Demineralized Bone Matrix Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

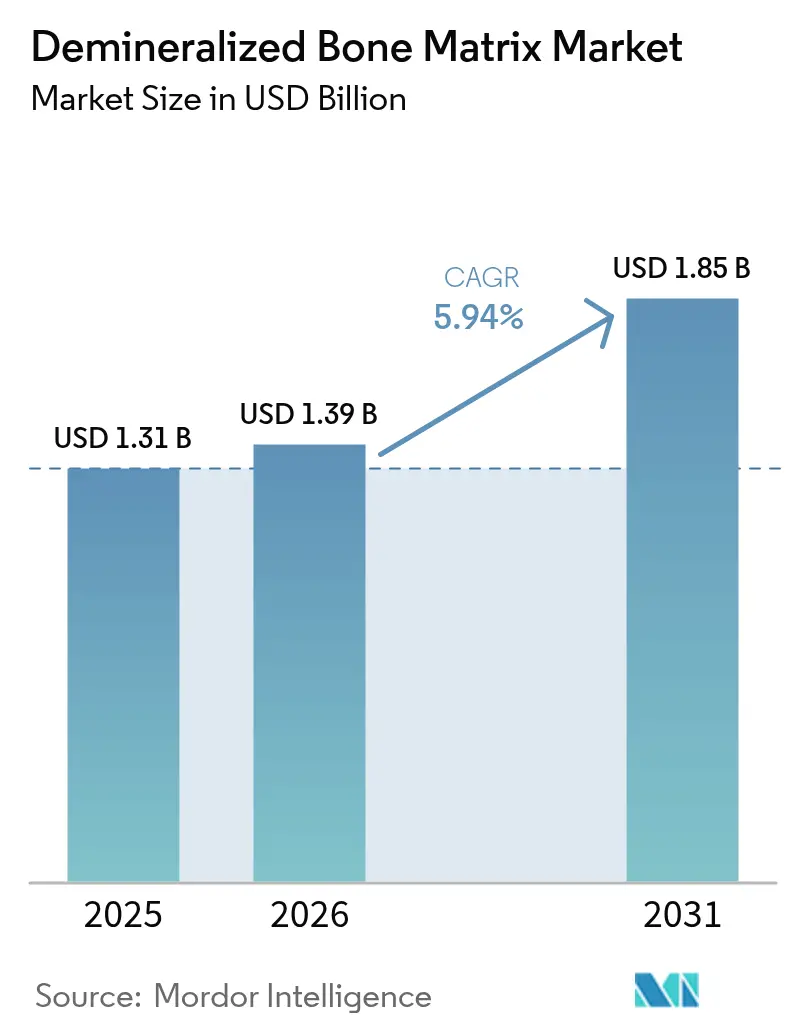

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 5.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

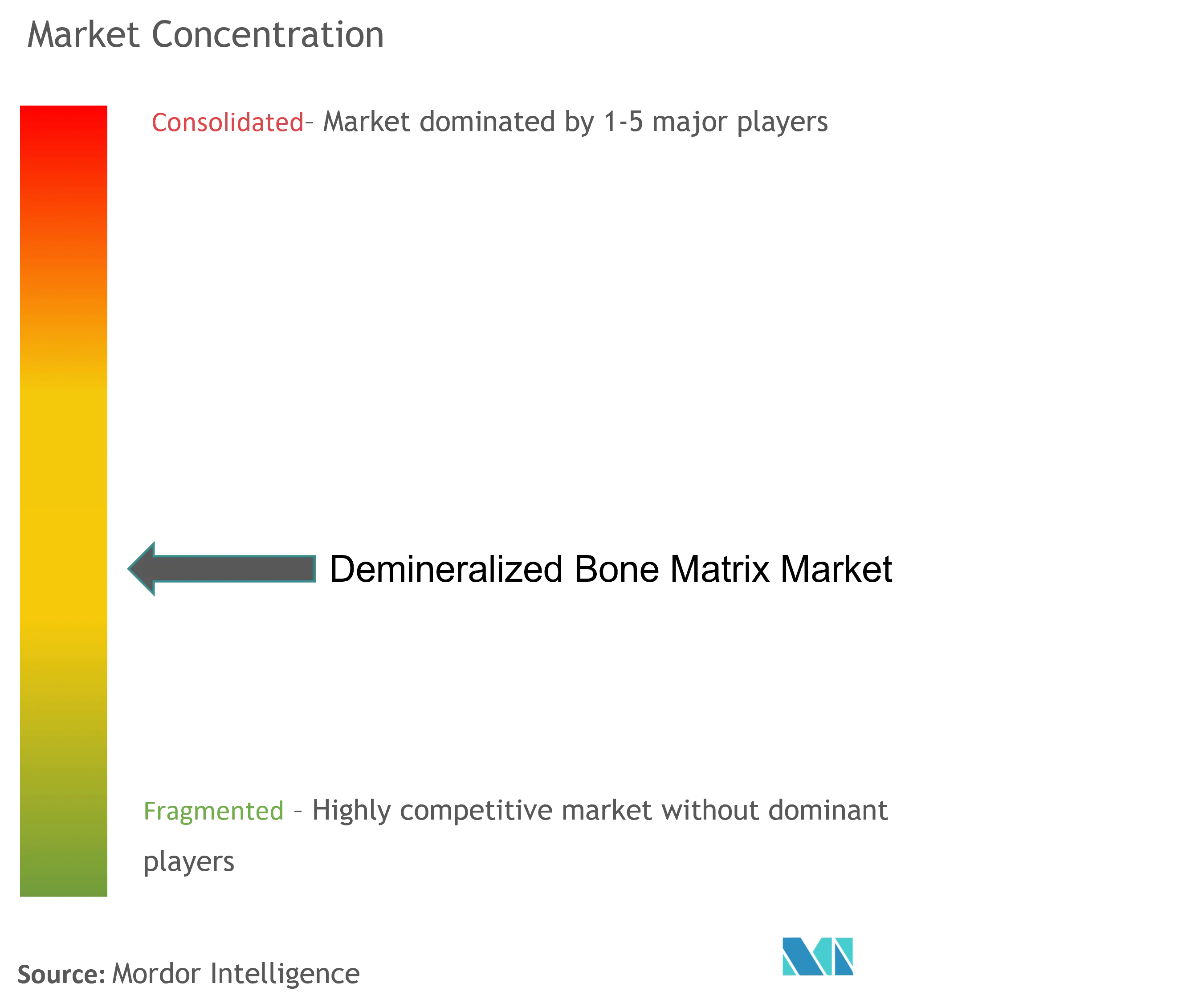

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Demineralized Bone Matrix Market Analysis by Mordor Intelligence

The demineralized bone matrix market size is expected to grow from USD 1.31 billion in 2025 to USD 1.39 billion in 2026 and is forecast to reach USD 1.85 billion by 2031 at 5.94% CAGR over 2026-2031. Growth reflects a shift from a niche orthobiologic to a mainstream grafting option as aging populations swell surgical volumes and tissue-processing innovations improve product reliability. Putty formats, cortical fiber advances, and viable‐cell matrices give surgeons biologic activity unavailable with synthetics while eliminating autograft morbidity. Regulatory tightening since January 2025 favors manufacturers that can document donor screening and sterility, shielding compliant players from low-quality competition[1]U.S. Food & Drug Administration, “Human Cells, Tissues, and Cellular and Tissue-Based Products Guidance,” fda.gov. Simultaneously, payers expanding coverage for biologic grafts in spine and dental indications temper reimbursement headwinds and help stabilize product pricing in developed markets.

Key Report Takeaways

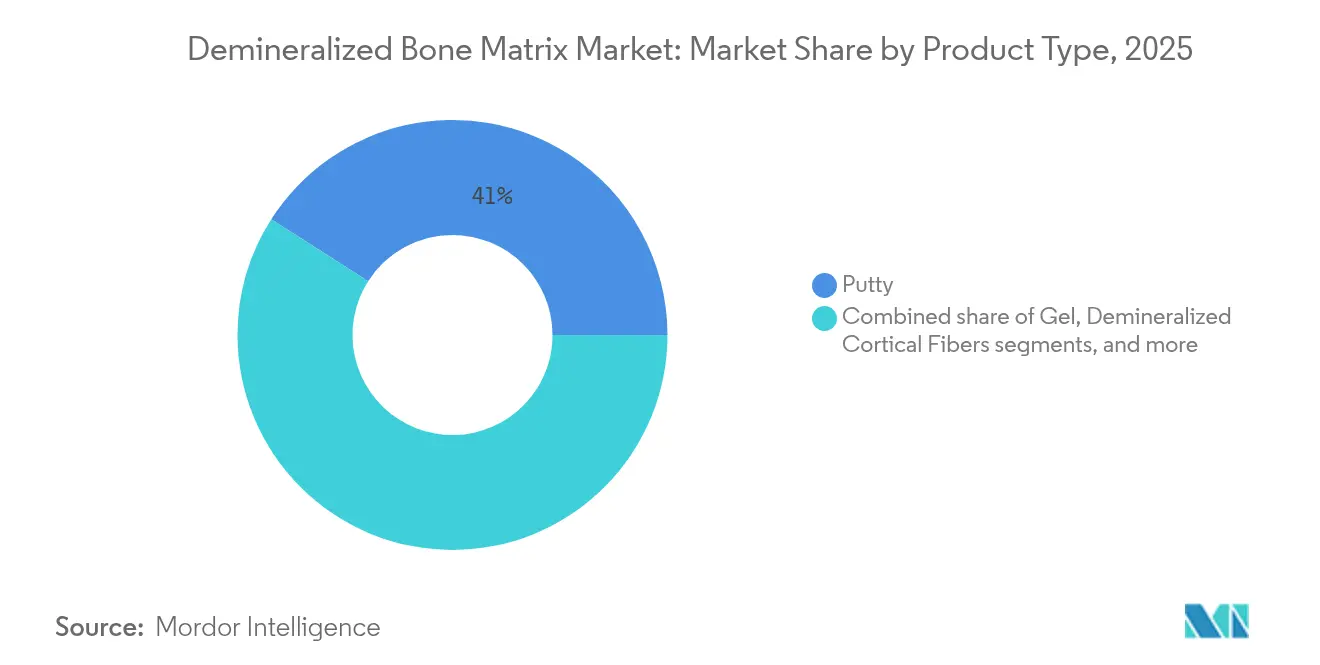

- By product type, putty formulations led with 40.96% revenue share in 2025; demineralized cortical fibers are projected to grow at an 8.02% CAGR through 2031.

- By form, cancellous allografts accounted for 44.15% of the demineralized bone matrix market share in 2025, while combined allograft–synthetic formats are set to expand at a 7.21% CAGR to 2031.

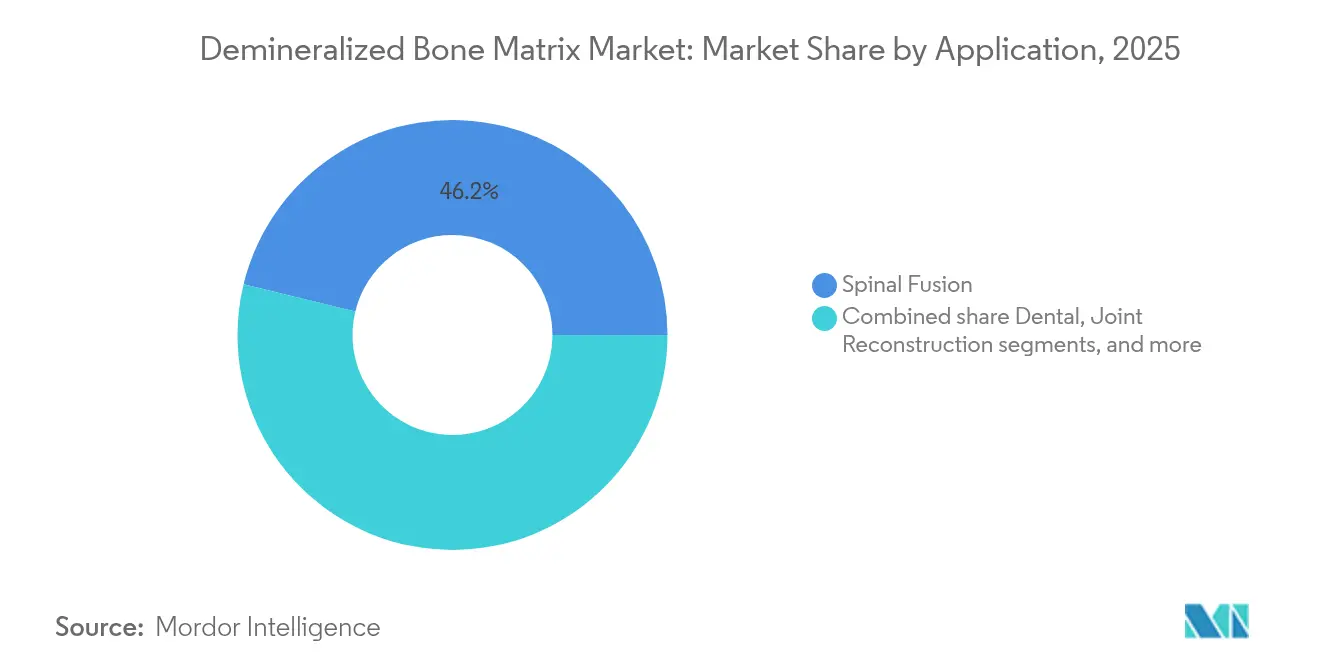

- By application, spinal fusion held 46.21% of the demineralized bone matrix market size in 2025; dental procedures are advancing at an 8.62% CAGR through 2031.

- By end-user, hospitals controlled 62.88% of 2025 revenue, whereas dental clinics lead growth with a 8.97% CAGR out to 2031.

- By geography, North America commanded 50.74% revenue share in 2025; Asia-Pacific is the fastest-growing region at 7.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Demineralized Bone Matrix Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising musculoskeletal disease prevalence | +1.8% | North America & Europe; aging populations globally | Long term (≥ 4 years) |

| Increasing volume of reconstructive surgeries | +1.5% | Global, led by Asia-Pacific | Medium term (2-4 years) |

| Expanding adoption of dental implants | +1.2% | North America & Europe; expanding in Asia-Pacific | Medium term (2-4 years) |

| Broadening reimbursement coverage for biologic grafts | +0.8% | North America & Europe | Short term (≤ 2 years) |

| Innovation in patient-specific demineralized bone constructs | +0.7% | Early adoption in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Musculoskeletal Disease Prevalence

Osteoporosis-related fractures are projected to top 60,000 annually in Australia by 2050, illustrating how aging populations anchor long-range demand for grafting biomaterials[2]OTA International, “Global Hip Fracture Burden,” otainternational.org. Posterior cervical fusion for deformity expanded at fastest CAGR, highlighting a sustained need for biologically active grafts to secure arthrodesis in compromised bone. Manufacturers respond with osteoporotic-specific putties that incorporate carriers enhancing protein release in low-density scaffolds. Health systems, facing higher fragility fracture admissions, increasingly reimburse DBM when autograft harvest adds morbidity and cost, embedding the demineralized bone matrix market into geriatric orthopedic care pathways.

Increasing Volume of Reconstructive Surgeries

Lumbar degenerative spondylolisthesis fusion procedures rose 387.1% from 2010-2022, whereas decompression-only growth lagged at 79.6%, underscoring surgeon preference for fusion-enhancing biologics[3]E-Neurospine, “Trends in Lumbar Spondylolisthesis Surgery,” eneurospine.org. Shoulder arthroplasty prevalence reached 0.258% of the U.S. population in 2017, and revisions climbed 392% over 15 years, compounding DBM demand in hardware exchange and bone-loss management. Minimally invasive techniques favor injectable DBM gels that fill confined defects without extending incision length. As procedure counts rise across orthopedics and sports medicine, hospitals adopt standardized DBM kits, cementing the demineralized bone matrix market as a staple rather than an exception.

Expanding Adoption of Dental Implants

DBM paired with barrier membranes reduces post-extraction ridge resorption, improving implant primary stability and lowering revision rates. Systematic reviews confirm superior periodontal outcomes versus debridement alone, prompting insurers to cover grafts for infrabony defects and ridge preservation. Injectable hydrogels incorporating platelet-rich fibrin simplify chair-side preparation, broadening adoption by general dentists. Dental uptake diversifies revenue streams and elevates the demineralized bone matrix market’s visibility beyond the orthopedic arena.

Broadening Reimbursement Coverage for Biologic Grafts

Aetna and other large payers now deem DBM medically necessary for spinal fusion and cartilage defect filling, giving surgeons billing clarity and reducing reliance on cost-capped autograft. Although Medicare reimbursements for joint replacements fell 44-51% from 2013-2021, private coverage expansion offsets some margin compression and encourages evidence-based use of higher-priced biologics. The policy environment thus both constrains and catalyzes growth, steering the demineralized bone matrix market toward value-based care narratives linked to shorter OR times and reduced revision rates.

Innovation in Patient-Specific Demineralized Bone Constructs

The FDA’s clearance of restor3d’s total talus replacement, produced with patient-matched 3D printing, signals regulatory openness to personalized biologics. Composite scaffolds weaving DBM with additive-manufactured lattices show 100% union in hindfoot cases and are emerging in complex spine oncology where defect geometry is unique. NIR-triggered shape-memory carriers further enable surgeon-controlled conformance to irregular cavities, aiming to cut operative fiddling time. These advances differentiate suppliers and fortify premium pricing within the demineralized bone matrix market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of demineralized bone matrix products | -1.2% | Global; most acute in price-sensitive markets | Short term (≤ 2 years) |

| Potential for immunogenic response and infection | -0.8% | Global; impact varies by regulatory rigor | Medium term (2-4 years) |

| Intensifying regulatory oversight of donor tissue | -0.6% | North America & Europe | Long term (≥ 4 years) |

| Growing competition from synthetic bone graft alternatives | -0.9% | Global, driven by cost-conscious health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Demineralized Bone Matrix Products

Medicare payment erosion creates scrutiny on per-case costs, pressing hospitals to quantify outcome gains over less costly synthetics. DBM also carries logistics expenses for cryostorage, validated shipping, and donor serology. In lower-income markets, surgeons default to calcium phosphate blocks when budgets are fixed, delaying penetration of the demineralized bone matrix industry.

Potential for Immunogenic Response and Infection

A 51% drainage rate and 34% deep infection with calcium sulfate-DBM putty prompted product withdrawals and heightened vigilance on processing consistency. Microscopic audits reveal residual cellular debris even in “fully demineralized” grafts, fostering hesitancy among infection-averse spine surgeons. These safety debates slow adoption until suppliers publish lot-to-lot performance data and pathogen-inactivation protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Putty Dominates Injectable Innovation

Putty held 40.96% of 2025 revenue, cementing the demineralized bone matrix market share lead by virtue of moldability and wash-out resistance during irrigation. Surgeons pack the cohesive mass against decorticated bone, trusting carrier polymers to retain proteins at the fusion site. Demineralized cortical fibers, although only emerging, post an 8.02% CAGR thanks to interlocking fibrils that mimic autograft chips and flow through MIS cannulas without clogging. In trauma cases, fibers mixed with autologous marrow shorten graft prep time and offset limited iliac crest volume. Gel syringes still appeal in dental sockets where flow fills voids under thin cortical plates. Strips and sheets fill cranial vault reconstructions, yet remain niche.

A parallel trend is carrier upgrade. Recent formulations swap glycerol for hyaluronic acid, increasing protein stability at room temperature and cutting thaw time in the operating room. Vendors promoting putty now co-package PRP activators, nudging procedure-average selling prices upward. Such differentiation keeps putty at the center of the demineralized bone matrix market even as fibers chase MIS share.

By Form: Cancellous Allografts Lead Combination Growth

Cancellous morsels captured 44.15% of 2025 sales, buoyed by trabecular porosity that speeds vascular ingrowth and cell migration—traits critical when surgeons bridge long-segment thoracolumbar constructs. The demineralized bone matrix market size for these cancellous products is forecast to climb steadily as hybrid graft packs pair morsels with collagen-rich DBM putty, allowing immediate structural bulk plus osteoinductive signal. Combined allograft–synthetic formats grow fastest at a 7.21% CAGR because ceramic granules lend compressive strength and resist resorption where load sharing is high.

Cortical dowels retain value in revision hip arthroplasty where diaphyseal voids need column support. Yet, adoption is limited due to machining costs and screw fixation complexity. Cryopreserved viable matrices—containing native mesenchymal progenitors—entered the market following Enovis’s 2024 distribution deal and target foot-and-ankle charcot arthropathy, offering live-cell remodeling without autograft harvest. Form diversification thus helps suppliers appeal to sub-specialty nuances, reinforcing the demineralized bone matrix market’s resilience against single-format obsolescence.

By Application: Dental Procedures Accelerate Beyond Spinal Dominance

Spinal fusion still claims 46.21% of 2025 revenue and remains the anchor for the demineralized bone matrix market. Multi-level lumbar fusions, boosted by sagittal balance awareness, consume up to three 10 cc syringes per case, dwarfing unit volumes in other specialties. Yet dental indications, projected to rise at 8.62% CAGR, are shrinking the spinal dominance gap. Sinus lifts and ridge preservation require only 1-2 cc, but procedure counts dwarf spine numbers, and chair-side usage is spreading beyond periodontists to general practitioners.

Cranio-maxillofacial trauma, joint reconstruction, and foot-and-ankle arthrodesis collectively add incremental volume. Meta-analysis of hindfoot fusions reports an 85.6% union rate when DBM augments hardware—comforting data for orthopedic subspecialists hesitant about biologics. This breadth of indications anchors the demineralized bone matrix industry against cyclicality in any single surgical line.

By End-User: Dental Clinics Drive Ambulatory Growth

Hospitals held 62.88% of 2025 sales due to complex spine and trauma workflows that still require operating theaters and perioperative teams. Nonetheless, dental clinics deliver the fastest growth at 8.97% CAGR on the back of in-office cone-beam CT planning and immediate implant placement protocols. Clinic buyers prefer single-use 1 cc syringes and value ambient-stable putties that bypass cold chain complexities. The shift pushes distributors to adopt just-in-time models, supporting new revenue channels within the demineralized bone matrix market.

Specialty orthopedics centers also expand share, especially in the United States where bundled payments reward volume efficiency. Such centers negotiate bulk DBM contracts tied to infection-reduction metrics, nudging suppliers to supply audit data down to the donor ID level. As ambulatory environments grow, manufacturers are redesigning kit sizes and field-ready thaw devices to suit the workflow.

Geography Analysis

North America contributed 50.74% of 2025 revenue, supported by well-defined reimbursement codes, 25-year product familiarity, and a dense network of AATB-accredited tissue banks. Yet falling Medicare joint replacement fees pressure hospital margins, forcing procurement teams to scrutinize biologic premiums and encouraging price negotiations inside the demineralized bone matrix market. FDA guidance effective February 2025 further elevates compliance hurdles, a shift expected to consolidate volume into large processors possessing in-house nucleic acid testing.

Asia-Pacific is the fastest-growing geography at 7.29% CAGR through 2031. Hip fracture incidence in China is projected to double between 2020-2035, while Japan faces a median age above 48 years, heightening orthopedic caseloads. Governments adding universal health coverage improve access to spinal procedures, yet reimbursement caps still favor competitively priced putty vials. Multinationals are partnering with domestic tissue banks in South Korea and India to localize supply and navigate diverse regulatory filings. These collaborations enlarge the demineralized bone matrix market while laying the groundwork for future personalized constructs.

Europe delivers steady single-digit growth as aging demographics offset slower procedural adoption curves. Variation in tissue directives among EU members complicates cross-border distribution, prompting suppliers to establish redundant processing hubs in Germany and Italy. Post-Brexit UK regulators align closely with MHRA guidance, mirroring FDA documentation requirements and favoring suppliers who already operate in North America. Meanwhile, Middle East & Africa and South America remain nascent but promising; Colombia’s lower-limb arthroplasty CAGR of 5.54% signals rising Latin American orthopedic volumes. Currency volatility and tender-driven purchasing temper immediate uptake, yet tier-two hospitals show interest where synthetic options underperform.

Regulatory Landscape

Demineralized bone matrix (DBM) products are regulated through a mix of human tissue controls and medical device requirements, with classification and intended use determining the regulatory pathway. In the United States, many DBM products are regulated as Class II devices, commonly aligned with resorbable bone void filler categories. When products incorporate carriers or additives, the regulatory posture can require clearer positioning as a device versus a combination product, which may overlap with the FDA Office of Combination Products early in the process.

A major compliance anchor is the FDA Quality Management System Regulation transition that incorporates ISO 13485:2016, with an effective date of February 2, 2026. This raises expectations for design controls, supplier management, and traceability. In Europe, DBM and other non-viable tissue-based graft substitutes are governed under the Medical Device Regulation (EU) 2017/745, with consolidated status in 2026 and added emphasis on clinical evaluation, post-market surveillance, and consistent labeling for cross-border commercial activity.

Competitive Landscape

The demineralized bone matrix market is moderately concentrated. Medtronic, Stryker, and Johnson & Johnson leverage global distribution and 25-year clinical track records to retain preference lists. Grafton DBM alone has featured in more than 1.5 million surgeries, a data trove newer entrants cannot yet match. Stryker posted 11.5% organic sales growth in Orthopaedics and Spine for Q3 2024, reflecting cross-selling of DBM with its implant portfolio. Johnson & Johnson, through DePuy Synthes, bundles DBM with expandable cages, highlighting a trend toward procedural packages.

Innovation drives differentiation. Enovis partnered with Ossium in 2024 to distribute cryopreserved viable matrices that maintain live donor cells, aiming at complex hindfoot fusions where biology is paramount. Restor3d’s 3D-printed composites integrate DBM and titanium, targeting oncology resections. Start-ups are exploring hydrogels that release BMP-2 under near-infrared stimulation, potentially reducing supraphysiologic dosing concerns. Synthetic competitors intensify price pressure: NuVasive’s Attrax ceramic demonstrated comparable fusion rates to DBM in posterolateral lumbar studies, incentivizing hospitals to trial non-biologic options.

Regulatory dynamics shape competition. FDA’s 2025 tissue guidances expand inspection scope, adding cost and complexity. Well-capitalized players view this as a barrier shielding share, whereas smaller processors may seek acquisition. M&A remains active: Zimmer Biomet’s February 2025 announcement of a Paragon 28 buyout shows incumbents purchasing specialty portfolios to penetrate foot-and-ankle growth pockets where DBM usage per case is rising. Collectively, these strategic moves ensure the demineralized bone matrix market remains dynamic and innovation-driven rather than commoditized.

Demineralized Bone Matrix Industry Leaders

Medtronic

Stryker

Johnson & Johnson (DePuy Synthes)

Zimmer Biomet

Exactech, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are strongest where products and channels fit tightening compliance and workflow needs, especially minimally invasive spine procedures and office-based dental grafting. Putty and fiber formats that provide predictable handling through cannulas and for small defects support continued movement toward injectable and carrier-optimized systems. At the same time, the FDA QMSR framework aligned to ISO 13485:2016 (effective February 2, 2026) supports tighter documentation, lot-to-lot traceability, and cross-site procurement practices.

The opportunity set is also broadening beyond traditional DBM-only portfolios, as competitors expand bone graft substitute offerings and use more structured distribution models for contracting with hospitals and dental clinics. A concrete signal is DePuy Synthes entering an exclusive distribution agreement for CGBIOs NOVOSIS across the United States, Canada, and Australia in May 2026, alongside a planned FDA IDE study in the second half of 2026. This evidence-building and channel expansion points to continued demand for upgraded carriers, procedure-specific kits, and more complete clinical and real-world evidence packages in spine and dental indications.

Recent Industry Developments

- May 2026: DePuy Synthes (Johnson & Johnson) entered an exclusive distribution agreement with CGBIO for NOVOSIS in the United States, Canada, and Australia. The collaboration also established a steering committee to guide joint development priorities, with an FDA IDE study planned for the second half of 2026. The agreement expands DePuy Synthes presence in bone graft substitutes and reinforces portfolio-based selling alongside implants in key developed markets.

- March 2026: MTF Biologics and Kolosis BIO announced the DBX Fiber line expansion within the DBX demineralized bone matrix family for spine and orthopedic procedures. This expands handling and delivery options for surgeons and adds incremental competitive pressure on traditional putties and gels in higher-value indications.

- February 2026: Medtronic announced U.S. FDA approval for expanded use of INFUSE Bone Graft in one- and two-level transforaminal lumbar interbody fusion TLIF procedures. The approval widens access to a premium, evidence-backed graft option within interbody fusion workflows. It increases pressure on DBM suppliers to differentiate through handling, indication-specific evidence, and contracting as surgeons and hospitals reassess biologic choices for TLIF.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from demineralized bone matrix (DBM) products used in surgical bone grafting to support bone repair and fusion, and sold through standard clinical commercial channels.

Scope exclusions: autografts, xenografts, and fully synthetic bone graft substitutes are excluded from this market sizing.

Segmentation Overview

- By Product Type

- Gel

- Putty

- Demineralized Cortical Fibers

- Other Product Types

- By Form

- Allograft (Cortical)

- Allograft (Cancellous)

- Combined Allograft & Synthetics

- By Application

- Spinal Fusion

- Dental

- Joint Reconstruction

- Craniomaxillofacial

- Trauma & Extremities

- Other Applications

- By End-User

- Hospitals

- Specialty Orthopedic Centers

- Dental Clinics

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping how DBM is produced and where it is used clinically, so our sizing stays tied to procedure demand and product adoption. We use public sources such as the US FDA database for clearance information, the US CDC and OECD health statistics for procedure and population context, and macro indicators from the World Bank that influence healthcare spending.

To tighten assumptions, we also review company annual reports and earnings decks, plus medical society or association websites that discuss spine, trauma, and orthopedic procedure volumes. Patent databases are used to track formulation activity and product-format innovation (for example, putty and fiber formats). An import and export shipment-level database is used selectively to sanity-check trade flow direction for relevant biologic material categories. These examples are not exhaustive, and other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys are used to pressure-test desk assumptions around DBM use per procedure, pricing bands by product format, and how often surgeons substitute DBM with adjacent graft options. We speak with manufacturers, distributors, hospital procurement contacts, and clinicians across major regions, so the final adoption and mix assumptions reflect how DBM is actually purchased and used, not only how it is described in public narratives.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 49% |

| Mid tier: 57% | Functional/Unit leaders: 41% | EMEA: 31% |

| Smaller Players: 17% | Managers: 44% | Americas: 20% |

Market-Sizing & Forecasting

The core model uses a top-down demand pool approach, where orthopedic and spine procedure volumes are translated into DBM consumption using adoption rates and typical usage per case. That consumption is then converted into value using observed ASP ranges. To reduce reliance on any single viewpoint, we corroborate totals with selective bottom-up approximations, such as rolling up sampled supplier revenues by region and doing channel checks on price points and mix.

Key DBM drivers include spinal fusion and trauma procedure trends, aging population indicators, hospital and ambulatory surgical center case mix, DBM format mix shifts (for example, putty versus fiber), reimbursement and coverage signals for grafting procedures, and local currency impacts for imported materials. When a bottom-up data point is missing for a smaller country, we fill the gap using proxy adoption assumptions based on similar clinical practice patterns, and then we revisit the proxy with interviews.

For forecasting, we run scenario analysis supported by a simple multivariate regression overlay for procedure growth and healthcare spend signals. We then apply expert-reviewed adjustments when a guideline change, supply constraint, or pricing reset is expected to alter the trajectory.

Data Validation & Update Cycle

Outputs are checked through multiple passes. We start with internal consistency tests across regions and year-over-year movement, then move to variance checks against independent signals like procedure growth and reported performance cues in public filings. Any outliers lead to a re-check of key assumptions, and if needed we reconnect with interviewees to confirm whether the movement reflects a real market shift or a data artifact.

Before sign-off, the model is reviewed by another analyst for calculation integrity and scope alignment, and the narrative is reconciled to the final tables. The reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass so clients receive the most current view.

Mordor Intelligence's Demineralized Bone Matrix Market Sizing Compared With Other Published Estimates

Published market values for DBM can differ even when the topic appears to describe the same products, because counted product boundaries, the base year, and the price and volume assumptions are not always aligned. We summarize these differences using a publisher-by-publisher comparison, so buyers can see which modeling choices contribute to the spread.

Procedure-volume signals and product-scope checks are the two anchors used to keep Mordor Intelligence's estimate tied to human-sourced DBM sold for clinical implantation. As a result, adjacent graft categories and non-comparable tissue sources are not blended into the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.31 B (2025) | |

| Independent Research House A | USD 1.24 B (2024) | Uses an earlier base year and does not clearly separate DBM-only revenue from neighboring bone graft substitute spend in all regions, which can shift the total when procedure and pricing assumptions are rolled forward. |

| Industry Publisher B | USD 1.06 B (2024) | Includes tissue-source scope that can extend beyond human allograft DBM and applies a broader segmentation lens, so the counted pool and the implied ASP trajectory can differ from a DBM-only commercial-channel view. |

The comparison indicates that most of the variance comes from scope boundaries and the year used for anchoring prices and procedure volumes. With clear inclusion rules and repeatable demand indicators, our total stays traceable to what is actually used and purchased in DBM procedures.

Key Questions Answered in the Report

What is the projected growth rate for the demineralized bone matrix market?

The market is forecast to grow at a 5.94% CAGR between 2026 and 2031.

Which region shows the fastest expansion?

Asia-Pacific leads with a projected 7.29% CAGR through 2031, driven by aging demographics and expanding surgical infrastructure.

Why are dental clinics gaining prominence in DBM demand?

Rising implant volumes and office-based ridge preservation procedures are pushing dental clinics to adopt small-volume injectable DBM, creating a 8.97% CAGR growth segment.

What product type currently dominates market revenue?

Putty formulations hold 40.96% of 2025 revenue because of their moldability and ease of use across spine and trauma surgeries.

How is regulation affecting DBM suppliers?

The FDA’s 2025 guidance on donor eligibility increases compliance costs, likely consolidating market share among tissue banks with robust screening and testing capabilities.

Are synthetic grafts replacing DBM?

Synthetics are growing but have not matched DBM’s osteoinductive biology; hybrid products combining DBM with ceramics are instead emerging to blend benefits of both materials.

Page last updated on: