Rich Communication Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

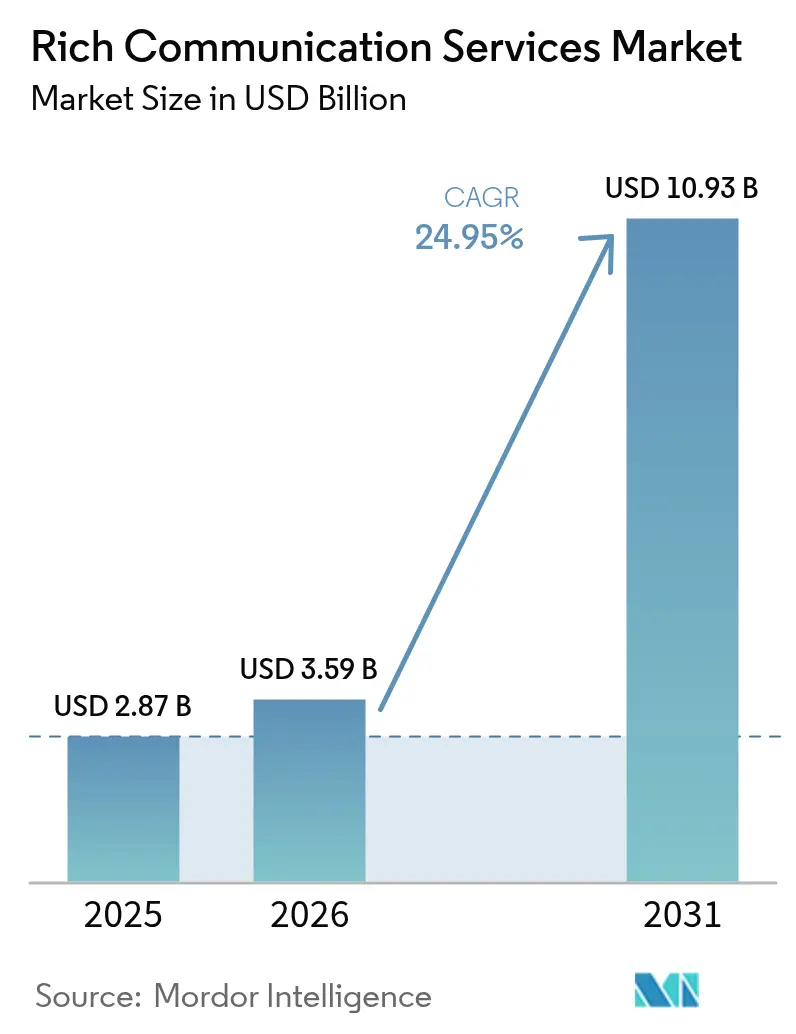

| Market Size (2026) | USD 3.59 Billion |

| Market Size (2031) | USD 10.93 Billion |

| Growth Rate (2026 - 2031) | 24.95% CAGR |

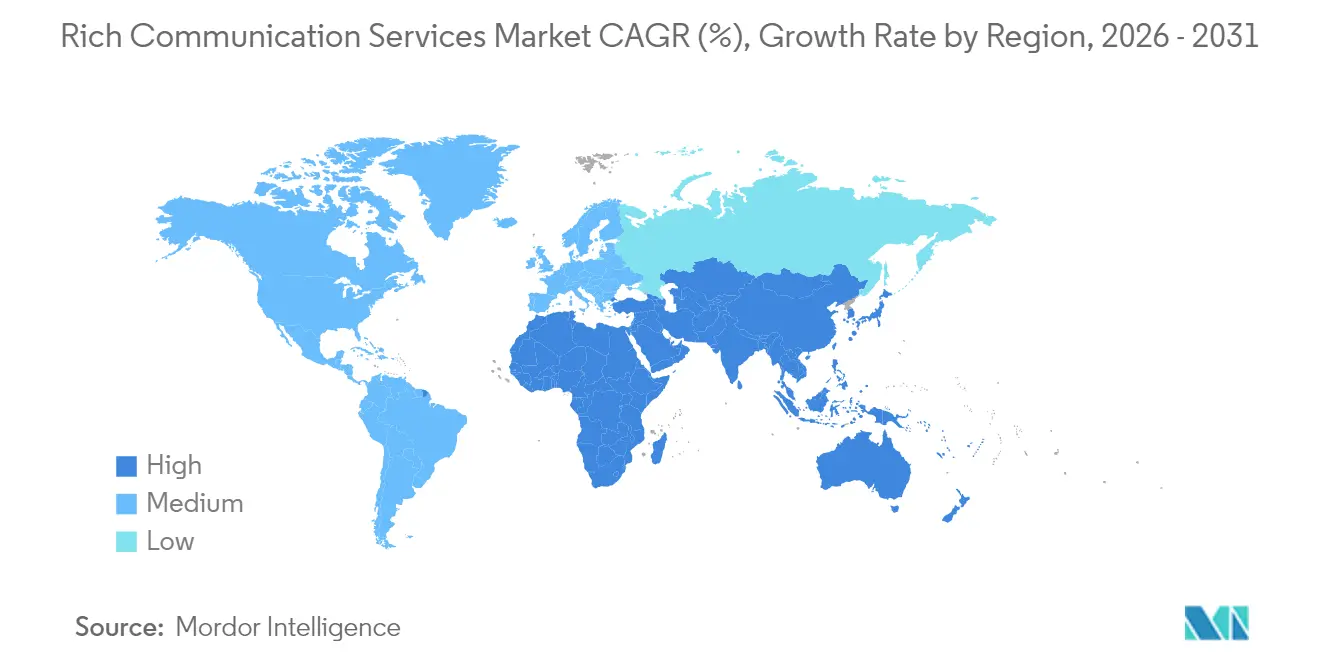

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rich Communication Services Market Analysis by Mordor Intelligence

The rich communication services market size was valued at USD 2.87 billion in 2025 and estimated to grow from USD 3.59 billion in 2026 to reach USD 10.93 billion by 2031, at a CAGR of 24.95% during the forecast period (2026-2031). Growing enterprise appetite for media-rich, branded customer engagement is pushing businesses to migrate from plain SMS to interactive messaging that supports images, video, and actionable buttons. Expanded carrier support, the inclusion of RCS in iOS 18, and Google’s report of more than 1 billion U.S. RCS messages per day underscore a tipping point in mainstream adoption. Large enterprises remain the principal revenue source, yet cloud-native CPaaS platforms are lowering entry barriers for small and medium businesses. Geographic momentum is strongest in Asia-Pacific as regional operators use 5G networks to support rich media traffic, while North America holds its lead on the back of long-standing carrier interoperability. Regulatory moves toward verified sender IDs are creating additional pull for enterprises that need secure, authenticated channels for customer contact.[1]FCC, “Emergency Communications by Rich Communication Services,” FCC, fcc.gov

Key Report Takeaways

- By communication type, Application-to-Person traffic led with 61.32% of rich communication services market share in 2025; Person-to-Application traffic is forecast to expand at a 30.75% CAGR to 2031.

- By deployment model, cloud solutions accounted for 72.15% of revenue in 2025, while on-premise solutions trailed but remain essential for industries with strict data-sovereignty rules.

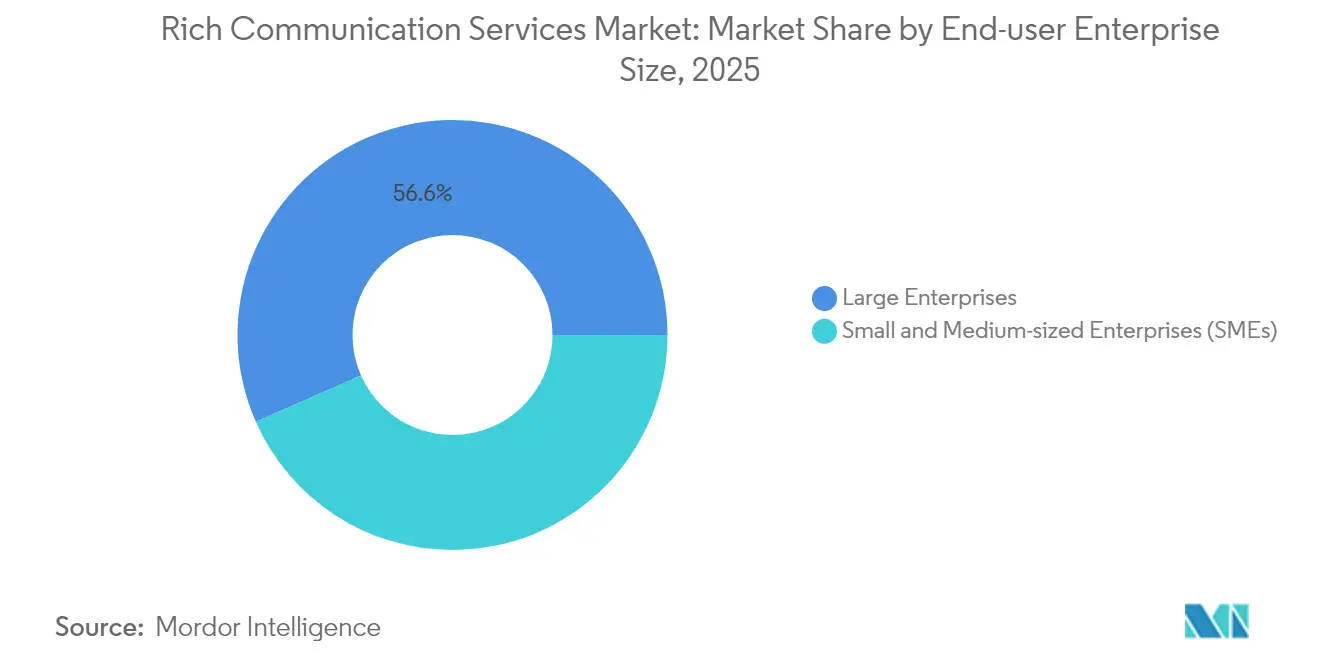

- By enterprise size, large organizations held 56.62% of 2025 revenue, whereas SMEs post the fastest 28.1% CAGR through 2031 as affordable SaaS offerings take hold.

- By end-user industry, retail and e-commerce captured 26.08% of revenue in 2025; that segment is poised for a 31.1% CAGR through 2031 on the back of conversational commerce.

- By region, North America controlled 38.12% of revenue in 2025; Asia-Pacific is the quickest-expanding region at a 29% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rich Communication Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise demand for A2P RCS business messaging | +6.2% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| iOS-18 support and expanding Android OEM pre-installs | +5.8% | Global, accelerated in North America and Asia-Pacific | Short term (≤ 2 years) |

| 5G roll-outs boosting high-resolution rich media traffic | +4.3% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Regulatory shift toward verified sender ID and anti-spam rules | +3.1% | Europe and North America, expanding to Asia-Pacific | Medium term (2–4 years) |

| CPaaS integration unlocking omni-channel orchestration | +2.9% | Global, enterprise-focused markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Enterprise Demand for A2P RCS Business Messaging

A2P campaigns deliver markedly higher conversion and click-through rates than legacy SMS, encouraging brands in banking and retail to shift considerable spend to the channel.[2]Vodafone Group, “Enterprise Messaging Strategy Whitepaper,” Vodafone, vodafone.com Multi-media cards and suggested replies let marketers guide shoppers from awareness to purchase within a single threaded conversation, generating 6.2 times the ROI of basic text pushes. CPaaS vendors have responded by embedding low-code templates, compliance workflows, and real-time analytics that quantify lift against email and app-push programs. Early adopters such as global banks report 10% conversion from personalized loan-upsell chats, validating the revenue upside. As more enterprises witness the impact, A2P usage is set to underpin overall rich communication services market expansion during the forecast window.

iOS-18 Support and Expanding Android OEM Pre-installs

Apple’s decision to embed RCS in iOS 18 removes the historic interoperability gap that steered traffic to OTT apps; nearly 900 million active iPhones instantly become reachable via operator-grade rich messaging.[3]Tim Cook, “Apple WWDC 2024 Keynote,” Apple, apple.com Samsung’s default adoption of Messages by Google on Galaxy devices further amplifies global reach. The unified experience eliminates pixelated images, broken group chats, and green/blue chat fragmentation that deterred consumers. Enterprises gain predictable reach across operating systems, unlocking larger addressable audiences without maintaining parallel OTT channels. This network effect is already visible in pilot campaigns that recorded 25% higher engagement after Apple rollout.

5G Roll-outs Boosting High-Resolution Rich Media Traffic

Mainstream 5G availability raises device bandwidth and lowers latency so that high-resolution video, carousel images, and interactive forms load instantly inside a message thread. Operators such as Verizon continue to earmark multi-billion-dollar budgets for 5G; that investment directly lifts the ceiling on message payload size and quality. In early 5G markets—Japan, South Korea—RCS adoption ratios are above 70%, supporting the thesis that next-gen networks lubricate rich communication uptake. As 5G coverage spreads through populous Asia-Pacific economies, elevated media capabilities will act as a demand multiplier for enterprise campaigns.

Regulatory Shift Toward Verified Sender ID and Anti-Spam Rules

Governments now consider message authentication critical to consumer trust. The FCC mandates verified sender IDs for emergency texts, while the European Union advances Digital Markets Act provisions requiring messaging interoperability.[4]RapidSOS, “RCS for Next-Gen 911 Services,” RapidSOS, rapidsos.com RCS benefits from built-in verification and spam scoring, letting enterprises satisfy compliance without extra APIs. For consumers, visibility of a branded logo and check-mark mitigates phishing fears, reducing opt-out rates. The net effect is regulatory pull in favor of RCS over unregulated OTT channels, especially in financial services and healthcare where audit trails are compulsory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented global operator interoperability | -4.7% | Global, most severe in emerging markets | Medium term (2–4 years) |

| Absence of full end-to-end encryption | -3.2% | Europe and North America | Short term (≤ 2 years) |

| OTT super-apps cannibalizing enterprise wallet share | -2.8% | Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Unclear operator monetization models | -1.9% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Fragmented Global Operator Interoperability

Only 57 carriers have aligned with GSMA Universal Profile 3.0, creating gaps that degrade cross-border experience. Enterprises sending campaigns into multiple regions must maintain fallback SMS or OTT channels, raising cost and operational complexity. While hubs such as Google’s Jibe and GSMA’s Interconnect projects are intended to streamline routing, uneven implementation throttles scale. Multinationals continue to lobby for consistent SLAs before migrating high-value traffic, delaying revenue realignment toward RCS.

Absence of Full End-to-End Encryption

Current RCS encryption works only for Android-to-Android traffic through Google Messages, leaving iOS and mixed-OS conversations outside the protection envelope. Financial institutions and healthcare providers subject to strict confidentiality rules remain reluctant to use RCS for sensitive payloads. Apple’s promise of encrypted RCS elevates the security baseline but may still conflict with certain government surveillance laws. Until a universally accepted encryption layer arrives, privacy concerns will cap adoption in compliance-heavy verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Type: A2P Commands Revenue Leadership

A2P traffic delivered 61.32% of 2025 revenue, making it the backbone of the rich communication services market. Banks, retailers, and airlines use multimedia cards and quick replies to convert routine notifications into conversational touchpoints that drive incremental sales. Person-to-Application conversations, though currently smaller, are expanding 30.75% annually as AI chatbots mature and consumers grow comfortable completing transactions inside a thread. This uptick will increase the rich communication services market size for P2A flows at a double-digit clip through 2031.

Enterprises are documenting conversion jumps of 8–10 percentage points when migrating loyalty promotions from SMS to RCS. Case studies in India show a 358% traffic surge for CPaaS provider Gupshup after integrating Vertex AI chatbots. Person-to-Person usage also climbs in markets with seamless iOS–Android interconnect, though monetization is operator-driven rather than enterprise-driven. High-engagement sectors such as gaming and ticketing rely on P2A flows to manage waitlists and authentication, signaling an evolving mix within the communication-type hierarchy.

By Deployment Model: Cloud Dominance Reflects API-First Strategies

Cloud-hosted platforms generated 72.15% of 2025 revenue, mirroring broader enterprise moves to eliminate cap-ex-heavy, on-premise messaging gateways. Multinational brands favor public-cloud RCS because it dovetails with existing CRM, CDP, and marketing-automation stacks via REST APIs.

On-premise environments remain non-trivial in sectors such as defense, healthcare, and government where data-residency laws require local processing. Those deployments stand to benefit from hybrid architectures in which sensitive content is rendered behind the firewall while global reach rides public-cloud interconnects. Twilio’s public beta underscores the vendor push to abstract carrier complexity behind SDKs, letting developers spin up RCS alongside SMS, WhatsApp, and email within one dashboard.

By End-user Enterprise Size: SMEs Accelerate Uptake

Large organizations held 56.62% of 2025 revenue, drawn by global reach, brand verification, and analytics dashboards that fit existing martech workflows. However, SMEs are set to grow 28.1% per year as SaaS providers bundle RCS into entry-level plans with drag-and-drop templates. This democratization will expand the rich communication services market share held by SMEs to roughly one-third by 2031.

Smaller retailers deploy conversational catalogs with embedded pay-now buttons, turning a single message into a storefront. Automated compliance features relieve resource-constrained teams from managing opt-outs and data-protection audits. As low-code tooling matures, onboarding times are shrinking from weeks to hours, removing yet another adoption barrier for small businesses.

By End-User Industry: Retail and E-Commerce Lead Conversational Commerce

Retail retained 26.08% revenue share in 2025 thanks to product carousels, personalized promotions, and check-out inside a chat thread, all of which cut friction in the customer journey. The segment’s 31.1% CAGR will push the rich communication services market size for retail to USD 3.79 billion by 2031. Banking and financial services are fast followers, employing RCS for two-factor authentication, portfolio updates, and interactive statements.

Healthcare providers lean on RCS for appointment reminders and medication adherence prompts, reducing no-show rates. Travel brands send dynamic boarding passes that auto-update gate changes, while media firms distribute trailers and ticket offers. Across industries, venture capital is flowing into plug-ins that connect e-commerce carts, payment gateways, and loyalty engines directly to RCS payloads, broadening monetizable use-cases.

Geography Analysis

North America generated 38.12% of 2025 revenue, underpinned by early universal profile adoption across Verizon, ATandT, and T-Mobile. Google’s disclosure of more than 1 billion daily RCS messages in the U.S. illustrates mature consumer uptake. Regulatory clarity also helps: the FCC now recognizes RCS for emergency 911 texts, encouraging municipalities and enterprises alike to adopt authenticated channel. The region’s high ARPU lets carriers capture incremental revenue through business messaging fees.

Asia-Pacific is the fastest-growing geography at a 29% CAGR, stimulated by ultra-high smartphone penetration and government digitization programs. India records 50 million monthly enterprise messages on a single CPaaS platform and is projected to eclipse North America in traffic volume by 2027. Japan and South Korea exhibit plus-70% RCS user ratios, proving how 5G density correlates with rich-media adoption. Despite fragmented operator landscapes, initiatives such as the GSMA Interconnect Hub aim to streamline cross-border routing, further boosting the rich communication services market in the region.

Europe posts steady expansion as data-protection regulations and Digital Markets Act interoperability rules favor verified, operator-controlled messaging over unregulated OTT apps. Deutsche Telekom’s EUR 115.8 billion 2024 revenue includes a growing slice from RCS-enabled value-added services. Conversely, the UK debate over lawful interception vis-à-vis Apple’s encrypted RCS shows that regulatory uncertainty can temporarily dampen deployment, yet enterprises continue pilot projects to gauge engagement lift. Latin America remains early-stage but is notable for outsized conversational commerce usage, especially in Brazil where tier-one carriers completed their first large-scale campaigns during 2024.

Competitive Landscape

The rich communication services market shows moderate consolidation as CPaaS leaders buy regional voice, messaging, and routing specialists to shore up global coverage. Sinch’s USD 1.14 billion purchase of Inteliquent secures direct interconnect to U.S. operators, lowering latency and cost for A2P traffic. Proximus Group’s pending takeover of Route Mobile would elevate combined revenue above EUR 2 billion by 2026, laying groundwork for a pan-European platform. Twilio counters by accelerating product velocity, rolling RCS into its omnichannel studio to defend share against newly bulked-up challengers.

Technology differentiation increasingly revolves around AI and automation. Gupshup embeds Google Vertex AI to create self-learning chat flows that surface personalized offers on the fly, reducing manual campaign design and improving statistical lift. Infobip deploys predictive audience segmentation, while Samsung files patents on augmented-reality overlays for future message formats. Providers with proprietary data models gain an edge, translating customer behavior into conversion-boosting content blocks.

Regional operators also play deal-maker: Singtel’s alliance with Sinch covers Singapore, Malaysia, and Indonesia, marrying carrier reach with CPaaS orchestration. This trend positions telcos not just as dumb pipes but as co-owners of enterprise engagement stacks. Competitive pressure is therefore shifting toward securing exclusive operator APIs, deeper wallet integrations, and advanced compliance features that answer vertical-specific needs.

Rich Communication Services Industry Leaders

Huawei Technologies Co. Ltd

Google LLC

AT&T Inc.

Verizon Communications Inc.

Vodafone Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Attentive unveiled RCS Business Messaging at Shoptalk 2025, targeting 2.2 billion active subscribers by 2028 through AI-driven personalization, supported by Verizon, ATandT, and T-Mobile.

- November 2024: Samsung and Google expanded their partnership to pre-install Messages by Google across Galaxy devices, positioning RCS as the default messaging standard globally.

- October 2024: Sinch and Singtel launched Singapore’s first RCS Business Messaging service, enhancing regional CPaaS coverage in Asia-Pacific.

- June 2024: Infobip integrated Google Vertex AI with its RCS platform, enabling brands to deploy intelligent chatbots for automated customer interactions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

In our study, Mordor Intelligence defines the global Rich Communication Services (RCS) market as the annual revenues earned when mobile network operators, CPaaS vendors, or aggregators deliver GSMA-compliant, IP-based messaging, calling, and content-sharing features through the phone's native client to enterprises or consumers. The figure captures platform license fees, connectivity and routing charges, verified-sender surcharges, and related enablement revenues.

Scope Exclusions: Over-the-top chat apps, proprietary push-notification channels, handset sales, and pure SMS or MMS traffic fall outside this analysis.

Segmentation Overview

- By Communication Type

- A2P (Application-to-Person)

- P2P (Person-to-Person)

- P2A (Person-to-Application)

- Others

- By Deployment Model

- Cloud

- On-Premise

- By End-user Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-User Industry

- BFSI

- Media and Entertainment

- Retail and E-commerce

- Travel and Hospitality

- Healthcare

- IT and Telecom

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Switzerland

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Vietnam

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- Nigeria

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed carrier product heads, CPaaS solution architects, and enterprise messaging buyers across North America, Europe, and Asia-Pacific, then ran structured surveys with SMEs.

These interactions validated penetration assumptions, uncovered regional price dispersion, and highlighted capex or policy hurdles that secondary sources missed.

Desk Research

We began by mining high-credibility public statistics from sources such as GSMA, ITU, the Ericsson Mobility Report, CTIA, and national telecom regulators, which let us size the RCS-capable smartphone base and average traffic per user. Operator 10-K filings, investor decks, and press coverage compiled through Dow Jones Factiva and D&B Hoovers helped benchmark enterprise adoption rates and blended message pricing. Academic journals plus 3GPP release notes traced protocol evolution and cost curves, while trade-body white papers and customs records (via Questel) offered extra signals on gateway deployments. The sources listed illustrate our approach; many additional open and paid references were consulted to corroborate data points and assumptions.

Market-Sizing & Forecasting

We construct a top-down model that multiplies the live RCS-enabled handset base by average monthly sessions and monetizable take-rates, then applies regional blended revenue per session. Select bottom-up checks, operator-reported A2P traffic volumes and sampled API billings, fine-tune outputs. Key inputs include 5G population coverage, verified-sender roll-out pace, cloud API pricing, and iOS adoption scenarios. Forecasts use multivariate regression, allowing handset growth and A2P conversion to explain most variance, while scenario analysis stress-tests the model for regulatory or platform shocks.

Data Validation & Update Cycle

Every estimate passes peer review, variance audits against third-party indicators, and reconciliation with historical currency series.

Reports refresh annually; interim updates are issued if major events shift traffic or pricing.

Why Mordor's Rich Communication Services Baseline Commands Reliability

Published RCS figures often diverge because firms bundle wider CPaaS revenues, apply aggressive penetration curves, or freeze exchange rates, whereas Mordor's disciplined scope, region-specific traffic benchmarks, and dual-path modeling keep the baseline balanced and transparent.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.87 B (2025) | Mordor Intelligence | - |

| USD 11.7 B (2025) | Global Consultancy A | Adds SMS & voice CPaaS, assumes universal Android roll-out |

| USD 10.14 B (2025) | Research Boutique B | Counts chat-app business APIs as RCS revenue |

| USD 3.22 B (2024) | Industry Association C | Models only P2P traffic, omits enterprise A2P streams |

The comparison shows that, once differing scopes are stripped away, Mordor's USD 2.87 billion baseline aligns closest to operator-reported monetizable traffic, giving decision-makers a dependable starting point.

Key Questions Answered in the Report

How fast is the rich communication services market expected to grow?

The market is forecast to expand at a 24.95% CAGR from USD 2.87 billion in 2025 to USD 10.93 billion by 2031.

Which segment currently contributes the most revenue?

Application-to-Person messaging delivered 61.32% of 2025 revenue, making it the single largest segment.

Why are SMEs adopting RCS so quickly?

Cloud-based CPaaS models provide low-cost APIs and pre-built templates, allowing SMEs to launch branded campaigns without heavy IT investment.

Which is the fastest growing region in Rich Communication Services Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

What role does 5G play in RCS adoption?

5G networks support high-resolution media and low-latency interactions, enabling richer in-message experiences that increase engagement rates.

Page last updated on: