Dental Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.14 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Cement Market Analysis by Mordor Intelligence

Dental cement market size in 2026 is estimated at USD 1.63 billion, growing from 2025 value of USD 1.54 billion with 2031 projections showing USD 2.14 billion, growing at 5.62% CAGR over 2026-2031. Momentum stems from a confluence of demographic pressures, rising procedural volumes, and technological progress in bio-active and nano-hybrid formulations that improve longevity and aesthetics. The European Union’s mercury amalgam ban, effective January 2025, has triggered rapid substitution toward fluoride-releasing, mercury-free cements and similar legislation is proliferating in other regions. Digital workflows in CAD/CAM and 3-D printing continue to widen the indications for advanced cement systems, while artificial intelligence is refining material selection and placement protocols. Supply-chain friction in specialty monomers and rare-earth fillers poses a headwind, yet manufacturers with diversified sourcing and validated regulatory dossiers maintain pricing power in premium segments.

Key Report Takeaways

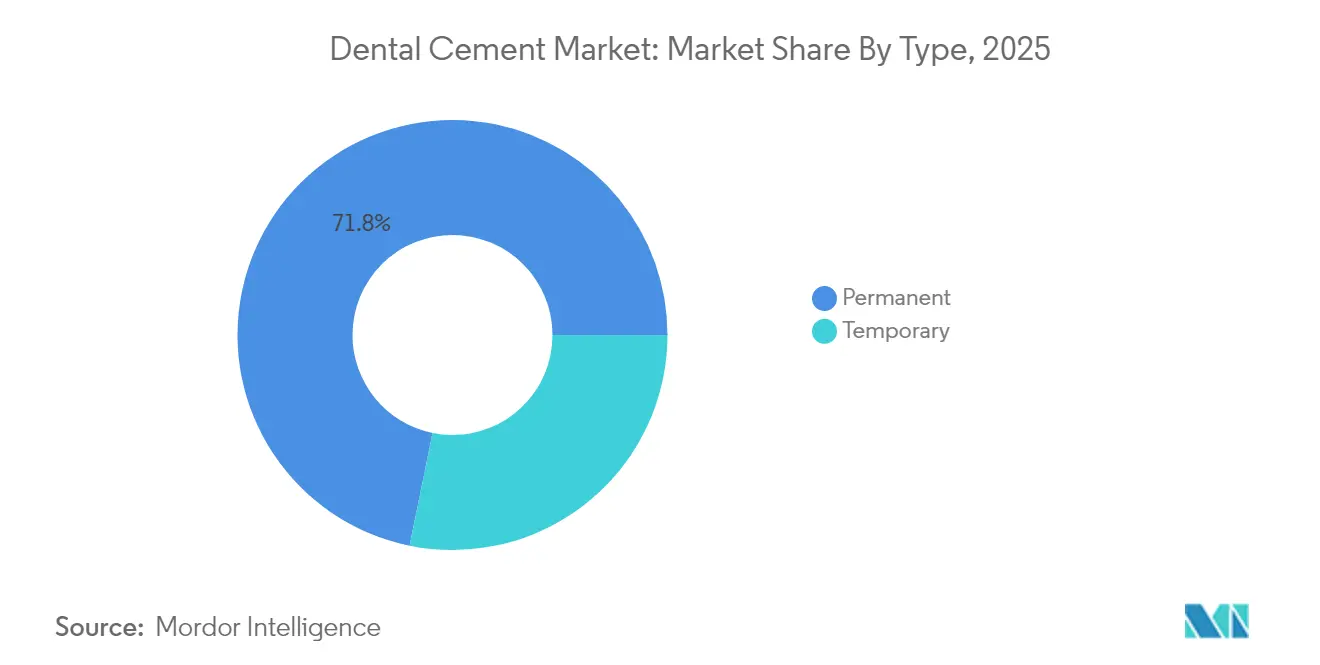

- By type, permanent cements led with 71.80% of the dental cement market share in 2025, whereas temporary cements are projected to advance at a 6.15% CAGR through 2031.

- By material, glass ionomer captured 31.05% revenue share in 2025; bio-active resin cements are forecast to expand at a 6.95% CAGR to 2031.

- By application, restorations accounted for a 38.90% share of the dental cement market size in 2025; surgical dressing applications show the fastest growth at an 7.65% CAGR through 2031.

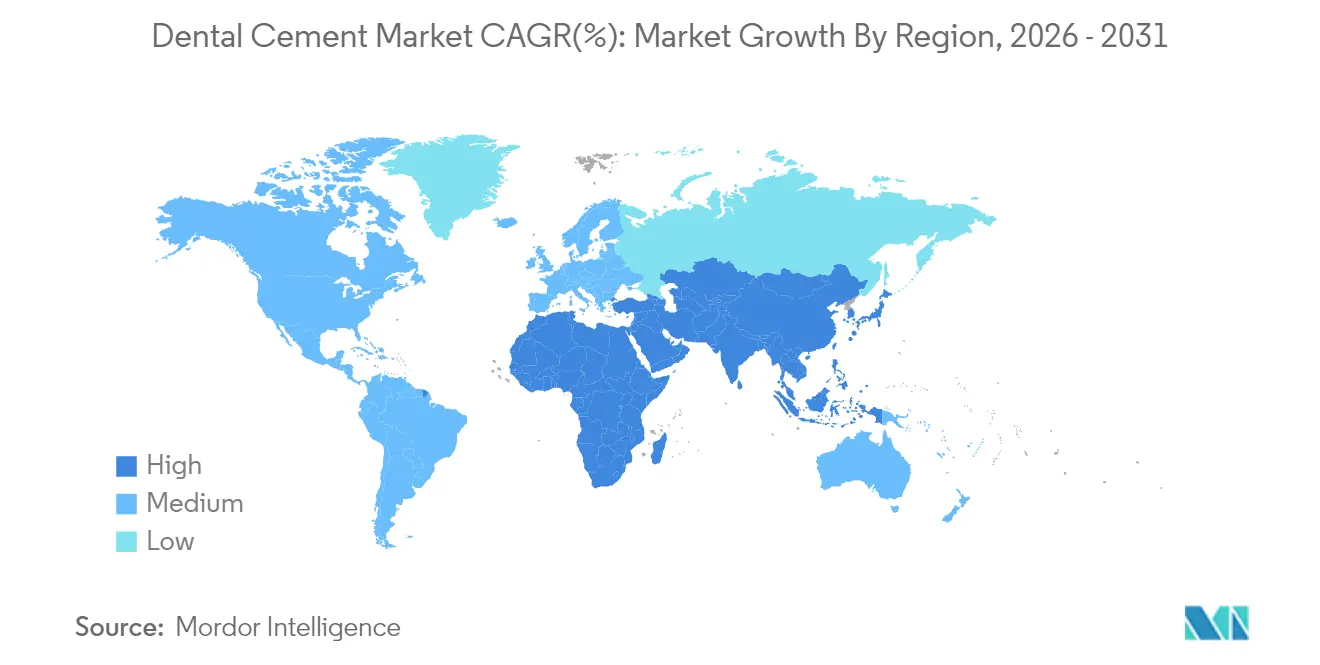

- By geography, North America commanded 39.05% of the dental cement market share in 2025, while Asia-Pacific is progressing at a 6.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Cement Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of dental caries and edentulism | +1.2% | Global, with higher impact in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Increasing orthodontic & prosthodontic procedure volumes | +1.0% | North America & Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth of cosmetic / aesthetic dentistry | +0.8% | North America & Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Regulatory push toward mercury-free, fluoride-releasing restoratives | +1.5% | Europe immediate, North America following, Global adoption | Short term (≤ 2 years) |

| Rapid emergence of bio-active & nano-hybrid cement technologies | +0.9% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries and Edentulism

Untreated dental caries affected nearly 3.5 billion people in 2024, establishing a persistent clinical workload that sustains the dental cement market. Aging demographics elevate edentulism rates and heighten demand for durable prosthodontic solutions that rely on high-strength permanent cements. The global economic burden—USD 387 billion in direct costs and USD 323 billion in indirect costs—reinforces the need for cements that minimize retreatment cycles. Manufacturers that demonstrate bio-activity, fluoride release, and simplified workflows strengthen adoption among cost-sensitive providers within the dental cement market.

Increasing Orthodontic & Prosthodontic Procedure Volumes

Surveys indicate 20.6% of young adults intend to pursue aligner therapy, intensifying demand for cements compatible with ceramic brackets and clear-aligner attachments. Prosthodontics is scaling as CAD/CAM and 3-D printing shorten chair time and elevate aesthetics, driving need for cements that bond to zirconia, lithium-disilicate, and polymer-infiltrated ceramics. Integration of robotics and AI in prosthodontics raises performance benchmarks for bond strength and marginal integrity. These factors reinforce long-term demand trajectories in the dental cement market.

Growth of Cosmetic / Aesthetic Dentistry

Social-media visibility and remote communication motivate elective cosmetic treatments, broadening restorative volumes that hinge on color-stable, translucent cements. Digital intraoral scanning and 3-D printing permit one-visit indirect restorations, catalyzing uptake of dual-cure, low-shrinkage cements with simplified cleanup. Dental service organizations, expected to reach 39% of U.S. practices by 2026, standardize procurement and favor suppliers offering consistent performance across multi-state locations. Bulk-fill composites require companion luting agents that resist marginal discoloration; universal bio-active cements address this gap and elevate brand differentiation within the dental cement market.

Regulatory Push Toward Mercury-Free, Fluoride-Releasing Restoratives

The EU ban eliminates roughly 40 tonnes of dental mercury annually, forcing clinicians to migrate to bio-compatible cements with demonstrable fluoride[1]Source: European Commission, “Revised Mercury Regulation Enters into Force,” environment.ec.europa.eu. The Minamata Convention extends pressure globally as regulators scrutinize amalgam alternatives. Glass ionomer and resin-modified glass ionomer cements stand to benefit owing to chemical adhesion and antimicrobial properties. Manufacturers fast-tracking smart ion-releasing matrices gain early mover advantage in the dental cement market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity among small dental clinics | -0.7% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Stringent ISO 4049 & FDA 510(k) performance validations | -0.5% | Global regulatory compliance requirements | Long term (≥ 4 years) |

| Supply-chain crunch in specialty monomers & rare-earth fillers | -0.6% | Global, with concentrated supplier dependencies | Short term (≤ 2 years) |

| Environmental scrutiny on eugenol & Bis-GMA disposal | -0.3% | Europe & North America primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity Among Small Dental Clinics

Ninety-five percent of independent practices reported higher supply costs in 2024, while hygienist wages increased 26.6% between 2018 and 2023, eroding margins. These clinics often substitute premium bio-active cements with lower-cost alternatives, slowing penetration in price-elastic regions. Insurance reimbursement ceilings exacerbate procurement trade-offs, prompting practices to evaluate total cost of care when selecting cement systems. In emerging markets, the dynamic limits volume growth for advanced formulations, moderating overall expansion in the dental cement market.

Stringent ISO 4049 & FDA 510(k) Performance Validations

Compliance with ISO 4049, ANSI/ADA, and expanded FDA guidance extends product-development lead times and increases validation expenses[2]Source: U.S. Food and Drug Administration, “Dental Composite Resin Devices and Dental Curing Lights—Premarket Notification (510(k)) Submissions,” federalregister.gov. The Safety and Performance Based Pathway still requires substantial equivalence, favoring entrenched brands with large clinical datasets. Smaller innovators encounter funding and resource constraints, limiting the pipeline of novel materials entering the dental cement market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Permanent Dominance Drives Market Stability

Permanent products held 71.80% of the dental cement market share in 2025, anchoring overall revenue due to their role in definitive crowns, bridges, and implant restorations. Enhanced bio-active formulations such as ACTIVA BioACTIVE release fluoride, calcium, and phosphate ions, promoting remineralization and mitigating secondary caries risk. Universal self-adhesive chemistries simplify clinical workflows by eliminating separate primers, reducing chair time for high-volume practices.

Temporary cements, although smaller in revenue, are forecast to expand at a 6.15% CAGR as multi-stage implant cases and complex rehabilitations proliferate. Demand is further buoyed by the rise of same-day CAD/CAM workflows that use temporary restorations for occlusal verification before final placement. Innovations in eugenol-free, resin-reinforced temporary cements improve stability without compromising retrievability, enhancing patient experience and clinic efficiency within the dental cement market.

By Material: Glass Ionomer Leadership Faces Bio-Active Challenge

Glass ionomer maintained 31.05% revenue leadership in 2025 owing to chemical adhesion and sustained fluoride release that supports caries prevention. Smart response additives now tailor ion release to pH fluctuations, extending preventive benefits.

Bio-active resin cements record the fastest 6.95% CAGR, combining high flexural strength with aesthetics demanded in anterior restorations. Nanofiller incorporation reduces polymerization shrinkage and improves translucency, aligning with cosmetic dentistry trends. Zinc-oxide eugenol and zinc-phosphate remain for pulpal protection and specialty uses, while research into phosphoric-slag-enhanced zinc phosphate aims to upgrade mechanical properties at competitive cost. Emerging calcium-silicate formulations and nano-hybrids widen the materials palette and intensify competition in the dental cement market.

By Application: Restorations Segment Anchors Market Growth

Restorations represented 38.90% of 2025 revenue, reflecting dependence on cements for indirect fixed prostheses and inlays/onlays. Dual-cure, low-film-thickness cements improve marginal fit for CAD/CAM restorations and extend indications to posterior load-bearing cases. Universal adhesive systems such as G-CEM ONE bond to metal, zirconia, and lithium-disilicate without separate primers, supporting streamlined digital workflows.

Surgical dressing applications advance at an 7.65% CAGR due to bio-active cements applied in endodontic and periodontal surgeries. Calcium silicate-based materials provide sealing and regenerative properties, broadening cement usage beyond traditional luting. Luting and bonding progress in tandem with the proliferation of high-translucency zirconia, whereas pulpal protection remains stable yet benefits from bioceramic upgrades that enhance vital pulp therapy outcomes in the dental cement market.

Geography Analysis

North America led with 39.05% of the dental cement market share in 2025, underpinned by advanced dental infrastructure, high insurance penetration, and widespread adoption of digital dentistry. Expansion of dental service organizations is standardizing procurement protocols and accelerating uptake of premium bio-active systems. Regulatory clarity provided by FDA 510(k) pathways, despite added stringency, encourages early commercial launches, particularly for universal adhesive and dual-cure products.

Asia-Pacific delivers the fastest 6.90% CAGR, propelled by growing middle-class populations and heightened awareness campaigns. India hosts roughly 65,000 dental clinics and a USD 1.7 billion dental ecosystem, fuelling demand for restorative materials that balance performance with affordability. China’s rapid urbanization raises restorative procedure volumes, while Japan and South Korea contribute through advanced materials innovation and insurance support for geriatric care. Nonetheless, price sensitivity dictates tiered portfolio strategies as clinics weigh premium features against budget constraints in the dental cement market.

Europe confronts immediate material transition challenges following the January 2025 mercury amalgam ban, instigating accelerated adoption of mercury-free, fluoride-releasing cements environment. Germany, France, and the United Kingdom spearhead demand given robust prosthodontic training programs and consumer preference for aesthetic treatments. Regulatory harmonization via ISO 106 dentistry standards elevates product quality thresholds, favoring manufacturers with documented biocompatibility and long-term clinical data.

Competitive Landscape

The dental cement market is moderately concentrated, with incumbents leveraging patent portfolios, clinical validation, and global distribution. Solventum’s spin-off from 3M positions the RelyX franchise for focused investment and agile product cycles. Dentsply Sirona’s Essential Dental Solutions division prioritizes universal resin cements within its restorative workflow ecosystem, supported by DS Academy educational programs. GC Corporation capitalizes on Smart Response Ion Technology to defend leadership in glass-ionomer hybrids, while regional brands such as Kuraray Noritake and Ivoclar focus on high-translucency cement systems for aesthetic ceramics.

Strategic alliances extend reach, exemplified by Young Specialties–BISCO–Torch Dental collaboration to streamline procurement for multisite practices. Private-equity activity exceeded USD 9 billion in 2024, funding portfolio additions in bio-active and nano-hybrid technologies. Supply-chain resilience, especially in rare-earth fillers, is emerging as a competitive differentiator as manufacturers diversify sourcing to mitigate geopolitical risks.

Marketing strategies increasingly emphasize evidence-based efficacy and digital workflow compatibility. Award recognitions, such as Dental Advisor’s 2024 Preferred Product Award for NX3 Nexus Third Generation, bolster brand prestige. Customer-centric service packages—training, software integration, and outcome tracking—support differentiation beyond baseline material properties, sustaining competitive intensity in the dental cement market.

Dental Cement Industry Leaders

Dentsply Sirona

Ivoclar Vivadent AG

BISCO Inc.

Shofu Dental Corporation

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Henry Schein gained exclusive DSO distribution rights for Curodont Repair Fluoride Plus, enhancing minimally invasive restorative portfolios.

- August 2024: Ultradent acquired majority stake in i-dental, broadening digital dentistry capabilities tied to cement placement for CAD/CAM restorations.

- July 2024: FDA released updated guidance for dental composite resin devices and curing lights, tightening 510(k) performance evidence requirements

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the dental cement market as the sale of ready-to-use permanent and temporary cements that bond, seal, or line natural teeth and indirect restorations (crowns, bridges, inlays, orthodontic brackets) in chair-side clinical settings. These materials include glass-ionomer, resin-modified glass-ionomer, zinc-phosphate, zinc-oxide eugenol, polycarboxylate, and resin-based formulations supplied in powders, pastes, or dual-barrel syringes.

Scope exclusion: We exclude bulk restorative composites, temporary luting pastes for laboratory models, and adhesives used solely in digital impression trays.

Segmentation Overview

- By Type

- Permanent

- Temporary

- By Material

- Zinc-Oxide Eugenol

- Zinc Phosphate

- Polycarboxylate

- Glass Ionomer

- Resin-Based

- Others

- By Application

- Pulpal Protection

- Luting & Bonding

- Restorations

- Surgical Dressing

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We validated desk findings through structured interviews with prosthodontists, procurement heads at multi-chair dental chains across North America, Europe, and Asia, plus senior product managers at regional distributors. Their inputs on average cement consumption per procedure, brand switching triggers, and expected price lifts in bulk packs sharpened our volume and ASP assumptions.

Desk Research

We first gathered foundational data from open sources such as the WHO Oral Health Observatory, the American Dental Association annual survey, Eurostat dental procedure files, and trade flows published by UN Comtrade. Patent families were screened on Questel for new fluoride-releasing resin chemistries, and D&B Hoovers supplied revenue splits for leading manufacturers. Our desk work then drew on peer-reviewed journals (Journal of Prosthetic Dentistry), customs codes HS 300640, and investor presentations that reveal kit pricing and shipment trends. These references formed the baseline demand universe; however, they are indicative, and many other sources also fed our evidence stack.

Market-Sizing & Forecasting

We applied a top-down flow: global restorative and orthodontic procedure counts were reconstructed from national health statistics, then multiplied by cement utilization factors and average kit sizes. Selective bottom-up checks of manufacturer shipments and distributor channel scans corrected outliers. Key variables in our model include: (1) number of practicing dentists, (2) average restorative procedures per dentist, (3) kit-level ASP shifts linked to resin upgrades, (4) fluoride-free regulation deadlines, and (5) adoption rate of CAD/CAM indirect workflows. A multivariate regression with ARIMA error correction projected each driver through 2030, and gaps in shipment data were bridged with distributor sell-through ratios discussed during primary calls.

Data Validation & Update Cycle

Outputs pass a two-stage analyst review; variance flags above +/-7% trigger re-checks with respondents, and our models refresh annually. Ad-hoc updates follow material events such as a new amalgam restriction.

Why Our Dental Cement Baseline Earns Dependability

Published values often diverge because firms choose different product mixes, pricing ladders, and refresh cadences. We signal these sources of variation upfront so decision-makers grasp why numbers are rarely identical.

Key gap drivers include competitor inclusion of laboratory lining materials, use of list rather than transacted ASPs, and single-scenario forecasting that ignores delayed EU mercury bans, whereas Mordor analysts embed mid-year regulatory scenarios and cross-verify kit prices before finalizing totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.54 B (2025) | Mordor Intelligence | - |

| USD 2.20 B (2025) | Global Consultancy A | Includes lab liners and uses catalog prices without discount grids |

| USD 1.91 B (2025) | Regional Consultancy B | Omits Asia-Pacific distributor data and applies uniform growth to all materials |

In sum, our disciplined mixing of verified procedure counts, real transaction prices, and timely regulatory triggers delivers a balanced, transparent baseline that clients can retrace and reproduce with confidence.

Key Questions Answered in the Report

What is the current valuation of the dental cement market?

The dental cement market size stood at USD 1.63 billion in 2026 and is projected to reach USD 2.14 billion by 2031 at a 5.62% CAGR.

Which segment holds the largest share in the dental cement market?

Permanent cements dominated with 71.80% of the dental cement market share in 2025, reflecting their critical role in long-term restorations.

Which material category is growing fastest?

Bio-active resin cements are advancing at a 6.95% CAGR through 2031 as clinicians seek materials that combine high strength, aesthetics, and fluoride release.

Why is Asia-Pacific the fastest-growing region?

Rising middle-class populations, expanding clinic networks, and increasing awareness of oral health are driving a 6.90% CAGR in Asia-Pacific demand for restorative materials.

How is the EU mercury amalgam ban influencing product demand?

The January 2025 ban is accelerating transition toward mercury-free, fluoride-releasing glass ionomer and resin-modified cements across Europe and influencing global policy adoption.

What years does this Dental Cement Market cover, and what was the market size in 2025?

In 2025, the Dental Cement Market size was estimated at USD 1.63 billion. The report covers the Dental Cement Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Dental Cement Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: