Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

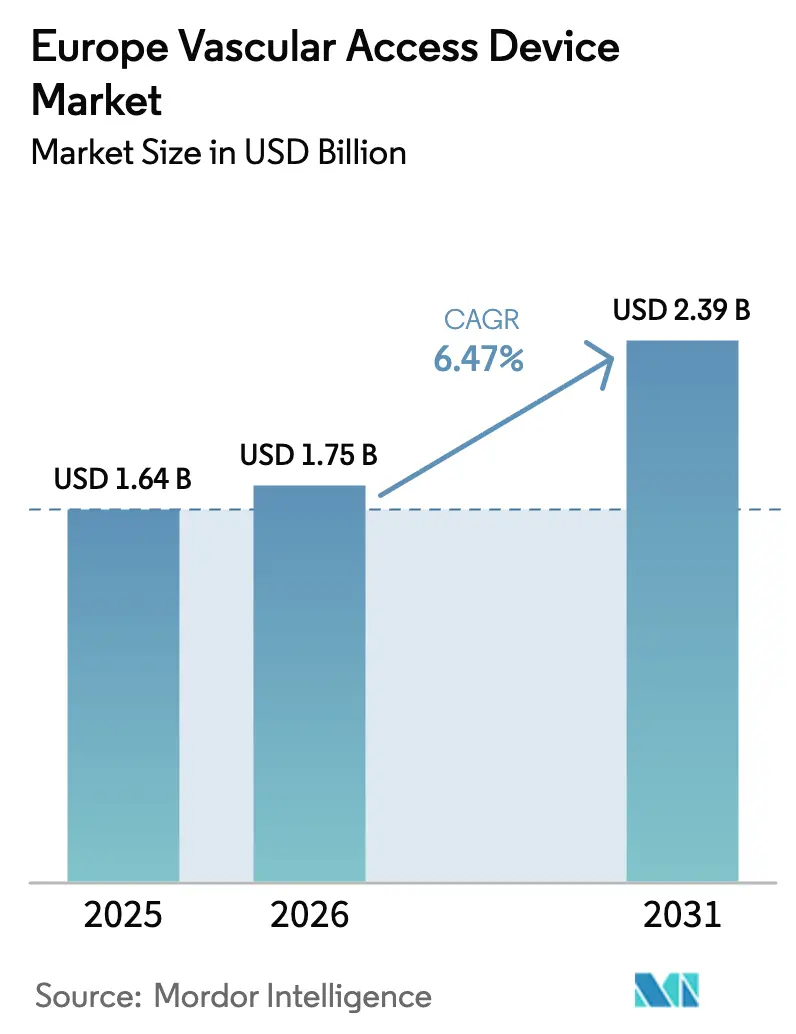

| Base Year Market Size (2025) | USD 1.64 Billion |

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Vascular Access Device Market Analysis by Mordor Intelligence

The Europe vascular access devices market size is expected to grow from USD 1.64 billion in 2025 to USD 1.75 billion in 2026 and is forecast to reach USD 2.39 billion by 2031 at 6.47% CAGR over 2026-2031. An increasingly older population, tighter infection-prevention standards, and material-science advances are combining to shift clinical practice toward safer, longer-dwelling catheters and wider use of peripheral insertion techniques. Hospitals augment demand as chronic-disease admissions rise, while home-infusion programs extend use beyond traditional facilities. EU Medical Device Regulation (EU-MDR) enforcement accelerates the replacement of legacy products with antimicrobial-coated or sensor-equipped alternatives, and Germany’s sizable procedural volume anchors regional revenues even as France posts the fastest growth. Polyurethane remains prevalent, yet silicone and next-generation hydrophilic polymers gain traction as suppliers hedge against PFAS restrictions and supply-chain volatility.

Key Report Takeaways

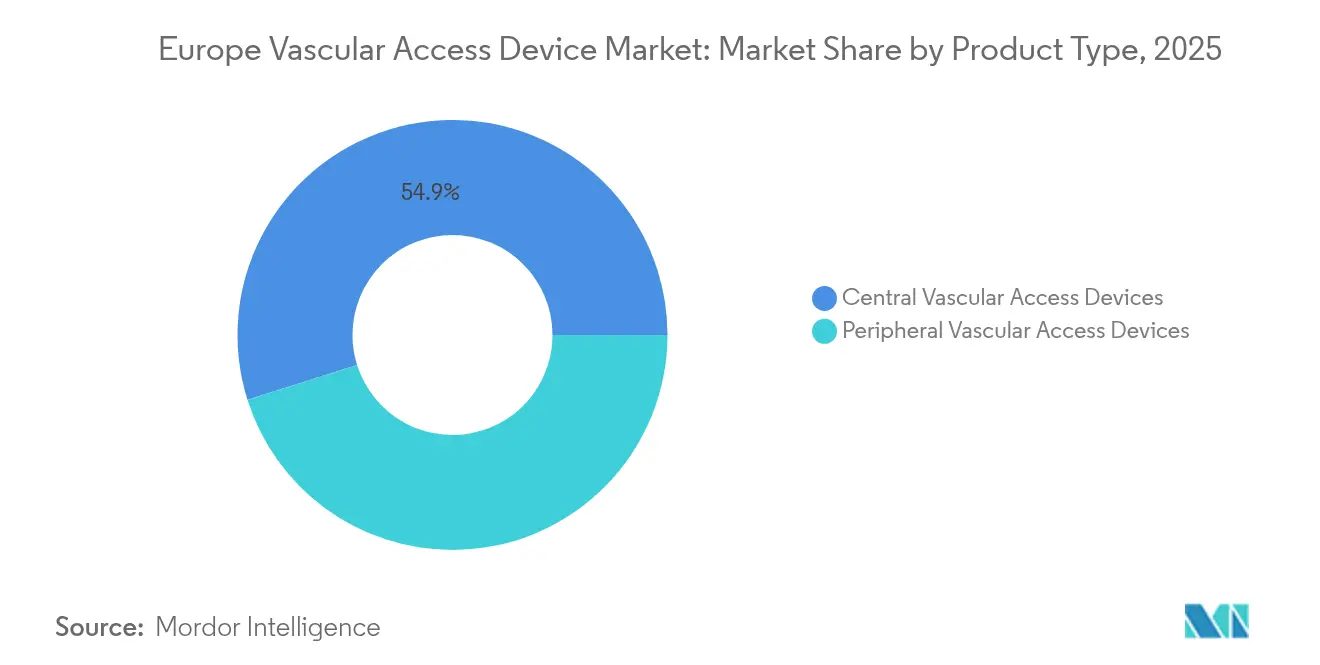

- By device type, central vascular access systems led with 54.86% revenue share in 2025, while peripheral devices are forecast to expand at a 7.29% CAGR through 2031 within the Europe vascular access devices market.

- By application, medication administration accounted for 38.02% of the Europe vascular access devices market size in 2025, whereas diagnostics and testing are advancing at a 7.36% CAGR to 2031.

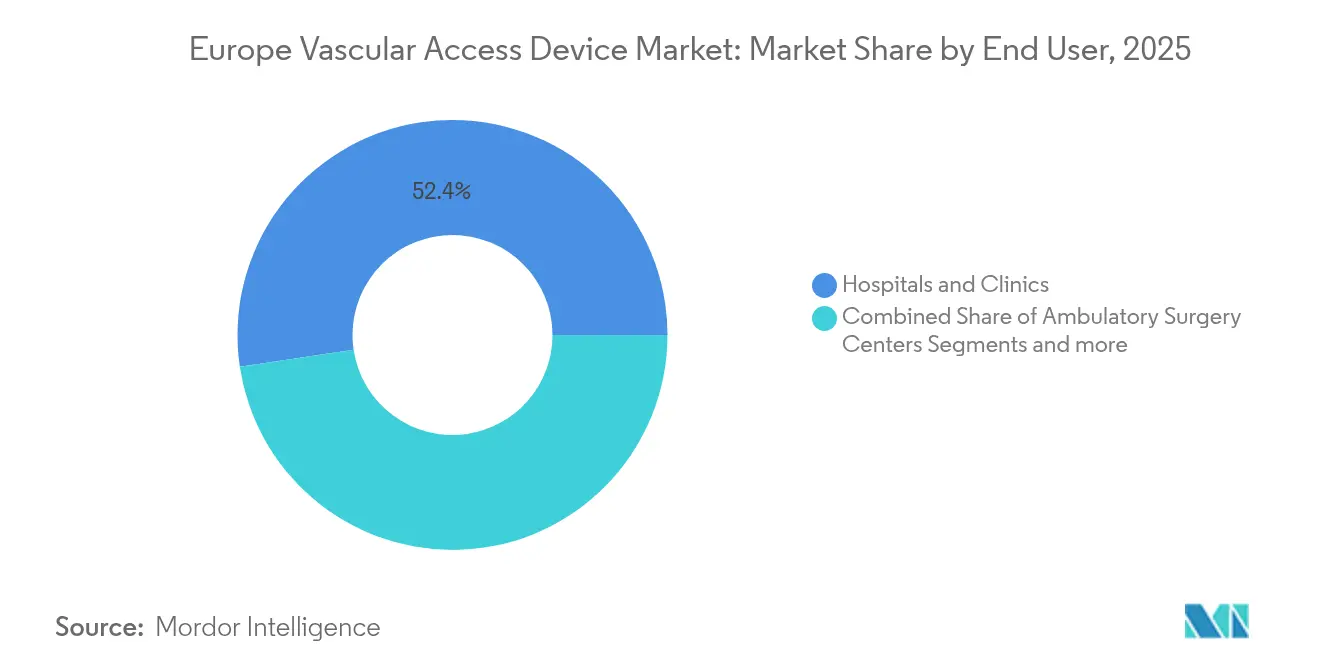

- By end user, hospitals and clinics held 52.35% of the Europe vascular access devices market share in 2025, but ambulatory surgery centers are projected to grow at a 7.48% CAGR over the same horizon.

- By material, polyurethane dominated with 47.41% share in 2025; silicone catheters record the swiftest expansion at a 7.62% CAGR.

- By geography, Germany captured 39.85% of regional revenues in 2025, while France is on course for a 7.55% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Vascular Access Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic diseases | +1.8% | EU-wide, concentrated in Germany, France, Italy | Long term (≥ 4 years) |

| Rising number of chemotherapy procedures & high hospitalization | +1.2% | EU-wide with oncology center concentration | Medium term (2-4 years) |

| Increasing pediatric utilization of VADs | +0.9% | Northern Europe, Scandinavia leading adoption | Medium term (2-4 years) |

| Shift toward home-infusion therapies in Europe | +1.5% | Germany, Netherlands, UK driving adoption | Long term (≥ 4 years) |

| EU-MDR-driven adoption of antimicrobial-coated catheters | +0.8% | EU-wide regulatory compliance requirement | Short term (≤ 2 years) |

| Pilots of sensor-enabled catheters for IV infiltration alerts | +0.4% | UK, Germany early adoption markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing prevalence of chronic diseases

Europe’s aging profile is increasing the incidence of cardiovascular, renal, and metabolic illnesses that require sustained venous access. By 2030, 22.9% of Europeans will be 65 years or older, and vascular procedures are projected to rise by 40.5%, underscoring the need for durable and low-complication catheters. Hospitals therefore favor antimicrobial-coated central lines, and peripheral midlines are gaining acceptance for outpatient follow-up. Device makers respond with hydrophilic biomaterials that resist thrombus formation, while clinicians expand ultrasound-guided insertion to minimize multiple punctures and unplanned replacements. Collectively, these trends reinforce steady demand across the Europe vascular access devices market as chronic-care pathways lengthen and readmission penalties tighten.

Rising number of chemotherapy procedures & high hospitalization

Oncology centers depend on reliable venous access to administer multidrug regimens that can last several months. Central venous ports show lower infection rates than tunneled catheters in pediatric cases, prompting wide adoption in children’s hospitals. Adult oncology units also prefer implantable ports because fewer dressing changes reduce nursing burden and permit outpatient regimens. The result is heightened consumption of power-injectable ports and accessories, a key volume driver in the Europe vascular access devices market. Competition now centers on thin-walled designs that withstand high flow rates for contrast media while meeting new EU-MDR mechanical-integrity testing.

Increasing pediatric utilization of VADs

European clinical societies endorse ultrasound imaging for line placement in neonates and children to curtail inadvertent arterial punctures. Extended-dwell peripheral intravenous catheters achieve 71.7% success rates in neonatal intensive care units, lowering exposure to central-line-associated bloodstream infections. Demand for smaller French size catheters manufactured from soft silicone is therefore accelerating. Pediatric dialysis programs also adopt low-profile tunneled catheters with subcutaneously anchored securement to reduce accidental dislodgement to 2.6%. Vendors that produce catheter-to-skin interfaces designed for fragile vessels are securing preferred-supplier status at children’s hospitals, bolstering the Europe vascular access devices market [1]Ran Li, "Heparin versus normal saline for the care of peripheral intravenous catheters in pediatrics: a meta-analysis of randomized controlled trials," BMC Pediatrics, bmcpediatr.biomedcentral.com.

Shift toward home-infusion therapies in Europe

Health authorities encourage home-based antibiotic, parenteral nutrition, and palliative chemotherapy infusions to relieve inpatient capacities. Device longevity and minimal maintenance become decisive purchase criteria, spurring R&D into coated ports that remain maintenance-free for six months. Portable elastomeric pumps paired with midline catheters simplify administration, and cloud-connected sensors allow nursing teams to verify flow status remotely. Germany and the Netherlands reimburse home-infusion consumables when supplied through accredited pharmacies, fueling peripheral line placement services that operate in community clinics. Collectively, home-care adoption adds meaningful incremental volume to the Europe vascular access devices market and opens after-sales revenue for flushing kits and securement dressings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risks & complications associated with catheter use | -1.1% | EU-wide, particularly ICU settings | Long term (≥ 4 years) |

| Stringent regulations & product recalls | -0.8% | EU-wide MDR compliance requirement | Short term (≤ 2 years) |

| Polyurethane supply-chain vulnerability | -0.6% | EU manufacturing dependent regions | Medium term (2-4 years) |

| Growth of needle-free connectors cannibalising short PIVCs | -0.4% | Northern Europe early adoption markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Risks & complications associated with catheter use

Central line infections remain a persistent obstacle [2]Alkmena Kafazi, "Device-Associated Infections in Adult Intensive Care Units: A Prospective Surveillance Study," MDPI, mdpi.com. Greek intensive-care units record 8.6 bloodstream infections per 1,000 catheter-days, extending patient stays by nearly 19 days and adding mortality of 20.1%. Similar patterns in Polish ICUs show catheter-associated urinary infections affecting 8.83% of patients. Peripheral infiltration injuries occur in 5.4% of monitored infusions despite adherence to best-practice guidelines. These incidents elevate malpractice costs, slow device turnover, and oblige hospitals to favor proven brands, capping short-term volume uplift in the Europe vascular access devices market [3]Jakub Sleziak, "Catheter-associated urinary tract infections in the intensive care unit during and after the COVID- 19 pandemic, " BMC Infectious Diseases, bmcinfectdis.biomedcentral.com.

Stringent regulations & product recalls

EU-MDR raised technical-file expectations for legacy devices and strained the capacity of the region’s 43 notified bodies. Only 4,873 certificates had been issued against 14,539 applications by 2023, leaving nearly 10,000 products awaiting assessment. Manufacturers channel engineering resources toward documentation rather than new-product launches, and smaller firms withdraw SKUs that cannot justify recertification expense. Recalls related to tip fracture or improper labeling further erode buyer confidence. Although long-term compliance will enhance patient safety, near-term supply disruptions and audit costs trim growth potential for the Europe vascular access devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Central Dominance Faces Peripheral Innovation

Central lines continued to account for 54.86% of revenue in 2025 as oncologists and critical-care teams rely on ports and tunneled catheters for multidose regimens. At the same time, peripheral alternatives recorded the highest 7.29% CAGR, reflecting clinician preference for lower-risk insertion sites and growing ultrasound-guided competency. New hydrophilic midline formats reduce thrombus formation by 96%, and antimicrobial polyurethane hubs exhibit 99.998% lower bacterial adhesion than standard plastics. Vendors are integrating blood-draw valves into peripherally inserted central catheters to support lab sampling without additional sticks, a feature valued in pediatric wards.

Integrated short peripheral cannulas increasingly carry closed systems that limit exposure, extending dwell times beyond 96 hours. Mid-sized hospitals adopt device-agility protocols that graduate patients from short cannulas to midlines rather than directly to central lines, tightening the cycle time between admissions and discharge. As a result, purchasing committees reevaluate the optimal mix of catheter SKUs, buoying unit shipments of peripheral devices within the Europe vascular access devices market. However, central implants remain irreplaceable for power-injection imaging and vesicant therapy, ensuring sustained baseline demand.

By Application: Medication Leadership Challenged by Diagnostic Growth

Medication delivery absorbed 38.02% of the Europe vascular access devices market size in 2025, driven by continual antimicrobial and chemotherapy infusion. Diagnostics and testing, though smaller, accelerate at a 7.36% CAGR to 2031 as point-of-care protocols mandate repeat blood draws. Manufacturers therefore package needle-free connectors with sample-optimized flow paths, addressing contamination risks. Sensor-enabled cannulas detect occlusions in real time, improving sample integrity and curtailing repeat sticks that can inflate consumable costs.

Blood-product transfusion lines benefit from closed-loop identification systems that synchronize with hospital information technology, cutting mismatch errors. Nutrition-delivery applications remain steady amid an aging patient population requiring long-term parenteral support in nursing facilities. Many facilities now update flush policy every 12 hours, lifting saline and heparin lock solution sales. With wider adoption of dual-lumen catheters in oncology, the Europe vascular access devices market positions itself to capture both therapeutic and diagnostic revenues in a single procedure.

By End User: Hospital Dominance Yields to Ambulatory Expansion

Hospitals still represented 52.35% of the Europe vascular access devices market share in 2025 because intensive care, oncology, and interventional radiology departments collectively generate high-value procedures. Yet ambulatory surgery centers are pacing a 7.48% CAGR as minimally invasive procedures migrate to day-case settings. Outpatient centers prefer midlines and power-injectable ports that support rapid turnover, prompting bulk purchases of pre-assembled kits that shorten prep time.

Home-health programs, backed by insurers seeking to decongest hospital beds, deploy portable infusion pumps paired with silicone midlines. Community-based nurses receive remote alerts if flow deviates from baseline, reducing unplanned emergency visits. Specialty dialysis clinics invest in tunneled catheters with antimicrobial cuffs to lessen infection readmissions. These patterns diversify demand channels while enhancing procedural consistency, reinforcing overall volume growth for the Europe vascular access devices market.

By Material: Polyurethane Prevalence Challenged by Silicone Innovation

Polyurethane captured 47.41% of 2025 revenues, favored for tensile strength and manufacturing familiarity. However, EU proposals to curtail PFAS usage stir conversion toward silicone and novel copolymers. Silicone catheters, expanding at a 7.62% CAGR, exhibit reduced thrombogenicity and ease of insertion in tortuous vessels. Hydrophilic surface treatments bonded to silicone further lower protein adsorption, and antimicrobial silver-ion impregnations meet infection-control targets without systemic antibiotic exposure.

PTFE shortages during 2024 prompted leading suppliers to insource extrusion lines and qualify alternative grades from Asian producers. Concurrently, research groups pioneer bio-resorbable polymers for temporary arteriovenous shunts, opening a new premium tier. As notified bodies scrutinize extractables data, materials that generate fewer leachables secure faster conformity assessment, indirectly accelerating market entry within the Europe vascular access devices market.

Geography Analysis

Germany anchored 39.85% of regional revenue in 2025 on the back of dense hospital networks, high diagnostic throughput, and early reimbursement for antimicrobial innovations. Federal infection-control mandates reimburse coated lines at a premium, and local manufacturers collaborate with Fraunhofer institutes to co-develop PFAS-free extrusion processes, broadening product portfolios. Continuous medical-education curricula ensure that vascular access insertion is ultrasound-guided across most tertiary centers, keeping complication rates comparatively low and sustaining predictable re-ordering cycles.

France posted the fastest 7.55% CAGR by modernizing outpatient oncology services and widening access to day-hospital infusion suites. National surveillance covering 55,000 catheters confirmed a downward trend in bloodstream infections when silver-ion cuffs were systematically deployed. The outcomes convinced regional procurement groups to bundle coated ports with dressing kits, creating multi-year supply contracts that favor vendors able to guarantee EU-MDR certificates.

The United Kingdom leverages National Health Service (NHS) technology funds to trial sensor-equipped midlines that alert clinicians to early infiltration, cutting extravasation incidents by 23%. Italy and Spain prioritize pediatric access improvement programs financed through EU cohesion funds, while Nordic countries integrate telehealth monitoring for patients discharged with peripherally inserted central catheters. Central-Eastern European markets align local legislation with EU-MDR, facilitating imports yet facing limited notified-body capacity; hospitals therefore rely on larger multinationals that already possess certificates, indirectly concentrating sales among top players in the Europe vascular access devices market.

Competitive Landscape

Market leadership tilts toward multinationals that maintain comprehensive EU-MDR technical files and supported clinical-evidence dossiers. Becton Dickinson, Teleflex, and Cook Medical collectively supply a broad portfolio spanning short PIVCs, PICCs, ports, and antimicrobial coatings. Mid-tier firms emphasize niche specializations such as pediatric-sized silicone catheters or hydrophilic biomaterials. Access Vascular’s MIMIX platform exemplifies material differentiation by offering near-zero bacterial adhesion, earning adoption in infection-prone oncology wards.

Strategic activity centers on vertical integration and portfolio broadening. Teleflex’s EUR 760 million purchase of Biotronik’s vascular intervention arm in February 2025 broadens its access to drug-coated balloons and stents that complement catheter lines. BD released an intraosseous access system in October 2024, filling gaps for emergency scenarios where peripheral cannulation fails. Vendors are also entering distribution alliances with digital-health startups to embed flow-monitoring chips that transmit via Bluetooth Low Energy to nurse dashboards. This convergence of hardware and software enhances switching costs and underpins long-term contracts across the Europe vascular access devices market.

Investment in manufacturing resilience rises as suppliers localize extrusion and sterilization capacity inside the EU to hedge against raw-material interruptions and shipping delays. Firms adopting silicone or PFAS-free substitutes file new patents on surface-modification chemistries, signaling an innovation wave that could reset brand hierarchies. Competitive intensity remains moderate, yet EU-MDR attrition of smaller players lifts combined top-five share above 70%, pointing to consolidation momentum.

Europe Vascular Access Device Industry Leaders

-

B.Braun Melsungen Ag

-

Becton, Dickinson and Company

-

Teleflex Incorporated

-

Baxter International Inc.

-

NIPRO Medical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex announced acquisition of Biotronik’s Vascular Intervention business for approximately EUR 760 million, expanding its interventional portfolio with drug-coated balloons and stents.

- January 2025: Xeltis completed enrolment in its EU pivotal trial for aXess, a restorative vascular access conduit for adults with end-stage renal disease, across 22 European centers.

- December 2024: Teleflex launched the Pressure Injectable Arrowg+ard Blue Plus MSB Procedure Kit in EMEA, featuring a full-spectrum antimicrobial central venous catheter.

- October 2024: BD introduced the BD Intraosseous Vascular Access System for rapid fluid or medication delivery when IV access is difficult.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European vascular access device market as all peripherally or centrally inserted catheters, implantable ports, and dialysis access lines placed in a vein to draw blood or deliver drugs, fluids, nutrition, or hemodialysis over short or extended dwell times. These devices are counted at factory gate prices and cover both acute and home-care usage across 27 EU states, the UK, EFTA nations, and candidate countries.

Scope exclusion: arterial closure or graft products used after cardiovascular interventions are not included.

Segmentation Overview

-

By Device Type

-

Central Vascular Access Devices

- Peripherally-Inserted Central Catheters (PICCs)

- Non-tunnelled Catheters

- Tunnelled Catheters

- Other Central Vascular Access Devices

-

Peripheral Vascular Access Devices

- Peripheral IV Catheters (PIVC)

- Midline Catheters

- Other Peripheral Vascular Access Devices

-

Central Vascular Access Devices

-

By Application

- Medication or Drug Administration

- Fluid and Nutrition Administration

- Blood and Blood-Product Transfusion

- Diagnostics and Testing

- Other Applications

-

By End User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Others

-

By Material

- Polyurethane

- Silicone

- Others

-

By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed vascular nurses, interventional radiologists, dialysis program heads, and procurement officers across Germany, France, Spain, the Nordics, and the UK. Discussions tested average dwell days, failure rates, and antimicrobial premium uptake, letting us tune utilization ratios and cross-check price corridors that secondary sources only hint at.

Desk Research

We began with open data from Eurostat inpatient procedure files, the European Centre for Disease Prevention and Control's CLABSI surveillance summaries, and OECD Health Statistics that track chemotherapy and dialysis sessions. Trade and reimbursement angles were clarified through European Medicines Agency safety notices, national tender portals such as Tenders Electronic Daily, and clinical evidence in journals like the Journal of Vascular Access. Company 10-Ks and investor decks enriched average selling price trends, while paid screens in D&B Hoovers and Dow Jones Factiva helped us align manufacturer revenues with public shipment numbers. The sources listed illustrate our approach and are not exhaustive.

A second pass captured catheter import volumes from UN Comtrade, patent momentum via Questel, and material cost shifts reported by PlasticsEurope. These threads built the historical demand spine before we spoke to market participants.

Market-Sizing & Forecasting

We first ran a top-down procedure-based model that multiplies chemotherapy, dialysis, critical-care, and surgical episodes by device penetration and replacement frequency, which are then adjusted for dwell-day compliance suggested by experts. Select bottom-up roll-ups of leading supplier revenues and sampled ASP × volume data validated the totals and revealed outliers. Key variables include EU27 cancer incidence, hemodialysis patient pool, ICU bed expansion, catheter-related infection targets, and polyurethane versus silicone mix. A multivariate regression linked these drivers to historical sales and delivered the baseline value and a growth rate toward the end of the forecast period. Gap pockets in bottom-up estimates were bridged using weighted averages from comparable countries.

Data Validation & Update Cycle

Each model iteration passes variance checks against independent procedure audits and customs data. Senior reviewers sign off only after anomalies are reconciled. Reports refresh every twelve months, with interim updates triggered by regulatory shifts, tender shocks, or major product launches, so clients always receive the latest view.

Why Our Europe Vascular Access Device Baseline Commands Reliability

Published numbers vary because firms pick different device mixes, price bases, and refresh cadences, and because many apply flat growth factors without testing against procedure reality.

Key gap drivers arise when alternate studies fold arterial closure kits into scope, apply single-country ASPs across Europe, or freeze 2021 COVID-era volumes, whereas Mordor re-benchmarks every year and tracks mix shifts such as the rise of midline catheters and antimicrobial coatings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.64 B (2025) | Mordor Intelligence | - |

| USD 1.96 B (2024) | Regional Consultancy A | Includes arterial closure and uses list prices without tender discounts |

| USD 1.50 B (2024) | Global Consultancy B | Excludes home-infusion volumes and applies uniform ASP across all countries |

In sum, by grounding our totals in procedure counts, price audits, and annual refreshes, Mordor delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeat quickly with public data.

Key Questions Answered in the Report

What is the current size of the Europe vascular access devices market?

The market is valued at USD 1.75 billion in 2026 and is forecast to reach USD 2.39 billion by 2031.

Which device type holds the largest share in Europe?

Central vascular access systems lead with 54.86% revenue share in 2025, although peripheral devices are growing the fastest.

How does EU-MDR affect manufacturers?

Stricter documentation and limited notified-body capacity delay certifications, raising compliance costs and favoring well-resourced companies.

Which material is gaining ground against polyurethane catheters?

Silicone is expanding at a 7.62% CAGR over 2026-2031 due to its biocompatibility and resilience to upcoming PFAS restrictions.

Why are ambulatory surgery centers important to future growth?

Outpatient facilities perform more minimally invasive procedures, driving a 7.48% CAGR over 2026-2031 for vascular access devices suitable for same-day care.

Page last updated on: