Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.38 Billion |

| Market Size (2031) | USD 33.59 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

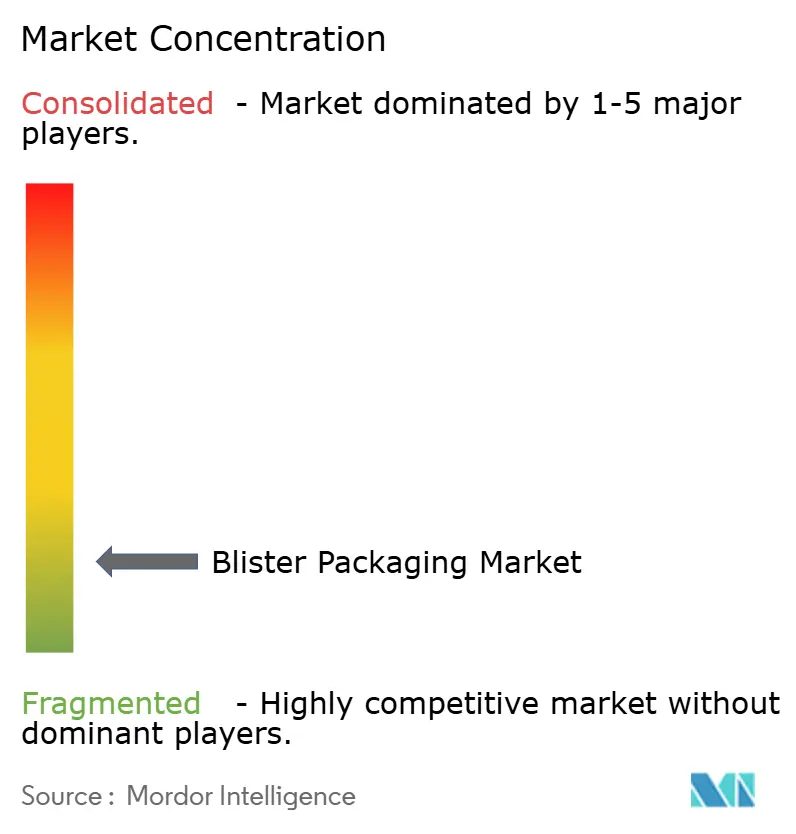

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blister Packaging Market Analysis by Mordor Intelligence

The blister packaging market size was valued at USD 26.28 billion in 2025 and estimated to grow from USD 27.38 billion in 2026 to reach USD 33.59 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031). Robust demand from prescription drugs, over-the-counter medications, and increasingly complex biologics underpins this growth, while unit-dose formats continue to displace bulk bottles across hospital, long-term-care, and retail channels. Regulatory pressure—most notably the European Union’s Regulation 2025/40 mandating full recyclability by 2030 and the U.S. FDA’s strengthened tamper-evident rules—has sparked a wave of compliance-driven innovation that commands premium pricing and protects margins even as raw-material costs fluctuate.[1]European Commission, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” eur-lex.europa.eu Asia-Pacific leads global demand thanks to China and India’s manufacturing scale, while North America and Europe shape high-value niches through serialization, smart packs, and sustainability upgrades. Meanwhile, industry consolidation—typified by Amcor’s USD 8.43 billion purchase of Berry Global—signals a pivot toward integrated flexible, rigid, and intelligent solutions that can serve multinational pharmaceutical clients.

Key Report Takeaways

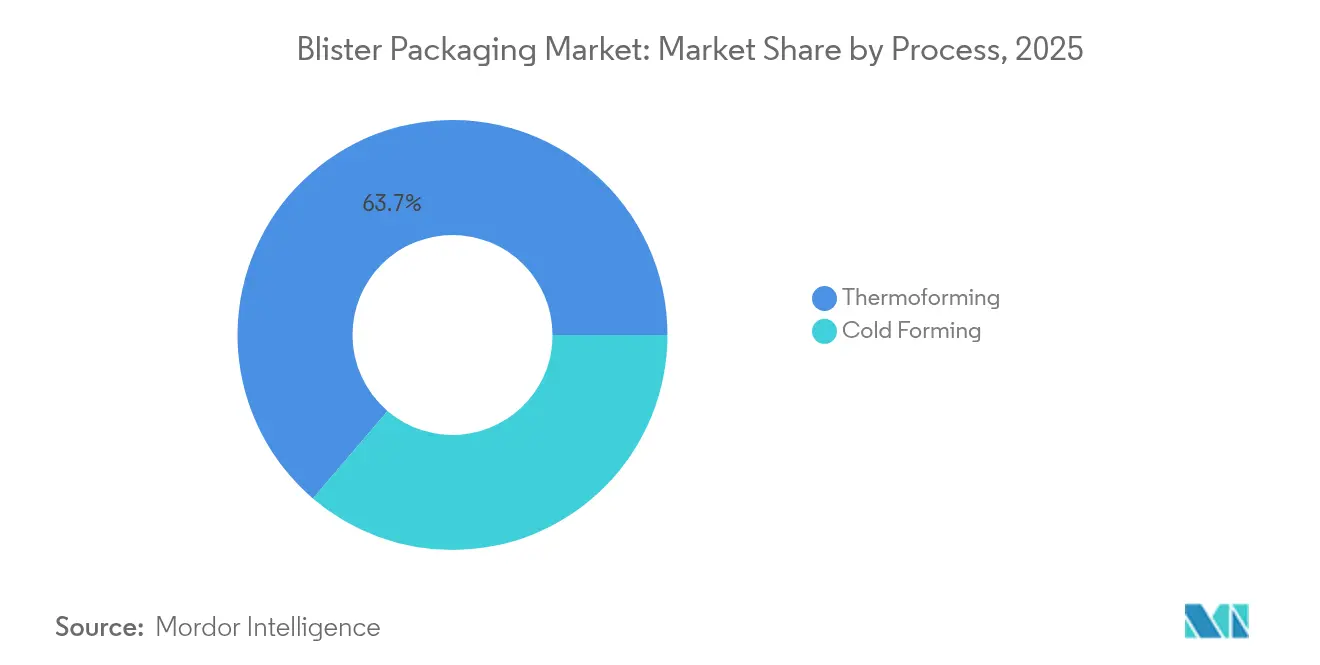

- By process, thermoforming led with 63.75% of the blister packaging market share in 2025 and is progressing at a 5.54% CAGR through 2031.

- By material, plastic films held 67.52% revenue share in 2025, while paper and paperboard are expanding fastest at 7.02% CAGR to 2031.

- By product type, carded/face-seal blisters captured 51.78% revenue in 2025; clamshell formats post the strongest outlook at 7.68% CAGR through 2031.

- By end-user industry, pharmaceuticals commanded 57.62% share of the blister packaging market size in 2025, whereas nutraceuticals are forecast to grow at 7.55% CAGR to 2031.

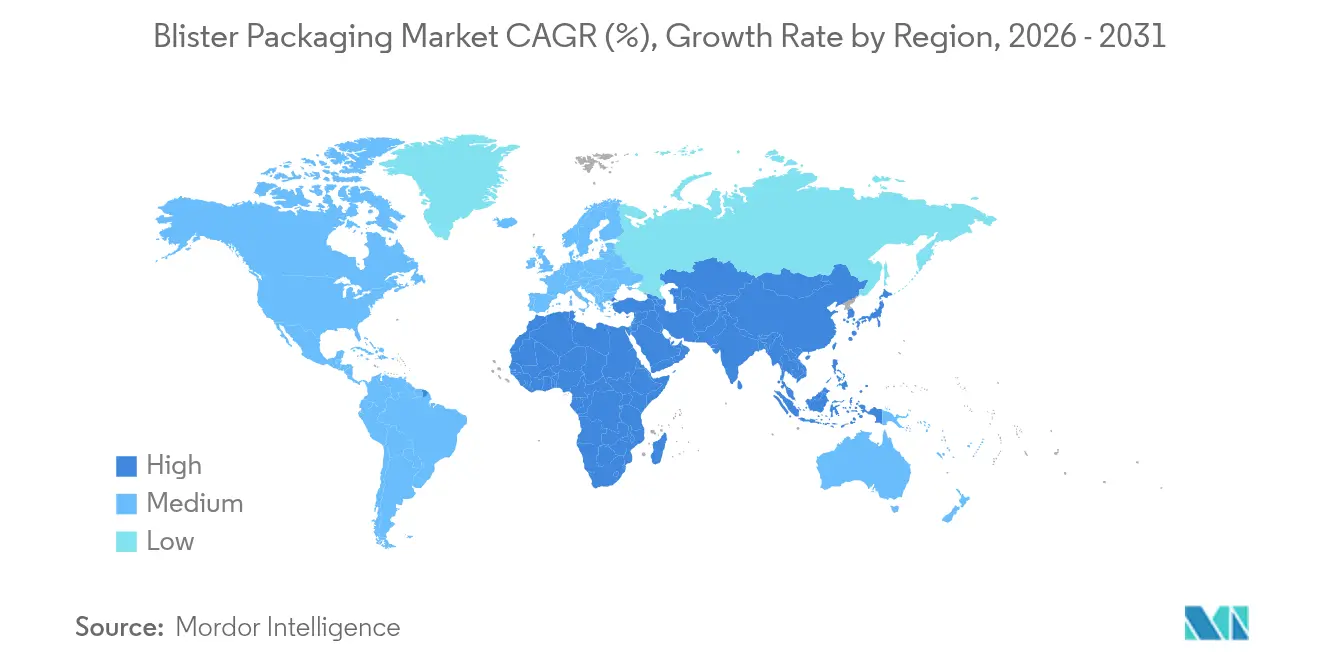

- By geography, Asia-Pacific dominated with 40.95% share in 2025; the region is advancing at 7.29% CAGR, the fastest globally.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blister Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing geriatric population & chronic diseases | +1.2% | Global; North America & Europe concentrated | Long term (≥ 4 years) |

| Rising demand for unit-dose adherence packs | +0.8% | Global; strongest in developed markets | Medium term (2-4 years) |

| Regulatory push for tamper-evident formats | +0.6% | North America & EU; APAC catching up | Short term (≤ 2 years) |

| Smart packs with NFC/QR for track-and-trace | +0.4% | EU & North America first; global roll-out | Medium term (2-4 years) |

| Personalized-medicine small-batch blister lines | +0.3% | North America & EU core | Long term (≥ 4 years) |

| PVC-to-PE retrofits driven by sustainability targets | +0.2% | EU leading; global adoption follows | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Population and Chronic-Disease Prevalence

The global cohort aged 60 and above will surge 56% by 2030, intensifying demand for user-friendly blister packs that improve medication adherence while offering tamper evidence. Senior-centric designs—larger print, color coding, and low opening force—are being commercialized by converters such as Drug Plastics Group, whose Pop & Click closure reduces required hand pressure by roughly a quarter. Chronic conditions like diabetes and cardiovascular disease further amplify multi-dose pack adoption, enabling clear visual cues for complex regimes and reinforcing premium price realization for blister specialists.

Demand for Unit-Dose and Patient-Adherence Packs

Hospitals, pharmacies, and home-health providers increasingly link reimbursement to adherence metrics, elevating the role of blister-based unit-dose packs. Automated equipment from Parata now integrates directly with electronic health-record platforms, cutting dispensing errors while simplifying repack operations. The FDA’s proposal to require single-unit containers for orally disintegrating OTC forms underscores regulatory endorsement of unit-dose safety benefits.[2]U.S. Federal Register, “Proposed Rule on Single-Unit Containers for OTC Drugs,” federalregister.gov Pharmaceutical brands also leverage unit-dose blisters for differentiation, combining brand visibility with tamper-evidence that bottles cannot replicate.

Regulatory Push for Tamper-Evident Formats

U.S. 21 CFR 211.132 obliges OTC drugs to integrate overt tamper-evident features, while Europe’s Falsified Medicines Directive mandates unique identifiers and anti-tamper devices on prescription packs. These overlapping frameworks favor blister formats that pair mechanical indicators with serialization, enabling cross-border compliance and reducing counterfeit risk for high-value therapies.

Smart Blister Packs with NFC/QR for Track-and-Trace

Embedding NFC chips or QR codes turns everyday blisters into data-rich assets. Schreiner Group’s NFC labels allow patients to confirm authenticity and log usage with a tap of a smartphone. Aardex Group’s electronics record time-stamped dose events, permitting healthcare teams to intervene promptly when adherence deviations surface. The approach dovetails with the U.S. Drug Supply Chain Security Act and EU mandates for serialized medicines, giving early adopters a compliance-plus-engagement edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile PVC & aluminium prices | -0.9% | Global; especially import-dependent markets | Short term (≤ 2 years) |

| Tightening PVC disposal/recycling rules | -0.7% | EU leads; North America follows | Medium term (2-4 years) |

| PVDC resin supply bottlenecks | -0.4% | Global; specialty niches | Short term (≤ 2 years) |

| OTC stick-pack & sachet substitution | -0.3% | Global; fastest in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile PVC and Aluminium Prices

China’s jump in PVC import tariffs from 1% to 5.5% in 2025 lifted resin costs for downstream converters, spotlighting vulnerability to policy shifts. Indian converters remain exposed since 60% of their PVC feedstock is sourced abroad, making hedging and backward integration central to risk management. Aluminium foil prices also swing with energy markets, straining smaller blister firms that lack the scale to lock in multi-year contracts.

Tightening PVC Disposal/Recycling Legislation

The EU’s Packaging and Packaging Waste Regulation defines recyclability requirements for all formats by 2030, and discussions on classifying PVC as hazardous waste in the U.S. could raise disposal costs dramatically. In response, leaders such as TekniPlex are commercializing blister films with 30% post-consumer recyclate, balancing barrier performance with circular-economy targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process: Thermoforming Dominance Faces Cold-Form Innovation

Thermoforming commanded 63.75% of global revenues in 2025 and will grow 5.54% a year as drug makers favor its low tooling cost, fast line speeds, and compatibility with diverse film substrates. Brown Machine’s Quad-Series thermoformers now deliver up to 250,000 lids per hour while trimming energy use by roughly one-quarter, giving contract packers productivity gains that sustain the blister packaging market’s momentum. Smaller laboratories gain access through modular machines introduced by GEA, broadening supplier bases beyond large multinationals.

Cold-form foil, though a minority share, is indispensable for moisture- or light-sensitive molecules. Drug makers often specify aluminium-aluminium structures when stability studies demand near-zero water vapor transmission. As biologics and high-potency actives proliferate, cold form’s installed base expands, intensifying R&D into thinner foils and hybrid lamination that cut weight without compromising barrier. Together, these advances widen the technology palette, reinforcing the blister packaging market as a versatile platform for both mass-production generics and niche specialty drugs.

By Material: Plastic Films Lead While Paper Gains Sustainability Momentum

Plastic films, led by PVC, PET, and PP, accounted for 67.52% of blister revenues in 2025 thanks to mature supply chains and easy thermoformability. Yet heightened scrutiny of fossil-based materials is spurring rapid incremental gains for paper-based solutions, which log a 7.02% CAGR through 2031. TekniPlex now offers transparent recyclable mid-barrier PET blisters containing 30% recycled content, illustrating how converters preserve pharmacopoeial compliance while advancing circularity.

Paperboard entrants such as Rohrer’s EcoVolve-30 use fiber plus functional coatings to withstand line forming temperatures and protect moisture-tolerant tablets. Although moisture sensitivity limits broad substitution, brand owners deploy paper variants in vitamins, nutraceuticals, and short shelf-life SKUs, bolstering eco-credentials. Over time, material science breakthroughs are expected to let hybrid fiber-polymer laminates secure higher-barrier categories, reinforcing the blister packaging market size trajectory and aligning with regulatory recycled-content mandates.

By Product Type: Carded Blisters Dominate as Clamshells Surge

Carded or face-seal formats held 51.78% of 2025 revenue owing to cost-efficient inline carding and broad acceptance across prescription and OTC drugs. Their design simplicity keeps tooling budgets modest, benefiting generic manufacturers competing on unit economics. The blister packaging market continues to rely on carded solutions for high-volume SKUs where shelf visibility and tamper evidence suffice.

Clamshell packs, the fastest-expanding product type at an 7.68% CAGR, blend premium feel with robust mechanical protection, gaining traction for nutraceuticals, medical devices, and combination kits. Converters integrate child-resistance and senior-friendliness using next-generation mechanisms such as Fresh-Lock’s push-and-turn Child-Guard closure, which satisfies U.S. Consumer Product Safety Commission protocols while reducing opening torque for elderly users. Continuous refinement of full-card and trapped-blister designs offers brand teams heightened security against pilferage and counterfeiting, reinforcing the blister packaging market’s versatility.

By End-User Industry: Pharmaceuticals Lead While Nutraceuticals Accelerate

Pharmaceutical companies consumed 57.62% of global blister output in 2025, a testament to regulatory preference for tamper-evident, unit-dose formats that fit electronic pedigree and patient-adherence programs. Personalized-medicine pathways now drive capital investment in small-batch blister lines capable of frequent changeovers without yield loss, extending the blister packaging industry into oncology and orphan-drug niches where run sizes are measured in thousands rather than millions.

Nutraceuticals, posting a 7.55% CAGR to 2031, benefit from consumer interest in preventive health and premium delivery. Moisture-sensitive probiotics and omega-3 capsules move from bulk bottles into aluminium-aluminium blisters, commanding higher retail price points while reassuring consumers about product integrity. Beyond healthcare, electronics, personal-care, and hardware retain steady demand for barrier properties and hang-tab retail merchandising. Such diversity cushions the blister packaging market against cyclical swings in any single sector and supports long-term revenue visibility.

Geography Analysis

Asia-Pacific led with 40.95% of 2025 revenue and will outpace all regions at 7.29% CAGR as China and India scale active-pharmaceutical-ingredient output and align with Western quality standards. WuXi STA’s new Taixing API site and proposed Singapore expansion exemplify regional manufacturing build-out, directly lifting local demand for compliant blister lines. China’s tariff hike on imported PVC to 5.5% further encourages domestic film extrusion, reinforcing supply-chain localization that underpins the blister packaging market in East Asia.

North America remains a technological bellwether. Stringent FDA serialization plus tamper-evidence rules sustain premium margins for intelligent formats, while machinery capex expands in anticipation of biologic fill-finish demand. PMMI projects packaging-machinery sales will hit record highs by 2027, with pharmaceutical applications outperforming food and beverage. Amcor’s Berry Global acquisition consolidates flexible and rigid capabilities inside a single platform, ensuring scale and vertical reach that smaller North American converters will find hard to match.

Europe confronts the most aggressive sustainability legislation. Regulation 2025/40 enforces recyclability and 30% recycled content in PET packs by 2030, directing investment into circular-ready designs. TekniPlex’s showcase of transparent recyclable mid-barrier blisters demonstrates compliance pathways that still satisfy stringent EMA barrier specifications. Clinical-trial packs also adapt to EU 536/2014, prompting Catalent to equip its Shiga, Japan, site with high-speed blister lines that serve pan-regional studies and underscore the global nature of compliance-driven demand. Consequently, the blister packaging market share in Europe remains resilient even as material choices evolve.

Competitive Landscape

The blister packaging market sits in the mid-range of concentration. Top players—Amcor, Constantia Flexibles, WestRock, and select regional specialists—collectively control an estimated two-thirds of global pharmaceutical blister capacity. Consolidation is accelerating: Amcor’s USD 8.43 billion purchase of Berry Global cements a healthcare-focused powerhouse that targets USD 650 million in cost synergies within three years. Meanwhile, Nutra-Med’s acquisition of Legacy Pharma Solutions equips the nutraceutical co-packer with high-speed blistering to address dietary-supplement growth.

Technology differentiation drives competitive edge. Pharmaworks’ TF1e blister machine caters to mid-volume drug makers seeking GMP compliance without the footprint of legacy lines. Ecobliss Pharma’s cold-seal technology lowers energy consumption, aligning with decarbonization targets while preserving high-barrier protection. Patent filings on single-piece re-closable unit packs reveal sustained R&D investment into user-friendly, adherence-boosting formats. As sustainability and digital traceability become table stakes, innovators capable of integrating post-consumer recycled content with embedded electronics are positioned to outpace conventional rivals.

Smaller converters focus on niche strengths—specialty films, rapid-changeover lines, or country-specific compliance expertise—to capture high-margin contracts that global majors overlook. Strategic partnerships between machinery OEMs and material suppliers further erode barriers for mid-tier entrants, keeping the blister packaging industry dynamic despite headline consolidation.

Blister Packaging Industry Leaders

Klockner Pentaplast Group

Amcor PLC

Constantia Flexibles GmbH

Honeywell International Inc.

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Amcor completed its USD 8.43 billion acquisition of Berry Global, targeting USD 650 million in synergies over three years.

- January 2025: TekniPlex Healthcare unveiled blister films with 30% post-consumer recyclate plus the first transparent recyclable mid-barrier pack at Pharmapack Europe.

- January 2025: The EU enacted Regulation 2025/40, mandating full recyclability of all packaging by 2030 with recycled-content thresholds for PET.

- January 2025: China raised PVC import tariffs to 5.5%, reshaping resin supply for blister converters.

Global Blister Packaging Market Report Scope

Blister pack is a term for several types of pre-formed plastic packaging used for small consumer goods, foods, and for pharmaceuticals. These packaging solutions are useful for protecting products against external factors, such as humidity and contamination, for extended periods of time. Opaque blisters also protect light-sensitive products against UV rays. Such wide base of application has helped it gain traction in the market.

By Process

| Thermoforming |

| Cold Forming |

By Material

| Plastic Films (PVC, PET, PP, PE, rPET, COP, others) |

| Aluminium (ALU-ALU, PTP foil) |

| Paper and Paperboard |

By Product Type

| Carded / Face-Seal Blisters |

| Clamshell Blisters |

| Trapped and Full-Card Blisters |

| Child-Resistant / Senior-Friendly Packs |

By End-User Industry

| Pharmaceuticals |

| Nutraceuticals and Dietary Supplements |

| Consumer Electronics and Hardware |

| Personal Care and Cosmetics |

| Other End-user Industry |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Process | Thermoforming | ||

| Cold Forming | |||

| By Material | Plastic Films (PVC, PET, PP, PE, rPET, COP, others) | ||

| Aluminium (ALU-ALU, PTP foil) | |||

| Paper and Paperboard | |||

| By Product Type | Carded / Face-Seal Blisters | ||

| Clamshell Blisters | |||

| Trapped and Full-Card Blisters | |||

| Child-Resistant / Senior-Friendly Packs | |||

| By End-User Industry | Pharmaceuticals | ||

| Nutraceuticals and Dietary Supplements | |||

| Consumer Electronics and Hardware | |||

| Personal Care and Cosmetics | |||

| Other End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the blister packaging market in 2026?

The blister packaging market size is USD 27.38 billion in 2026 and is projected to reach USD 33.59 billion by 2031 at a 4.18% CAGR.

Which region is growing fastest in blister packaging?

Asia-Pacific leads growth with a 7.29% CAGR through 2031, driven by pharmaceutical production expansion in China and India.

What process dominates blister production?

Thermoforming holds 63.75% of global revenue and remains preferred for its cost-efficiency and high throughput.

How are sustainability regulations affecting materials?

EU Regulation 2025/40 mandates recyclability and recycled-content thresholds, accelerating the shift from PVC toward recyclable PET and paper-based structures.

Why are smart blister packs gaining traction?

NFC and QR-enabled blisters meet serialization laws and allow real-time adherence monitoring, improving patient outcomes and supply-chain visibility.

What impact do raw-material price swings have on converters?

Volatile PVC and aluminium costs can shave up to 0.9 percentage points off forecast CAGR, pressuring margins and hastening industry consolidation.

Page last updated on: