapy Drugs

- 5.1.2Targeted Therapy Drugs

- 5.1.3Chemotherapy Drugs

- 5.2By Mechanism of Action

- 5.2.1Immune Checkpoint Inhibition

- 5.2.2Signal Pathway Inhibition

- 5.2.3Oncolytic Virus-mediated Cytotoxicity

- 5.2.4Adoptive T-Cell Transfer

- 5.3By Route of Administration

- 5.3.1Intravenous

- 5.3.2Oral

- 5.3.3Intratumoral

- 5.4By Distribution Channel

- 5.4.1Hospital Pharmacies

- 5.4.2Retail Pharmacies

- 5.4.3Online Pharmacies

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Bristol-Myers Squibb Company

- 6.3.2Merck & Co., Inc.

- 6.3.3Novartis AG

- 6.3.4F. Hoffmann-La Roche Ltd

- 6.3.5Pfizer Inc.

- 6.3.6Amgen Inc.

- 6.3.7AstraZeneca plc

- 6.3.8Sanofi

- 6.3.9Incyte Corporation

- 6.3.10Regeneron Pharmaceuticals

- 6.3.11BeiGene Ltd.

- 6.3.12Exelixis Inc.

- 6.3.13Takeda Pharmaceutical Co.

- 6.3.14Daiichi Sankyo Co.

- 6.3.15Eisai Co., Ltd.

- 6.3.16Accord Healthcare

- 6.3.17Amneal Pharmaceuticals LLC

- 6.3.18Innovent Biologics

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Metastatic Melanoma Drugs Market Report Scope

As per the scope of the report, metastatic melanoma is a disease that occurs when the cancerous cells from the original tumor (primary tumor) get loose, spread by traveling through the lymph or blood circulation, and start a new tumor (metastatic tumor) somewhere else. The metastatic melanoma drugs are used to treat patients who are suffering from this advanced stage of melanoma. The metastatic melanoma drugs market is segmented by drug type (chemotherapy drugs, immunotherapy drugs, and targeted therapy drugs), end-user (hospitals, specialty clinics, and other end-users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.