Coagulation Analyzers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.75 Billion |

| Market Size (2031) | USD 6.31 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

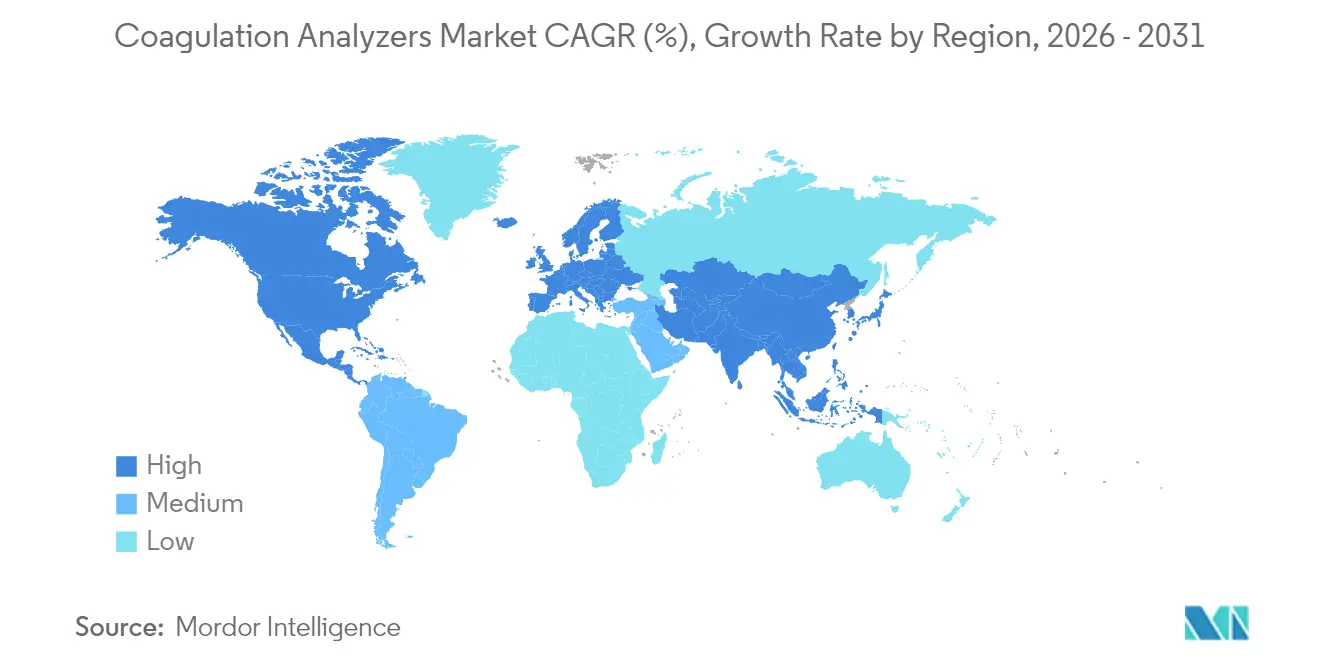

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coagulation Analyzers Market Analysis by Mordor Intelligence

The coagulation analyzers market size was valued at USD 4.49 billion in 2025 and estimated to grow from USD 4.75 billion in 2026 to reach USD 6.31 billion by 2031, at a CAGR of 5.85% during the forecast period (2026-2031). Growth stems from the shift toward real-time viscoelastic platforms, tighter quality regulations, and wider adoption of AI-guided dosing that trims adverse events by 30% compared with conventional monitoring. Viscoelastic analyzers deliver complete clotting profiles within minutes, enabling surgical teams to save blood products and shorten operating room time. At the same time, Class II re-classification in May 2025 has lowered regulatory barriers, encouraging regional manufacturers to enter the coagulation analyzers market and diversify supply. Intensifying M&A activity—such as Werfen’s purchase of Accriva and the long-term Siemens–Sysmex OEM pact—signals a race to secure reagent lines and embedded analytics.

Key Report Takeaways

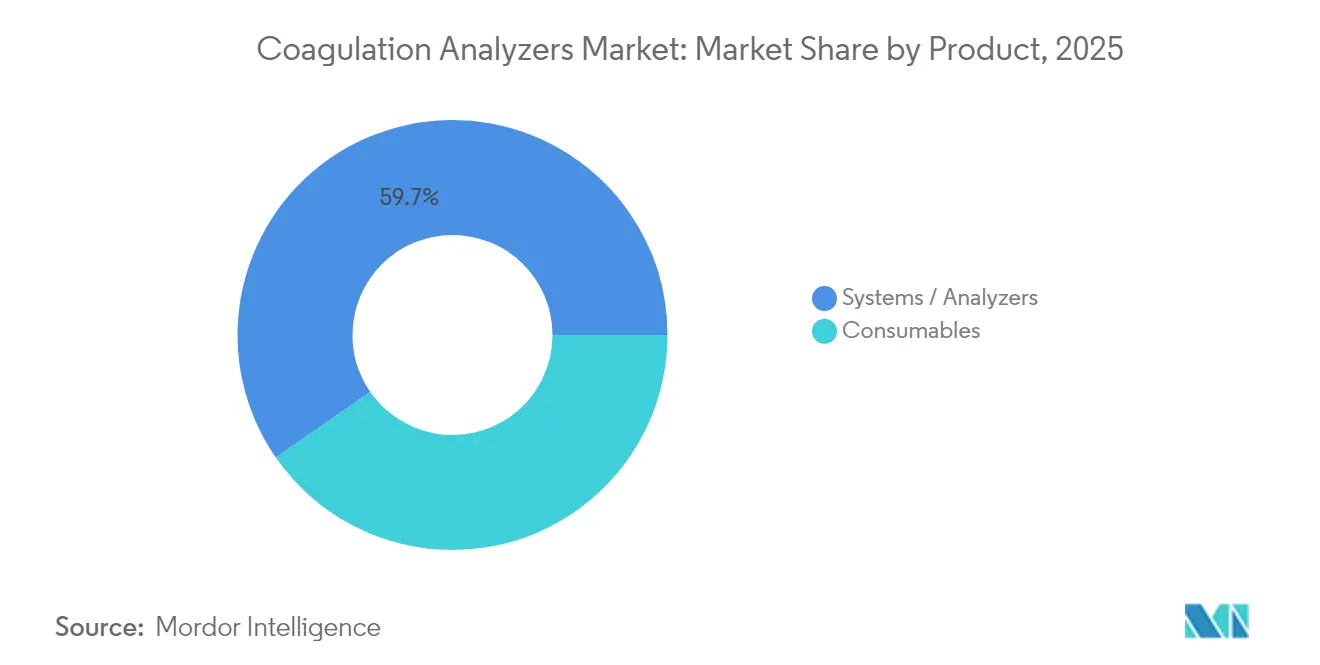

- By product, systems and analyzers led with 59.65% revenue share in 2025; point-of-care analyzers are projected to ramp up at an 11.05% CAGR to 2031.

- By test type, PT/INR accounted for 30.25% of the coagulation analyzers market size in 2025, while D-Dimer assays are on course for a 11.95% CAGR through 2031.

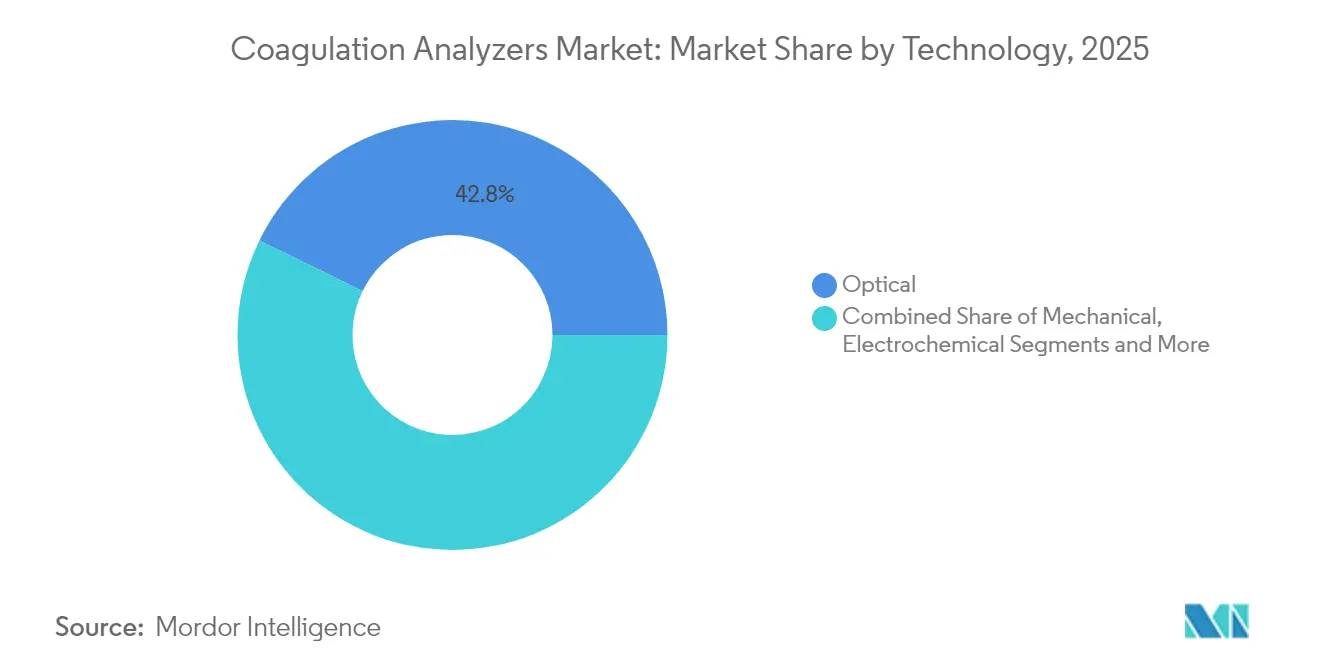

- By technology, optical methods held 42.75% of the coagulation analyzers market share in 2025; viscoelastic/magnetic technologies are forecast to rise at 13.65% CAGR between 2026 and 2031.

- By modality, hospital-based central laboratories captured 53.90% share of the coagulation analyzers market size in 2025; point-of-care devices are poised for a 15.1% CAGR through 2031.

- By geography, North America led with a 43.10% share of the coagulation analyzers market in 2025, while Asia-Pacific is set to register the fastest growth at an 15.35% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coagulation Analyzers Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of bleeding & thrombotic disorders | +1.80% | Global, higher in aging populations | Long term (≥ 4 years) |

| Aging population & chronic-disease burden | +1.50% | Developed markets | Long term (≥ 4 years) |

| Laboratory automation & high-throughput analyzers | +1.20% | North America & Europe | Medium term (2–4 years) |

| Rise of point-of-care clotting tests | +1.00% | Emergency and surgical settings worldwide | Medium term (2–4 years) |

| Rapid uptake of viscoelastic testing | +0.80% | North America & Europe | Short term (≤ 2 years) |

| AI-driven, patient-specific algorithms | +0.60% | Early adoption in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Bleeding & Thrombotic Disorders

Hemophilia affects 273,000 diagnosed individuals, with an additional 563,000 likely undiagnosed, elevating demand for precise coagulation monitoring.[1]James O’Donnell, “Global Hemophilia Burden,” frontiersin.orgVon Willebrand disease remains the most common hereditary bleeding disorder, and 72–94% of patients experience clinical bleeding episodes that benefit from rapid laboratory confirmation. New therapies such as fitusiran, cleared by the FDA in March 2025, require antithrombin assays, further broadening the coagulation analyzers market.

Ageing Population & Chronic-Disease Burden

Surging atrial fibrillation prevalence in seniors heightens long-term anticoagulation needs. Thromboelastography demonstrates superior bleed-prediction accuracy versus conventional tests in elderly cohorts. Direct oral anticoagulant uptake, led by apixaban, underlines a market pivot toward newer drugs that still warrant episodic coagulation checks.[2]Wei Zhang, “Carbon-Nanotube Fluorescent Clot Sensor,” mdpi.com

Laboratory Automation & High-Throughput Analyzers

Platforms such as Sysmex CS-5100 process up to 402 tests per hour with ≤3% CV, meeting hospitals’ drive for turnaround time under 60 minutes. Siemens’ Atellica COAG 360 posts 98% operator satisfaction, highlighting usability gains vital for the coagulation analyzers market.

Rise of Point-of-Care Clotting Tests

Handheld INR meters deliver lab-equivalent accuracy, fostering home-based therapy adjustment and unclogging outpatient clinics.[3]Kenneth Uhl, “Handheld INR Accuracy,” mayoclinicproceedings.org The April 2024 TEG 6s HN cartridge brings viscoelastic insight to heparinized cardiac cases, trimming transfusion rates

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & reagent costs | -1.20% | Emerging markets worldwide | Medium term (2–4 years) |

| Limited adoption in low-income nations | -0.80% | Sub-Saharan Africa & parts of Asia | Long term (≥ 4 years) |

| Reagent-supply shocks from porcine heparin & IVDR | -0.60% | Global supply chains | Short term (≤ 2 years) |

| Emerging non-invasive biomarkers | -0.40% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Automation Drives Systems Dominance

Systems and analyzers held a 59.65% share of the coagulation analyzers market in 2025 as laboratories prioritized walk-away automation to control rising test volumes without adding staff. Point-of-care units posted the quickest uptake, supported by the TEG 6s clearance that expanded viscoelastic testing into cardiac theaters. Robust throughput-402 tests per hour on high-end models-reduces bottlenecks during morning phlebotomy peaks, cementing vendor lock-in through consumable contracts.

Consumables form the recurring backbone of the coagulation analyzers market. Reagent integrity demands have sharpened since porcine-heparin contamination alerts triggered global recalls. In response, OEM alliances such as the 2024 Siemens-Sysmex pact guarantee steady reagent pipelines and forward-integration of AI-enabled QC packs. Calibration materials also benefit from stricter CLIA precision goals, nudging laboratories toward premium controls with validated lot-to-lot consistency.

By Test Type: D-Dimer Surges Amid Thrombosis Focus

PT/INR continues to anchor chronic warfarin surveillance, capturing 30.25% of coagulation analyzers market size in 2025. Nonetheless, clinicians increasingly prefer anti-Xa assays for low-molecular-weight heparin, reflecting therapy migration. D-Dimer, meanwhile, is posting the fastest 11.95% CAGR as emergency departments rely on it to triage venous thromboembolism and monitor post-COVID coagulopathy.

Fibrinogen and platelet-function panels round out the catalog, supporting trauma protocols and antiplatelet agent adjustment. Global hemostasis applications-TEG and ROTEM-are expanding beyond operating theaters into intensive-care settings, fueled by the May 2025 Class II reclassification that trimmed time-to-market for new cartridges.

By Technology: Viscoelastic Methods Challenge Optical Dominance

Optical analyzers retained a 42.75% coagulation analyzers market share in 2025 thanks to deep installed bases and mature QC frameworks. Even so, viscoelastic and magnetic modalities are scheduled for a 13.65% CAGR as perioperative teams seek whole-blood insight that standard photometric curves cannot provide. Portable viscoelastic units now fit on anesthesia carts, tightening feedback loops during liver resections.

Electrochemical chips and smartphone-linked optical sensors are moving from proof-of-concept to pilot deployments in outpatient anticoagulation clinics. Researchers report successful clot-time tracking via carbon-nanotube fluorescence, hinting at low-cost disposables that could open the coagulation analyzers market to community pharmacies.

By Modality: Point-of-Care Gains Ground

Central laboratories still dominate hospital contracts because they deliver broad menus and bulk reagent discounts. Yet point-of-care models logged a 15.1% CAGR as caregivers push testing to bedsides for trauma, transplant, and obstetric cases, where 10-minute answers alter surgical decisions.

Home-care self-testing represents the next frontier. Pocket INR meters paired with cloud dashboards show stable time-in-therapeutic range and fewer clinic visits, aligning with payer incentives for remote management. However, reimbursement clarity and operator-training thresholds vary, limiting near-term rollouts outside high-income countries.

By End User: Home-Care Emerges as Growth Leader

Hospitals accounted for 53.90% of revenue in 2025, reflecting comprehensive in-house need across emergency, surgery, and specialized coagulation clinics. Clinical reference labs handle esoteric factor analyses and genetic panels that smaller hospitals outsource.

Home-care lines, projected to grow 15.1% annually, benefit from population aging and digital literacy improvements. Wearable biosensors under development promise continuous coagulation trendlines rather than spot checks, potentially shrinking readmission risk in heart-failure patients receiving dual antithrombotic therapy.

Geography Analysis

North America leads the coagulation analyzers market, supported by well-funded hospitals, rapid AI adoption, and favorable reimbursement frameworks. The March 2025 FDA approval of fitusiran with a companion antithrombin assay illustrates how therapeutic innovation immediately triggers diagnostic demand. Canada’s single-payer model drives nationwide INR management networks, while Mexico’s emerging private hospital chains are investing in point-of-care devices to shorten emergency room stay times.

Asia Pacific is the fastest-advancing region, reflecting swift infrastructure upgrades and growing senior populations that require routine coagulation surveillance. China’s role as the world’s largest heparin supplier offers cost advantages but also vulnerability to raw-material shocks. Japan’s stringent device review process ensures high laboratory standards, whereas recent regulatory reforms in India have opened pathways for domestic manufacturing of mid-throughput analyzers. Sysmex reported double-digit regional sales growth in Q1 2025, underscoring unmet demand for reagents and controls.

Europe balances strong scientific capability with the added burden of IVDR compliance. Germany, France, and the United Kingdom operate expansive reference-lab networks that already meet most new documentation mandates, but smaller centers face costly validation work. Supply concerns around porcine-derived reagents have sparked pilot studies into bovine alternatives, while NHS blood shortage episodes in England spotlight the importance of viscoelastic testing for judicious transfusion practice.

Regulatory Landscape

Coagulation analyzers are regulated as in vitro diagnostic medical devices, with market access shaped by U.S. FDA premarket requirements and the European Union IVDR framework. In the United States, automated and semi-automated systems used for in vitro coagulation studies fall under FDA oversight and generally follow the 510(k) premarket notification pathway, with increasing scrutiny on device software functions as connectivity, middleware, and algorithmic decision support become embedded in hemostasis workflows.

In Europe, Regulation (EU) 2017/746 (IVDR), as amended by (EU) 2024/1860, continues to raise documentation and Notified Body expectations for coagulation testing systems and associated assays. Key 2026 milestones tighten execution timelines: May 26, 2026 is a deadline for manufacturers of legacy Class C IVDs to lodge formal conformity assessment applications with a Notified Body to retain eligibility for extended transition provisions, and September 26, 2026 requires a signed written agreement with a Notified Body for those legacy Class C devices. EUDAMED onboarding also adds an additional compliance layer, with mandatory use for new IVD devices starting May 28, 2026, affecting registrations and post-market data flows for newly placed hemostasis products.

Competitive Landscape

The coagulation analyzers market exhibits moderate consolidation: the top five vendors control an estimated two-thirds of global revenue, yet technological churn allows nimble entrants to secure niche footholds. Siemens Healthineers and Sysmex extend a 25-year alliance through a fresh OEM deal that bundles instruments and reagents under shared service contracts. Roche strengthens its high-throughput position with Factor Xa tests tailored to direct oral anticoagulant monitoring.

Werfen deepened its point-of-care reach by acquiring Accriva Diagnostics, gaining Hemochron and VerifyNow to complement its laboratory GEM line. Haemonetics focuses on viscoelastic leadership, adding heparin-neutralized cartridges to cover cardiovascular surgeries. Across the tier-two scene, start-ups leverage AI to convert raw clot curves into predictive bleed-risk scores, pitching cloud APIs that fit alongside legacy LIS systems.

Competitive pressure is likely to intensify as pharmaceutical firms seek companion diagnostics synchronized with next-generation anticoagulants. The May 2025 easing of U.S. regulatory classification for viscoelastic systems also lowers capital hurdles for local manufacturers, potentially fragmenting share in price-sensitive segments.

Coagulation Analyzers Industry Leaders

F. Hoffmann-La Roche Ltd

Siemens Healthineers AG

Sysmex Corporation

Beckman Coulter (Danaher)

Werfen (Instrumentation Laboratory)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Laboratories are using the current IVDR-driven compliance workload and staffing constraints to justify modernization toward higher-throughput, more automated hemostasis platforms with tighter QC and improved data-management integration. A tangible proof point in the report context is the March 2026 completion of the first UK installation of Diagnostica Stago's sthemO 301 at the Royal Sussex County Hospital (Brighton), which reflects ongoing procurement by medium-to-large labs looking to consolidate test menus and improve workflow. This supports a clear demand for vendors that bundle instruments, reagents, and informatics together, including connectivity layers that support multi-site standardization and audit-ready documentation aligned with ISO 15189 laboratory accreditation practices.

Decentralized coagulation testing also remains an open avenue where hospitals and outpatient pathways push results closer to clinical decision points, particularly in emergency and perioperative settings where minutes matter. The segment shift toward viscoelastic testing and point-of-care modalities in the report context aligns with demand for cartridge-based platforms, heparin-neutralized applications in cardiac surgery, and remote anticoagulation management programs that link home INR self-testing to cloud dashboards. In parallel, the expansion of companion diagnostics for newer hemophilia and anticoagulation therapies broadens the need for specific assays, including antithrombin testing linked to fitusiran use, which in turn supports differentiated reagent portfolios and analyzer menus spanning routine PT/INR and specialized factor and inhibitor monitoring.

Recent Industry Developments

- July 2026: Siemens Healthineers launched the CN-3000 and CN-6000 hemostasis systems in Canada following Health Canada licensing. The launch expands access to automated coagulation workflows in a major North American market and supports instrument standardization across sites that already rely on integrated lab automation and service contracts.

- March 2026: Roche launched the cobas MPX-E assay for blood donor screening in CE mark-accepting countries. While positioned for transfusion safety, the launch reinforces a broader trend of expanding assay portfolios on automated platforms, which influences purchasing decisions in labs that consolidate hemostasis and related testing under shared instrumentation and QC regimes.

- April 2024: Siemens Healthineers and Sysmex commenced independent distribution of their combined hemostasis testing portfolio under their respective brand names in the United States and Europe. This shift reshaped go-to-market execution for instruments and reagents, giving each company tighter control over service, supply continuity, and portfolio roadmaps in two of the largest regulated geographies for coagulation testing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers instruments used to run clinical coagulation testing and monitoring, along with the consumables that enable those tests in routine care and emergency workflows.

Scope exclusions: It excludes veterinary-use devices, complete-blood-count instruments that do not perform coagulation testing, and reagent-rental arrangements where instrument revenue is not separately recognized.

Segmentation Overview

- By Product

- Systems / Analyzers

- High-throughput Lab Analyzers

- Mid-throughput Lab Analyzers

- Point-of-Care Analyzers

- Consumables

- Reagents & Assays

- Calibrators & Controls

- Others

- Systems / Analyzers

- By Test Type

- Prothrombin Time (PT/INR)

- Activated Partial Thromboplastin Time (aPTT)

- D-Dimer

- Fibrinogen

- Platelet Function

- Anti-Factor Xa

- Global Hemostasis (TEG/ROTEM)

- Other Tests

- By Technology

- Optical

- Mechanical

- Electrochemical

- Magnetic / Viscoelastic

- Other Technologies

- By Modality

- Central-Laboratory Platforms

- Point-of-Care Devices

- Self-Testing / Home-care Devices

- By End User

- Hospitals

- Clinical & Reference Laboratories

- Ambulatory Surgical Centers

- Home-care Settings

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public healthcare and diagnostics signals that help us anchor demand and adoption. We use sources such as the World Health Organization for disease burden context, the US FDA device databases for product clearances and device categories, and the US Centers for Medicare and Medicaid Services for reimbursement and test-setting clues. Trade and procurement indicators are also checked using sources such as UN Comtrade, plus relevant public health agency dashboards where laboratory capacity trends are discussed.

To connect these signals to revenue, we review manufacturer annual reports and investor presentations, peer-reviewed lab medicine journals, and association publications that describe coagulation testing practices. A paid subscription for company financials and intelligence is used to standardize revenue mapping where disclosures are inconsistent, and a patent database is used to spot technology shifts that can influence ASP paths. The sources listed here are illustrative and not exhaustive, and many other public references were used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions with people who see purchasing and utilization closely, including laboratory managers, hospital procurement teams, independent clinical labs, and distributors that manage instrument placements and consumables pull-through. For a global view, we balance inputs across mature and emerging markets so that reimbursement, test mix, and installed-base replacement cycles are not over-generalized. When a data point moved the model materially, we re-checked it with a second respondent type before locking it in.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 46% |

| Mid tier: 59% | Functional/Unit leaders: 43% | EMEA: 33% |

| Smaller Players: 14% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Market totals are constructed using a top-down build that links the addressable testing pool to adoption and spend patterns, and then converts that into annual instrument and consumables value. The demand pool is shaped using indicators such as coagulation test volumes in core panels (PT/INR and aPTT as routine anchors), the split of centralized lab testing versus point-of-care use, the installed base and replacement timing in hospitals and independent labs, and reagent utilization per active analyzer. Pricing assumptions are kept practical by tracking typical analyzer ASP bands, service coverage rates, and reagent price progression by region.

After the top-down build is complete, we corroborate totals using selective bottom-up approximations, such as roll-ups of sampled supplier revenues where available, channel checks on placement volumes, and sanity checks using average consumables spend per installed analyzer. Gaps are handled by using proxy ratios from similar end users in the same region (for example, independent labs versus hospitals) and then adjusting those ratios based on interview feedback.

For forecasting, scenario analysis is used so the model can reflect how reimbursement shifts, decentralization toward point-of-care, and instrument automation upgrades might move utilization and ASPs differently by region. The final growth path is aligned to what respondents expect for replacement activity, test mix changes, and procurement timing, rather than relying on a single straight-line trend.

Data Validation & Update Cycle

Validation happens in steps so the numbers stay explainable and stable. We check the model output against independent signals like instrument placement momentum, consumables pull-through logic, and regional healthcare spending direction, and then we review any sharp jumps that do not match those signals. If a variance is driven by one assumption, it is flagged and either re-estimated or taken back to a respondent for confirmation.

Before sign-off, the work is reviewed by another analyst to confirm arithmetic, scope alignment, and the reasonableness of key inputs. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or notable pricing shifts. Right before delivery, a final pass is completed so clients receive the most up-to-date view available at that time.

Mordor Intelligence's Coagulation Analyzers Market Size Compared With Other Published Estimates

Published market sizes for coagulation analyzers can differ even when they describe a similar product set, and it usually comes down to what is counted and how revenue is timed. The starting year, the treatment of consumables and service revenue, and how point-of-care testing is blended with core lab analyzers can all move the total by a meaningful amount.

In practice, the biggest gaps typically come from whether estimates lean more on shipment-style assumptions versus installed-base utilization, plus how aggressively pricing is assumed to rise for reagents over time. Currency conversion timing also matters because a large share of sales occurs outside the United States, and some publishers retain older FX rates while others refresh them. Another driver is refresh cadence, since new hospital procurement cycles and tenders can shift placements quickly, which then changes the consumables pull-through that follows. This is handled after separating instrument revenue from recurring reagent demand in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.75 B (2026) | |

| Global Consultancy A | USD 4.72 B (2024) | Uses a different base year and may smooth the transition between historical and forecast periods, which can lower the implied current value when pricing and utilization are not refreshed at the same cadence. |

| Industry Publisher B | USD 4.60 B (2024) | Often leans on a broader diagnostics framing and segment averages, which can understate recurring consumables pull-through when installed-base utilization and test mix are not explicitly modeled by setting. |

The spread in the table is mostly explained by base-year choice and by how recurring reagent demand is translated from real-world utilization. When scope is kept consistent and key drivers are tied back to installed base, test volumes, and practical ASP bands, the resulting market value is easier to trace and repeat in future updates.

Key Questions Answered in the Report

What is the current size and growth outlook for the global coagulation analyzers market?

The market is valued at USD 4.75 billion in 2026 and is projected to reach USD 6.31 billion by 2031, reflecting a 5.85% CAGR.

Which product category is expanding the quickest?

Point-of-care analyzers are growing at an 11.05% CAGR as hospitals and emergency units prioritize bedside coagulation results.

Why is viscoelastic testing (TEG/ROTEM) gaining rapid adoption?

These platforms deliver real-time, whole-blood clotting profiles within minutes, improving transfusion decisions and benefiting from a May 2025 Class II re-classification that lowered regulatory hurdles.

Which geographic region is forecast to grow the fastest?

Asia Pacific leads with a 15.35% CAGR due to aging populations, infrastructure upgrades, and rising chronic-disease burdens.

Page last updated on: